MAY 2012 MELBOURNE CBD Office Market Overview

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Vision for a Smaller Planet

INFASTRUCTURE Vision for a smaller planet Andrew Gray THE VPELATHE ARG Planning victorianrevue / planning / environmental / law / association / volume 95 June 2015 1 / VPELA Revue June 2015 Contents President 3 Awards 4 Minister 9 Shadow Minister 11 Seminar Reports The (new) residential zones – 1 year on 15 Meet the Minister 21 Coastal planning – where are we at? 54 Expert Evidence Seminar 57 Places Planning… Like an Egyptian 22 Melbourne School of Design 40 People 1950’s Rock n Roll Gala 28 A day with Prof. Rob Adams 38 Peter Allen’s brilliant career 56 The Business New members 59 VCAT Bias: real or perceived 7 In the know 59 Planning policy and government investment 10 Residential zones, reflecting one year on 13 The new residential zones one year in transition 17 The low down on tall towers in Melbourne 25 Apartment standards, more Maslow or more area 33 Infrastructure provision in growth areas 35 Municipal matters 42 Making better decisions in Australian cities 45 The fast lane 47 Permit Triggers…to tick or not to tick 48 Legal world 51 Rory’s ramble 53 Cover photo: The Hon Richard Wynne MLA, Minister for Planning presenting Geoff Underwood the Richard J Evans Award. Newsletter editor: VPELA Bernard McNamara PO Box 1291 Camberwell 3124 M: 0418 326 447 www.vpela.org.au E: [email protected] E: [email protected] T: 9699 7025 T: 9813 2801 2 / VPELA Revue June 2015 President Utopia and bipartisanship Tamara Brezzi President, VPELA Inevitably upon the coming and going of each election cycle, a arose not only from the ABC TV show of the same name, but from discussion about planning, and its system, turns to bipartisanship. -

MELBOURNE EDITION the Local Perspective on Prime Property and Lifestyle

The Wealth Report City Series MELBOURNE EDITION The local perspective on prime property and lifestyle THE WEALTH REPORT – MELBOURNE EDITION Welcome to the Melbourne Edition Andrew Hay Global Head of Residential [email protected] +44 20 7861 1071 Welcome to the Melbourne Edition of attractive to wealthy residents from The Wealth Report, Knight Frank’s annual across Australia, the wider Asia-Pacific Contents thought-leadership publication for our region and even further afield. UHNW clients and their advisors. The importance of Melbourne’s 01 It is particularly fitting that Melbourne economic mix and skilled employment Briefing should be the focus of our first special base in the context of future investment in In the 12 months to the end of city edition. Its reputation as one of the city-wide infrastructure is also discussed. December 2016, Melbourne prime world’s most exciting urban centres was Findings from previous editions of residential prices increased by underlined when it was named the world’s The Wealth Report have confirmed 8.8%, and grew by 35.1% over the most liveable city for the sixth that lifestyle is a critical issue driving past four years consecutive year in the latest rankings by investment into residential markets page 02 The Economist Intelligence Unit. globally. We consider place-making, This publication not only builds architecture, art, fashion, health, sport 02 on the research and insight Knight and the burgeoning food scene in Living Frank provides every year in The Wealth Melbourne to provide a rounded view From culture to countryside, Report, but also takes a deeper, more of the opportunities the city offers and employment to education, we look localised focus on the issues that that justify its world ranking. -

29 January 2007

14 December 2011 The Manager Company Announcements Office ASX Limited Exchange Centre 20 Bridge Street Sydney NSW 2000 Dear Sir/Madam, APN Development Fund No 2 secures Westpac as anchor tenant for 150 Collins Street APN Property Group Limited is pleased to announce that APN Development Fund No 2 and its joint venture partner, Grocon, have secured Westpac Banking Corporation as anchor tenant for its 150 Collins Street, Melbourne site. Details of the agreement are set out in the attached media release. Further information If you would like any further information in relation to this announcement, please contact Clive Appleton on +613 8656 1000. Yours sincerely John Freemantle Company Secretary For personal use only APN Property Group Limited About APN Property Group APN Property Group Limited (ASX code: APD) is one of Australia’s leading real estate investment managers, with a strong record of investment performance. We actively invest in, develop and manage real estate and real estate securities on behalf of corporations, superannuation funds, high net worth and individual investors. As a specialist real estate investment manager, we are committed to delivering superior investment performance and outstanding service. APN & Grocon secure Westpac as anchor tenant at 150 Collins St Wednesday, December 14, 2011 An Agreement of Lease has been signed by Australia’s first bank, Westpac Banking Corporation, as the anchor tenant for the APN /Grocon joint development at 150 Collins Street, Melbourne. 150 Collins Street, located between heritage landmarks Scots Church and The Assembly Hall, represents a new generation of building, blending the old and the new. The modern Peddle Thorpe designed office will integrate with the rich historical surrounds, making it the ideal new headquarters for Victorian based Westpac staff. -

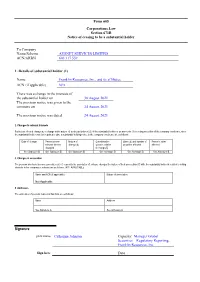

Notice of Change of Interests of Substantial Holder

Form 605 Corporations Law Section 671B Notice of ceasing to be a substantial holder To Company Name/Scheme AUSNET SERVICES LIMITED ACN/ARBN 603 317 559 1. Details of substantial holder (1) Name Franklin Resources, Inc., and its affiliates ACN (if applicable) N/A There was a change in the interests of the substantial holder on 30 August 2021 The previous notice was given to the company on 24 August 2021 The previous notice was dated 24 August 2021 2. Changes in relevant interests Particulars of each change in, or change in the nature of, a relevant interest (2) of the substantial holder or an associate (3) in voting securities of the company or scheme, since the substantial holder was last required to give a substantial holding notice to the company or scheme are as follows: Date of change Person whose Nature of Consideration Class (6) and number of Person’s votes relevant interest change (4) given in relation securities affected affected changed to change(5) See Annexure B See Annexure B See Annexure B See Annexure B See Annexure B See Annexure B 3. Changes in association The persons who have become associates (3) of, ceased to be associates of, or have changed the nature of their association (7) with, the substantial holder in relation to voting interests in the company or scheme are as follows: NOT APPLICABLE Name and ACN (if applicable) Nature of association Not Applicable 4. Addresses The addresses of persons named in this form are as follows: Name Address See Annexure A See Annexure A Signature print name Catherine Johnson Capacity: Manager Global Securities – Regulatory Reporting, Franklin Resources, Inc. -

Banking Act Unclaimed Money As at 31 December 2007

Commonwealth of Australia Gazette No. ASIC 40A/08, Wednesday, 21 May 2008 Published by ASIC ASIC Gazette Contents Banking Act Unclaimed Money as at 31 December 2007 RIGHTS OF REVIEW Persons affected by certain decisions made by ASIC under the Corporations Act 2001 and the other legislation administered by ASIC may have rights of review. ASIC has published Regulatory Guide 57 Notification of rights of review (RG57) and Information Sheet ASIC decisions – your rights (INFO 9) to assist you to determine whether you have a right of review. You can obtain a copy of these documents from the ASIC Digest, the ASIC website at www.asic.gov.au or from the Administrative Law Co-ordinator in the ASIC office with which you have been dealing. ISSN 1445-6060 (Online version) Available from www.asic.gov.au ISSN 1445-6079 (CD-ROM version) Email [email protected] © Commonwealth of Australia, 2008 This work is copyright. Apart from any use permitted under the Copyright Act 1968, all rights are reserved. Requests for authorisation to reproduce, publish or communicate this work should be made to: Gazette Publisher, Australian Securities and Investment Commission, GPO Box 9827, Melbourne Vic 3001 ASIC GAZETTE Commonwealth of Australia Gazette ASIC 40A/08, Wednesday, 21 May 2008 Banking Act Unclaimed Money Page 2 of 463 Specific disclaimer for Special Gazette relating to Banking Unclaimed Monies The information in this Gazette is provided by Authorised Deposit-taking Institutions to ASIC pursuant to the Banking Act (Commonwealth) 1959. The information is published by ASIC as supplied by the relevant Authorised Deposit-taking Institution and ASIC does not add to the information. -

MELBOURNE CBD Office Market Overview

RESEARCH OCTOBER MELBOURNE CBD Office Market Overview HIGHLIGHTS • Despite the current economic uncertainty, the Melbourne CBD office market recorded a surprisingly solid net absorption result in the first half of 2012 and only a slight rise in vacancy. However the immediate outlook is less promising, having been adversely impacted by contractions within the finance and government sectors; vacancy is forecast to steadily rise over the next year. • The subdued labour market conditions have also stalled rental growth with incentives having risen over the year to date, and these elevated incentive levels are forecast to remain for up to 18 months. • Investor demand remains strong for quality CBD assets, with further transactional activity only hindered by the lack of opportunities. Given the constrained volume of transactions, yields have remained stable despite the increasing investor interest. OCTOBER 2012 MELBOURNE CBD Office Market Overview MELBOURNE CBD OVERVIEW Table 1 Melbourne CBD Office Market Indicators as at October 2012 Market Total Stock Vacancy Annual Net Annual Net Additions Average Net Average Average Core Market (m²)^ Rate Absorption (m²)^ Face Rent Incentive Yield (%)^ (m²)^ ($/m²) (%) (%) Prime 2,524,452 4.6 46,799 54,794 380 – 700 15 – 25 6.75 – 7.25 Secondary 1,625,541 7.1 2,293 -13,451 260 – 430 20 – 22 7.50 – 9.00 Total 4,149,993 5.6 49,092 41,343 Source: Knight Frank/PCA ^ as at July 2012 SUPPLY & DEVELOPMENT ACTIVITY In the year to date, 55,868m² of office space New supply is forecast to pick up in 2013 with Of the new and refurbished supply currently has been added to the Melbourne CBD office 143,849m2 across five developments in the under construction, the vast majority are market, largely through the completion of 3 pipeline and a further 94,000m2 scheduled located in the Docklands precinct, accounting Collins Square and 990 LaTrobe Street, both for completion in 2014. -

201026 Speedcast COS DN

Case 20-32243 Document 897 Filed in TXSB on 11/02/20 Page 1 of 14 IN THE UNITED STATES BANKRUPTCY COURT FOR THE SOUTHERN DISTRICT OF TEXAS HOUSTON DIVISION § In re: § Chapter 11 § SPEEDCAST INTERNATIONAL § LIMITED, et al., § Case No. 20-32243 (MI) § Debtors.1 § (Jointly Administered) § CERTIFICATE OF SERVICE I, T ravis Buckingham, depose and say that I am employed by Kurtzman Carson Consultants LLC (KCC), the claims and noticing agent for the Debtors in the above-captioned case. On October 28, 2020, employees of KCC caused the following document to be served via Electronic Mail to the parties on the service lists attached hereto as Exhibit A and Exhibit B; and via First Class Mail to the parties on the service lists attached hereto as Exhibit C and Exhibit D: • Order (I) Authorizing and Approving NBN Transaction, Including (A) Private Sale Free and Clear of All Liens, Claims, Encumbrances, and Other Interests, (B) Assumption and Assignment of Certain Contracts, and (C) Settlement and Release of Claims, (II) Approving Form and Manner of Notices of NBN Transaction, and (III) Granting Related Relief [Docket No. 879] Dated: November 2, 2020 /s/ Travis Buckingham Travis Buckingham KCC 222 N Pacific Coast Highway, 3rd Floor El Segundo, CA 90245 Tel 310.823.9000 1 A complete list of the Debtors in these chapter 11 cases may be obtained on the website of the Debtors’ claims and noticing agent at http://www.kccllc.net/speedcast. The Debtors’ service address for the purposes of these chapter 11 cases is 4400 S. Sam Houston Parkway East, Houston, Texas 77048. -

Report to the Future Melbourne Committee Agenda Item 6.4

Page 1 of 283 Report to the Future Melbourne Committee Agenda item 6.4 Planning Scheme Amendment C387 Hoddle Grid Heritage (Permanent 18 May 2021 controls) Presenter: Emma Appleton, Director City Strategy Purpose and background 1. The purpose of this report is to consider the submissions received to Melbourne Planning Scheme Amendment C387 Hoddle Grid Heritage Permanent Controls (the Amendment) and to recommend that the Future Melbourne Committee refer all submissions listed at Attachment 2 to an independent Panel in accordance with the Planning and Environment Act 1987. 2. The Amendment implements the recommendations of the Hoddle Grid Heritage Review, 2020 (the Review) by Context and peer reviewed by GJM Heritage. It proposes to include 137 new individual heritage places and five new precincts within Heritage Overlays. Protection of these places contributes to the Grid’s hierarchy of memorable streets and laneways, and diverse precincts, attracting economic activity integral to the Victorian state economy and offering adaptable floor space within the city. 3. The Review was presented to the Future Melbourne Committee on 4 August 2020. Under delegation, management requested authorisation from the Minister for Planning to prepare and exhibit the Amendment. Exhibition was undertaken from 5 November to 17 December 2020, including a wide range of engagement activities that optimised community participation and celebrated heritage in the city. Key issues 4. Twenty-two submissions were received in support of the Amendment including from the National Trust, the Royal Historical Society of Victoria and Melbourne Heritage Action. Forty three submissions were received in opposition to inclusion of 48 places within Heritage Overlays in the Amendment. -

Publicly Accessible Private Plazas in Central Melbourne Amendment C308 Supplementary Analysis City of Melbourne Introduction

PUBLICLY ACCESSIBLE PRIVATE PLAZAS IN CENTRAL MELBOURNE AMENDMENT C308 SUPPLEMENTARY ANALYSIS CITY OF MELBOURNE INTRODUCTION Response to Submissions This research report was prepared in response to submissions received to the exhibition of • Clarification is sought on whether this provision Amendment C308: Urban Design in the Central City calls for a 50% retention of the existing plaza as and Southbank. it is or 50% of the existing plaza area. The report specifically focuses on the following • The provision fails to recognise that there provision within the proposed Design Development may be circumstances where built form on or Overlay Schedule 1 (DDO1): above existing plazas would achieve a superior outcome when compared with the protection of Retain a minimum of 50% of any existing publicly 50% of an existing plaza. accessible private plaza oriented to a main street or street that contributes to reducing pedestrian • The requirement to retain a minimum 50% congestion or where there is good potential of existing publicly accessible private plazas through retrofit and repurposing to achieve a high demands the provision of public open space on quality space with opportunities for stationary private land, which albeit discretionary, removes activity. the level playing field for negotiation. A summary of the submissions relevant to this • The publicly accessible private plazas provision are outlined below: requirement inhibits development and places a burden on any future redevelopment efforts. • This requirement makes no distinction between the qualities of the existing plazas within the Responses to these submissions were presented to Hoddle Grid, ie whether all existing plazas are of the Future Melbourne Committee on 20 November, a quality worthy of protection. -

Melbourne CBD Office Spring 2006 Record Net Absorption

COLLIERS INTERNATIONAL MARKET INDICATORS Melbourne CBD Office SPRING 2006 Record Net Absorption 181 William Street, Melbourne Pre-commitment According to the latest Property Council of Australia Dawson Waldron (8,800m²), AXA (28,700m²), Ericsson by IAG (27,100m²) and data (July 2006), the Melbourne CBD recorded a (10,000m²), Lend Lease (5,000m²), Australian Customs Blake Dawson Waldron (8,800m²). staggering net absorption figure in the last six Services (10,000m²) and National Foods (12,000m²). months of 173,121m², bringing the total absorption Forecast for the last twelve months to 213,159m². These are Further pre-commitments and speculative development the highest six and twelve month net absorption figures is expected to provide measured new supply over (6 months) for Melbourne since PCA records began in 1990. the next 36 months, but in the next twelve months the market will tighten significantly. Overall Performance: ➔ Melbourne has now had solid and sustained net Supply: ➔ absorption over the past three years totalling 465,000m². Incentives have generally reduced across precincts and office grades and are expected to continue to Tenant Demand: ➔ The data reveals the overall vacancy rate has fallen ➔ from 8.3% in January to 7.5% in July. Vacancy in tighten for the remainder of 2006 resulting in increases Vacancy: ➔/ ➔ Premium and A Grade properties decreased while B in effective rentals. Incentives: Grade vacancy increased slightly indicating a flight Investment activity has provided several significant Effective Rents: ➔/ ➔ to quality from tenants in B Grade buildings to A and Premium Grade buildings. transactions during the last twelve months, including ➔ Capital Values: ➔ the sale of 321 Exhibition Street for $120 million and Yields: Most of the positive absorption in the first half of 2006 a 50% interest in 101 Collins Street for $285 million. -

MELBOURNE: SETTLEMENT to GOLD 21,221 Words, 23 May 2012

School of Design (TAFE) MELBOURNE: SETTLEMENT TO GOLD 21,221 words, 23 May 2012 Week 26 Terms Sod, wattle and daub, slab, adobe, cob, Pattern Book. Background Journey to Australia. Trauma of settlement in the wilderness. No building skills. Buildings first influenced by English rural vernacular. Historic development Settlement at Sorrento, 1803. Failed, due to a source of sufficent fresh water. Settlement at Corinella, Western Port Bay, 1826. Only some bricks survive. Melbourne was settled in 1835, illegally, by land-hungry pastoralists from Launceston. The District of Port Phillip, in the Colony of New South Wales was imposed on the settlers. Although not generally acknowledged as such, it was the only settlement in Australia unsanctioned by any government. Gold was discovered in 1851, at Warrandyte and Clunes: instant wealth. Gold towns Clunes. Building types: cottages, post office, banks, rail link (in 1862 to Ballarat and 1864 to Castlemaine), hotels, store, town hall, and schools particularly following the Education Act, 1873. Primitive buildings: material types Thatch, eg: haystacks and barns using reeds, near Hopetoun. 1 School of Design (TAFE) Sod, eg: at Parwan. This was the main material for early Melbourne, particularly for labourers houses. The was turf selected, mown, ploughed, and cut with a hatchet. Walls were 1,300 mm thick. Bark, eg: at the Seven Creeks Station, near Longford. Roofing and cladding. Poles frame and holding down. Axe cut, singed. Wood pegs fixing. They lasted 10-12 years. Two men could strip 40 - 60 trees/day. Wattle and Daub, eg: near Alberton, French Island and at Bacchus Marsh. More sophisticated, generally not in Melbourne. -

Melbourne Office Vacancy Guide Advisory & Transaction Services - Office Leasing

MARCH 2017 MELBOURNE OFFICE VACANCY GUIDE ADVISORY & TRANSACTION SERVICES - OFFICE LEASING www.cbre.com.au MELBOURNE OFFICE VACANCY MARCH 2017 CONTENTS WELCOME CBRE IS PLEASED TO PRESENT THE MARCH 2017 EDITION OF THE MELBOURNE CBD OFFICE VACANCY GUIDE. THIS GUIDE HAS BEEN + Market View PREPARED IN ORDER TO ASSIST OUR CLIENTS IN MAKING INFORMED DECISIONS BASED ON CURRENT MARKET INTELLIGENCE. + Market Vacancy + CBD Vacancy Report CONTACT US ANDREW TRACEY MARC MENGONI CAITLIN MURDOCH MARK BOLIS PATRICK MOUNT Regional Director Director Senior Associate Director Senior Associate Director Senior Associate Director T. +61 3 8621 3325 T. +61 3 8621 3416 T. +61 3 8621 3417 T. +61 3 8621 3322 T. +61 3 8621 3337 M. +61 412 809 300 M. +61 413 484 966 M. +61 417 473 015 M. +61 412 237 809 M. +61 413 253 593 [email protected] [email protected] [email protected] [email protected] [email protected] SCOTT MCGLONE WILL DUNGEY ED LOWER CHARLOTTE MCCANN JAMES ALLEN Associate Director Manager Manager Negotiator Analyst T. +61 3 8621 3336 T. +61 3 8621 3495 T. +61 3 8621 3324 T. +61 3 8621 3061 T. +61 3 8621 3060 M. +61 419 468 871 M. +61 400 994 351 M. +61 423 734 043 M. +61 419 042 088 [email protected] [email protected] [email protected] [email protected] [email protected] MELBOURNE OFFICE VACANCY MARCH 2017 MARKET VIEW MELBOURNE CBD OFFICE Demand Supply Rents Absorption Victoria’s state final demand continued to grow over Over 2016, the Melbourne CBD saw the completion The Melbourne CBD leasing market continued to Net absorption in the Melbourne CBD has now been the 12 months ending September 2016, up 2.5%.