Private Equity In

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Combining Banking with Private Equity Investing*

Unstable Equity? * Combining Banking with Private Equity Investing First draft: April 14, 2010 This draft: July 30, 2010 Lily Fang INSEAD Victoria Ivashina Harvard University and NBER Josh Lerner Harvard University and NBER Theoretical work suggests that banks can be driven by market mispricing to undertake activity in a highly cyclical manner, accelerating activity during periods when securities can be readily sold to other parties. While financial economists have largely focused on bank lending, banks are active in a variety of arenas, with proprietary trading and investing being particularly controversial. We focus on the role of banks in the private equity market. We show that bank- affiliated private equity groups accounted for a significant share of the private equity activity and the bank’s own capital. We find that banks’ share of activity increases sharply during peaks of the private equity cycles. Deals done by bank-affiliated groups are financed at significantly better terms than other deals when the parent bank is part of the lending syndicate, especially during market peaks. While bank-affiliated investments generally involve targets with better ex-ante characteristics, bank-affiliated investments have slightly worse outcomes than non-affiliated investments. Also consistent with theory, the cyclicality of banks’ engagement in private equity and favorable financing terms are negatively correlated with the amount of capital that banks commit to funding of any particular transaction. * An earlier version of this manuscript was circulated under the title “An Unfair Advantage? Combining Banking with Private Equity Investing.” We thank Anna Kovner, Anthony Saunders, Antoinette Schoar, Morten Sorensen, Per Strömberg, Greg Udell and seminar audiences at Boston University, INSEAD, Maastricht University, Tilburg University, University of Mannheim and Wharton for helpful comments. -

Preqin Research Report Fig

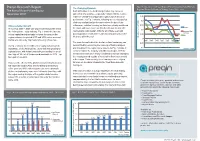

Preqin Research Report Fig. 3 Comparison of Private Equity Performance by Fund Primary The Changing Dynamic Regional Focus for Funds of Vintage Years 1995 - 2007 The Rise of Asian Private Equity Such diffi culties in the fundraising market may come as November 2010 somewhat of a surprise – especially considering the relative resilience of Asia-focused private equity funds in terms of 0.25 performance. As Fig. 3 shows, following an extended period 0.2 of strong median fund performance since the turn of the Unprecedented Growth millennium, vehicles focusing on Asia have clearly weathered 0.15 the storm with more success than their European and US Europe The period 2003 – 2008 saw unprecedented growth within 0.1 the Asian private equity industry. Fig. 1 shows the increase counterparts, with median IRRs for all vintage years still Asia and Rest of World posting positive results while funds focusing primarily on the 0.05 in total capital raised annually by funds focusing on the US region between the period 2003 and 2008, when a record West are still in the red. IRR Median Net-to-LP 0 $91bn was raised by 194 funds achieving a fi nal close. 1995 1997 1999 2001 2003 2005 2007 The main factors behind the decline in Asia fundraising can -0.05 As Fig. 2 shows, the record level of capital raised saw the be identifi ed by examining the make-up of fund managers -0.1 Vintage Year importance of the Asian private equity industry growing on and investors in the region more closely. As Fig. -

TRS Contracted Investment Managers

TRS INVESTMENT RELATIONSHIPS AS OF DECEMBER 2020 Global Public Equity (Global Income continued) Acadian Asset Management NXT Capital Management AQR Capital Management Oaktree Capital Management Arrowstreet Capital Pacific Investment Management Company Axiom International Investors Pemberton Capital Advisors Dimensional Fund Advisors PGIM Emerald Advisers Proterra Investment Partners Grandeur Peak Global Advisors Riverstone Credit Partners JP Morgan Asset Management Solar Capital Partners LSV Asset Management Taplin, Canida & Habacht/BMO Northern Trust Investments Taurus Funds Management RhumbLine Advisers TCW Asset Management Company Strategic Global Advisors TerraCotta T. Rowe Price Associates Varde Partners Wasatch Advisors Real Assets Transition Managers Barings Real Estate Advisers The Blackstone Group Citigroup Global Markets Brookfield Asset Management Loop Capital The Carlyle Group Macquarie Capital CB Richard Ellis Northern Trust Investments Dyal Capital Penserra Exeter Property Group Fortress Investment Group Global Income Gaw Capital Partners AllianceBernstein Heitman Real Estate Investment Management Apollo Global Management INVESCO Real Estate Beach Point Capital Management LaSalle Investment Management Blantyre Capital Ltd. Lion Industrial Trust Cerberus Capital Management Lone Star Dignari Capital Partners LPC Realty Advisors Dolan McEniry Capital Management Macquarie Group Limited DoubleLine Capital Madison International Realty Edelweiss Niam Franklin Advisers Oak Street Real Estate Capital Garcia Hamilton & Associates -

PEI Investor Relations, Marketing & Communications Forum 2019

June 19-20 | Convene, 730 Third Ave | New York Attendee list A.P. Moller Capital Bain Capital C-Bridge Capital Partners FTV Capital ACME Capital Banner Real Estate Group CCMP Capital Advisors Further Capital Partners Actis Barings Centerbridge Partners GCM Grosvenor Advent International Basis Investment Group Cerberus Capital Management General Atlantic AE Industrial Partners Battery Ventures Charlesbank Capital Partners General Catalyst Partners AEA Investors BBH Capital Partners The Chauncey F. Lufkin III Gennx360 AEW Capital Management BC Partners Foundation Genstar Capital AIMA The Beach Company The City of New York, Finance Global Infrastructure Partners Alcentra Berkshire Partners Civitas Capital Grain Management Alcion Ventures Bernhard Capital Partners Coller Capital Gryphon Investors Allianz Capital Partners Bicknell Family Holding Cornell Capital GTCR Altor Equity Partners Company Court Square Capital Partners Halstatt American Securities Bison Crescent Capital Group Hamilton Lane AMP Capital BKM Capital Partners CRV Hammes Angelo Gordon Blackstone Cypress Real Estate Advisors Hammond, Kennedy, Whitney Antares Capital Blue Heron Asset Managment Denham Capital & Co Apollo Global Management Blue Water Energy Duff & Phelps Hancock Capital Management ARC Financial Corp Bridge Investment Group Dyal Capital Partners Harvard Management Company ArcLight Capital Partners BroadVail Capital Edelman HCI Equity Partners Argosy Capital Brook Venture Partners EnCap Investments HGGC Arroyo Energy Investment Brookfield Asset Management EQT Partners -

ANNUAL REVIEW 2017 Land of the Giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus

ANNUAL REVIEW 2017 Land of the giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus Ares Management is honored to be recognized as Lender of the Year in North America for the fourth consecutive year as well as Lender of the Year in Europe Lender of the year in Europe Ares Management, L.P. (NYSE: ARES) is a leading global alternative asset manager with approximately $106 billion of AUM1 and offices throughout the United States, Europe, Asia and Australia. With more than $70 billion in AUM1 and approximately 235 investment professionals, the Ares Credit Group is one of the largest global alternative credit managers across the non-investment grade credit universe. Ares is also one of the largest direct lenders to the U.S. and European middle markets, operating out of twelve office locations in both geographies. Note: As of December 31, 2017. The performance, awards/ratings noted herein may relate only to selected funds/strategies and may not be representative of any client’s given experience and should not be viewed as indicative of Ares’ past performance or its funds’ future performance. 1. AUM amounts include funds managed by Ivy Hill Asset Management, L.P., a wholly owned portfolio company of Ares Capital Corporation and a registered investment adviser. learn more at: www.aresmgmt.com | www.arescapitalcorp.com The battle of the brands the US market on page 80, advisor Hamilton TOBY MITCHENALL Lane said it had received a record number EDITOR'S of private placement memoranda in 2017 – ISSN 1474–8800 LETTER MARCH 2018 around 800 – and that this, combined with Senior Editor, Private Equity faster fundraising processes, has made it dif- Toby Mitchenall, Tel: +44 207 566 5447 [email protected] ficult to some investors to make considered Special Projects Editor decisions. -

Genstar Capital Partners X, LP

Investment Summary Genstar Capital Partners X, L.P. A North American Buyout Fund January 2021 Trade Secret and Confidential Trade Secret and Confidential EXECUTIVE SUMMARY OVERALL RATING Genstar Capital Partners LLC (“Genstar” or the “Firm”) has demonstrated an ability to build substantial value for limited partners through its in-depth sector knowledge, focus on talent management, M&A value creation strategy, and 29-member Strategic Advisory Board (“SAB”). Led by a seasoned and long tenured group of managing partners, Genstar has delivered strong performance across its four recent funds. Category Rating Business ✓ Staff ✓ Process ✓ Risk ✓ Operations ✓ Performance ✓ Terms &Conditions ✓ Aon has reviewed and performed an in-depth analysis of the above categories which includes, but is not limited to: ▪Retention of Limited Partners ▪Complementary Skill Sets ▪Market Opportunity ▪Institutional Investor Representation ▪Alignment of Interest ▪Stability of Strategy ▪Management Company Ownership ▪Turnover/Tenure ▪Investment Restrictions ▪Reporting Transparency ▪Depth of Team Resources ▪Approval process ▪Back-office Resources ▪Management Team Network ▪Ability to handle troubled deals ▪Firm Leadership ▪Exit strategy ▪Size of Fund ▪Consistency / Volatility of Returns ▪Management Fee and Offsets ▪Ability to Create Value in Deals ▪Realization Record ▪Priority of Distributions ▪Quality of Source ▪Unrealized Portfolio Performance ▪Clawback ▪Valuation Discipline ▪Write-Offs ▪Investment Period ▪Sole or Consortium Deals ▪Transaction Experience in Strategy -

PEI June2020 PEI300.Pdf

Cover story 20 Private Equity International • June 2020 Cover story Better capitalised than ever Page 22 The Top 10 over the decade Page 24 A decade that changed PE Page 27 LPs share dealmaking burden Page 28 Testing the value creation story Page 30 Investing responsibly Page 32 The state of private credit Page 34 Industry sweet spots Page 36 A liquid asset class Page 38 The PEI 300 by the numbers Page 40 June 2020 • Private Equity International 21 Cover story An industry better capitalised than ever With almost $2trn raised between them in the last five years, this year’s PEI 300 are armed and ready for the post-coronavirus rebuild, writes Isobel Markham nnual fundraising mega-funds ahead of the competition. crisis it’s better to be backed by a pri- figures go some way And Blackstone isn’t the only firm to vate equity firm, particularly and to towards painting a up the ante. The top 10 is around $30 the extent that it is able and prepared picture of just how billion larger than last year’s, the top to support these companies, which of much capital is in the 50 has broken the $1 trillion mark for course we are,” he says. hands of private equi- the first time, and the entire PEI 300 “The businesses that we own at Aty managers, but the ebbs and flows of has amassed $1.988 trillion. That’s the Blackstone that are directly affected the fundraising cycle often leave that same as Italy’s GDP. Firms now need by the pandemic, [such as] Merlin, picture incomplete. -

Investor Relations Marketing & Communications Forum

Investor Relations Marketing & Communications Forum Virtual experience 2020 September 2-3 | Available anywhere The largest global event for PE Investor Relations, Marketing & Communications A new virtual experience Customize your agenda Available anywhere Industry leading IR and Mix and match 3 think tank Enjoy the Forum from the marketing content selections, 3 interactive comfort of your home office and The Forum’s in-depth sessions are discussion rooms, 12 breakouts on-demand access for up to 12 designed to help you formulate and panel sessions to your liking months after the event is over effective plans and develop crucial for a personalize event strategies to attract investors experience A new kind of networking Built-in calendar and Networking lounges Gain early access to the attendee automated reminders Explore and meet with industry list and start scheduling 1-to-1 Easily download and sync your service providers to discover the or small group meetings or direct event agenda with preferred latest trends and technologies message fellow attendees in tracks and 1-to-1 meetings to your advance own work calendar Speakers include Marilyn Adler Nicole Adrien Christine Anderson Mary Armstrong Michael Bane Managing Partner Chief Product Officer Senior Managing Senior Vice President, Head of US Investor Mizzen Capital and Global Head of Director, Global Head Global Head of Relations Client Relations of Public Affairs & Marketing and Ardian Oaktree Capital Marketing Communications Blackstone General Atlantic Devin Banerjee Charles Bauer Gina -

The Fintech Spotlight

plaid.com The Fintech Spotlight A look at what’s happening across the fintech ecosystem elcome to the Fintech Spotlight, a quarterly W report that provides insights and analysis on trends across the fintech ecosystem. The report is divided into six sections: • Personal financial management (PFM): The next frontier of rewards • Wealth: Blending traditional wealth management and robo-advisors • Lending & Advance access to funds: Targeting consumer needs • Consumer payments: Tender steering to ACH payments • Business financial management (BFM): Untapped opportunities among SMEs • Banking: A future in embedded finance A WORD FROM PLAID The three months since the last edition of the Fintech Spotlight might as “ The ability to tap a screen well have been three years. Multiple COVID vaccines were approved, a new and instantly have a car at administration was sworn into office, and a third stimulus package was your door or the latest movie passed by Congress (not to mention, Reddit paid a visit to Wall Street1). on your TV has upped the expectations for every aspect While the Biden-Harris administration faces a great number of challenges as of life—including banking.” 2021 continues to unfold, two particular areas of focus stand out beyond the immediate concerns over vaccine roll-out. First, there’s the mammoth task of ERIC SAGER rehabilitating the economy in a post-COVID world. Given the changes to Chief Operating Officer, Plaid both consumer circumstances and behavior over the past twelve months, this economic rebuild represents a continued opportunity for fintechs to meet consumers’ evolving needs and expectations. The ability to tap a screen and instantly have a car at your door or the latest movie on your TV has upped the expectations for every aspect of life—including banking. -

Trs Investment Relationships As of June 2020

TRS INVESTMENT RELATIONSHIPS AS OF JUNE 2020 Global Public Equity (Global Income continued) Acadian Asset Management Oaktree Capital Management AQR Capital Management Pacific Investment Management Company Arrowstreet Capital Pemberton Capital Advisors Axiom International Investors PGIM Dimensional Fund Advisors Proterra Investment Partners Emerald Advisers Riverstone Credit Partners Grandeur Peak Global Advisors Solar Capital Partners JP Morgan Asset Management Taplin, Canida & Habacht/BMO LSV Asset Management Taurus Funds Management Northern Trust Investments TCW Asset Management Company RhumbLine Advisers Varde Partners Strategic Global Advisors T. Rowe Price Associates Real Assets Wasatch Advisors Barings Real Estate Advisers The Blackstone Group Transition Managers Brookfield Asset Management The Carlyle Group Citigroup Global Markets CB Richard Ellis Loop Capital Dyal Capital Macquarie Capital Exeter Property Group Northern Trust Investments Fortress Investment Group Penserra Gaw Capital Partners Heitman Real Estate Investment Management Global Income INVESCO Real Estate AllianceBernstein LaSalle Investment Management Apollo Global Management Lion Industrial Trust Beach Point Capital Management Lone Star Cerberus Capital Management LPC Realty Advisors Dolan McEniry Capital Management Macquarie Group Limited DoubleLine Capital Madison International Realty Edelweiss Niam Franklin Advisers Oak Street Real Estate Capital Garcia Hamilton & Associates Principal Real Estate Investors Hayfin Capital Management Proterra Investment Partners -

Download the 2020 Report

MBA Careers 2020 Employment Summary CLASS OF 2021 INTERNSHIPS CLASS OF 2020 FULL-TIME NUMBER PERCENTAGE NUMBER PERCENTAGE TOTAL NUMBER OF STUDENTS 852 904 Students Seeking Employment 775 91.0% 681 75.3% Reporting Job Offers 774 99.9 637 93.5 Reporting Job Acceptances 771 99.5 624 91.6 Students Not Seeking Employment 48 5.3 159 17.6 Company-Sponsored (Returning to Company) 3 111 Self-Employed/Starting Own Business 24 28 Postponed Job Search/Continuing Education 1 17 Personal Reasons/Other 20 3 Students Not Responding to Survey 33 3.6 64 7.1 Data current as of September 14, 2020, and it is collected and reported according to MBA Career Services and Employer Alliance standards. Compensation CLASS OF 2021 INTERNSHIPS CLASS OF 2020 FULL-TIME by Industry (MONTHLY) (ANNUAL) PERCENT ACCEPTS MEDIAN SALARY PERCENT ACCEPTS MEDIAN SALARY ALL INDUSTRIES $9,200 $150,000 Consulting 16.4% $13,500 24.5% $165,000 Consumer Products 2.8 8,333 2.4 122,500 Energy 1.3 7,667 0.2 — Financial Services 36.0 10,416 36.2 150,000 Hedge Funds/Other Investments 3.3 10,000 3.2 150,000 Insurance & Diversified Services 2.3 9,666 1.4 125,000 Investment Banking/Brokerage 10.7 12,500 12.2 150,000 Investment Management 4.6 10,721 4.5 150,000 Private Equity/Buyouts/Other 8.0 10,000 11.9 170,000 Venture Capital 7.1 6,000 3.0 171,500 FinTech 1.5 5,000 2.1 140,000 Future Mobility 0.4 — — — Health Care 7.4 7,954 6.7 140,000 Legal & Professional Services 1.2 12,917 1.8 190,000 Manufacturing 2.3 7,800 0.8 — Media, Entertainment & Sports 1.3 5,170 1.3 150,000 Real Estate 2.1 7,210 2.9 120,000 Retail 5.2 6,150 3.2 140,000 Social Impact 5.3 4,480 1.8 89,250 Technology 16.9 8,666 16.2 139,345 Travel & Hospitality 0.1 — — — Median base salary for one year only. -

The Rise of Private Equity Media Ownership in the United States: a Public Interest Perspective

City University of New York (CUNY) CUNY Academic Works Publications and Research Queens College 2009 The Rise of Private Equity Media Ownership in the United States: A Public Interest Perspective Matthew Crain CUNY Queens College How does access to this work benefit ou?y Let us know! More information about this work at: https://academicworks.cuny.edu/qc_pubs/171 Discover additional works at: https://academicworks.cuny.edu This work is made publicly available by the City University of New York (CUNY). Contact: [email protected] International Journal of Communication 2 (2009), 208-239 1932-8036/20090208 The Rise of Private Equity Media Ownership in the United States: ▫ A Public Interest Perspective MATTHEW CRAIN University of Illinois, Urbana-Champaign This article examines the logic, scope, and implications of the influx of private equity takeovers in the United States media sector in the last decade. The strategies and aims of private equity firms are explained in the context of the financial landscape that has allowed them to flourish; their aggressive expansion into media ownership is outlined in detail. Particular attention is paid to the public interest concerns raised by private equity media ownership relating to the frenzied nature of the buyout market, profit maximization strategies, and the heavy debt burdens imposed on acquired firms. The article concludes with discussion of the challenges posed by private equity to effective media regulation and comparison of private equity and corporate media ownership models. The media sector in the United States is deeply and historically rooted in the capitalist system of private ownership. The structures and demands of private ownership foundationally influence the management and operation of media firms, which must necessarily serve the ultimate end of profitability within such a system.