Lebanon's Fashion Design Ecosystem

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bella Hadid in Elie Saab

Editor’s LETTER We have weddings on the brain this issue. Not only do we have the brand new season of Bridal Fashion Week to fawn over, but a certain former First Avenue cover star only went and married herself a Prince… and we’re making pretty big deal out of it! Once you’re done with staring at pictures of Prince Harry and Meghan Markle’s glorious Royal Wedding, we invite you to cast your eyes over to Hollywood royalty in the form of the sparkling Cannes Film Festival red carpet. Is it just us, or do the looks get better and better each year? And that’s not all – from gushing over cover star Penelope Cruz and her glorious style, to showing you how to steal a very simple but oh so chic Burberry-heavy celeb look, it’s a jam-packed issue to say the least! Plus, keep the sun out in style with our selection of the most fashionable, statement-making sunglasses around. And we haven’t even mentioned our trendy leopard print edit yet… “Myles Mellor PENELOPE CRUZ - PAGE 38 6 CONTENTS June - July 2018 Style Crushing on… 38 Penelope Cruz Bridal Fashion Week… 12 Spring 2019 Eye Spy… 64 Stunning new season sunnies 10 38 Trend to Try… 32 Leopard print Cannes Film Festival 2018 52 Our most glamorous red carpet looks Get the Look… 10 Dove Cameron 12 52 www.firstavenuemagazine.com First Avenue Magazine @firstavenuemagazine 8 Publisher Hares Fayad Editor Myles Mellor Senior writer Maria Pierides Art Director Ahmad Yazbek Overseas Contributers Nabil Massad, Paris Kristina Rolland, Italy Samo Suleiman, Lebanon Isabel Harsh, New York Kamilia Al Osta, London Offices (U.A.E.), Dubai Jumeirah Lakes Towers, JBC 2 P.O. -

The United States Of

SAAB’S BIG THE BATTLE FOR PUSH DOWNTOWN ELIE SAAB IS AMONG A WAVE OF LEBANESE DESIGNERS RAISING THEIR PROFILES IN THE WESTFIELD WORLD TRADE CENTER UNVEILS U.S. AND ABROAD. PAGE 8 ITS FIRST LIST OF TENANTS AT LAST. PAGE 3 WWDMONDAY, NOVEMBER 17, 2014 ■ $3.00 ■ WOMEN’S WEAR DAILY THE UNITED STATES OF LUXURY By MILES SOCHA and SAMANTHA CONTI 16 percent; Hermès’ jumped 16.9 percent at constant exchange, and Gucci’s increased 8 percent at its own stores. AMERICA THE BEAUTIFUL. The data are unequivocal: In the third quarter, the U.S. That seems to be the song luxury brands are singing these days. notched 3.5 percent growth in gross domestic product, With the Chinese market cooling and Europe in the doldrums, demonstrating broad-based improvement across the economy. the U.S. is looking more like the luxury El Dorado it used to The most recent study by Bain & Co. and Fondazione be. Simply scanning the third-quarter, or nine-month, results of Altagamma, the Italian luxury goods association, confi rmed the leading luxury brands is proof of the market’s buoyancy: Saint Americas as a key growth driver, accounting for 32 percent of a Laurent’s North American sales leaped 47 percent in the third global market for personal luxury goods estimated at 223 billion quarter; Moncler’s were up 32 percent; Brunello Cucinelli’s rose SEE PAGE 4 2 WWD MONDAY, NOVEMBER 17, 2014 WWD.COM Kors’ Instagram Adds ‘Buy’ THE BRIEFING BOX most social engagement to date one of the fi rst brands to imple- IN TODAY’S WWD By RACHEL STRUGATZ — handbags, such as the Dillon ment an initiative like this. -

Download The

The House of an Artist Recognized as one of the world’s most celebrated perfumers, Francis Kurkdjian has created over the past 20 years more than 40 world famous perfumes for fashion houses such as Dior, Kenzo, Burberry, Elie Saab, Armani, Narciso Rodriguez… Instead of settling comfortably into the beginnings of a brilliant career started with the creation of ”Le Mâle” for Jean Paul Gaultier in 1993, he opened the pathways to a new vision. He was the first in 2001 to open his bespoke fragrances atelier, going against the trend of perfume democratization. He has created gigantic olfactory installations in emblematic spaces, making people dream with his ephemeral and spectacular perfumed performances. All this, while continuing to create perfumes for world famous fashion brands and designers, as fresh as ever. Maison Francis Kurkdjian was a natural move in 2009, born from the encounter between Francis Kurkdjian and Marc Chaya, Co-founder and President of the fragrance house. Together, they fulfilled their desire for a sensual, generous and multi-facetted landscape of free expression, creating a new emblem of French know-how and lifestyle. A high-end fragrance house Maison Francis Kurkdjian’s unique personality is fostered by the creative power of a man who has a taste for precision. The Maison is guided by enchanting yet precise codes: purity, sophistication, timelessness and the boldness of a classicism reinvented. Designed in the tradition of luxury French perfumery, the Maison Francis Kurkdjian collection advocates nevertheless a contemporary vision of the art of creating and wearing perfume. Francis Kurkdjian creations were sketched like a fragrance wardrobe, with myriad facets of emotions. -

Pitfalls of Multitasking COVER PGSTORY 2&3 02 Wednesday, May 18, 2016 COVER STORY Too Distracted? Try Monotasking

QATAR TRIBUNE Publication Wednesday Marion Cotillard just the right person for the role of 18.05.2016 Gabrielle in Mal de Pierres ... Hollywood Pitfalls of multitasking COVER PGSTORY 2&3 02 Wednesday, May 18, 2016 COVER STORY Too distracted? Try monotasking NYT SYNDICATE TOP what you’re doing. Well, keep reading. Just stop everything else that you’re doing. Mute your music. Turn off Syour television. Ignore that text mes- sage. While you’re at it, put your phone away entirely. (Unless you’re reading this on your phone. In which case, don’t.) Just read. You are now monotask- ing. Maybe this doesn’t feel like a big deal. Doing one thing at a time isn’t a new idea. Indeed, multitasking, that bulwark of anaemic resumes everywhere, has come under fire in recent years. A 2014 study in the Journal of Experimental Psychology found that interruptions as brief as 2 to 3 seconds — less than the amount of time it would take you to toggle from this article to your email and back again — were enough to dou- ble the number of errors participants made in an assigned task. Earlier research out of Stanford University revealed that self-identified “high media multitaskers” are actually more easily distracted than those who limit their time toggling. So, in layman’s terms, by doing more you’re getting less done. But monotasking, also referred to as 4\S[P[HZRPUN[OH[I\S^HYRVMHUHLTPJYLZ\TLZL]LY`^OLYLOHZJVTL single-tasking or unitasking, isn’t just about getting things done. \UKLYÄYLPUYLJLU[`LHYZ(Z[\K`PU[OL1V\YUHSVM,_WLYPTLU[HS Not the same as mindfulness, which -

Moderne Professionnel C.V

CRISTINA GIBELLI T R A N S L A T O R I N T E R P R E T E R & B U S I N E S S D E V E L O P M E N T L A N G U A G E S Italian Bilingual English Bilingual French Fluent C O N T A C T S K I L L S Translations Consecutive interpreting [email protected] Remote Video interpreting +33(0)6 37 67 18 16 Phone interpreting Transcriptions www.linkedin.com/in/cristin Audio visual subtitling without time codes a-gibelli-0a718910/ Content Creation www.instagram.com/ Newsletters cristinagibelli/ Marketing Research International Business Development & Sales Digital Marketing Cultural Mediation Luxury Fashion Guide W H O I A M W O R K E X P E R I E N C E P A R I S - "Learning from different cultures F R O M 2 0 0 9 and different points of view" I have a multi-cultural background; TRANSLATING & INTERPRETING TOURISM I am versatile, curious and sociable. Projects include: Italian – Canadian, I lived 12 years in MODEMONLINE Publisher: Content Management, London before moving to Paris in Translating and Customer Relation 2019 2009. I offer services of translating, FONDATION AZZEDINE ALAIA: Translations for the interpreting, high end fashion “Adrian and Alaia” Exhibition 2019 guiding as well as business FORUM CONSTRUCTION EN BOIS: Translations for the PR development, marketing & sales to Office 2019 independent luxury niche fashion NOTARY Jean-Michel Simeon: Interpreting for property designers targeting international sale 2019 buyers of boutiques and INTERNATIONAL HOME website translations and content department stores worldwide creation 2019 VESTIAIRE -

Lebanese Fashion Designer Who Took Hollywood by Storm, Now Runs An

WHEN A MAN IS DENIED THE RIGHT TODAY IN QUOTE TO LIVE THE LIFE HE BELIEVES IN, 1238 1301 1856 1992 HISTORY OF THE HE HAS NO CHOICE BUT TO BECOME The Mongols burn Edward of Caernarion Colonial Tasmanian Parliament passes the Maastricht Treaty signed by DAY the Russian city of (later Edward II) be- 1st piece of legislation (the Electoral Act 12 countries from the Euro- AN OUTLAW Vladimir comes first (English) of 1856) anywhere in the world providing pean Community (EC) to cre- FRIDAY FEBRUARY 7, 2020 NELSON MANDELA Prince of Wales for elections by way of a secret ballot ate the European Union (EU) RUNWAY HEROES Elie Saab, king of the red carpet Every time is like the first time. We always have a new item to present, a new style to reveal. It’s not easy, because I like to be perfect, always ELIE SAAB Lebanese as $150. fashion designer The next step? Developing his own e-com- merce platform, adding to his sizeable online presence in a number of regional and inter- who took national websites including Harvey Nichols and Net-A-Porter. Hollywood It is no secret the digital wave has hit even the biggest of brands and retailers. There is no guarantee Saab will not be one of them, espe- Artists on stage during the event by storm, cially given the rise of fast online fashion that imitates runway collections and gets them from concept to sale in as little as a week. now runs an The risks drive Saab, who says fear played a major role in his opening of the first shop in Arabic anime voice actors international, Beirut as a university dropout. -

Safilo Introduces Atelier Eyewear with Elie Saab Couture and Oxydo

SAFILO INTRODUCES ATELIER EYEWEAR WITH ELIE SAAB COUTURE AND OXYDO Padua, 25 January 2017 – Safilo Group, the fully integrated Italian Eyewear creator and worldwide distributor of quality and trust, opens its Atelier Division with Elie Saab Couture and OXYDO, the first brands to offer exquisite and differing Atelier Eyewear expressions. Positioned above the Fashion Luxury segment, Atelier offers to the most discerning customers across the world an exclusive new eyewear selection of highly sophisticated brands. They share the most refined product, expertly crafted in Italy, outstanding quality expressing exquisite artisanship, and combine aesthetic unicity, intricate detail and superior materials of innovative compositions. Safilo’s Atelier represents a most refined eyewear concept in the context of design, art, and fashion trends. It will be available in the most exclusive specialist optical and fashion boutique stores, rigorously selected across the world. The Atelier brands will be presented in bespoke collections, designed with limited pieces in capsule collections, and exclusive Limited Editions made to order. Safilo Group designs, creates, manufactures and distributes its iconic Eyewear collections derived from a prestigious and unique portfolio of international brands that spans the key eyewear segments of Fashion Luxury with Dior, Jimmy Choo and Fendi, and Premium Fashion with Max Mara and Hugo Boss, Contemporary Lifestyle with Carrera, Marc Jacobs, Tommy Hilfiger, kate spade new york and Fossil, Sports Inspired Smith, and Mass Cool with Polaroid, havaianas and Swatch-the-Eyes. “With Atelier, we enter as per our 2020 Strategic Plan also the Segment of Super Luxury Eyewear. It offers very interesting growth and profitability rates. Because we have made high quality product and distribution differentiation the bedrock of our corporate strategy over the past few years, we can now scale that to match precisely also the requirements of the Super Luxury business model,” says Luisa Delgado, CEO of Safilo. -

Fall 2019 Rizzoli Fall 2019

I SBN 978-0-8478-6740-0 9 780847 867400 FALL 2019 RIZZOLI FALL 2019 Smith Street Books FA19 cover INSIDE LEFT_FULL SIZE_REV Yeezy.qxp_Layout 1 2/27/19 3:25 PM Page 1 TABLE OF CONTENTS RIZZOLI Marie-Hélène de Taillac . .48 5D . .65 100 Dream Cars . .31 Minä Perhonen . .61 Achille Salvagni . .55 Missoni . .49 Adrian: Hollywood Designer . .37 Morphosis . .52 Aēsop . .39 Musings on Fashion & Style . .35 Alexander Ponomarev . .68 The New Elegance . .47 America’s Great Mountain Trails . .24 No Place Like Home . .21 Arakawa: Diagrams for the Imagination . .58 Nyoman Masriadi . .69 The Art of the Host . .17 On Style . .7 Ashley Longshore . .43 Parfums Schiaparelli . .36 Asian Bohemian Chic . .66 Pecans . .40 Bejeweled . .50 Persona . .22 The Bisazza Foundation . .64 Phoenix . .42 A Book Lover’s Guide to New York . .101 Pierre Yovanovitch . .53 Bricks and Brownstone . .20 Portraits of a Master’s Heart For a Silent Dreamland . .69 Broken Nature . .88 Renewing Tradition . .46 Bvlgari . .70 Richard Diebenkorn . .14 California Romantica . .20 Rick Owens Fashion . .8 Climbing Rock . .30 Rooms with a History . .16 Craig McDean: Manual . .18 Sailing America . .25 David Yarrow Photography . .5 Shio Kusaka . .59 Def Jam . .101 Skrebneski Documented . .36 The Dior Sessions . .50 Southern Hospitality at Home . .28 DJ Khaled . .9 The Style of Movement . .23 Eataly: All About Dolci . .40 Team Penske . .60 Eden Revisited . .56 Together Forever . .32 Elemental: The Interior Designs of Fiona Barratt Campbell .26 Travel with Me Forever . .38 English Gardens . .13 Ultimate Cars . .71 English House Style from the Archives of Country Life . -

Haute-Couture-Fall-Winter

1 GAULTIER PARIS 2 3 FRANCESCO SCOGNAMIGLIO 4 5 JEWELRY SUZANNE SYZ ART JEWELS 7 ON AURA TOUT VU 8 9 GAULTIER PARIS 10 11 ELIE SAAB 12 13 ARTISANAL INTELLIGENCE “GRAND TOUR” PH:ANDREA BUCCELLA MARIA SOLE FERRAGAMO 14 15 CHANEL Mai come in questi ultimi tempi il mondo dell’alta moda ha deciso di spalancare le sue porte al pubblico mondiale diventando, in quest’epoca così social, quasi virale attraverso la pubblicazione online e la messa in onda televisiva di centinaia e centinaia di video e conte- nuti dedicati al suo affascinante savoir faire. L’alta moda si svela e alza il sipario sul making of, ossia su tutto ciò che accade prima che favolosi abiti e accessori deluxe sfilino in pas- serella incantando pubblico e addetti ai lavori con la loro meravigliosa bellezza. Un trend consacrato quest’anno dalla sfilata fall/winter 2016-17 di Chanel che ha dedicato la sua collezione ai suoi atelier Haute Couture, celebrando così il talento delle persone che dietro le quinte lavorano alla realizzazione di autentici capolavori. Durante la sfilata gli ospiti sono stati come proiettati nell’ambientazione intima, e un tempo off limits, degli atelier di Rue Cambon, ricreati per l’occasione sotto il soffitto di vetro del Grand Palais con tavoli, macchine da cucire, spilli, scampoli di stoffa, manichini sartoriali, specchi: la quotidianità dei quattro atelier della Maison è stata così svelata in tutto il suo efficiente splendore e stra- ordinario heritage. Perchè è questa la realtà. È qui che tutto ha inizio e le idee dello stilista e i suoi bozzetti prendono vita. -

DesignerBrandList

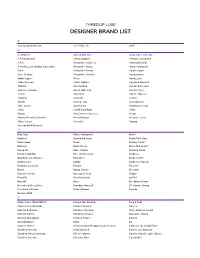

THREDUP LUXE DESIGNER BRAND LIST # 10 Crosby Derek Lam 3.1 Phillip Lim 6397 A A Détacher Alessandra Rich Anna-Karin Karlsson A.F.Vandevorst Alexa Wagner Anthony Vaccarello A.P.C. Alexander McQueen Antonio Berardi A.W.A.K.E. by Natalia Alaverdian Alexander Wang Anya Hindmarch Acne Alexandre Birman Apiece Apart Acne Studios Alexandre Vauthier Aquascutum Adam Lippes Alexis Aquazzura Adam Selman Alexis Mabille Aquilano Rimondi ADEAM Alice McCall Armani Collezioni Adrienne Landau Alix of Bohemia Armani Prive Aether Altuzarra Arthur Arbesser Agnona Alumnae Ashish AKRIS Amelia Toro Atea Oceanie Akris punto Andrew Gn Atlantique Ascoli Alaïa André Courrèges Atlein Alanui Ann Demeulemeester Attico Alberta Ferretti Collection Anna October Au Jour Le Jour Albus Lumen Anna Sui Azzaro Alessandra Chamonix B Baja East Bibhu Mohapatra Brioni Baldinini Bionda Castana Brock Collection Balenciaga Biyan Brother Vellies Balmain Black Fleece Brunello Cucinelli Banjanan Blaze Milano Building Block Banjo & Matilda Bliss and Mischief Burberry Bao Bao Issey Miyake Blumarine Burberry Brit Barbara Bui Bodkin Burberry Prorsum Barbara Casasola Bogner Buscemi Barrie Borgo De Nor BUwood Barton Perreira Bottega Veneta Bvlgari Beaufille Bouchra Jarrar by FAR Belstaff Boyy By Malene Birger Benedetta Bruzziches Brandon Maxwell BY. Bonnie Young Bernhard Willhelm Brian Atwood Byredo Bertoni 1949 C Calvin Klein 205W39NYC Chanel Identification Cinq à Sept Calvin Klein Collection Charles Youssef Clare V. Camilla and Marc Charlotte Olympia Class Roberto Cavalli Camilla Elphick -

Georges Hobeika

dress: ZUHAIR MURAD necklace and earrings PIAGET IRIS VAN HERPEN ZUHAIR MURAD DIOR ZIAD NAKAD CHANEL JEAN-PAUL GAULTIER DIOR CHRISTOPHE JOSSE DiRECTOR Sandra Rondini [email protected] EDiTOR iN CHiEF Alessandra Safoue [email protected] EDiTORiAL COORDiNATOR Mariella Valdiserri [email protected] TREND RESEARCH Annalisa Campara [email protected] FRANCE CORRESPONDENT Francesco Rapazzini [email protected] CANADA CORRESPONDENT Sonia Giovinazzo [email protected] PHOTOGRAPHER iN CHiEF Daniele Cipriani [email protected] PHOTOGRAPHER Isshogai MARKETiNG ADVERTiSiNG Cinzia Ana Cortejosa [email protected] ADMiNiSTRATiON Noemi Manna [email protected] GRAPHiCS Lorenzo Stalfieri [email protected] EDiTORiAL TEAM Maria Cristina Rigano Fiorella Bellagotti TRANSLATOR Sonia Giovinazzo [email protected] EDiTORiAL OFFiCE ROME Via dei Platani, 126 00069, Rome Italy Phone (+39) 06 9997861 [email protected] STUDiO PRODUCTiONS Via Chiusa, 12 01100, Viterbo Italy Phone (+39) 0761 344545 [email protected] EDiTORiAL OFFiCE DUBAi P. O. Box 502511 Dubai Media City Phone (+971) 558917527 [email protected] PUBLiSHER Rocio Cortejosa [email protected] GIVENCHY CONTENTS 21 BON VOYAGE! 254 LIU CHAO 25 LOST MIND BY ISSHOGAI 258 IRIS VAN HERPEN 38 JEAN-PAUL GAULTIER 262 ASHI STUDIO 44 GALIA LAHAV 266 MAURIZIO GALANTE 50 GUO PEI 270 GEORGES CHAKRA 56 KITHE BREWSTER 278 YUMI KATSURA 60 NIHILO 284 VALENTINO 64 FRANCK SORBIER 294 RALPH & RUSSO 68 JULIEN FOURNIE 302 ANTONIO GRIMALDI 74 RAMI KADI 80 VICTOR & ROLF 86 ZUHAIR MURAD 94 DIDIT HEDIPRASETYO 100 CELIA KRITHARIOTI 106 ANTONIO ORTEGA 110 YANINA COUTURE 116 ALEXANDRE VAUTHIER 122 ELIE SAAB 132 APATRICK PHAM 138 ARMINE OHANYAN 142 ROMANCE WAS BORN 148 MARIA ARISTIDOU 152 AZULANT AKORA 156 REDEMPTION 162 PATUNA 166 EVA MINGE 174 XUAN 178 ARMANI PRIVÈ 192 ULYANA SERGEENKO 198 STEPHANE ROLLAND 204 ALEXIS MABILLE 212 CHANEL 222 GEORGE HOBEIKA 230 RONALD VAN DER KEMP 236 DIOR 246 FENDI ASHI STUDIO Com’era bello un tempo quando si era bambini partire per un viaggio in treno. -

Fashion's New Frontiers; What's Next

! ! !"#$%&'(#)*+,)!-&'.%+-#/)0$".(#)*+1.2)) FBS C19 Issue 3: 22.05.20 ! ! ! ROMA, LAZIO, ITALY Whilst the UN delegates discuss the issues of the climate of the planet in Paris, many cities of the world organised events and demonstrations for Earth's climate and nature. In Rome almost a million people took to the streets of the capital to take part in the Global climate march. [Photo by Davide Bosco/Pacific Press | LightRocket via Getty Images]! “I don’t really follow market research; I trust my instincts” Anna Wintour, Editor in Chief Vogue ! "! Context: Fashion has not been dormant or slumbering, and certainly not fast asleep, during lockdown. Many designers and creatives have been active in ideas, fund raising, communication and generally keeping busy. However, the loosening of the lockdown rules in several countries has resulted in many more people declaring potentially exciting new plans for the future, ways to engage with consumers and other innovative future facing initiatives. The main fashion organisations of London, Paris, and Italy; Rome Florence Milan, have been busy with many reassurances and actions during the past couple of months. Some of these plans are now coming to fruition, The fashion industry landscape is changing, fashion is thinking, and we are reporting on a cross section of new ideas, concepts and potential innovation routes now starting to appear. Statements being made by many in the creative industries are strong, positive and future forward, but realistic attitudes are still very much in evidence. Facts are facts and understanding the key realities of our situation is both important and multifaceted.