Securities Litigation & Regulation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Rapport Match

MATCH REPORT RAPPORTWALES VS IRELAND MATCH 25 - 7 SEASON SEASON samedi, 16. mars 2019 WALES VS IRELAND 25 - 7 samedi, 16. mars 2019 samedi, 16. mars 2019 Millennium Stadium Angus Gardner SEASON SEASON Wales 25 - 7 Ireland Hadleigh Parkes Jordan Larmour Rob Evans H Parkes Essais J Larmour Cian Healy Ken Owens Rory Best Tomas Francis G Anscombe Transformations J Carty Tadhg Furlong Adam Beard Tadgh Beirne Alun Wyn Jones G Anscombe (6) Pénalités James Ryan Josh Navidi Peter O'Mahony Justin Tipuric Drops Sean O'Brien Ross Moriarty CJ Stander Gareth DaviesWales POSSESSION ET OCCUPATION Ireland Conor Murray Gareth Anscombe Johnny Sexton Josh Adams Jacob Stockdale Jonathan Davies Bundee Aki 41% 44% 12.7 29:27 59% 56% 18.5 George North Garry Ringrose Liam Williams Keith Earls ElliotPossession Dee % Occupation % Minutes Attaque Temps de jeu Possession % Occupation % Minutes Attaque Nicky Smith effectif Dillon1 1 1 Lewis1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 0 1 1SEASON1 1 1 1 1 # 0 1 1 1 1 1 # Dave Kilcoyne SEASON Jake Ball Wales RESUME Ireland Andrew Porter Aaron Wainwright Quinn Roux ATTAQUE Dan BiggarXV DE DÉPART mins 57 Percussions 113 XV DE DÉPART mins Kieran Marmion Owen1 Rob Watkin Evans 54 231 Mètres Parcourus 478 1 Cian Healy 60 Jack Carty 2 Ken Owens 60 2 Franchissements 1 2 Rory Best 65 Gareth3 Tomas Anscombe Francis 54 73 Gain Ligne Avantage % 69 3 Tadhg Furlong 65 Jack Carty Rob4 EvansAdam Beard 70 24 (694) Jeu au Pied (Mètres) 17 (377) 4 Tadgh Beirne 58 Cian Healy Ken5 OwensAlun Wyn Jones 80 67 Passes 133 5 James Ryan 80 Rory -

Etymology of the Principal Gaelic National Names

^^t^Jf/-^ '^^ OUTLINES GAELIC ETYMOLOGY BY THE LATE ALEXANDER MACBAIN, M.A., LL.D. ENEAS MACKAY, Stirwng f ETYMOLOGY OF THK PRINCIPAL GAELIC NATIONAL NAMES PERSONAL NAMES AND SURNAMES |'( I WHICH IS ADDED A DISQUISITION ON PTOLEMY'S GEOGRAPHY OF SCOTLAND B V THE LATE ALEXANDER MACBAIN, M.A., LL.D. ENEAS MACKAY, STIRLING 1911 PRINTKD AT THE " NORTHERN OHRONIOLB " OFFICE, INYBRNESS PREFACE The following Etymology of the Principal Gaelic ISTational Names, Personal Names, and Surnames was originally, and still is, part of the Gaelic EtymologicaJ Dictionary by the late Dr MacBain. The Disquisition on Ptolemy's Geography of Scotland first appeared in the Transactions of the Gaelic Society of Inverness, and, later, as a pamphlet. The Publisher feels sure that the issue of these Treatises in their present foim will confer a boon on those who cannot have access to them as originally published. They contain a great deal of information on subjects which have for long years interested Gaelic students and the Gaelic public, although they have not always properly understood them. Indeed, hereto- fore they have been much obscured by fanciful fallacies, which Dr MacBain's study and exposition will go a long way to dispel. ETYMOLOGY OF THE PRINCIPAI, GAELIC NATIONAL NAMES PERSONAL NAMES AND SURNAMES ; NATIONAL NAMES Albion, Great Britain in the Greek writers, Gr. "AXfSiov, AX^iotv, Ptolemy's AXovlwv, Lat. Albion (Pliny), G. Alba, g. Albainn, * Scotland, Ir., E. Ir. Alba, Alban, W. Alban : Albion- (Stokes), " " white-land ; Lat. albus, white ; Gr. dA</)os, white leprosy, white (Hes.) ; 0. H. G. albiz, swan. -

Whyte, Alasdair C. (2017) Settlement-Names and Society: Analysis of the Medieval Districts of Forsa and Moloros in the Parish of Torosay, Mull

Whyte, Alasdair C. (2017) Settlement-names and society: analysis of the medieval districts of Forsa and Moloros in the parish of Torosay, Mull. PhD thesis. http://theses.gla.ac.uk/8224/ Copyright and moral rights for this work are retained by the author A copy can be downloaded for personal non-commercial research or study, without prior permission or charge This work cannot be reproduced or quoted extensively from without first obtaining permission in writing from the author The content must not be changed in any way or sold commercially in any format or medium without the formal permission of the author When referring to this work, full bibliographic details including the author, title, awarding institution and date of the thesis must be given Enlighten:Theses http://theses.gla.ac.uk/ [email protected] Settlement-Names and Society: analysis of the medieval districts of Forsa and Moloros in the parish of Torosay, Mull. Alasdair C. Whyte MA MRes Submitted in fulfillment of the requirements for the Degree of Doctor of Philosophy. Celtic and Gaelic | Ceiltis is Gàidhlig School of Humanities | Sgoil nan Daonnachdan College of Arts | Colaiste nan Ealain University of Glasgow | Oilthigh Ghlaschu May 2017 © Alasdair C. Whyte 2017 2 ABSTRACT This is a study of settlement and society in the parish of Torosay on the Inner Hebridean island of Mull, through the earliest known settlement-names of two of its medieval districts: Forsa and Moloros.1 The earliest settlement-names, 35 in total, were coined in two languages: Gaelic and Old Norse (hereafter abbreviated to ON) (see Abbreviations, below). -

Caverns Measureless to Man: Interdisciplinary Planetary Science & Technology Analog Research Underwater Laser Scanner Survey (Quintana Roo, Mexico)

Caverns Measureless to Man: Interdisciplinary Planetary Science & Technology Analog Research Underwater Laser Scanner Survey (Quintana Roo, Mexico) by Stephen Alexander Daire A Thesis Presented to the Faculty of the USC Graduate School University of Southern California In Partial Fulfillment of the Requirements for the Degree Master of Science (Geographic Information Science and Technology) May 2019 Copyright © 2019 by Stephen Daire “History is just a 25,000-year dash from the trees to the starship; and while it’s going on its wild and woolly but it’s only like that, and then you’re in the starship.” – Terence McKenna. Table of Contents List of Figures ................................................................................................................................ iv List of Tables ................................................................................................................................. xi Acknowledgements ....................................................................................................................... xii List of Abbreviations ................................................................................................................... xiii Abstract ........................................................................................................................................ xvi Chapter 1 Planetary Sciences, Cave Survey, & Human Evolution................................................. 1 1.1. Topic & Area of Interest: Exploration & Survey ....................................................................12 -

Barristers on Panel

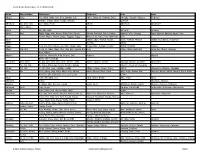

st Report Run Date: 21 Jun 2019 BARRISTERS ON PANEL The below list contains information on the number of payments* and the total amount paid to On Panel barristers for the period 1/07/18 – 31/12/18 Amount Number Amount Number Amount Number Amount Number Barrister Name Payable of Barrister Name Payable of Barrister Name Payable of Barrister Name Payable of (€) Payments (€) Payments (€) Payments (€) Payments Buckley, Declan 417,945 52 McGrath, Imogen 43,604 15 Binchy, Michael 11,132 8 Fitzpatrick, Andrew 3,094 6 Egan, Emily 394,952 24 Boughton, David 43,480 86 Farrelly, Aoife 10,908 13 Fitzgerald, William 2,653 11 Hanratty, Patrick 385,932 11 Fleck, Kieran 43,142 7 Delaney, Michael Patrick 10,701 2 MacMahon, Noel A. 2,583 1 Halpin, Conor 337,833 26 Gayer, Sasha Louise 39,452 4 Lydon, Eileen 10,578 2 Roberts, Conor 2,030 3 O'Braonain, Luan 231,215 17 Ramsey, Michael 37,023 1 Hand, Derry 10,376 8 Cheatle, John 1,845 1 Kavanagh, James M. 187,198 6 Fahey, Grainne 36,678 73 Scully, Lorraine 9,696 6 Maher, Jeremy 1,538 2 Foley, Brian 181,914 20 McGuinness, Donal 29,223 5 Hogan, John 9,545 7 Keleher, Daniel 1,162 1 Woulfe, Donnchadh 179,160 9 Lowe, Robert 28,226 2 Walsh, Aidan 8,979 1 Hewson, Dermot G. 1,119 1 McCrann, Oonah 159,623 18 Barrington, Eileen 27,596 2 Kilfeather, Jonathan 8,642 4 Keane, Deirdre 1,076 4 McCullough, Eoin 143,268 14 White, Rory 27,032 14 Fleming, David 8,107 2 Danaher, Gerard 954 2 Corcoran, Sarah 139,707 104 Farren, Georgina 25,227 5 Tennyson, Lauren 7,679 3 Cullinane, Padraig J. -

Transatlantic Connections 2 Confer - That He Made, and the Major Global and Transatlantic Projects He Is Currently Ence, 2015

GETTING TO BUNDORAN Located at Donegal’s most southerly point, Bundoran is the first stop as you enter the county from Sligo and Leitrim on the main N15 Sligo to Donegal Road. By Car By Coach Bundoran can be reached by the following routes: Bus Eireann’s Route 30 provides regular coach TRANSATLANTIC From Dublin via Cavan, Enniskillen N3 service from Dublin City and Dublin Airport From Dublin via Sligo N4 - N15 to Donegal. Get off the bus at Ballyshannon From Galway via Sligo N17 - N15 Station in County Donegal. Complimentary CONNECTIONS 2 From Belfast via Enniskillen M1 - A4 - A46 transfer from Ballyshannon to Bundoran; advanced booking necessary A Drew University Conference in Ireland buseireann.com SPECIAL THANKS Our sincere gratitude to the Institute of Study Abroad Ireland for its cooperation and partnership with Drew January 1 5–18, 2015 University. Many thanks also to Michael O’Heanaigh at Donegal County Council, Shane Smyth at Discover Bundoran, Martina Bromley and Joan Crawford at Failte Ireland, Gary McMurray for kind use of Bundoran, Donegal, Ireland cover photograph, Marc Geagan from North West Regional College, Tadhg Mac Phaidin and staff at Club Na Muinteori, Maura Logue, Marion Rose McFadden, Travis Feezell from University of the Ozarks, Tara Hoffman and Melvin Harmon at AFS USA, Kevin Lowery, Elizabeth Feshenfeld, Rebeccah Newman, Macken - zie Suess, and Lynne DeLade, all who made invaluable contributions to the organization of the conference. KEYNOTE SPEAKERS DON MULLAN “From Journey to Justice” Stories of Tragedy and Triumph from Bloody Sunday to the WWI Christmas Truces Thursday, 15 January • 8:30 p.m. -

Etymology of the Principal Gaelic National Names Personal Names

PR E F AC E. The following Outlines of Gaelic Etymology originally formed of was bound fir t G , , s part and up with the edition of the aelic , b E MacBain . tymological Dictionary by the late Dr The pu lisher, now thinking that there are students of the Language who might “ w a haLnd orm ish to have the Outlines in separate and y f , is here publishing them . S words b The upplement, the and letters in square rackets, and a few slight changes from the original are the work of the G u . H Rev Dr eorge enderson, Lect rer in Celtic Languages and r U G as ow wh o u d Literatu e in the niversity of l g , fo n it necessary to abandon his intention of seeing the Gaelic Etymological Dictionary through the press, after reaching the sixteenth page ” of these Outlines . OUTL INES OF GAEL IC ETYM OL OGY. G I t c AEL C belongs to the Celtic group of languages, and the Cel i is itself a branch of the Indo-Euro eam r A c 5 p vg ryan family of spee h for it has been found that the languages of Europe (with the e c H s and U o- x eption of Turkish, ungarian, Ba que, gr Finnish), and 1 t A c hose of sia from the Cau asus to Ceylon, resemble each other i n grammar and vocabulary to such an extent that they mus t all b e e consider d as descended from one parent or original tongue . -

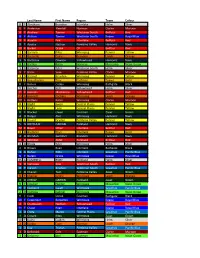

Last Name First Name Region Team Colour 8 F Abraham Brandon

Last Name First Name Region Team Colour 8 F Abraham Brandon Interlake Helm Silver 8 F Anderson Kendall Norman Clarke Maroon 8 F Andrew Tanner Westman South Belfour Red 8 F Ardron Tanner Westman South Keane Royal Blue 9 F Asselin Erik Interlake Belfour Red 8 F Ayotte Nathan Pembina Valley Hamonic Navy 10 F Barker Drake CP Belfour Red 2 D Barroso Riley Winnipeg Penner Yellow 8 F Barscello Caley Brandon Leach Orange 3 D Barteaux Dawson Yellowhead Hamonic Navy 8 F Bartley Rylan Norman Mosienko Neon Green 1 G Bateman Tyler Westman South Helm Silver 9 F Bazin Svan Pembina Valley Clarke Maroon 3 D Bazinet Brayden Winnipeg Penner Yellow 8 F Beauchemin Troy Eastman Toews Gold 8 F Behun Codey Winnipeg Bathgate Black 9 F Belcher Josh Yellowhead Helm Silver 11 F Belinski Mackenzie Yellowhead Belfour Red 35 G Bennett Zachary Winnipeg Leach Orange 10 F Bettens Rylan Winnipeg Clarke Maroon 8 F Blight Jaxon Central Plains Penner Yellow 9 F Blight Lane Central Plains Penner Yellow 8 F Blocker Owen Eastman Zajac Green 4 D Borger Alec Winnipeg Hamonic Navy 10 F Bound Dryden Pembina Valley Penner Yellow 5 D BOYCHUK DARIAN Parkland Hamonic Navy 12 F Boyer Ethan Interlake Belfour Red 2 D Bremner Rhys Interlake Toews Gold 2 D Brendan Gairdner Brandon Hamonic Navy 2 D BRINDLE ZANE Parkland Belfour Red 2 D Broda Tyler Winnipeg Helm Silver 2 D Brown Ryan Interlake Bathgate Black 1 G Buhay Riley Interlake Sawchuk Pacific Blue 9 F Burgin Drake Winnipeg Keane Royal Blue 35 G CAMPBELL RORY Parkland Helm Silver 3 D Campion Kyle Westman South Belfour Red 8 F Carson -

Given Name Alternatives for Irish Research

Given Name Alternatives for Irish Research Name Abreviations Nicknames Synonyms Irish Latin Abigail Abig Ab, Abbie, Abby, Aby, Bina, Debbie, Gail, Abina, Deborah, Gobinet, Dora Abaigeal, Abaigh, Abigeal, Gobnata Gubbie, Gubby, Libby, Nabby, Webbie Gobnait Abraham Ab, Abm, Abr, Abe, Abby, Bram Abram Abraham Abrahame Abra, Abrm Adam Ad, Ade, Edie Adhamh Adamus Agnes Agn Aggie, Aggy, Ann, Annot, Assie, Inez, Nancy, Annais, Anneyce, Annis, Annys, Aigneis, Mor, Oonagh, Agna, Agneta, Agnetis, Agnus, Una Nanny, Nessa, Nessie, Senga, Taggett, Taggy Nancy, Una, Unity, Uny, Winifred Una Aidan Aedan, Edan, Mogue, Moses Aodh, Aodhan, Mogue Aedannus, Edanus, Maodhog Ailbhe Elli, Elly Ailbhe Aileen Allie, Eily, Ellie, Helen, Lena, Nel, Nellie, Nelly Eileen, Ellen, Eveleen, Evelyn Eibhilin, Eibhlin Helena Albert Alb, Albt A, Ab, Al, Albie, Albin, Alby, Alvy, Bert, Bertie, Bird,Elvis Ailbe, Ailbhe, Beirichtir Ailbertus, Alberti, Albertus Burt, Elbert Alberta Abertina, Albertine, Allie, Aubrey, Bert, Roberta Alberta Berta, Bertha, Bertie Alexander Aler, Alexr, Al, Ala, Alec, Ales, Alex, Alick, Allister, Andi, Alaster, Alistair, Sander Alasdair, Alastar, Alsander, Alexander Alr, Alx, Alxr Ec, Eleck, Ellick, Lex, Sandy, Xandra, Zander Alusdar, Alusdrann, Saunder Alfred Alf, Alfd Al, Alf, Alfie, Fred, Freddie, Freddy Albert, Alured, Alvery, Avery Ailfrid Alberedus, Alfredus, Aluredus Alice Alc Ailse, Aisley, Alcy, Alica, Alley, Allie, Allison, Alicia, Alyssa, Eileen, Ellen Ailis, Ailise, Aislinn, Alis, Alechea, Alecia, Alesia, Aleysia, Alicia, Alitia Ally, -

Tuairimí an 23

T U A I R I M Í A N 2 3 L I S T E N U P F O R E C A S T S U M M E R 2 0 1 7 T E R N D S I R I S L E A B H A R R A N G 3 2 0 1 8 Nuacht Ginerálta Bás Anthony 'Axel' Foley Le Rory agus Donnhcadh Anthony Foley was a great man. He played rugby for Munster and Ireland. He was a legend, loved by his McGregor i NYC son's, wife, family and friends. He grew up to be a great manager. Munster had a game in Paris against Conor McGregor went to Racing Metro but Anthony Foley never woke up the court for attacking a day of the match. The following week the doctors said russian UFC fighter and a that Axel died of a heart attack. People from all over bus full of his teammates. He throw a trolly at a bus left flowers and jerseys on the fence at Thomond Park. with a Russian UFC There was a game the week after Anthony Foley died fighter in it and he in Thomond Park against the Glasgow Warriors. seriously injured him. He Munster won 31-13 in a game where Keith Earls was went to court and was in sent off. It was a very emotional game and the jail for a short while. He was released but had tp supporters made lots of noise to celebrate the life of pay $50,000. -

JFK Jr., Wife, Sister-In-Law Presumed Dead in Crash

The Phillies post 18 hits as they knock around the Red Sox, 11-3 – D1 LOTTERY, PAGE A2 THE WEATHER Volume 256 Today: Sunny, humid, 95 Tomorrow: Clouding up, 86 Number 18 Details, Page B4 $1.50 fghijkl *** SUNDAY, JULY 18, 1999 Inside A grim search JFK Jr., wife, sister-in-law presumed dead in crash By Mitchell Zuckoff and Matthew Brelis GLOBE STAFF Once again, John F. Kennedy Jr., who Moon struck crawled out from under his father’s anguish and Oval Office desk into a life of trage- Thirty years ago this week- dy-tinged celebrity, was presumed end during a summer ofsocial dead yesterday along with his wife disbelief upheaval, Americans watched and her sister when the small plane in awe and fascination as as- he was piloting apparently crashed By David M. Shribman tronauts walked on the moon. off Martha’s Vineyard. GLOBE STAFF Today, it is a memory they’ll Hope that the glamorous and never forget. B1 free-spirited member of the nation’s Even now, no words prompt so most chronicled political family had much anguish, so much grief, so simply made an unscheduled landing much disbeliefas these: John F. dimmed when wreckage and luggage Kennedy is were found off Philbin’s Beach at the Commentary dead. westernmost end ofthe island. A Those short walk down the beach is the words flew around the country yes- Vineyard home that Kennedy and his terday in frantic electronic pulses, sister inherited from their mother, though this time it was not news of Jacqueline Kennedy Onassis. -

Download This PDF File

THE BIG ANDTHE BIG AND THE LONG THE LONG FELLOW FELLOW Fearghal Mac Bhloscaidh Fearghal Mac Bhloscaidh formed the basis of the civil war. As Liam Mellows told the Dáil on 4 January 1922: ‘The people who are in favour of the Treaty are not in favour of the Treaty on its merits, but are in favour of the Treaty The Big and the Long because they fear what is to happen if it be rejected. That is not the will of the people, that is the fear of Fellow; or the Tragedy the people’.5 and Farce of the Irish In retrospect, two men appeared to dominate southern politics in the period. Michael Collins, the Big Counter-Revolution. Fellow, was one; the other, Eamon de Valera—the Tall Fellow—apparently believed that history would Fearghal McCluskey record Collins’ greatness at his own expense. Yet this traditional concentration on ‘great men’ ignores the fact that both did indeed make their own history, but under circumstances directly found, given, and transmitted from the past. Ireland and its dead generations clearly weighed like a nightmare on the In June 1920, the head of the British Army, Henry living. The calibre of leadership that emerged during Wilson, feared ‘the loss of Ireland to begin with; the counter-revolution arguably doubled the burden, the loss of empire in the second place; and the loss as the aborted class struggle in Ireland created of England itself to finish with.’1 Two years later, circumstances and relationships that made it possible with Wilson’s corpse barely cold, Michael Collins, for a pair of grotesque mediocrities to play the part of who apparently ordered his assassination, launched heroes—one at the tail end of the revolutionary crisis a civil war against his former republican comrades precipitated by World War I, the other on the coattails with British artillery.