201 ,QWHUQDWLRQDO 9Aluation Handbook ,QGXVWU\ Cost of Capital

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

May CARG 2020.Pdf

ISSUE 30 – MAY 2020 ISSUE 30 – MAY ISSUE 29 – FEBRUARY 2020 Promoting positive mental health in teenagers and those who support them through the provision of mental health education, resilience strategies and early intervention What we offer Calm Harm is an Clear Fear is an app to Head Ed is a library stem4 offers mental stem4’s website is app to help young help children & young of mental health health conferences a comprehensive people manage the people manage the educational videos for students, parents, and clinically urge to self-harm symptoms of anxiety for use in schools education & health informed resource professionals www.stem4.org.uk Registered Charity No 1144506 Any individuals depicted in our images are models and used solely for illustrative purposes. We all know of young people, whether employees, family or friends, who are struggling in some way with mental health issues; at ARL, we are so very pleased to support the vital work of stem4: early intervention really can make a difference to young lives. Please help in any way that you can. ADVISER RANKINGS – CORPORATE ADVISERS RANKINGS GUIDE MAY 2020 | Q2 | ISSUE 30 All rights reserved. No part of this publication may be reproduced or transmitted The Corporate Advisers Rankings Guide is available to UK subscribers at £180 per in any form or by any means (including photocopying or recording) without the annum for four updated editions, including postage and packaging. A PDF version written permission of the copyright holder except in accordance with the provision is also available at £360 + VAT. of copyright Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency, Barnard’s Inn, 86 Fetter Lane, London, EC4A To appear in the Rankings Guide or for subscription details, please contact us 1EN. -

Rightmove Plc, Winterhill (RMV:LN)

Rightmove Plc, Winterhill (RMV:LN) Real Estate/Real Estate Services Price: 737.40 GBX Report Date: September 22, 2021 Business Description and Key Statistics Rightmove operates as an online property portal. Co.'s segments Current YTY % Chg include The Agency, which includes resale and lettings property advertising services provided on Co.'s platforms and tenant Revenue LFY (M) 289 8.0 referencing and insurance products sold by Van Mildert Landlord EPS Diluted LFY 0.19 10.2 and Tenant Protection Limited; and The New Homes, which provides property advertising services to new home developers Market Value (M) 6,453 and housing associations on Co.'s platforms. Co.'s customers are primarily estate agents, lettings agents and new homes developers Shares Outstanding LFY (000) 875,062 advertising properties for sale and to rent in the United Kingdom. Book Value Per Share 0.05 EBITDA Margin % 75.10 Net Margin % 60.8 Website: www.rightmove.co.uk Long-Term Debt / Capital % 20.3 ICB Industry: Real Estate Dividends and Yield TTM 0.04 - 0.61% ICB Subsector: Real Estate Services Payout Ratio TTM % 34.9 Address: 2 Caldecotte Lake;Business Park;Caldecotte Lake Drive 60-Day Average Volume (000) 1,679 Milton Keynes 52-Week High & Low 746.80 - 555.80 GBR Employees: 538 Price / 52-Week High & Low 0.99 - 1.33 Price, Moving Averages & Volume 756.4 756.4 Rightmove Plc, Winterhill is currently trading at 737.40 which is 4.4% above its 50 day 730.1 730.1 moving average price of 706.13 and 15.3% above its 703.8 703.8 200 day moving average price of 639.56. -

KOSPI 200 (Stock Code: 4520)

Supplemental Listing Document If you are in any doubt about this document, you should consult your stockbroker or other registered dealer in securities, bank manager, solicitor, accountant or other professional adviser. The Stock Exchange of Hong Kong Limited (the “Stock Exchange”) and Hong Kong Securities Clearing Company Limited (“HKSCC”) take no responsibility for the contents of this document, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this document. Placing of 370,000,000 European Style (Cash Settlement) Put Warrants 2006 relating to the KOSPI 200 (Stock Code: 4520) exercisable only on 15 September 2006 issued by SGA Société Générale Acceptance N.V. (incorporated in the Netherlands Antilles with limited liability) unconditionally and irrevocably guaranteed by Société Générale (incorporated in France) Strike Level: 184.50 This document is published for the purpose of obtaining a listing of all the above warrants (the “Warrants”) to be issued by SGA Société Générale Acceptance N.V. (the “Issuer”) and unconditionally and irrevocably guaranteed by Société Générale (“Société Générale” or the “Guarantor”), is supplemental to and should be read in conjunction with a base listing document published on 6 May 2005 (the “Base Listing Document”) and an addendum published on 13 October 2005 (the “Addendum”) and contains particulars given in compliance with the Rules Governing the Listing of Securities on the Stock Exchange (the "Rules") for the purpose of giving information with regard to the Issuer, the Guarantor and the Warrants. -

Possibilities of Applying Markowitz Portfolio Theory on the Croatian Capital Market

POSSIBILITIES OF APPLYING MARKOWITZ PORTFOLIO THEORY ON THE CROATIAN CAPITAL MARKET Dubravka Pekanov Starčević, Ph.D. J. J. Strossmayer University of Osijek, Faculty of Economics in Osijek E-mail: [email protected] Ana ZRNIć, Ph.D. Student, J. J. Strossmayer University of Osijek, Faculty of Economics in Osijek E-mail: [email protected] Tamara Jakšić, BEcon, student J. J. Strossmayer University of Osijek, Faculty of Economics in Osijek E-mail: [email protected] POSSIBILITIES OF APPLYING MARKOWITZ PORTFOLIO THEORY ON THE CROATIAN CAPITAL... MARKOWITZ PORTFOLIO THEORY ON THE CROATIAN POSSIBILITIES OF APPLYING Abstract In order to achieve the maximum possible profit by taking the lowest possible risk, investors build a stock portfolio consisting of a specific number of stocks which, according to the principle of diversification, significantly reduce the risk of loss. To build a portfolio, in developed capital markets investors have used the Markowitz portfolio optimization model for many years that enables us to find an optimal risk-return trade-off by selecting certain stock combinations. Despite the development of the Zagreb Stock Exchange, i.e., the central trading venue in the Republic of Croatia, the Croatian capital market is still under- developed. It is characterized by numerous shortcomings such as low liquidity, lack of transparency, high stock price volatility and insufficient traffic. Accord- ingly, the aim of this paper is to provide an insight into the functioning of the Dubravka Pekanov Starčević • Ana Zrnić • Tamara Jakšić: Dubravka Pekanov Starčević • Ana Zrnić Tamara 520 Croatian capital market and to examine the possibility of building an optimal stock portfolio by using the Markowitz model. -

2006 FIRST Annual Report

annual report For Inspiration & Recognition of Science & Technology 2006 F I R Dean Kamen, FIRST Founder John Abele, FIRST Chairman President, DEKA Research & Founder Chairman, Retired, Development Corporation Boston Scientific Corporation S Recently, we’ve noticed a shift in the national conversation about our People are beginning to take the science problem personally. society’s lack of support for science and technology. Part of the shift is in the amount of discussion — there is certainly an increase in media This shift is a strong signal for renewed commitment to the FIRST T coverage. There has also been a shift in the intensity of the vision. In the 17 years since FIRST was founded, nothing has been more conversation — there is clearly a heightened sense of urgency in the essential to our success than personal connection. The clearest example calls for solutions. Both these are positive developments. More is the personal commitment of you, our teams, mentors, teachers, parents, awareness and urgency around the “science problem” are central to sponsors, and volunteers. For you, this has been personal all along. As the FIRST vision, after all. However, we believe there is another shift more people make a personal connection, we will gain more energy, happening and it has enormous potential for FIRST. create more impact, and deliver more success in changing the way our culture views science and technology. If you listen closely, you can hear a shift in the nature of the conversation. People are not just talking about a science problem and how it affects This year’s Annual Report echoes the idea of personal connections and P02: FIRST Robotics Competition someone else; they are talking about a science problem that affects personal commitment. -

Study on the Competitiveness of the EU Gas Appliances Sector

Ref. Ares(2015)2495017 - 15/06/2015 Study on the Competitiveness of the EU Gas Appliances Sector Within the Framework Contract of Sectoral Competitiveness Studies – ENTR/06/054 Final Report Client: Directorate-General Enterprise & Industry Rotterdam, 11 August 2009 Disclaimer: The views and propositions expressed herein are those of the experts and do not necessarily represent any official view of the European Commission or any other organisations mentioned in the Report ECORYS SCS Group P.O. Box 4175 3006 AD Rotterdam Watermanweg 44 3067 GG Rotterdam The Netherlands T +31 (0)10 453 88 16 F +31 (0)10 453 07 68 E [email protected] W www.ecorys.com Registration no. 24316726 ECORYS Macro & Sector Policies T +31 (0)31 (0)10 453 87 53 F +31 (0)10 452 36 60 Table of contents 1 Introduction 1 2 Objectives and policy rationale 5 3 Main findings and conclusions 7 4 The gas appliances sector 11 4.1 Introduction 11 4.2 Definition 11 4.3 Overview of sub-sectors 16 4.3.1 Heating, ventilation and air conditioning (HVAC) 16 4.3.2 Domestic appliances 18 4.3.3 Fittings 20 4.4 The application of statistics 22 4.5 Statistical approach to sector and subsectors 23 5 Key characteristics of the European gas appliances sector 29 5.1 Introduction 29 5.2 Importance of the sector 30 5.2.1 Output 30 5.2.2 Employment 31 5.2.3 Demand 32 5.3 Production, employment, demand and trade within EU 33 5.3.1 Production share EU-27 output per country 33 5.3.2 Employment 39 5.3.3 Demand by Member State 41 5.3.4 Intra EU trade in GA 41 5.4 Industry structure and size distribution -

2014 ESG Integrated Ratings of Public Companies in Korea

2014 ESG Integrated Ratings of public companies in Korea Korea Corporate Governance Service(KCGS) annouced 2014 ESG ratings for public companies in Korea on Aug 13. With the ESG ratings, investors may figure out the level of ESG risks that companies face and use them in making investment decision. KCGS provides four ratings for each company which consist of Environmental, Social, Governance and Integrated rating. ESG ratings by KCGS are graded into seven levels: S, A+, A, B+, B, C, D. 'S' rating means that a company has all the system and practices that the code of best practices requires and there hardly exists a possibility of damaging shareholder value due to ESG risks. 'D' rating means that there is a high possibility of damaging shareholder value due to ESG risks. Company ESG Integrated Company Name Code Rating 010950 S-Oil Corporation A+ 009150 Samsung Electro-Mechanics Co., Ltd. A+ 000150 DOOSAN CORPORATION A 000210 Daelim Industrial Co., Ltd. A 000810 Samsung Fire & Marine Insurance Co., Ltd. A 001300 Cheil Industries Inc. A 001450 Hyundai Marine&Fire Insurance Co., Ltd. A 005490 POSCO. A 006360 GS Engineering & Construction Corp. A 006400 SAMSUNG SDI Co., Ltd. A 010620 Hyundai Mipo Dockyard Co., Ltd. A 011070 LG Innotek Co., Ltd. A 011170 LOTTE CHEMICAL CORPORATION A 011790 SKC Co., Ltd. A 012330 HYUNDAI MOBIS A 012450 Samsung Techwin Co., Ltd. A 023530 Lotte Shopping Co., Ltd. A 028050 Samsung Engineering Co., Ltd. (SECL) A 033780 KT&G Corporation A 034020 Doosan Heavy Industries & Construction Co., Ltd. A 034220 LG Display Co., Ltd. -

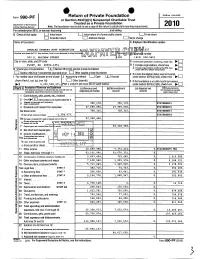

Form 990-P F Return of Private Foundation

Private Foundation OMB No 1545-0052 Form 990-P F Return of or Section 4947(a)(1) Nonexempt Charitable Trust Department of the Treasury Treated as a Private Foundation internal Revenue Service Note. The foundation may be able to use a copy of this return to satisfy state reporting requirements. 2010 For calendar year 2010 , or tax year beginning , and ending G Check all that apply. IInitial return L-J Initial return of a former public charity L-J Final return 0 Amended return 0 Address change 0 Name change Name of foundation A Employer identification number CHARLES STEWART MOTT FOUNDATION `V/ D ( 1 1227 Number and street (or P O box number if mail is not delivered to street addr I r v { suV a) epho number 503 S. SAGINAW STREET u 1 2000 `J (810) 238-5651 C if exemption application is check City or town, state, and ZIP code pend i ng, here _ ► FLINT , MI 48502-1851 0 1- Foreign organizations, check here 2. 85% test H Check type of organization: x Section 501(c)(3) exempt private foundation Fcine there and attach computation 4947(a)(1) nonexem pt charitable trust 0 Other taxable private foundation 0 Section E If private foundation status was terminated Fair market value of all assets at end of year J Accounting method: L-J Cash x Accrual I under section 507(b)(1)(A), check here ► ^ (from Part ll, col. (c), line 16) 0 Other (specify) F If the foundation is in a 60-month termination 2, 230 528 471. -

87198 Construction 2025 V2.Indd

www.bre.co.uk Meeting Construction 2025 Targets The positive impact of BRE Group products and services Construction 2025 is the joint strategy from government and industry for the future of the UK construction industry This document summarises the positive impacts in respect of these targets, Lower costs of a selection of products Industrial Strategy: government and industry in partnership BREEAM CLIP and services developed by the BRE Group. Brief average saved 150 descriptions of the projected companies a total products – BREEAM, savings of of £56 million Construction 2025 CALIBRE, CLIP and 22.56% SMARTWaste – and of BRE are also included. July 2013 Buildings assessed under Since 2003 BRE’s Construction BREEAM 2011 New Lean Improvement Construction enjoy average Programme (CLIP) has projected savings of 22.56% saved 150 companies a on their energy bills.1 total of £56 million. Construction 2025 sets out challenging construction targets for 2025 that include: CALIBRE SMARTWaste improvement in 50% exports 10% cost saving savings could equates to be £1.4 million 33% lower costs £1,144 2 per in 2015 and £1.7 house million in 20166 50% lower emissions A 10% cost saving can be Companies have saved around achieved by using CALIBRE 20% of waste going to landfill to identify non-value added by using SMARTWaste. This faster delivery activities on housing projects. is the equivalent to £1.2 50% 7 This equates to savings million a year. If this level of of around £1,1442 per waste diversion continued, house. Savings for housing then future cost savings projects using CALIBRE in could be £1.4 million in 2015 Improvement in 2013 are estimated to be and £1.7 million in 20166. -

001 Emma the Bunny #006 Georgina the Hippo #011 Germaine

#001 #002 #003 #004 #005 Emma the bunny Alexandre the russian Piotr the polar bear Bridget the elephant Simon the sheep blue cat #006 #007 #008 #009 #010 Georgina the hippo Seamus the alpaca Austin the rhino Rufus the lion Richard the large white pig #011 #012 #013 #014 #015 Germaine the gorilla Winston the aardvark Penelope the bear Hank the dorset Fiona the panda down sheep #016 #017 #018 #019 #020 Juno the siamese cat Angharad the donkey Benedict the chimpanzee Samuel the koala Douglas the highland cow #021 #022 #023 #024 #025 Laurence the tiger Chardonnay the Claudia the Alice the zebra Audrey the nanny goat palomino pony saddleback pig #026 #027 #028 #029 #030 Clarence the bat Martin the tabby cat Sarah the friesian cow Timmy the jack russell Caitlin the giraffe #031 #032 #033 #034 #035 Esme the fox Blake the orangutan Siegfried the monkey Boris the red squirrel Hamlet the cheetah #036 #037 #038 #039 #040 Francis the hedgehog Jessie the raccoon Bradlee the grey squirrel Noah the zwartbles sheep Christophe the wolf #041 #042 #043 #044 #045 Sheila the kangaroo Andre the lemur Erica the Frank the armadillo Mae the snow leopard dromedary camel #046 #047 #048 #049 #050 Harriet the sloth Susan the badger Zack the skunk Donna the reindeer Logan the moose #051 #052 #053 #054 #055 Simone the suri alpaca Fred the herdwick sheep Eustice the beltex sheep Tobias the Seth the hebridean sheep wensleydale sheep #056 #057 #058 #059 #060 Tracy the racka sheep Xavier the gibbon Sid the giant anteater Caroline the platypus Harold the teeswater sheep -

Sleep and Nesting Behavior in Primates: a Review

Received: 29 July 2017 | Revised: 30 November 2017 | Accepted: 2 December 2017 DOI: 10.1002/ajpa.23373 REVIEW ARTICLE Sleep and nesting behavior in primates: A review Barbara Fruth1,2,3,4 | Nikki Tagg1 | Fiona Stewart2 1Centre for Research and Conservation/ KMDA, Antwerp, Belgium Abstract 2Faculty of Science/School of Natural Sleep is a universal behavior in vertebrate and invertebrate animals, suggesting it originated in the Sciences and Psychology, Liverpool John very first life forms. Given the vital function of sleep, sleeping patterns and sleep architecture fol- Moores University, United Kingdom low dynamic and adaptive processes reflecting trade-offs to different selective pressures. 3 Department of Developmental and Here, we review responses in sleep and sleep-related behavior to environmental constraints Comparative Psychology, Max-Planck- across primate species, focusing on the role of great ape nest building in hominid evolution. We Institute for Evolutionary Anthropology, Leipzig, Germany summarize and synthesize major hypotheses explaining the proximate and ultimate functions of 4Faculty of Biology/Department of great ape nest building across all species and subspecies; we draw on 46 original studies published Neurobiology, Ludwig Maximilians between 2000 and 2017. In addition, we integrate the most recent data brought together by University of Munich, Germany researchers from a complementary range of disciplines in the frame of the symposium “Burning the midnight oil” held at the 26th Congress of the International Primatological Society, Chicago, Correspondence Barbara Fruth, Liverpool John Moores August 2016, as well as some additional contributors, each of which is included as a “stand-alone” University, Faculty of Science/NSP, article in this “Primate Sleep” symposium set. -

Korean Multinationals Show Solid Recovery After Global Crisis

Korean multinationals show solid recovery after global crisis Report dated November 16, 2010 EMBARGO: The contents of this report must not be quoted or summarized in the print, broadcast or electronic media before November 16, 2010, 10:00 a.m. Seoul; 1 a.m. GMT, and 9:00 p.m. November 15, 2010, New York. Seoul and New York, November 16, 2010 The Institute of International Affairs of the Graduate School of International Studies (GSIS) at Seoul National University in Seoul, and the Vale Columbia Center on Sustainable International Investment (VCC) at Columbia University in New York, are releasing the first annual report on leading Korean multinationals. The research for this report was conducted in 2010 and covers the period 2007 to 2009. 1 Highlights The Republic of Korea (henceforth ‘Korea’), the 11 th largest economy in the world, has now become one of the leading investors abroad. The number and the size of the corporate giants that dominate the economy have increased over the years, boosting and diversifying their investments around the world. Korea’s multinational enterprises ranked by their foreign assets (see table 1 below) show about USD 93 billion in assets held abroad. 2 Samsung Electronics Co., Ltd. (SEC), a member of a leading Korean conglomerate, ranked 1 st with slightly over USD 18 billion, followed by another top conglomerate member, LG Electronics, with over USD 10 billion dollars. Hyundai Heavy Industries Co., Ltd, and DSME Co., Ltd, had foreign assets of over USD 8 billion each and LG Display had over USD 6 billion. The top five firms together accounted for just over half of the total foreign assets of the top 20 companies.