Real Vs. Personal Property in This Section You'll Learn The

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Real Estate Marketplace Glossary: How to Talk the Talk

Federal Trade Commission ftc.gov The Real Estate Marketplace Glossary: How to Talk the Talk Buying a home can be exciting. It also can be somewhat daunting, even if you’ve done it before. You will deal with mortgage options, credit reports, loan applications, contracts, points, appraisals, change orders, inspections, warranties, walk-throughs, settlement sheets, escrow accounts, recording fees, insurance, taxes...the list goes on. No doubt you will hear and see words and terms you’ve never heard before. Just what do they all mean? The Federal Trade Commission, the agency that promotes competition and protects consumers, has prepared this glossary to help you better understand the terms commonly used in the real estate and mortgage marketplace. A Annual Percentage Rate (APR): The cost of Appraisal: A professional analysis used a loan or other financing as an annual rate. to estimate the value of the property. This The APR includes the interest rate, points, includes examples of sales of similar prop- broker fees and certain other credit charges erties. a borrower is required to pay. Appraiser: A professional who conducts an Annuity: An amount paid yearly or at other analysis of the property, including examples regular intervals, often at a guaranteed of sales of similar properties in order to de- minimum amount. Also, a type of insurance velop an estimate of the value of the prop- policy in which the policy holder makes erty. The analysis is called an “appraisal.” payments for a fixed period or until a stated age, and then receives annuity payments Appreciation: An increase in the market from the insurance company. -

Business Personal Property

FAQs Business Personal Property What is a rendition for Business Personal Property? A rendition is simply a form that provides the District with the description, location, cost, and acquisition dates for personal property that you own. The District uses the information to help estimate the market value of your property for taxation purposes. Who must file a rendition? Renditions must be filed by: Owners of tangible personal property that is used for the production of income Owners of tangible personal property on which an exemption has been cancelled or denied What types of property must be rendered? Business owners are required by State law to render personal property that is used in a business or used to produce income. This property includes furniture and fixtures, equipment, machinery, computers, inventory held for sale or rental, raw materials, finished goods, and work in progress. You are not required to render intangible personal property (property that can be owned but does not have a physical form) such as cash, accounts receivable, goodwill, application computer software, and other similar items. If your organization has previously qualified for an exemption that applies to personal property, for example, a religious or charitable organization exemption, you are not required to render the exempt property. When and where must the rendition be filed? The last day to file your rendition is April 15 annually. If you mail your rendition, it must be postmarked by the U. S. Postal Service on or before April 15. Your rendition must be filed at the appraisal district office in the county in which the business is located, unless the personal property has situs in a different county. -

REAL ESTATE LAW LESSON 1 OWNERSHIP RIGHTS (IN PROPERTY) Real Estate Law Outline LESSON 1 Pg

REAL ESTATE LAW LESSON 1 OWNERSHIP RIGHTS (IN PROPERTY) Real Estate Law Outline LESSON 1 Pg Ownership Rights (In Property) 3 Real vs Personal Property 5 . Personal Property 5 . Real Property 6 . Components of Real Property 6 . Subsurface Rights 6 . Air Rights 6 . Improvements 7 . Fixtures 7 The Four Tests of Intention 7 Manner of Attachment 7 Adaptation of the Object 8 Existence of an Agreement 8 Relationships of the Parties 8 Ownership of Plants and Trees 9 Severance 9 Water Rights 9 Appurtenances 10 Interest in Land 11 Estates in Land 11 Allodial System 11 Kinds of Estates 12 Freehold Estates 12 Fee Simple Absolute 12 Defeasible Fee 13 Fee Simple Determinable 13 Fee Simple Subject to Condition Subsequent 14 Fee Simple Subject to Condition Precedent 14 Fee Simple Subject to an Executory Limitation 15 Fee Tail 15 Life Estates 16 Legal Life Estates 17 Homestead Protection 17 Non-Freehold Estates 18 Estates for Years 19 Periodic Estate 19 Estates at Will 19 Estate at Sufferance 19 Common Law and Statutory Law 19 Copyright by Tony Portararo REV. 08-2014 1 REAL ESTATE LAW LESSON 1 OWNERSHIP RIGHTS (IN PROPERTY) Types of Ownership 20 Sole Ownership (An Estate in Severalty) 20 Partnerships 21 General Partnerships 21 Limited Partnerships 21 Joint Ventures 22 Syndications 22 Corporations 22 Concurrent Ownership 23 Tenants in Common 23 Joint Tenancy 24 Tenancy by the Entirety 25 Community Property 26 Trusts 26 Real Estate Investment Trusts 27 Intervivos and Testamentary Trusts 27 Land Trust 27 TEST ONE 29 TEST TWO (ANNOTATED) 39 Copyright by Tony Portararo REV. -

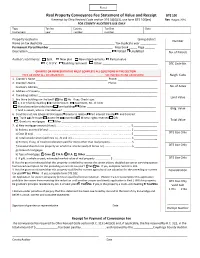

Real Property Conveyance Fee Statement of Value and Receipt

Real Property Conveyance Fee Statement of Value and Receipt DTE 100 If exempt by Ohio Revised Code section 319.54(G)(3), use form DTE 100(ex) Rev 1/14 FOR COUNTY AUDITOR’S USE ONLY Type Tax list County Tax Dist Date Instrument year number number Property located in ____________________________________________________________ taxing district Number Name on tax duplicate ____________________________________________ Tax duplicate year __________ Permanent Parcel Number _______________________________________ Map book _____ Page ______ Description ___________________________________________________ Platted Unplatted No. of Parcels Auditor’s comments: Split New plat New improvements Partial value C.A.U.V. Building removed Other __________________________________ DTE Code No. GRANTEE OR REPRESENTATIVE MUST COMPLETE ALL QUESTIONS IN THIS SECTION TYPE OR PRINT ALL INFORMATION SEE INSTRUCTIONS ON REVERSE Neigh. Code 1. Grantor’s Name _________________________________________________ Phone: ___________________________ 2. Grantee’s Name _________________________________________________ Phone: ___________________________ Grantee’s Address__________________________________________________________________________________ No. of Acres 3. Address of Property ________________________________________________________________________________ 4. Tax billing address _________________________________________________________________________________ Land Value 5. Are there buildings on the land? Yes No If yes, Check type: 1, 2 or 3 family dwelling Condominium -

Conveyancing and the Law of Real Property

September 2014 - ISSUE 19 Conveyancing and The Law of Real Property The questions may be asked what is Conveyancing and why is Property Rules and his first act must be to undertake an inves‐ it attached to the Law of Real Property. tigation into the title of the Vendor’s property. This search which must be conducted in the Register of Deeds and should When dealing with the Law of Real Property there are two involve a period of time of thirty years or longer in the case fundamental points which must be understood‐‐‐ where the date of the Vendor’s Deed is older than thirty years. (i) You acquire knowledge of the rights and liabilities attached to the interests of the owner in the land and The Cause List search is undertaken in the Supreme Court Registry and the purpose of which is to ascertain whether (ii) The foundation of the Rules of Conveyancing. there are any liens pending against the Vendor in the Su‐ preme Court Register. If there are pending liens, they must be It is not easy to distinguish accurately between Real Property settled by the Vendor before he is able to sell the property. and Conveyancing. It is said that Real Property deals with the rights and liabilities of land owners. Conveyancing on the The original documents of title must be produced by the Ven‐ other hand is the art of creating and transferring rights in land dor and delivered to the attorney for review. I the Vendor is and thus the Rules of Conveyancing and the Law of Real Prop‐ unable to produce the same and the attorney has found the erty cannot be distinguished as separate subjects though re‐ title to be good and marketable, then the Vendor must sign lated closely but should be distinguished as two parts of one and swear an Affidavit of Loss in respect of such lost or mis‐ subject of land law. -

Real & Personal Property

CHAPTER 5 Real Property and Personal Property CHRIS MARES (Appleton, Wsconsn) hen you describe property in legal terms, there are two types of property. The two types of property Ware known as real property and personal property. Real property is generally described as land and buildings. These are things that are immovable. You are not able to just pick them up and take them with you as you travel. The definition of real property includes the land, improvements on the land, the surface, whatever is beneath the surface, and the area above the surface. Improvements are such things as buildings, houses, and structures. These are more permanent things. The surface includes landscape, shrubs, trees, and plantings. Whatever is beneath the surface includes the soil, along with any minerals, oil, gas, and gold that may be in the soil. The area above the surface is the air and sky above the land. In short, the definition of real property includes the earth, sky, and the structures upon the land. In addition, real property includes ownership or rights you may have for easements and right-of-ways. This may be for a driveway shared between you and your neighbor. It may be the right to travel over a part of another person’s land to get to your property. Another example may be where you and your neighbor share a well to provide water to each of your individual homes. Your real property has a formal title which represents and reflects your ownership of the real property. The title ownership may be in the form of a warranty deed, quit claim deed, title insurance policy, or an abstract of title. -

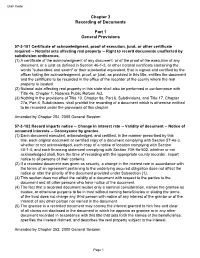

Chapter 3 Recording of Documents Part 1 General Provisions

Utah Code Chapter 3 Recording of Documents Part 1 General Provisions 57-3-101 Certificate of acknowledgment, proof of execution, jurat, or other certificate required -- Notarial acts affecting real property -- Right to record documents unaffected by subdivision ordinances. (1) A certificate of the acknowledgment of any document, or of the proof of the execution of any document, or a jurat as defined in Section 46-1-2, or other notarial certificate containing the words "subscribed and sworn" or their substantial equivalent, that is signed and certified by the officer taking the acknowledgment, proof, or jurat, as provided in this title, entitles the document and the certificate to be recorded in the office of the recorder of the county where the real property is located. (2) Notarial acts affecting real property in this state shall also be performed in conformance with Title 46, Chapter 1, Notaries Public Reform Act. (3) Nothing in the provisions of Title 10, Chapter 9a, Part 6, Subdivisions, and Title 17, Chapter 27a, Part 6, Subdivisions, shall prohibit the recording of a document which is otherwise entitled to be recorded under the provisions of this chapter. Amended by Chapter 254, 2005 General Session 57-3-102 Record imparts notice -- Change in interest rate -- Validity of document -- Notice of unnamed interests -- Conveyance by grantee. (1) Each document executed, acknowledged, and certified, in the manner prescribed by this title, each original document or certified copy of a document complying with Section 57-4a-3, whether or not acknowledged, each copy of a notice of location complying with Section 40-1-4, and each financing statement complying with Section 70A-9a-502, whether or not acknowledged shall, from the time of recording with the appropriate county recorder, impart notice to all persons of their contents. -

Purchase Price Allocation in Real Estate Transactions

PURCHASE PRICE ALLOCATION IN REAL ESTATE TRANSACTIONS: Does A + B + C Always Equal Value? Morris A. Ellison, Esq. 1 Womble Carlyle Sandridge & Rice, LLP Nancy L. Haggerty, Esq. Michael Best & Friedrich, LLP Purchasers of income-generating real estate generally focus solely on cash flow rather than the individual components generating that cash flow. This seeming truism has not been true either for larger transactions involving substantial personal property or goodwill or in the context of ad valorem taxation where taxing authorities generate separate tax bills, often at different rates, for real property, personal property and business licensing fees. This proposition is becoming less true in the current economic environment, as lenders face increasing regulatory pressure to “take less risk” by separately valuing the components generating the income and valuing the risk separately. Originating primarily in the context of valuing hotel properties for proper determination of the project’s real estate value for ad valorem tax purposes, the concept of component analysis has far broader applications. The Appraisal Institute 2 currently includes as potential additional candidates for component analysis: (i) health care facilities such as hospitals, nursing homes and ambulatory surgical centers; (ii) regional shopping centers, office buildings and apartments; (iii) restaurants and nightclubs; (iv) recreational facilities such as theme parks, theaters, sports venues and golf courses; and (v) manufacturing firms. 3 The purpose of this paper is not to present a study of component analysis bur rather to identify some of the areas where component analysis should be considered. The Concept of Component Analysis Investors typically look primarily at total cash flow without attributing cash flow to specific components. -

SECTION 1.0 Summary of California Water Rights

SECTION 1.0 Summary of California Water Rights 1.1 Types of Water Rights In California, the different types of water rights include: 1.1.1 Prescriptive Water use rights gained by trespass or unauthorized taking that ripen into a title, on a par with rights to land gained through adverse possession.1 1.1.2 Pueblo A water right possessed by a municipality that, as a successor of a Spanish-law pueblo, is entitled to the beneficial use of all needed, naturally occurring surface and groundwater of the original pueblo watershed.2 1.1.3 Groundwater The Dictionary of Real Estate Appraisal, defines groundwater as “all water that has seeped down beneath the surface of the ground or into the subsoil; water from springs or wells.”3 This is an adequate working definition if the “springs or” is eliminated because once water issues out of a spring it becomes surface water, not groundwater. As is also indicated in the following text, it is not water flowing in an underground channel. Groundwater should be thought of as the water that occupies the space between soil particles beneath the surface of the land. Groundwater is extracted exclusively by means of wells. Whenever groundwater reaches the surface in a natural manner, whether through springs or seepage into a surface water stream channel or lake, it ceases to be groundwater and becomes surface water. The jurisdiction of the SWRCB [State Water Resources Control Board] to issue permits and licenses for appropriation of underground water is limited by section 1200 of the California Water Code to “subterranean streams flowing through known and definite channels.” If use of underground water on nonoverlying land is proposed and the source of the water is a subterranean stream flowing in a known and definite channel, an application pursuant to the California Water Code is required. -

Booklet 2 Housing Code Checklist (March 2021)

Representing Yourself in an Eviction Case Housing Code Checklist with Key Provisions of the State Sanitary Code In Massachusetts, the state Sanitary Code is the main law that gives tenants a right to decent housing. All rental housing must at least meet the state Sanitary Code. The Housing Code Checklist will help you protect your right to safe and decent housing. You can also use the state Sanitary Code to defend against an eviction because a tenant’s duty to pay rent is based on the landlord’s duty to keep the apartment in good condition. The Sanitary Code defines what is good condition. If you are facing an eviction for nonpayment of rent or a no-fault eviction, the checklist can help you prepare your case. A no-fault eviction is where a landlord is evicting a tenant who has done nothing wrong. If you can prove to a judge the landlord knew about the bad conditions before you stopped paying rent, the judge may not order you to move. A judge might order you to pay only some of the rent the landlord claims you owe. Or, the judge may order the landlord to pay you money because you lived with such bad conditions. The landlord may have to pay you even if the problems were fixed. The judge may also order the landlord to make repairs. The right column of the Housing Code Checklist refers to the law. In most cases, it is the Sanitary Code in the Code of Massachusetts Regulations (C.M.R.). See the Sanitary Code online: www.mass.gov/eohhs/docs/dph/regs/105cmr410.pdf. -

Real Property Conveyance Fee

Real Property Conveyance Fee tate law establishes a mandatory conveyance fee that is exempt from federal income taxation, when on the transfer of real property. The fee is calculated the transfer is without consideration and furthers the Sbased on a percentage of the property value that is agency’s charitable or public purpose. transferred. In addition to the mandatory fee, all but one • when property is sold to provide or release security county levies a permissive real property transfer fee. The for a debt, or for delinquent taxes, or pursuant to a revenue from both the mandatory fee and the permissive court order. fee is deposited in the general fund of the county in which • when a corporation transfers property to a stock the property is located - no revenue goes to the state. In holder in exchange for their shares during a corporate 2013, the latest year for which data is available, convey reorganization or dissolution. ance fees generated approximately $108.7 million in rev • when property is transferred by lease, unless the enues to counties: $34.0 million from mandatory fees and lease is for a term of years renewable forever. $74.7 million from permissive fees. • to a grantee other than a dealer, solely for the pur pose of, and as a step in, the prompt sale to others. Taxpayer • to sales or transfers to or from a person when no (Ohio Revised Code 319.202 and 322.06) money or other valuable and tangible consideration The real property conveyance fee is paid by persons readily convertible into money is paid or is to be paid who make sales of real estate or used manufactured for the realty, and the transaction is not a gift. -

Condominium Ownership of Real Property

CHAPTER 47-04.1 CONDOMINIUM OWNERSHIP OF REAL PROPERTY 47-04.1-01. Definitions. In this chapter, unless context otherwise requires: 1. "Common areas" means the entire project excepting all units therein granted or reserved. 2. "Condominium" is an estate in real property consisting of an undivided interest or interests in common in a portion of a parcel of real property together with a separate interest or interests in space in a structure, on such real property. 3. "Interest" means the fractional or percentage interest or interests ascribed to each unit by the declaration provided for in section 47-04.1-03. 4. "Limited common areas" means those elements designed for use by the owners of one or more but less than all of the units included in the project. 5. "Project" means the entire parcel of real property divided, or to be divided into condominiums, including all structures thereon. 6. "To divide" real property means to divide the ownership thereof by conveying one or more condominiums therein but less than the whole thereof. 7. "Unit" means the elements of a condominium which are not owned in common with the owners of other condominiums in the project. 47-04.1-02. Recording of declaration to submit property to a project. When the sole owner or all the owners, or the sole lessee or all of the lessees of a lease desire to submit a parcel of real property to a project established by this chapter, a declaration to that effect shall be executed and acknowledged by the sole owner or lessee or all of such owners or lessees and shall be recorded in the office of the recorder of the county in which such property lies.