Real Property Conveyance Fee

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Real Estate Marketplace Glossary: How to Talk the Talk

Federal Trade Commission ftc.gov The Real Estate Marketplace Glossary: How to Talk the Talk Buying a home can be exciting. It also can be somewhat daunting, even if you’ve done it before. You will deal with mortgage options, credit reports, loan applications, contracts, points, appraisals, change orders, inspections, warranties, walk-throughs, settlement sheets, escrow accounts, recording fees, insurance, taxes...the list goes on. No doubt you will hear and see words and terms you’ve never heard before. Just what do they all mean? The Federal Trade Commission, the agency that promotes competition and protects consumers, has prepared this glossary to help you better understand the terms commonly used in the real estate and mortgage marketplace. A Annual Percentage Rate (APR): The cost of Appraisal: A professional analysis used a loan or other financing as an annual rate. to estimate the value of the property. This The APR includes the interest rate, points, includes examples of sales of similar prop- broker fees and certain other credit charges erties. a borrower is required to pay. Appraiser: A professional who conducts an Annuity: An amount paid yearly or at other analysis of the property, including examples regular intervals, often at a guaranteed of sales of similar properties in order to de- minimum amount. Also, a type of insurance velop an estimate of the value of the prop- policy in which the policy holder makes erty. The analysis is called an “appraisal.” payments for a fixed period or until a stated age, and then receives annuity payments Appreciation: An increase in the market from the insurance company. -

Full Report Introduction to Project

THE ILLUSION OF CHOICE: Evictions and Profit in North Minneapolis Author: Principal Investigator, Dr. Brittany Lewis, Senior Research Associate Contributing Authors: Molly Calhoun, Cynthia Matthias, Kya Conception, Thalya Reyes, Carolyn Szczepanski, Gabriela Norton, Eleanor Noble, and Giselle Tisdale Artist-in-Residence: Nikki McComb, Art Is My Weapon “I think that it definitely has to be made a law that a UD should not go on a person’s name until after you have been found guilty in court. It is horrific that you would sit up here and have a UD on my name that prevents me from moving...You would rather a person be home- less than to give them a day in court to be heard first...You shouldn’t have to be home- less to be heard.” – Biracial, female, 36 years old “I’ve heard bad “There is a fear premium attached to North Min- things. He’s known neapolis. Because what’s the stereotypical image as a slumlord...But people have of North Minneapolis? I could tell you. against my better Bang, bang. People are afraid of it. If you tell people, judgment, to not I bought a property in North Minneapolis. What they wanting to be out say is, ‘Why would you do that?’” – White, male, a place and home- 58 year old, property manager and owner less and between moving, I took the first thing. It was like a desper- ate situation.” – Biracial, female, 45 years old For more visit z.umn.edu/evictions PURPOSE, SELECT LITERATURE REVIEW, RESEARCH DESIGN AND METHODS Purpose Single Black mothers face the highest risk of eviction in the Single Black women with children living below the poverty line United States. -

Colorado Amends Unclaimed Property Law Regarding Gift Cards; Will Other States Follow?

Journal of Multistate Taxation and Incentives Volume 23, Number 10, February 2014 Department: PROCEDURE Colorado Amends Unclaimed Property Law Regarding Gift Cards; Will Other States Follow? States are reviewing their processes and looking for the means to enhance revenue, a course that includes increasing enforcement efforts and accelerating dormancy periods and reporting deadlines. By: JAMSHID EBADI AND SAMUEL SCHAUNAMAN JAMSHID EBADI is a Director with the Abandoned and Unclaimed Property Practice at Ryan LLC, in Greenwood Villa, Colorado. SAMUEL SCHAUNAMAN, J.D., is a Senior Manager with the same practice group, in Tulsa, Oklahoma, and he has previously written for The Journal. This article appears in and is reproduced with the permission of the Journal of Multistate Taxation and Incentives, Vol. 23, No. 10, February 2014. Published by Warren, Gorham & Lamont, an imprint of Thomson Reuters. Copyright (c) 2014 Thomson Reuters/Tax & Accounting. All rights reserved. All states, as well as an increasing number of foreign countries, have laws regulating the reporting and remitting of unclaimed property to the respective jurisdictions. Colorado has recently amended its Unclaimed Property Act ("Colorado Act" or "the Act") and the following discussion provides a synopsis of the Act and highlights the recent legislative developments in Colorado affecting the Act. First, however, we provide an overview of what typically constitutes unclaimed property. While not a "tax," unclaimed property nevertheless has become a significant source of funds for many states. The field of unclaimed property (also referred to as "abandoned property" or "escheat") concerns the requirement that businesses holding such property (the "holders") report the property to state governments. -

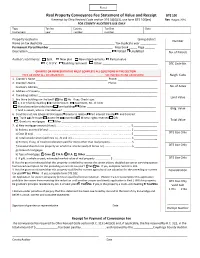

Real Property Conveyance Fee Statement of Value and Receipt

Real Property Conveyance Fee Statement of Value and Receipt DTE 100 If exempt by Ohio Revised Code section 319.54(G)(3), use form DTE 100(ex) Rev 1/14 FOR COUNTY AUDITOR’S USE ONLY Type Tax list County Tax Dist Date Instrument year number number Property located in ____________________________________________________________ taxing district Number Name on tax duplicate ____________________________________________ Tax duplicate year __________ Permanent Parcel Number _______________________________________ Map book _____ Page ______ Description ___________________________________________________ Platted Unplatted No. of Parcels Auditor’s comments: Split New plat New improvements Partial value C.A.U.V. Building removed Other __________________________________ DTE Code No. GRANTEE OR REPRESENTATIVE MUST COMPLETE ALL QUESTIONS IN THIS SECTION TYPE OR PRINT ALL INFORMATION SEE INSTRUCTIONS ON REVERSE Neigh. Code 1. Grantor’s Name _________________________________________________ Phone: ___________________________ 2. Grantee’s Name _________________________________________________ Phone: ___________________________ Grantee’s Address__________________________________________________________________________________ No. of Acres 3. Address of Property ________________________________________________________________________________ 4. Tax billing address _________________________________________________________________________________ Land Value 5. Are there buildings on the land? Yes No If yes, Check type: 1, 2 or 3 family dwelling Condominium -

Conveyancing and the Law of Real Property

September 2014 - ISSUE 19 Conveyancing and The Law of Real Property The questions may be asked what is Conveyancing and why is Property Rules and his first act must be to undertake an inves‐ it attached to the Law of Real Property. tigation into the title of the Vendor’s property. This search which must be conducted in the Register of Deeds and should When dealing with the Law of Real Property there are two involve a period of time of thirty years or longer in the case fundamental points which must be understood‐‐‐ where the date of the Vendor’s Deed is older than thirty years. (i) You acquire knowledge of the rights and liabilities attached to the interests of the owner in the land and The Cause List search is undertaken in the Supreme Court Registry and the purpose of which is to ascertain whether (ii) The foundation of the Rules of Conveyancing. there are any liens pending against the Vendor in the Su‐ preme Court Register. If there are pending liens, they must be It is not easy to distinguish accurately between Real Property settled by the Vendor before he is able to sell the property. and Conveyancing. It is said that Real Property deals with the rights and liabilities of land owners. Conveyancing on the The original documents of title must be produced by the Ven‐ other hand is the art of creating and transferring rights in land dor and delivered to the attorney for review. I the Vendor is and thus the Rules of Conveyancing and the Law of Real Prop‐ unable to produce the same and the attorney has found the erty cannot be distinguished as separate subjects though re‐ title to be good and marketable, then the Vendor must sign lated closely but should be distinguished as two parts of one and swear an Affidavit of Loss in respect of such lost or mis‐ subject of land law. -

Real & Personal Property

CHAPTER 5 Real Property and Personal Property CHRIS MARES (Appleton, Wsconsn) hen you describe property in legal terms, there are two types of property. The two types of property Ware known as real property and personal property. Real property is generally described as land and buildings. These are things that are immovable. You are not able to just pick them up and take them with you as you travel. The definition of real property includes the land, improvements on the land, the surface, whatever is beneath the surface, and the area above the surface. Improvements are such things as buildings, houses, and structures. These are more permanent things. The surface includes landscape, shrubs, trees, and plantings. Whatever is beneath the surface includes the soil, along with any minerals, oil, gas, and gold that may be in the soil. The area above the surface is the air and sky above the land. In short, the definition of real property includes the earth, sky, and the structures upon the land. In addition, real property includes ownership or rights you may have for easements and right-of-ways. This may be for a driveway shared between you and your neighbor. It may be the right to travel over a part of another person’s land to get to your property. Another example may be where you and your neighbor share a well to provide water to each of your individual homes. Your real property has a formal title which represents and reflects your ownership of the real property. The title ownership may be in the form of a warranty deed, quit claim deed, title insurance policy, or an abstract of title. -

An Environmental Critique of Adverse Possession John G

University of the Pacific Scholarly Commons McGeorge School of Law Scholarly Articles McGeorge School of Law Faculty Scholarship 1994 An Environmental Critique of Adverse Possession John G. Sprankling Pacific cGeM orge School of Law Follow this and additional works at: https://scholarlycommons.pacific.edu/facultyarticles Part of the Environmental Law Commons, and the Property Law and Real Estate Commons Recommended Citation John G. Sprankling, An Environmental Critique of Adverse Possession, 79 Cornell L. Rev. 816 (1994) This Article is brought to you for free and open access by the McGeorge School of Law Faculty Scholarship at Scholarly Commons. It has been accepted for inclusion in McGeorge School of Law Scholarly Articles by an authorized administrator of Scholarly Commons. For more information, please contact [email protected]. Cornell Law Review Volume 79 Article 2 Issue 4 May 1994 Environmental Critique of Adverse Possession John G. Sprankling Follow this and additional works at: http://scholarship.law.cornell.edu/clr Part of the Law Commons Recommended Citation John G. Sprankling, Environmental Critique of Adverse Possession , 79 Cornell L. Rev. 816 (1994) Available at: http://scholarship.law.cornell.edu/clr/vol79/iss4/2 This Article is brought to you for free and open access by the Journals at Scholarship@Cornell Law: A Digital Repository. It has been accepted for inclusion in Cornell Law Review by an authorized administrator of Scholarship@Cornell Law: A Digital Repository. For more information, please contact [email protected]. AN ENVIRONMENTAL CRITIQUE OF ADVERSE POSSESSION John G. Spranklingf INTRODUCTION Consider three applications of modem adverse possession law to wild, undeveloped land. -

Nonprofit Real Estate Development Toolkit: Stable, Affordable Space for Manufacturing

NONPROFIT REAL ESTATE DEVELOPMENT TOOLKIT: STABLE, AFFORDABLE SPACE FOR MANUFACTURING DEVELOPED FOR THE URBAN MANUFACTURING ALLIANCE BY THE PRATT CENTER FOR COMMUNITY DEVELOPMENT Purpose of this toolkit This toolkit is meant to help manufacturers understand developers, and help developers understand manufac- turers, so they can better identify and pursue opportunities to work together. We also want state, local, and federal govern- ment actors to understand the particular challenges urban manufacturers face in securing the space they need; and we want to promote the development of policy and financing tools that can lower some of the barriers to nonprofit industrial development that now impede the growth of vibrant, diverse, and stable industrial communities. Reclaiming legacy industrial buildings in urban markets demands development Introduction: why is nonprofit industrial expertise and a mission-driven commitment. real estate development important to urban Different markets: different challenges manufacturers? Hot market challenges: Manufacturers need space that is: • In high-cost, high-demand cities, land that has traditionally Stable been industrial is under pressure from users who can pay Affordable more – much more – for space than manufacturers. A parcel of land used for manufacturing may have value of Right Size $150 per square foot; if residential development is allowed on the same parcel, its value may be $3,000 per square Right Quality foot or more. Right Location • Political leaders in many cities have rezoned Industrial land to accommodate residential and commercial growth, But good space is hard to find – in hot-market cities and in often with the stated goal of increasing local property and cool ones. -

Condominium Ownership of Real Property

CHAPTER 47-04.1 CONDOMINIUM OWNERSHIP OF REAL PROPERTY 47-04.1-01. Definitions. In this chapter, unless context otherwise requires: 1. "Common areas" means the entire project excepting all units therein granted or reserved. 2. "Condominium" is an estate in real property consisting of an undivided interest or interests in common in a portion of a parcel of real property together with a separate interest or interests in space in a structure, on such real property. 3. "Interest" means the fractional or percentage interest or interests ascribed to each unit by the declaration provided for in section 47-04.1-03. 4. "Limited common areas" means those elements designed for use by the owners of one or more but less than all of the units included in the project. 5. "Project" means the entire parcel of real property divided, or to be divided into condominiums, including all structures thereon. 6. "To divide" real property means to divide the ownership thereof by conveying one or more condominiums therein but less than the whole thereof. 7. "Unit" means the elements of a condominium which are not owned in common with the owners of other condominiums in the project. 47-04.1-02. Recording of declaration to submit property to a project. When the sole owner or all the owners, or the sole lessee or all of the lessees of a lease desire to submit a parcel of real property to a project established by this chapter, a declaration to that effect shall be executed and acknowledged by the sole owner or lessee or all of such owners or lessees and shall be recorded in the office of the recorder of the county in which such property lies. -

41.01.01 Real Property

41.01.01 Real Property Revised September 21, 2021 Next Scheduled Review: September 21, 2026 Click to view Revision History. Regulation Summary This regulation provides uniform guidance for the acquisition, disposition, lease and license of real property and delegates authority to the chief executive officers (CEO) or designees of The Texas A&M University System (system). Definitions Click to view Definitions. Regulation 1. GENERAL PROVISIONS 1.1 System Real Estate Office. Except as otherwise provided in this regulation, all activities involving the acquisition, disposition, lease and license of a surface estate, except those activities and operations commonly associated with easements and right-of-ways, will be consolidated in the System Real Estate Office (SREO) and coordinated with the appropriate member or members. 1.2 System Energy Resource Office. Except as otherwise provided in this regulation, all activities involving the acquisition, disposition and lease of a mineral estate, and those activities commonly associated with easements and right-of-ways of a surface estate, will be consolidated in the System Energy Resource Office (SERO) and coordinated with the appropriate member or members. 1.3 Intrasystem Assignment of Real Property. Subject to any legal requirements or donor restrictions, real property used primarily for member purposes will be assigned to the using member for maintenance, operation and management purposes. Real property may be reassigned by the chancellor based on the primary use or proposed use of the property. The reassignment will be evidenced by a form prepared by SREO, signed by the chancellor and maintained by SREO. 1.4 Maintenance of Inventory and Records. -

Connecticut Valley Environmental Services, Inc. of the Profit Sharing Plan of Connecticut Valley Environmental Services, Inc

THE STATE OF NEW HAMPSHIRE SUPREME COURT 2011 TERM OCTOBER SESSION Case No. 2011-0227 MICHAEL O’HEARNE AND MARIE O’HEARNE Petitioners – Appellees v. JAMES U. McCLAMMER, JR. Respondent – Appellant and JAMES U. McCLAMMER, JR., TRUSTEE OF THE PROFIT SHARING PLAN OF CONNECTICUT VALLEY ENVIRONMENTAL SERVICES, INC. Petitioner – Appellant v. MICHAEL O’HEARNE AND MARIE O’HEARNE Respondents – Appellees ______________________________________________________________________________ RULE 7 APPEAL FROM SULLIVAN COUNTY SUPERIOR COURT ______________________________________________________________________________ OPENING BRIEF OF APPELLANT - JAMES U. McCLAMMER, JR., TRUSTEE OF THE PROFIT SHARING PLAN OF CONNECTICUT VALLEY ENVIRONMENTAL SERVICES, INC. ______________________________________________________________________________ Bradford T. Atwood, Esq. NH Bar No. 8512 CLAUSON & ATWOOD 10 Buck Road Hanover, NH 03755 603-643-2102 Oral Argument by: James M. McClammer or Bradford T. Atwood, Esq. TABLE OF CONTENTS TABLE OF AUTHORITIES ......................................................................................................... iii STATUTORY PROVISIONS .........................................................................................................v QUESTIONS PRESENTED ...........................................................................................................1 STATEMENT OF CASE, FACTS AND PROCEDURAL HISTORY .........................................2 SUMMARY OF THE ARGUMENT ............................................................................................11 -

State of Hawaii Guidelines for Reporting and Remitting Unclaimed

GUIDELINES FOR REPORTING AND REMI1TING UNCLAIMED PROPERTY HOLDER REPORT DUE NOVl Updated July 2016 HOLDER INFORMATION "Holders of unclaimed property are usually companies, businesses, corporations, partnerships, professional associations, non-profit organizations, private organizations, government entities or state agencies in possession of unclaimed property as defined in Chapter 523A, HRS. Holders are required to annually report and escheat unclaimed property to the State of Hawaii Unclaimed Property Program." Contents Unclaimed Property Statutes ........................ 3 Holder Reporting Guidelines .......................... 4 Holder Reporting Requirements ..................... 5 HOLDER REPORT TOTAL & REMITTANCE AMOUNT MUST AGREE A REPORT WHICH DIFFERS FROM THE REMITTANCE AMOUNT MAY BE RETURNED HOLDER REPORT SHARES TOTAL & TRANSFER OF SHARES TOTAL MUST AGREE A REPORT OF SHARES WHICH DIFFERS FROM THE DOCUMENT CONFIRMING TRANSFER OF THE SHARES MAY BE RETURNED Unclaimed Property Program References 250 S. Hotel Street Room 304 • Unclaimed Property Statutes http://www.capitol. hawa ii.gov /hrscurrenWol12_C h050 1- 0588/HRS0523A/H RS_0523A- .him (808) 586-1589 • NAUPA Standard Electronic File Format https://www.unclaimed.org/uploads/resources/52/naupa-format-revised-9-26-13-new- relationship-ownership-codes-final-correct1.pdf • Holder Request for Reimbursement Form https://www.unclaimed.org/uploads/resources/319/naupa-holder-reimbursement-form-rev- make-fillable-update-2016.pdf State of Hawaii Updated July 2016 HOLDERS: HOLDER REPORT Submittals DUE NOV 1 The State of Hawaii Unclaimed Property Program will acknowledge acceptance of a holder report by email. REMITTANCE CHECK AMOUNT & REPORT TOTAL MUST AGREE CONFIRMATION DOCUMENT & TOTAL SHARES MUST AGREE REPORT SUBMITTALS MAY NOT BE ACCEPTED IF REPORT AND REMITTANCE DIFFER AND/OR IF TOTAL SHARES AND CONFIRMATION DOCUMENT DIFFER HRS 523A: A holder of abandoned property shall make a report and pay, deliver or cause to be paid or delivered to the administrator the property described in the report as unclaimed.