In Re Inphonic, Inc. 07-CV-00930-First Amended Class

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

"Trendy" Wireless Phones Most Likely to Be Researched Online; Low-Cost Models Most Often Ordered

"Trendy" Wireless Phones Most Likely To Be Researched Online; Low-Cost Models Most Often Ordered Motorola RAZR V3C Tops the List of Most Researched Wireless Phones; Sony Ericsson Z520A Most Frequently Ordered Online, with More than Two-Thirds at No Cost to the Consumer "Trendy" Wireless Phones Most Likely To Be Researched Online; Low-Cost Models Most Often Ordered RESTON, VA. June 12, 2006 - comScore Networks, a leader in the measurement and analysis of consumer behavior and attitudes, today released an analysis of the online research and purchase behavior of consumers in the wireless phone market. comScore revealed that consumers were most likely to research newly released and "trendy" models, with the Motorola RAZR V3C topping the list during the first quarter of 2006. Other models securing spots on the most researched list include the Palm Treo 650, the Palm Treo 700W, and the Motorola Pebl. Top 10 Wireless Phones Researched Online First Quarter 2006 Source: comScore Networks Manufacturer Model Motorola Razr V3C Palm Treo 650 Motorola E815 Palm Treo 700W Motorola Razr V3 Samsung A900 Motorola Pebl Sony Ericsson Z520A Nokia 6101/6102 LG C2000 The Motorola Q is the latest phone to be released, with Verizon Wireless positioned as sole provider of this model for a limited time. As a measure of interest in the model, comScore found that the Motorola Q product page on the Verizon Wireless Web site received slightly more than 100,000 unique visitors in the second half of May, 2006. Price is a Driving Factor When Purchasing a Phone comScore also analyzed trends in ordering cell phones online, among new and existing customers, at major carrier and wireless sites in the first quarter of 2006. -

Multidistrict Litigation Terminated Through September 30, 2016 Multidistrict Litigation Terminated Through September 30, 2016

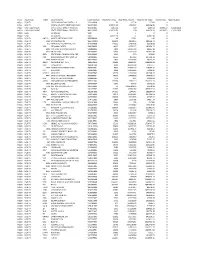

UNITED STATES JUDICIAL PANEL ON MULTIDISTRICT LITIGATION Multidistrict Litigation Terminated Through September 30, 2016 Multidistrict Litigation Terminated Through September 30, 2016 Actions Terminated District MDL MDL Caption Transferee Judge Total Tr'd Total Filed Closed Remanded Year of Court Code No. in Tr'e Court Termination GRAND TOTALS (1,435 Litigations) 99,958 65,073 151,980 13,051 52 in 2016 DISTRICT OF COLUMBIA CIRCUIT 090 DISTRICT OF COLUMBIA (37 Litigations) 50 Ampicillin AT Richey, C.R. 16 45 61 0 1984 54Alsco-Harvard Fraud Oberdorfer, L.F.81901983 105 National Student Marketing Parker, B.D. 7 4 11 0 1983 135 Mutual Fund Sales AT Corcoran, H.F. 43 4 47 0 1975 205Griseofulvin AT Robinson, Jr., A.E.21301978 213Radiation Incident - 4/5/74 CD Hart, Jr., G.L. 16701978 221 Saigon, S. Vietnam AD Oberdorfer, L.F. 32 14 42 4 1986 258Government Employees Insurance Co. SEC Hart, Jr., G.L. 22401978 283Taipei Airport - 7/31/75 AD Bryant, W.M. 41501981 328 Amoxicillin PAT & AT Richey, C.R. 51241984 330 Swine Flu Immunization PL Gesell, G.A. 1,585 20 306 1,299 1988 344General Aircraft Corp./Tort Claims Act AT Green, J.L. 11201979 372 Federal Election Campaign Act Richey, J.L. 17 2 19 0 1979 389Barrow, AK - 10/13/78 AD Robinson, Jr., A.E.31401980 458 Riyadh Airport, Saudi Arabia - 8/19/80 AD Flannery, T.A. 38 8 46 0 1982 499 Washington, DC - 1/13/82 AD Green, J.H. 33 50 83 0 1988 565 Korean Airlines - 9/1/83 AD Robinson, Jr., A.E. -

Merrill Lynch Security Risk Evaluation 1-07

Security Risk Evaluation ALPHA January 2007 Price As of December 2006 Month End COPYRIGHT 1998 MERRILL LYNCH, PIERCE, FENNER & SMITH INCORPORATED (MLPF&S). APPROVED FOR PUBLICATION IN THE UNITED KINGDOM BY MERRILL LYNCH, PIERCE, FENNER & SMITH LIMITED, AN AFFILIATED COMPANY AND REGULATED BY THE SECURITIES AND FUTURES AUTHORITY LIMITED. THE INFORMATION HEREIN WAS OBTAINED FROM VARIOUS SOURCES; WE DO NOT GUARANTEE ITS ACCURACY. ADDITIONAL INFORMATION AVAILABLE. GLOBAL SECURITIES RESEARCH & ECONOMICS RESEARCH TECHNOLOGY ALPHA (1) 800 255-9107 CONTINENTAL UNITED STATES January 2007 (1) 212 449-1072 WORLD WIDE PRICE AS OF December 2006 MONTH END Merrill Lynch, Pierce, Fenner & Smith, Inc. Market Sensitivity Statistics 2006/ 12 Resid Number Ticker Close Std --Std Error-- Adjusted Of Symbol Security Name Price Beta Alpha R-Sqr Dev-n Beta Alpha Beta Observ DOWI DOW JONES & CO 30 INDUSTRIALS 12463.150 0.96 0.03 0.91 1.09 0.04 0.14 0.98 60 DJ 20 DOW JONES & CO 20 TRANS ACTUAL 4560.200 0.94 0.65 0.42 3.86 0.14 0.50 0.96 60 DJ 15 DOW JONES & CO 15 UTIL ACTUAL 456.770 0.57 0.60 0.19 4.12 0.15 0.54 0.72 60 DJ 65 DOW JONES & CO 65 STOCK COMPOSITE 4120.960 0.89 0.28 0.86 1.29 0.05 0.17 0.93 60 SPALNS S&P 500 500 STOCKS 1418.300 1.00 0.00 1.00 0.00 0.00 0.00 1.00 60 Based on S&P 500 Index Using Straight Regression Merrill Lynch, Pierce, Fenner & Smith, Inc. -

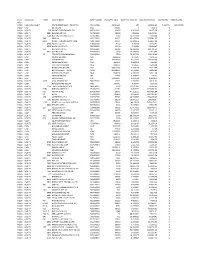

Fund Asset Class Ticker Security Name CUSIP Number Shares/Par

Fund Asset Class Ticker Security Name CUSIP Number Shares/Par Value Base Price Amount Base Market Value Interest Rate Maturity Date NQ11 EQUITY GREEN MOUNTAIN CAPITAL L.P '394990998 50 427.38 21369 0 NQ11 EQUITY NORTH ATLANTIC VENTURE FUND II '651991929 275572.22 1.959947 540106.95 0 NQ11 CASH EQUIVALENT STATE STREET BANK + TRUST CO '8611239B5 4483.64 100 4483.64 0.190652 12/31/2030 NQ20 CASH EQUIVALENT STATE STREET BANK + TRUST CO '8611239B5 196470.54 100 196470.54 0.190652 12/31/2030 NQ20 CASH US DOLLAR 'USD 0 1 0 0 NQ20 CASH US DOLLAR 'USD 12907.48 1 12907.48 0 NQ20 EQUITY NRTLQ NORTEL NETWORKS CORP '656568508 48 0.031 1.49 0 NQ2A EQUITY 5020 JX HOLDINGS INC 'B627LW906 202200 4.938411 998546.73 0 NQ2A EQUITY 510 HIAP SENG ENGINEERING LTD '616207908 132000 0.454838 60038.68 0 NQ2A EQUITY VOR SEQUANA CAPITAL '546924903 14919 12.255127 182834.25 0 NQ2A EQUITY 9842 ARC LAND SAKAMOTO CO LTD '604800904 5800 14.645723 84945.19 0 NQ2A EQUITY 7279 HI LEX CORP '664347002 12500 13.120127 164001.58 0 NQ2A EQUITY SBIDl STATE BANK OF INDIA SPON GDR '513109900 2000 99.9 199800 0 NQ2A EQUITY PKN POLSKI KONCERN NAFTOWY SA '581006905 10236 10.5059 107538.39 0 NQ2A EQUITY 9945 PLENUS CO LTD '669270902 3800 15.335066 58273.25 0 NQ2A EQUITY GIB/A CGI GROUP INC CL A '39945C950 80496 14.906131 1199883.91 0 NQ2A EQUITY CGO COGECO INC '19238T100 1200 28.231309 33877.57 0 NQ2A EQUITY 9936 OHSHO FOOD SERVICE CORP '666093901 4600 25.663917 118054.02 0 NQ2A EQUITY KIN KINEPOLIS '543952907 1419 52.854446 75000.46 0 NQ2A EQUITY SAAB B SAAB AB B '546955907 34176 11.449499 -

Plaintiff's Motion for Preliminary Approval of Class Settlement And

UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF NORTH CAROLINA No. 5:15-cv-231 GARY and ANNE CHILDRESS, THOMAS ) and ADRIENNE BOLTON, STEVEN and ) MORGAN LUMBLEY, RAYMOND and ) JACKIE LOVE, HARRY and MARIANNE CHAMPAGNE, and RUSSELL and MARY ) BETH CHRISTE, on behalf of themselves ) and others similarly situated, ) ) Plaintiffs, ) vs. ) ) BANK OF AMERICA, N.A., ) Defendant. ) PLAINTIFFS’ MOTION FOR PRELIMINARY APPROVAL OF CLASS SETTLEMENT AND CERTIFICATION OF THE SETTLEMENT CLASS Plaintiffs Gary and Anne Childress, Thomas and Adrienne Bolton, Steven and Morgan Lumbley, Raymond and Jackie Love, Harry and Marianne Champagne, and Russell and Mary Beth Christe (collectively “plaintiffs”), with agreement of the Defendant, Bank of America, N.A. (“Bank of America” or “Defendant”), under Fed. R. Civ. P. 23 and Local Rule 7.1, respectfully move the Court for an order: 1. Certifying, for settlement purposes, a proposed nationwide class of persons defined as: All persons identified in Bank of America’s records as obligors or guarantors on an obligation or account who, at any time on or after September 11, 2001, received and/or may have been eligible to receive additional compensation related to military reduced interest rate benefits from Defendant, but excluding persons who have executed a release of the rights claimed in this action; 2. Granting preliminary approval of a settlement of this action between the class and Case 5:15-cv-00231-BO Document 106 Filed 07/20/17 Page 1 of 5 Bank of America; 3. Granting preliminary approval of the proposed distribution plan; 4. Appointing named plaintiffs in this action as class representatives and the law firms Hagens Berman Sobol Shapiro LLP, Smith & Lowney, PLLC, and Shanahan Law Group, PLLC as class counsel; 5. -

Fund Asset Class Ticker Security Name CUSIP Number Shares/Par

Fund Asset Class Ticker Security Name CUSIP Number Shares/Par Value Base Price Amount Base Market Value Interest Rate Maturity Date NQ11 ' NQ20 CASH EQUIVALENT STATE STREET BANK + TRUST CO '8611239B5 459562.42 100 459562.42 0.155781 12/31/2030 NQ20 CASH US DOLLAR 'USD -3168.1 1 -3168.1 0 NQ2A EQUITY 316 ORIENT OVERSEAS INTL LTD '665911905 10000 4.847328 48473.28 0 NQ2A EQUITY 9997 BELLUNA CO LTD '607035904 19000 7.883193 149780.67 0 NQ2A EQUITY 7518 NET ONE SYSTEMS CO LTD '603654906 3600 13.247274 47690.19 0 NQ2A EQUITY EAD EADS NV '401225909 63129 35.457258 2238381.23 0 NQ2A EQUITY IFS B_ INDUST + FINANCIAL SYSTEM B '508170909 10371 15.682951 162647.88 0 NQ2A EQUITY 6406 FUJITEC CO LTD '635682008 4000 6.35418 25416.72 0 NQ2A EQUITY 8056 NIHON UNISYS LTD '664268000 35100 7.30668 256464.47 0 NQ2A EQUITY BLT BHP BILLITON PLC '005665906 32542 28.326213 921791.61 0 NQ2A EQUITY 7631 MACNICA INC '620789909 1100 22.358692 24594.56 0 NQ2A EQUITY TD TORONTO DOMINION BANK '891160954 7500 78.159792 586198.44 0 NQ2A CASH POUND STERLING 'GBP 28911.69 1.56845 45346.55 0 NQ2A CASH JAPANESE YEN 'JPY 35926970 0.012533 450269.08 0 NQ2A CASH CANADIAN DOLLAR 'CAD 5601.52 0.980921 5494.65 0 NQ2A CASH AUSTRALIAN DOLLAR 'AUD 73410.53 1.02505 75249.48 0 NQ2A CASH HONG KONG DOLLAR 'HKD 308101.62 0.128918 39719.94 0 NQ2A CASH MEXICAN PESO (NEW) 'MXN 803148.56 0.074483 59820.84 0 NQ2A CASH NORWEGIAN KRONE 'NOK 240817.9 0.168224 40511.38 0 NQ2A CASH SWEDISH KRONA 'SEK 725.52 0.144877 105.11 0 NQ2A CASH SWISS FRANC 'CHF 122129.07 1.056524 129032.3 0 NQ2A EQUITY AGFB AGFA GEVAERT NV '568905905 29401 1.637075 48131.63 0 NQ2A CASH NEW ZEALAND DOLLAR 'NZD 7307.71 0.80375 5873.57 0 NQ2A EQUITY 7729 TOKYO SEIMITSU CO LTD '689430007 3500 17.646322 61762.13 0 NQ2A EQUITY HSBA HSBC HOLDINGS PLC '054052907 131069 8.800575 1153482.52 0 NQ2A EQUITY RIO RIO TINTO PLC '071887004 39671 47.351515 1878481.94 0 NQ2A EQUITY BP. -

John Sculley in Conversation with David Greelish

John Sculley: The Truth About Me, Apple, and Steve Jobs Part One Interviewed by: David Greelish Recorded: December 2011 Transcribed by: Julie Kuehl CHM Reference number: X6382.2012 © The Mac Observer, Inc. John Sculley / David Greelish Hi. My name is David Greelish from ClassicComputing.com and I’m a computer historian. I write and produce podcasts about computer history nostalgia. I’m also a huge fan of the Macintosh, Apple Computer, and, of course, Steve Jobs. I am and have been very inspired by Steve. But I’m also a fan of John Sculley and have owned his book for many years. John Sculley has a bad rap. He is blamed for firing Steve Jobs, as well as almost bankrupting Apple. I fell in love with the Mac and Apple in late 1986, while John was at the helm. Thus began my romance with the company, the Mac, and other Apple products, and the culture in being one within the minority of personal computing. A non-DOS, then non- Windows user. A Mac user. It was a few years later that I started studying computer history. I’ve been learning more about the two Steves, Steve Jobs and Steve Wozniak. In recent years, and now after Steve’s death, John Sculley has been very remorseful for his actions surrounding Steve’s departure from the company. I believe that John has been way too hard on himself about this. As he took his position seriously as CEO, took a stand on the decision about the Apple ][, then was essentially forced by Steve to have the board vote between them. -

Australia 7-Eleven Speak

Country MVNO Name Technology Network Used Comments 7-Eleven Speak- Pre-paid MVNO/ESP owned by low-cost telco Commoditel boasting 15.000 subscribers as of June Up 2005 in combination with Revolution Telecom Macquarie SP focused on business and government markets. Telecom Mobile Mobile Innovations Gametel ESP owned by Bugal focusing previously on Australia Mobile Mojo GSM Vodafone ringtones, games and wallpapers and now engaged in a branded SIM venture with Commoditel ESP featuring pre-paid SIM-only proposition and Revolution internet distribution, owned by low-cost telco Telecom Commoditel and boasting 15.000 subscribers as of June 2005. Reward Mobile Niche ESP player targeting ethnic communities SlimTel through MVNE Virtel ESP (similar to Mobile Mojo above) owned by Bugal focusing previously on ringtones, games and Zany Mobile wallpapers and now engaged in a branded SIM venture with Commoditel Australia Boost Mobile IDEN B Digital Lifestyle ESP targeting the youth market. A division of Nextel. Cellhire GSM GSM Australia Digiplus Optus GSM 100% Optus-owned pre-paid service offering. Not really an iSim GSM MVNO or ESP, but a cheaper-calling promotion vehicle. GSM Full MVNO launched in October 2000, a joint-venture between Optus and The Virgin Group. Virgin Mobile Virgin Mobile Australia owns and manages it's own switching infrastructure and boasts over 500.000 customers. Communic8(Telstra Australia GSM Telstra Prepaid Plus) Australia Fone Zone CDMA Telstra Optus(GDM), Australia Austar GSM/CDMA Telstra(CDMA) Globalstar Australia Pty Optus and Australia GSM GSM / Satellite SP in Australia and New Zealand Limited Telstra Optus and Australia People Telecom Telstra Australia Primus GSM Optus and Australia Southern Cross Mobile Telstra Optus and Australia Telecall Telstra A1-Telekom Austria bob Austria Mobilkom Austria AG & Austria GSM ONE ESP focusing on ethnic groups. -

PROJECT NOVA/TRAVELPORT * FORM S-4 Proj: P3496NYC06 Job: 06NYC5200 File: BA5200A.;18 Merrill/New York (212) 229-6500 Page Dim: 8.250� X 10.750� Copy Dim: 40

MERRILL CORPORATION JGUERRE//30-MAR-07 00:22 DISK132:[06NYC0.06NYC5200]BA5200A.;18 mrll.fmt Free: 10DM/0D Foot: 0D/ 0D VJ J1:1Seq: 1 Clr: 0 DISK024:[PAGER.PSTYLES]UNIVERSAL.BST;60 53 C Cs: 12029 As filed with the Securities and Exchange Commission on March 30, 2007 No. 333- UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form S-4 REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 Travelport Limited (Exact name of registrant parent guarantor as specified in its charter) Bermuda 4700 98-0505100 (State or jurisdiction (Primary Standard Industrial (I.R.S. Employer of incorporation or organization) Classification Code Number) Identification No.) Clarendon House 2 Church Street Hamilton HM 11 Bermuda TDS Investor (Luxembourg) S.a.r.l.` (Exact name of registrant intermediate parent guarantor as specified in its charter) Luxembourg 4700 98-0505096 (State or jurisdiction (Primary Standard Industrial (I.R.S. Employer of incorporation or organization) Classification Code Number) Identification No.) 4a, vue Henri Schnadt Luxembourg 2530 Luxembourg Travelport LLC (Exact name of registrant issuer as specified in its charter) (see also Table of Additional Registrant Subsidiary Guarantors) Delaware 4700 20-8662915 (State or other jurisdiction of (Primary Standard Industrial (I.R.S. Employer incorporation or organization) Classification Code Number) Identification No.) 400 Interpace Parkway Building A Parsippany, NJ 07054 Travelport Holdings, Inc. (Exact name of registrant co-obligor as specified in its charter) Delaware 4700 20-8657242 (State or jurisdiction (Primary Standard Industrial (I.R.S Employer of incorporation or organization) Classification Code Number) Identification No.) 400 Interplace Parkway Building A Parsippany, NJ 07054 (973) 939-1000 (Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) Eric J. -

Wireless Deputy General Counsel Regulatory Law Verizon Wireless 1300 I Street, N.W

- John T. Scott, 111 Vice President & wireless Deputy General Counsel Regulatory Law Verizon Wireless 1300 I Street, N.W. Suite 400 West Washington, DC 20005 October 25,2005 Phone 202 589-3760 Fax 202 589-3750 john.scott @verizonwireless.com Ms. Marlene H. Dortch Secretary Federal Communications Commission 445 Twelfth Street, SW Washington, DC 20554 Re: WT Docket No. 05-194: CTIA Petition for Expedited Declaratory Ruling on Early Termination Fees: Ex Parte Written Presentation Dear Ms. Dortch: Verizon Wireless is filing the enclosed declaration of Dr. Jerry A. Hausman in the record in this proceeding. Dr. Hausman is MacDonald Professor of Economics at the Massachusetts Institute of Technology, and has studied the economics of the mobile phone industry for over 20 years. His qualifications for commenting on issues raised in this docket are detailed in the declaration. CTIA has asked the Commission to confirm that early termination fees (“ETFs”) in mobile telephone subscriber contracts constitute “rates charged” or components of “rates charged” within the meaning of Section 332(c)(3)(A) of the Communications Act. CTIA seeks this ruling because various courts are being asked to order carriers to return ETFs that have been paid and to ban ETFs prospectively, on the theory that states (and state courts) can regulate the amount or reasonableness of ETFs. As the Commission has found, however, Section 332(c)(3)(A) not only bans states from regulating wireless rates and fees, but also forbids states, including state courts, from assessing the reasonableness of such rates and fees. CTIA’s petition should be granted. -

November 14, 2005 Yahoo About Yahoo!

v TABLE OF CONTENTS Yahoo About Yahoo! 1 Q Model Portfolio 7 Yahoo About Yahoo! By James Altucher I’m adding five picks to the portfolio today, including growth stocks Yahoo! (YHOO:Nasdaq) and Marchex (MCHX:Nasdaq), value stock Liberty Media (L:NYSE), and China stocks Netease (NTES:Nasdaq) and Tom Online (TOMO:Nasdaq). The picks should be bought as a basket, because I’m not saying Yahoo! is going to double from here. Rather, I believe that selectively picking a group of growth stocks and riding them as they continue their high double-digit -- and in some cases triple-digit -- growth, will serve an investor well. First in the Basket: Yahoo! I have to say I’m extremely jealous of Jerry Yang and David Filo. I just can’t help it. All they did was collect bookmarks in 1994 and now they have billions of dollars personally. That said, they earned every penny of it. I’m a heavy user of several of Yahoo!’s services, most particularly Yahoo! Finance and their newest acquisition, Flickr. Today I’m recommending a Speculative Buy of their company’s stock. Yahoo! has matured as a company. In 1999 its ad sales team was so cocky they wouldn’t even return calls on a million dollar sales deal. The company changed management, bringing in seasoned media executive Terry Semel, and has been gradually repositioning the company by buying and introducing profitable services such as hotjobs.com. More recently, the company has made a concerted push in three areas: international, VOIP and the so-called Web 2.0, which introduces collaborative services such as the flickr network. -

Cumulative Terminated 2014

USJNITED TATES UDICIAL P ANEL ON MLULTIDISTRICT ITIGATION Multidistrict Litigation Terminated Through September 30, 2014 Multidistrict Litigation Terminated Through September 30, 2014 Actions Terminated District MDL MDL Caption Transferee Judge Total Tr'd Total Filed Dis'd Rem'd Year of Court Code No. in Tr'e Court Termination GRAND TOTALS (1,337 Litigations) 74,844 46,816 109,228 12,432 50 in FY 2014 DISTRICT OF COLUMBIA CIRCUIT 090 DISTRICT OF COLUMBIA (38 Litigations) 50 Ampicillin AT Richey, C.R. 16 45 61 0 1984 54Alsco-Harvard Fraud Oberdorfer, L.F.8190 1983 105 National Student Marketing Parker, B.D. 7 4 11 0 1983 135 Mutual Fund Sales AT Corcoran, H.F. 43 4 47 0 1975 205Griseofulvin AT Robinson, Jr., A.E.2130 1978 213Radiation Incident - 4/5/74 CD Hart, Jr., G.L. 1670 1978 221 Saigon, S. Vietnam AD Oberdorfer, L.F. 32 14 42 4 1986 258Government Employees Insurance Co. SEC Hart, Jr., G.L. 2240 1978 283Taipei Airport - 7/31/75 AD Bryant, W.M. 4150 1981 328 Amoxicillin PAT & AT Richey, C.R. 5124 1984 330 Swine Flu Immunization PL Gesell, G.A. 1,585 20 306 1,299 1988 344General Aircraft Corp./Tort Claims Act AT Green, J.L. 1120 1979 372 Federal Election Campaign Act Richey, J.L. 17 2 19 0 1979 389Barrow, AK - 10/13/78 AD Robinson, Jr., A.E.3140 1980 458 Riyadh Airport, Saudi Arabia - 8/19/80 AD Flannery, T.A. 38 8 46 0 1982 499 Washington, DC - 1/13/82 AD Green, J.H.