UAW Labor Negotiations

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Small Suvs, Minicars Make Big Gains in 2006 the Renault Megane CC (Shown) Ended Peugeot’S 5-Year Reign at the Top of Luca Ciferri the Fastest-Growing Segment

AN_070402_18&19good.qxd 13.04.2007 8:58 Uhr Page 18 PAGE 18 · www.autonewseurope.com April 2, 2007 Market analysis by segment, European sales ROADSTER & CONVERTIBLE Small SUVs, minicars make big gains in 2006 The Renault Megane CC (shown) ended Peugeot’s 5-year reign at the top of Luca Ciferri the fastest-growing segment. Changing segments the roadster and convertible seg- Automotive News Europe Minicars, the No. 3 segment last year in ment. Peugeot’s 307 CC was No. 1 in terms of growth, increased 22.1 percent to Europe’s 2006 winners and losers 2004; the 206 CC led the other years. Rising fuel costs, growing concerns about 992,227 units thanks largely to strong Small SUV +63.6 2006 2005 % Change Seg. share % CO2 and a flurry of new products sparked sales of three cars built at Toyota and Upper premium +26.4 Renault Megane 32,344 42,514 -23.9% 13.4% a sales surge for small SUVs and minicars PSA/Peugeot-Citroen’s plant in Kolin, Minicar +22.1 Peugeot 307CC/306C 31,786 39,640 -19.8% 13.1% in Europe last year. Czech Republic. Peugeot 206 CC 29,833 43,518 -31.4% 12.3% The arrival of three new small SUVs Europe’s largest segment, small cars, Small minivan -13.6 VW Eos 21,759 59 – 9.0% helped the segment grow 63.6 percent to rose 7.0 percent to 3,811,009 units. The Premium roadster & convertible -10.9 Opel/Vauxhall Tigra TwinTop 20,406 32,633 -37.5% 8.4% 94,153 units in 2006, according to UK- second-biggest segment – lower-medium Lower medium -8.2 Mazda MX-5 19,288 9,782 97.2% 8.0% based market researcher JATO Dynamics. -

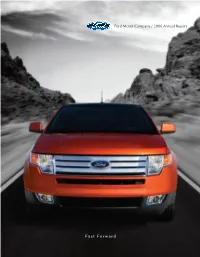

Fast Forward 2006 Annual Report

Ford Motor Company Ford Motor Company / 2006 Annual Report Fast Forward 2006 www.ford.com Annual Fast Forward Ford Motor Company • One American Road • Dearborn, Michigan 48126 Report cover printer spreads_V2.indd 1 3/14/07 7:41:56 PM About the Company Global Overview* Ford Motor Company is transforming itself to be more globally integrated and customer-driven in the fiercely competitive world market of the 21st century. Our goal is to build more of the products that satisfy the wants and needs of our customers. We are working as a single worldwide team to improve our cost structure, raise our Automotive Core and Affi liate Brands quality and accelerate our product development process to deliver more exciting new vehicles faster. Featured on the front and back cover of this report is one of those vehicles, the 2007 Ford Edge. Ford Motor Company, a global industry leader based in Dearborn, Michigan, manufactures or distributes automobiles in 200 markets across six continents. With more than Dealers 9,480 dealers 1,515 dealers 1,971 dealers 125 dealers 871 dealers 2,352 dealers 1,376 dealers 6,011 dealers and 280,000 employees and more than 100 plants worldwide, the company’s core and affiliated Markets 116 markets 33 markets 25 markets 27 markets 64 markets 102 markets 138 markets 136 markets automotive brands include Ford, Jaguar, Land Rover, Lincoln, Mercury, Volvo, Aston Martin Retail 5,539,455 130,685 188,579 7,000 74,953 428,780 193,640 1,297,966** and Mazda. The company provides financial services through Ford Motor Credit Company. -

Ford Motor Company One American Road Dearborn, MI 48126 U.S.A

Report Home | Contact | GRI Index | Site Map | Glossary & Key Terms This report is structured according to our Business Principles, which you can access using the colored tabs above. This report is aligned with the Global Reporting Initiative (GRI) G3 Sustainability Reporting Guidelines released in October 2006, at an application level of A+. See the GRI Index ● Print this report "Welcome to our 2006/7 Sustainability Report. These are challenging times, not only for our Company but for our planet and its inhabitants. The markets for our products are changing rapidly, and there is fierce competition everywhere we operate. Collectively, we face daunting global sustainability ● Download resources challenges, including climate change, depletion of natural resources, poverty, population growth, urbanization and congestion." ● Send feedback Alan Mulally, President and CEO Read the full letter from Bill Ford, Executive Chairman Alan Mulally and Bill Ford Fast track to data: ● Products and Customers ● Vehicle Safety ● Environment ● Quality of Relationships ● Community ● Financial Health ● Workplace Safety Overview Our industry, the business environment and societal expectations continue to evolve, and so does our reporting. Learn about our Company and our vision for sustainability. Our Impacts As a major multinational enterprise, our activities have far-reaching impacts on environmental, social and economic systems. Read about our analysis and prioritization of these issues and impacts. Voices Nine people from inside and outside Ford provide their perspectives on key challenges facing our industry and how Ford is responding, including “new mobility,” good practices in the supply chain and the auto industry’s economic impact. This report was published in June 2007. -

“DURATEC ” Engines

2007 NORTH AMERICAN PRODUCT CENTERS Vehicle Lineup SERVICE ENGINEERING 1 NOTES 2 SERVICE ENGINEERING PASSENGER CARS Model/ Transmissions/ Bodystyle Engines Series Transaxles ZX4ST 4-Dr. Station Wagon 2.0L 4V, I-4 Duratec ZXW 3 Dr. Coupe 2.3L 4V, I-4 Duratec MTX-75 ZX3 4F27E ZX4 4-Dr. Sedan 2.0L 4V Duratec & PZEV ZX5 5-Dr. Sedan Model/ Transmissions/ Bodystyle Engines Series Transaxles TR-3650 Base 2-Dr. Coupe 4.0L 2V, V-6 SOHC T50D GT 2-Dr. Convertible 4.6L 3V, V-8 5R55S Model/ Transmissions/ Bodystyle Engines Series Transaxles FNR5 2.3L 4V, I-4 Duratec G5M 4-Dr. Sedan 3.0L 4V, V-6 Duratec 6 Speed (AWF21) Model/ Transmissions/ Bodystyle Engines Series Transaxles FNR5 2.3L 4V, I-4 Duratec G5M 4-Dr. Sedan 3.0L 4V, Duratec 6 Speed (AWF21) SERVICE ENGINEERING 3 PASSENGER CARS Model/ Transmissions/ Bodystyle Engines Series Transaxles 2-Dr. Coupe 5.4L,4V SC V-8 GT650/6 Model/ Transmissions/ Bodystyle Engines Series Transaxles LX SE 3.0L 2V, V-6 4-Dr. Sedan 4F50N VULCAN SES SEL Model/ Transmissions/ Bodystyle Engines Series Transaxles CVT 3.0L 4V, V-6 4-Dr. Sedan DURATEC 6 Speed (AWF21) Model/ Transmissions/ Bodystyle Engines Series Transaxles Police Interceptor Fleet 4.6L 2V, V-8 SOHC 4-Dr. Sedan 4R75E SEFI Standard LX 4 SERVICE ENGINEERING PASSENGER CARS Model/ Transmissions/ Bodystyle Engines Series Transaxles GS LS 4.6L 2V, V-8 SOHC 4-Dr. Sedan 4R75E SEFI LSE Ultimate Model/ Transmissions/ Bodystyle Engines Series Transaxles Executive 4.6L 2V, V-8 SOHC Signature 4-Dr. -

List of ACEA Member Company Petrol Vehicles Compatible with Using “E10” Petrol

List of ACEA member company petrol vehicles compatible with using “E10” petrol Important note applicable for the complete list hereunder: The European Fuel Quality Directive (1) introduced a new market petrol specification from 1st January 2011 that may contain up to 10%vol (% by volume) ethanol (commonly known as “E10”). It is up to the individual country of the European Union and fuel marketers to decide if and when to introduce E10 petrol to the market For vehicles equipped with a spark-ignition (petrol) engine introduced into the EU market, this list indicates their compatibility (or otherwise) with the use of E10 petrol. Note: In countries that offer E10 petrol, before you fill your vehicle with petrol please check that your vehicle is compatible with the use of E10 petrol. If, by mistake, you put E10 petrol into a vehicle that is not declared compatible with the use of E10 petrol, it is recommended that you contact your local vehicle dealer, the vehicle manufacturer or roadside assistance provider who may advise that the fuel tank be drained. If it is necessary to drain the fuel from the tank then you should ensure it is done by a competent organisation and the tank is refilled with the correct grade of petrol for your vehicle. Owners experiencing any issues when using E10 petrol are advised to contact their local vehicle dealer or vehicle manufacturer and to use instead 95RON (or 98RON) petrol that might be identified by “E5” (or have no specific additional marking) in those countries that offer E10 petrol. Other information: The European Fuel Quality Directive (1) requires that countries of the European Union that introduce E10 petrol must ensure that sufficient volumes of today’s petrol (sometimes described as E5) are available for vehicles that are not compatible with the use of E10 petrol. -

No. WYR340107R, WYR340113R Saab 9-3 Limousine Bj

No. WYR340107R, WYR340113R Saab 9-3 Limousine Bj. 09.02 – 02.15 Saab 9-3 Sport Combi Bj. 08.05 – 02.15 Saab 9-3 Cabriolet Bj. 07.03 – 02.15 Cadillac BLS Limousine Bj. 03.06 – 2009 Cadillac BLS Wagon Bj. 12.07 – 2009 KIT 340107 KIT 340113 D Elektrischer Anbausatz für Anhängerkupplung GB Electrical Set for Trailer Connection F Ensemble électrique pour brancher le crochet d’attelage NL Elektrische aansluitset voor trekhaak DK Elektrisk tilslutningssat for trakkrog N Elektrisk monteringssett for tihengerkontakt S Elektrisk förbindelsebyggsats av bogseringskrok FIN Hinauskoukun sähköliitäntäpaketti I Kit di congiunzione del gancio per rimorchio E Juego de conexión eléctrica de gancho de remolque CZ Elektrická připojovací sestava tažného zařízení H Elektromos kábelköteg vonóhorog bekötéséhez RU Электрический присоединительный комплект буксирного крюка LT Elektroninis jungiamasis traukimo kablio rinkinys LV Elektroniskais vilkšanas āķa savienojuma komplekts EST Elektriline tiisli ühenduskomplekt SK Elektroinštalácia pre zapojenie ťažného zariadenia PL Elektryczny zestaw przyłączeniowy haka holowniczego 340107-13R-T / 28.03.2019-00 / Seite 1 von 12 D ! Der Einbau dieses Elektrosatzes muss von einer Fachwerkstatt oder einer entsprechend qualifizierten Person durchgeführt werden. Vor Beginn aller Montagearbeiten unbedingt die Einbauanleitung komplett durchlesen. Nach Einbau des Elektrosatzes ist die Einbauanleitung den Serviceunterlagen des Fahrzeuges beizulegen! Bei unsachgemäßer Anwendung oder Veränderung des Elektrosatzes bzw. der darin befindlichen -

Cadillac BLS Wagon 1.9 Tid Sport Automatik (DPF) Fünftürige Kombilimousine Der Mittelklasse (132 Kw / 180 PS) ADAC Testergebnis Note 2,2

Stand: Januar 2008 ADAC Autotest Test und Text: P. Thywissen Cadillac BLS Wagon 1.9 TiD Sport Automatik (DPF) Fünftürige Kombilimousine der Mittelklasse (132 kW / 180 PS) ADAC Testergebnis Note 2,2 Der Cadillac BLS ist identisch mit dem Saab 9-3, hat nur eine geänderte Front und ist teurer als dieser. Der Motor, den man auch aus dem Opel Vectra kennt, ist kräftig, dabei laufruhig aber nicht allzu genügsam. Die umwelt- und gesund- heitsschädigenden Rußpartikel werden von einem geschlossenem Filtersystem wirksam abgefangen. Die aufpreispflichtige 6-Gang-Automatik arbeitet weitge- hend ruckfrei und situationsangepasst, sie hält dabei die Motordrehzahlen ange- nehm niedrig. Fazit: Otisch ein kleiner Cadillac mit den Werten des soliden Saab 9-3 und des Opel Vectra. Ziemlich teuer: 42.680 € mit Navigation, Radio und Einparkhilfe. Karosserievarianten: Stufenheck. Konkurrenten: Alfa 159, Audi A4, BMW 3er, Ford Mondeo, Honda Accord, Jaguar X-Type, Mazda 6, Mercedes C-Klasse, Opel Vectra, Peugeot 407, Renault Laguna, Saab 9-3, Skoda Octavia, Toyota Avensis, Volvo V50, VW Passat.. + gute Verarbeitung + variabler Kofferraum + gute Heizung u. Klimaanlage + Stabilitätssystem Serie + sehr gute Fahrleistungen + ruhiger Dieselmotor + hohe passive Sicherheit − Frontantriebseinflüsse − Traktionsprobleme − dünnes Servicenetz reduziert Kraftstoffverbrauch erhöhende Luftwirbel. Auf der Dach- Karosserie/Kofferraum Note 2,4 reling sind bis zu 100 kg Last erlaubt. Verarbeitung Note: 1,9 − Bei einer Reifenpanne steht nur ein Reparaturset zur Verfügung, + Die Verarbeitung der Karosserie macht einen guten Eindruck, obwohl eine Mulde für ein vollwertiges Rad vorhanden ist. Spaltabstände sind gleichmäßig, Türschweller und -Ausschnitte Sicht Note: 2,7 sind gegen Schmutz von außen abgedichtet. Materialien im Innen- Bei der ADAC-Rundumsichtmessung schneidet der BLS Wagon raum sind von ordentlicher Qualität und sauber verarbeitet, Blen- insgesamt mit noch durchschnittlicher Note ab. -

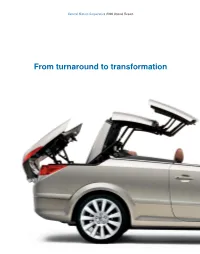

From Turnaround to Transformation

General Motors Corporation 2006 Annual Report From turnaround to transformation Contents 3 Letter to Stockholders 44 Management’s Discussion and Analysis 76 Notes to Consolidated Financial Statements 4 Financial Highlights 67 Disclosure Controls and Procedures 125 Selected Financial Data 10 Design Transformation 68 Management’s Report on Internal Control 126 Board of Directors and Committees 22 Global Transformation over Financial Reporting 128 Senior Leadership Group 28 Technology Transformation 70 Report of Independent Registered Inside Back Cover 36 People Transformation Public Accounting Firm General Information 42 At a Glance 72 Consolidated Financial Statements Front cover: 2007 Opel Astra TwinTop There’s a major turnaround under way at GM. We made broad and signifi cant progress in 2006. We accomplished more than people expected, and in many cases, we even surpassed our goals, on or ahead of schedule. We’re not fi nished. There’s much more to do. But our growing confi dence and excitement is rooted in the fact that we’re not just fi xing problems. We’re transforming GM for fundamental, sustainable, long-term success. General Motors Corporation 1 A full-scale production clay model of the 2009 Chevrolet Camaro starts to take shape at GM’s Warren, Michigan, Design Center, Rear Wheel Drive Performance Studio. Bob Lutz Rick Wagoner Fritz Henderson Vice Chairman, Chairman and Vice Chairman and Global Product Development Chief Executive Offi cer Chief Financial Offi cer 2 General Motors Corporation Dear Stockholders: Our company is in a crucial period in its nearly 100-year history. goals of steady growth, solid profi tability and positive cash I’m pleased to report that, in 2006, the entire GM team rose up generation. -

North American Product Centers

2005 NORTH AMERICAN PRODUCT CENTERS Vehicle Lineup SERVICE ENGINEERING 1 PASSENGER CARS Powertrains Model/ Transmissions/ Bodystyle Engines Series Transaxles 4-Dr. Sedan 2.0L 4V, I-4 Duratec ZTS 4-Dr. Station 2.3L 4V I4 Duratec Wagon ZXW 4-Dr. Station MTX-75 Wagon 4F27E 2.0L 4V Duratec & ZX3 3 Dr. Coupe PZEV ZX4 4-Dr. Sedan ZX\5 5-Dr. Sedan Powertrains Model/ Transmissions/ Bodystyle Engines Series Transaxles TR-3650 Base 2-Dr. Coupe 4.0L 2V, V-6 SOHC T50D GT 2-Dr. Convertible 4.6L 3V, V-8 5R55S Powertrains Model/ Transmissions/ Bodystyle Engines Series Transaxles Coupe 3.9L, V-8 5R55S Convertible Powertrains Model/ Transmissions/ Bodystyle Engines Series Transaxles 2-Dr. Coupe 5.4L, V-8 T56 SERVICE ENGINEERING 3 PASSENGER CARS Powertrains Model/ Transmissions/ Bodystyle Engines Series Transaxles 3.0L 2V, V-6 LX VULCAN 4-Dr. Sedan SE 3.0L 4V, V-6 4-Dr. Station 4F50N SES DURATEC Wagon SEL 3.0L 2V, V-6 VULCAN FF Powertrains Model/ Transmissions/ Bodystyle Engines Series Transaxles 3.0L 4V, V-6 4-Dr. Sedan GS DURATEC 4-Dr. Station 4F50N LS 3.0L 2V, V-6 Wagon VULCAN Powertrains Model/ Transmissions/ Bodystyle Engines Series Transaxles 3.0L 4V, V-6 CVT 4-Dr. Sedan DURATEC AWF21 6 Speed Powertrains Model/ Transmissions/ Bodystyle Engines Series Transaxles Police Interceptor 4.6L 2V, V-8 SOHC Fleet 4-Dr Sedan 4R70E SEFI Standard LX 4 SERVICE ENGINEERING PASSENGER CARS Powertrains Model/ Transmissions/ Bodystyle Engines Series Transaxles GS LS 4.6L 2V, V-8 SOHC 4-Dr. -

Cadillac Bls User Manual

cadillac bls user manual File Name: cadillac bls user manual.pdf Size: 3041 KB Type: PDF, ePub, eBook Category: Book Uploaded: 13 May 2019, 14:23 PM Rating: 4.6/5 from 599 votes. Status: AVAILABLE Last checked: 19 Minutes ago! In order to read or download cadillac bls user manual ebook, you need to create a FREE account. Download Now! eBook includes PDF, ePub and Kindle version ✔ Register a free 1 month Trial Account. ✔ Download as many books as you like (Personal use) ✔ Cancel the membership at any time if not satisfied. ✔ Join Over 80000 Happy Readers Book Descriptions: We have made it easy for you to find a PDF Ebooks without any digging. And by having access to our ebooks online or by storing it on your computer, you have convenient answers with cadillac bls user manual . To get started finding cadillac bls user manual , you are right to find our website which has a comprehensive collection of manuals listed. Our library is the biggest of these that have literally hundreds of thousands of different products represented. Home | Contact | DMCA Book Descriptions: cadillac bls user manual The specifications, design particulars and illus tinual improvement, we retain the right to trations included in the manual are not binding. Radiator fan may start at any time.We recommend that you contact an authorised Cadillac workshop for Xenon bulb replacement 3. The diagonal strap must be as far WARNING in on the shoulder as possible. Fasten the belt by smoothly pulling out the The belt guide for the front seat belts can be Press the red button on the buckle to. -

The Re-Innovation of Ford Motor Company to a Sustainable Lean Enterprise

University of Louisville ThinkIR: The University of Louisville's Institutional Repository Electronic Theses and Dissertations 8-2006 The re-innovation of Ford Motor Company to a sustainable lean enterprise. Kenneth A. Ryan 1968- University of Louisville Follow this and additional works at: https://ir.library.louisville.edu/etd Recommended Citation Ryan, Kenneth A. 1968-, "The re-innovation of Ford Motor Company to a sustainable lean enterprise." (2006). Electronic Theses and Dissertations. Paper 1243. https://doi.org/10.18297/etd/1243 This Master's Thesis is brought to you for free and open access by ThinkIR: The University of Louisville's Institutional Repository. It has been accepted for inclusion in Electronic Theses and Dissertations by an authorized administrator of ThinkIR: The University of Louisville's Institutional Repository. This title appears here courtesy of the author, who has retained all other copyrights. For more information, please contact [email protected]. THE RE-INNOVATION OF FORD MOTOR COMPANY TO A SUSTAINABLE LEAN ENTERPRISE By Kenneth A. Ryan B.S.A.E., St. Louis University, 1990 B.S.M.E., University of Missouri, 1991 A Thesis Submitted to the Faculty of the University of Louisville J.B. Speed School of Engineering in Partial Fulfillment of the Requirements for the Professional Degree Master of Engineering in Engineering Management July, 2006 11 Copyright, 2006 Kenneth A. Ryan 111 THE RE-INNOVATION OF FORD MOTOR COMPANY TO A SUSTAINABLE LEAN ENTERPRISE Submitted by: Kenneth A. Ryan A Thesis Approved on 6/19/06 (Date) by the following Reading and Examination Committee: Surja Alexander, PhD., P.E., Thesis Director William Biles, PhD., P.E., Faculty Advisor John S. -

Small Suvs Are Big Winners in 2007

20080526-0022_23-ANE.qxd 5/30/08 10:43 AM Page 18 PAGE 22 · www.autonewseurope.com May 26, 2008 Market analysis by segment, European sales ROADSTER & CONVERTIBLE Small SUVs are big winners in 2007 The arrival of the new 207 CC (shown) helped Peugeot take the top spot in the market researchers JATO Dynamics shows Changing segments segment from Renault. Peugeot’s Luca Ciferri that the the big winners in 2007 were small 307CC was No. 5 in the niche. Automotive News Europe SUVs, premium coupes and exotic cars. The Europe’s 2007 winners and losers big losers were volume coupes, small mini- Small SUV +49.1% 2007 2006 % Change Seg.share% Minicar sales last year grew a modest vans and large SUVs. Premium coupe +37.0% Peugeot 207CC/206CC 51,181 29,313 74.6% 19.8% 8.3 percent after a 22.1 percent rise in 2006, The next two pages offer sales results Exotics +29.4% VW Eos 35,293 22,128 59.5% 13.6% despite the introduction last summer of the and analysis for the 22 market segments Opel/Vauxhall Astra TwinTop 26,303 17,525 50.1% 10.2% new Fiat 500, the reigning European Car of that ANE covers. Coupe -31.7% Renault Megane 25,577 33,156 -22.9% 9.9% the Year, and the Renault Twingo. Small minivan -22.6% Peugeot 307CC 19,824 32,653 -39.3% 7.7% An analysis of 2007 sales by Automotive You can download this list as a PDF from our Large SUV -19.1% Smart ForTwo 19,610 10,266 91.0% 7.6% News Europe using data from UK-based Web site at www.autonews.com/segments08 Mazda MX5 18,962 19,338 -1.9% 7.3% Opel/Vauxhall Tigra TwinTop 12,196 20,478 -40.4% 4.7% Ford Focus Coupe Cabriolet 10,033 83 – 3.9% MINICAR Citroen C3 Pluriel 9,983 12,357 -19.2% 3.9% UPPER MEDIUM SEGMENT TOTAL 258,757 245,077 5.6% 1.58% After surpassing the 1 million mark for the first time in 2006, total The new Ford Mondeo’s 13% sales increase made it the upper-medi- Segment total includes: Chrysler Crossfire, PT Cruiser and Sebring; Daihatsu Copen, minicar sales grew another 8.3% last year to 1,101,104 um segment’s No.