Collateralized Loan Obligations Introduction

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mortgage-Backed Securities & Collateralized Mortgage Obligations

Mortgage-backed Securities & Collateralized Mortgage Obligations: Prudent CRA INVESTMENT Opportunities by Andrew Kelman,Director, National Business Development M Securities Sales and Trading Group, Freddie Mac Mortgage-backed securities (MBS) have Here is how MBSs work. Lenders because of their stronger guarantees, become a popular vehicle for finan- originate mortgages and provide better liquidity and more favorable cial institutions looking for investment groups of similar mortgage loans to capital treatment. Accordingly, this opportunities in their communities. organizations like Freddie Mac and article will focus on agency MBSs. CRA officers and bank investment of- Fannie Mae, which then securitize The agency MBS issuer or servicer ficers appreciate the return and safety them. Originators use the cash they collects monthly payments from that MBSs provide and they are widely receive to provide additional mort- homeowners and “passes through” the available compared to other qualified gages in their communities. The re- principal and interest to investors. investments. sulting MBSs carry a guarantee of Thus, these pools are known as mort- Mortgage securities play a crucial timely payment of principal and inter- gage pass-throughs or participation role in housing finance in the U.S., est to the investor and are further certificates (PCs). Most MBSs are making financing available to home backed by the mortgaged properties backed by 30-year fixed-rate mort- buyers at lower costs and ensuring that themselves. Ginnie Mae securities are gages, but they can also be backed by funds are available throughout the backed by the full faith and credit of shorter-term fixed-rate mortgages or country. The MBS market is enormous the U.S. -

HIGH YIELD OR “JUNK' BONDS, HAVEN OR HORROR by Mason A

HIGH YIELD OR “JUNK’ BONDS, HAVEN OR HORROR By Mason A. Dinehart III, RFC A high yield, or “junk” bond is a bond issued by a company that is considered to be a higher credit risk. The credit rating of a high yield bond is considered “speculative” grade or below “investment grade”. This means that the chance of default with high yield bonds is higher than for other bonds. Their higher credit risk means that “junk” bond yields are higher than bonds of better credit quality. Studies have demonstrated that portfolios of high yield bonds have higher returns than other bond portfolios, suggesting that the higher yields more than compensate for their additional default risk. It should be noted that “unrated” bonds are legally in the “junk” category and may or may not be speculative in terms of credit quality. High yield or “junk” bonds get their name from their characteristics. As credit ratings were developed for bonds, the credit agencies created a grading system to reflect the relative credit quality of bond issuers. The highest quality bonds are “AAA” and the credit scale descends to “C” and finally to “D” or default category. Bonds considered to have an acceptable risk of default are “investment grade” and encompass “BBB” bonds (Standard & Poors) or “Baa” bonds (Moody’s) and higher. Bonds “BB” and lower are called “speculative grade” and have a higher risk of default. Rulemakers soon began to use this demarcation to establish investment policies for financial institutions, and government regulation has adopted these standards. Since most investors were restricted to investment grade bonds, speculative grade bonds soon developed negative connotations and were not widely held in investment portfolios. -

Understanding Alpha Versus Beta in High Yield Bond Investing

PERITUS ASSET MANAGEMENT, LLC Market Commentary Independent Credit Research – Leveraged Finance – July 2012 Understanding Alpha versus Beta in High Yield Bond Investing Investors have come to recognize that there is a secular change occurring in financial markets. After the 2008 meltdown, we have watched equities stage an impressive rally off the bottom, only to peter out. There is no conviction and valuations are once again stretched given the lack of growth as the world economy remains on shaky ground. In another one of our writings (“High Yield Bonds versus Equities”), we discussed our belief that U.S. businesses would plod along, but valuations would continue their march toward the lower end of their historical range. So far, this looks like the correct call. Europe still hasn’t been fixed, the China miracle is slowing and, perhaps, the commodity supercycle is also in the later innings. The amount of debt assumed by the developed world is unsustainable so deleveraging began a few years ago. These are not short or pleasant cycles and both governments and individuals will be grumpy participants in this event. It simply means that economic growth will be subdued for years to come. I have never really been able to understand economic growth rates that are significantly ahead of the population growth anyway…oh yeah, the productivity miracle. I have written chapter and verse on the history of financial markets and where returns have come from: yield. Anyone with access to the internet can verify that dividends, dividend growth and dividend re-investment are what have driven stock returns over the decades. -

Foundations of High-Yield Analysis

Research Foundation Briefs FOUNDATIONS OF HIGH-YIELD ANALYSIS Martin Fridson, CFA, Editor In partnership with CFA Society New York FOUNDATIONS OF HIGH-YIELD ANALYSIS Martin Fridson, CFA, Editor Statement of Purpose The CFA Institute Research Foundation is a not- for-profit organization established to promote the development and dissemination of relevant research for investment practitioners worldwide. Neither the Research Foundation, CFA Institute, nor the publication’s editorial staff is responsible for facts and opinions presented in this publication. This publication reflects the views of the author(s) and does not represent the official views of the CFA Institute Research Foundation. The CFA Institute Research Foundation and the Research Foundation logo are trademarks owned by The CFA Institute Research Foundation. CFA®, Chartered Financial Analyst®, AIMR- PPS®, and GIPS® are just a few of the trademarks owned by CFA Institute. To view a list of CFA Institute trademarks and the Guide for the Use of CFA Institute Marks, please visit our website at www.cfainstitute.org. © 2018 The CFA Institute Research Foundation. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the copyright holder. This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is sold with the understanding that the publisher is not engaged in rendering legal, accounting, or other professional service. If legal advice or other expert assistance is required, the services of a competent professional should be sought. -

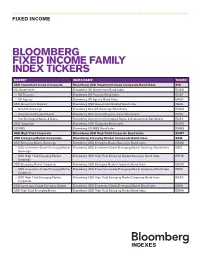

Bloomberg Fixed Income Family Index Tickers

///////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////// FIXED INCOME BLOOMBERG FIXED INCOME FAMILY INDEX TICKERS MARKET INDEX NAME TICKER USD Investment Grade Composite Bloomberg USD Investment Grade Composite Bond Index BIG US Government Bloomberg US Government Bond Index BUSG » US Treasury Bloomberg US Treasury Bond Index BUSY » US Agency Bloomberg US Agency Bond Index BAGY USD Government Related Bloomberg USD Government Related Bond Index BGRL » Non-US Sovereign Bloomberg Non-US Sovereign Bond Index BNSO » Government Regional/Local Bloomberg Government Regional/Local Bond Index BRGL » Gov Developed Banks & Supra Bloomberg Government Developed Banks & Supranational Bond Index BDEV USD Corporate Bloomberg USD Corporate Bond Index BUSC US MBS Bloomberg US MBS Bond Index BMBS USD High Yield Corporate Bloomberg USD High Yield Corporate Bond Index BUHY USD Emerging Market Composite Bloomberg Emerging Market Composite Bond Index BEM USD Emerging Market Sovereign Bloomberg USD Emerging Market Sovereign Bond Index BEMS » USD Investment Grade Emerging Market Bloomberg USD Investment Grade Emerging Market Sovereign Bond Index BEIS Sovereign » USD High Yield Emerging Market Bloomberg USD High Yield Emerging Market Sovereign Bond Index BEHS Sovereign USD Emerging Market Corporate Bloomberg USD Emerging Market Corporate Bond Index BEMC » USD Investment Grade Emerging Market Bloomberg USD Investment Grade Emerging Market Corporate Bond Index BIEM Corporate -

GGD-89-48 High Yield Bonds

GAO Iteport, to Congressional Rcqueskrs -..- ~--. .--- March 1!))I!) HIGH YIELD BONDS Issues Concerning Thrift Investments in High Yield Bonds i ,I unitedstates General Accounting Office GAO Wahington, D.C. 20548 General Government Division B-231276.8 March 2, I989 The Honorable Donald W. Riegle Chairman, Committee on Banking, Housing and Urban Affairs United States Senate The Honorable Henry B. Gonzalez Chairman, Committee on Banking, Finance and Urban Affairs House of Representatives This report completes our responseto the requirements of Section 1201 of the Competitive Equality Banking Act of 1987 (P.L. lOO-86),which directed us to study several aspects of the high yield bond market As required by the act, we did our work in consultation with the Securities and Exchange Commission, the Federal Home Loan Bank Board, the Comptroller of the Currency, the Board of Governors of the Federal ReserveSystem, the Federal Savings and Loan Insurance Corporation, the Federal Deposit Insurance Corporation, the Secretary of the Treasury, and the Secretary of Labor. Copies of this report are being provided to those agenciesand are available to others on request. This report was prepared under the direction of Craig A. Simmons, Director, Financial Institutions and Markets Issues, Other major contributors are listed in the appendix. Richard L. Fogel Assistant Comptroller General Ekecutive Summ~ The growth of the high yield (“junk”) bond market in the 1980s has Purpose been fraught with controversy. Numerous congressionalhearings have focused on the role of these bonds as a tool to finance takeovers-of com- panies. Major figures in the high yield bond market have been the target of investigations by congressionalcommittees, the Securities and Exchange Commission, and the Justice Department. -

Chapter 3 Fixed Income Securities

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. • Fixed-income securities. • Stocks. • Real assets (capital budgeting). Part C Determination of risk-adjusted discount rates. Part D Introduction to derivatives. Main Issues • Fixed-Income Markets • Term Structure of Interest Rates • Interest Rate Risk • Inflation Risk • Credit Risk Chapter 3 Fixed Income Securities 3-1 1 Fixed-Income Markets Definition: Fixed-income securities are financial claims with promised cash flows of fixed amount paid at fixed dates. Classification of Fixed-Income Securities: 1. Treasury Securities: • U.S. Treasury securities (bills, notes, bonds). • Bunds, JGBs, U.K. Gilts ... 2. Federal Agency Securities: • Securities issued by federal agencies (FHLB, FNMA ...). 3. Corporate Securities: • Commercial paper. • Medium-term notes (MTNs). • Corporate bonds ... 4. Municipal Securities. 5. Mortgage-Backed Securities. 6. ... Fall 2006 c J. Wang 15.401 Lecture Notes 3-2 Fixed Income Securities Chapter 3 Overview of Fixed-income Markets Composition of U.S. Debt Markets (2005) Market value % (in trillion dollars) Treasury 4.17 16.5 Corporate 4.99 19.7 Mortgage 5.92 23.4 Agency 2.60 10.3 Munies 2.23 8.8 Asset-Backed 1.96 7.7 Money Market 3.47 13.7 Total 25.33 Current Trends T. Corp. MBS Agency ABS Munies MM Total 1995 3.31 1.94 2.35 0.84 0.32 1.29 1.18 11.23 1996 3.44 2.12 2.49 0.93 0.40 1.30 1.39 12.01 1997 3.44 2.36 2.68 1.02 0.54 1.32 1.69 13.05 1998 3.34 2.71 2.96 1.30 0.73 1.40 1.98 14.42 1999 3.27 3.05 3.33 1.62 0.90 1.46 2.34 15.96 2000 2.95 3.36 3.56 1.85 1.07 1.48 2.66 16.95 2001 2.97 3.84 4.13 2.15 1.28 1.60 2.57 18.53 2002 3.20 4.09 4.70 2.29 1.54 1.73 2.55 20.15 2003 3.57 4.46 5.31 2.64 1.69 1.89 2.53 22.10 2004 3.94 3.70 5.47 2.75 1.83 2.02 2.87 23.58 2005 4.17 4.99 4.92 2.60 1.96 2.23 3.47 25.33 15.401 Lecture Notes c J. -

Managing Fixed Income Late in the Credit Cycle: Navigating the Path Forward

INCOME INVESTING Managing fixed income late in the credit cycle: navigating the path forward nuveen knows Highlights • While we are clearly in the late stage of the credit cycle, we don’t think a recession is imminent and believe investors should feel comfortable investing in credit 2Q19 markets throughout the rest of 2019. • We believe investors should focus on higher-quality issues with improving credit fundamentals, while seeking to diversify across industries and geographies. • Nuveen’s sector specialist teams are finding attractive opportunities in U.S. credit sectors, including high yield, but they are increasingly diversifying into other higher-income areas, such as emerging market debt and leveraged loans. • Active management can add value in any environment, but we believe it is especially beneficial at the current stage of the credit cycle. The multi-trillion-dollar question for investors: How late are we in the credit cycle, and what are the portfolio implications? That’s the question we most often hear from our clients. And while there are few certainties in life or markets, we feel confident in our answer: We are clearly in the late stage of the credit cycle. But “late” doesn’t mean “done,” and credit cycles don’t die of old age. Rather, a combination of fundamentals and sentiment bring about their demise, and even in their later stages, savvy investors can find opportunities not only to protect their investments, but to position their portfolios for an emphasis on income as the cycle turns. Nuveen believes most investors should be comfortable investing in the credit markets throughout the rest of 2019. -

Product Pitchbook

2Q 2021 Separately Managed Accounts WESTERN ASSET MUNICIPAL BOND LADDERS Separately Managed Accounts (SMAs) are investment services provided by Legg Mason Private Portfolio Group, LLC (LMPPG), a federally registered investment advisor. Client portfolios are managed based on investment instructions or advice provided by one or more of the following Franklin Templeton affiliated subadvisors: ClearBridge Investments, LLC. Management is implemented by LMPPG, the designated subadvisor or, in the case of certain programs, the program sponsor or its designee. These materials are being provided for illustrative and informational purposes only. The information contained herein is obtained from multiple sources that are believed to be reliable. However, such information has not been verified, and may be different from the information included in documents and materials created by the sponsor firm in whose investment program a client participates. Some sponsor firms may require that these materials be preceded or accompanied by investment profiles or other documents or materials prepared by such sponsor firms, which will be provided upon a client's request. For additional information, documents and/or materials, please speak to your financial professional or contact your sponsor firm. INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE Introduction | Franklin Templeton Franklin Templeton We aim to offer the best of both worlds: global strength and boutique specialization. Providing real customization backed by the scale and -

Corporate Bonds

investor’s guide CORPORATE BONDS i CONTENTS What are Corporate Bonds? 1 Basic Bond Terms 2 Types of Corporate Bonds 5 Bond Market Characteristics 7 Understanding the Risks 8 Understanding Collateralization and Defaults 13 How Corporate Bonds are Taxed 15 Credit Analysis and Other Important Considerations 17 Glossary 21 All information and opinions contained in this publication were produced by the Securities Industry and Financial Markets Association (SIFMA) from our membership and other sources believed by SIFMA to be accurate and reli- able. By providing this general information, SIFMA is neither recommending investing in securities, nor providing investment advice for any investor. Due to rapidly changing market conditions and the complexity of investment deci- sions, please consult your investment advisor regarding investment decisions. ii W H A T A R E C O R P O R A T E BONDS? Corporate bonds (also called “corporates”) are debt obligations, or IOUs, issued by privately- and publicly-owned corporations. When you buy a corpo- rate bond, you essentially lend money to the entity that issued it. In return for the loan of your funds, the issuer agrees to pay you interest and to return the original loan amount – the face value or principal - when the bond matures or is called (the “matu- rity date” or “call date”). Unlike stocks, corporate bonds do not convey an ownership interest in the issuing corporation. Companies use the funds they raise from selling bonds for a variety of purposes, from building facilities to purchasing equipment to expanding their business. Investors buy corporates for a variety of reasons: • Attractive yields. -

Morningstar Global Fixed Income Classification Methodology

? Morningstar Global Fixed Income Classification Morningstar Research Introduction Effective Oct. 31, 2016 Fixed-Income Sectors Contents The fixed-income securities and fixed-income derivative exposures within a portfolio are mapped into 1 Introduction Secondary Sectors that represent the most granular level of classification. Each item can also be 2 Super Sectors 10 Sectors grouped into one of several higher-level Primary Sectors, which ultimately roll up to five fixed-income Super Sectors. Important Disclosure The conduct of Morningstar’s analysts is governed Cash Sectors by Code of Ethics/Code of Conduct Policy, Personal Cash securities and cash-derivative exposures within a portfolio are mapped into Secondary Sectors that Security Trading Policy (or an equivalent of), and Investment Research Policy. For information represent the most granular level of classification. Each item can also be grouped into cash & regarding conflicts of interest, please visit: http://global.morningstar.com/equitydisclosures equivalents Primary Sector and into cash & equivalents Super Sector (cash & equivalents Primary Sector = cash & equivalents Super Sector ). Morningstar includes cash within fixed-income sectors. Cash is not a bond, but it is a type of fixed- income. When bond-fund managers are feeling nervous about interest rates rising, they might increase their cash stake to shorten the portfolio’s duration. Moving assets into cash is a defensive strategy for interest-rate risk. In addition, Morningstar includes securities that mature in less than 92 days in the definition of cash. The cash & equivalents Secondary Sectors allow for more-detailed identification of cash, allowing clients to see, for example, if the cash holdings are in currency or short-term government bonds. -

SIFMA Research Quarterly – 1Q21 US Fixed Income Markets – Issuance & Trading

Executive Summary SIFMA Research Quarterly – 1Q21 US Fixed Income Markets – Issuance & Trading April 2021 The SIFMA Research Quarterlies contain data and statistics on U.S. markets. The fixed income reports are split into two – (1) issuance and trading, (2) outstanding – given a delay in the reporting of outstanding data. The reports cover data on total U.S. fixed income markets, as captured in the SIFMA Research database: U.S. Treasuries, mortgage-backed securities, corporate bonds, municipal securities, federal agency securities, asset-backed securities, money markets (outstanding only), repurchase agreements (outstanding only) and secured overnight financing rate. All reports, including the equity quarterly, and corresponding databases can be found at: www.sifma.org/research US Fixed Income Markets – Issuance & Trading Page | 1 Executive Summary Contents Executive Summary ................................................................................................................................................................................... 4 US Fixed Income Markets vs. Rest of World .............................................................................................................................................. 4 Quarterly Performance ............................................................................................................................................................................... 5 Chart Book: Total Fixed Income ................................................................................................................................................................