18 2Nd 06 E.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CSR for ITOCHU Corporation (PDF 780KB)

CSR for ITOCHU Corporation ITOCHU Corporation is pursuing multifacetted corporate activities in various regions of the world and a wide range of fields, and as such, ITOCHU is well aware of how significant its impact on society is. We believe that corporate social responsibility (CSR) lies in corporate thought and action on the question of how to play a role in building sustainable societies through business activities. We also believe that our mission is to fulfill our Corporate Social Responsibility as a global enterprise, always working from the viewpoint of whether we are contributing to the countries of the world and to society. ITOCHU Group Corporate Message ITOCHU founder Chubei Itoh first launched a wholesale linen business in 1858. For more than 150 years since, ITOCHU has passed down the spirit of sampo yoshi (good for the buyer, seller and society), a management philosophy embraced by Ohmi merchants that is the source of its CSR thinking today. After considering ways to demonstrate its commitment to society as an international corporation and to put this commitment into practice, in 1992 ITOCHU formulated “Committed to the Global Good” as a corporate philosophy. The conceptual framework for this philosophy was reorganized in 2009. In order for all employees to properly understand the responsibility that the ITOCHU Group is charged with fulfilling for society and to make this philosophy an integral part of actions everyday, its core element, “Committed to the Global Good,” was set as the ITOCHU Mission for the entire ITOCHU Group. Accompanying this is a new set of five values, called the ITOCHU Values, considered vital for enabling each employee to fulfill their role in realizing the ITOCHU Mission. -

Financial Section 2014

For the Year ended March 31, 2014 ended March For the Year Financial Section 2014 Financial Section 2014 ITOCHU Corporation ITOCHU Corporation FINANCIAL SECTION 2014 1 Contents 2 Six-year Summary (U.S. GAAP) 3 Summary (IFRS) 4 Management’s Discussion and Analysis of Financial Condition and Results of Operations 32 Consolidated Statement of Financial Position 34 Consolidated Statement of Comprehensive Income 36 Consolidated Statement of Changes in Equity 37 Consolidated Statement of Cash Flows 38 Notes to Consolidated Financial Statements 112 Independent Auditor’s Report 114 Supplementary Explanation 115 Management Internal Control Report (Translation) 116 Independent Auditor’s Report (filed under the Financial Instruments and Exchange Act of Japan) Forward-Looking Statements This Annual Report contains forward-looking statements regarding ITOCHU Corporation’s corporate plans, strategies, forecasts, and other statements that are not historical facts. They are based on current expectations, estimates, forecasts and projections about the industries in which ITOCHU Corporation operates. As the expectations, estimates, forecasts and projections are subject to a number of risks, uncertainties and assumptions, including without limitation, changes in economic conditions; fluctuations in currency exchange rates; changes in the competitive environment; the outcome of pending and future litigation; and the continued availability of financing; financial instruments and financial resources, they may cause actual results to differ materially from those presented in such forward-looking statements. ITOCHU Corporation, therefore, wishes to caution that readers should not place undue reliance on forward-looking statements, and, further that ITOCHU Corporation undertakes no obligation to update any forward- looking statements as a result of new information, future events or other developments. -

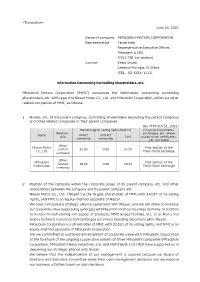

<Translation> June 24, 2021 Name of Company

<Translation> June 24, 2021 Name of company: MITSUBISHI MOTORS CORPORATION Representative: Takao Kato Representative Executive Officer, President & CEO (7211 TSE 1st section) Contact: Keiko Sasaki General Manager, IR Office (TEL.03-3456-1111) Information Concerning Controlling Shareholders, etc. Mitsubishi Motors Corporation (“MMC”) announces the information concerning controlling shareholders, etc. with regard to Nissan Motor Co., Ltd. and Mitsubishi Corporation, which are other related companies of MMC, as follows: 1 Names, etc. of the parent company, controlling shareholders (excluding the parent company) and other related companies or their parent companies (As of March 31, 2021) Percentage of voting rights held (%) Financial instruments Relation- exchanges, etc. where Name Direct Indirect ship Total issued share certificates, ownership ownership etc. are listed Other Nissan Motor First Section of the related 34.03 0.00 34.03 Co., Ltd. Tokyo Stock Exchange company Other Mitsubishi First Section of the related 20.02 0.00 20.02 Corporation Tokyo Stock Exchange company 2 Position of the company within the corporate group of its parent company, etc. and other relationships between the company and its parent company, etc. Nissan Motor Co., Ltd. (“Nissan”) is the largest shareholder of MMC with 34.03% of its voting rights, and MMC is an equity-method associate of Nissan. We have concluded a strategic alliance agreement with Nissan, and we will strive to increase our corporate value by pursuing synergies with Nissan in all of our business domains. In addition to mutual manufacturing and supply of products, MMC leases facilities, etc. to or from, and shares technical resources and exchanges personnel including executives with, Nissan. -

Into the Future on Three Wheels

Mitsubishi The 9th Grand Prix Winner A Bimonthly Review of the Mitsubishi Companies and Their People Around the World 2009-2010 Asian Children's2008- Enikki Festa 2009 Winners December & January Grand Prix Japan Humans are social beings. People live in groups. We Bangladeshis like to live with our parents, our brothers and sisters, our grandparents, and other relatives. In our family, I live with my brother, my parents, and my grandmother. We share each other’s joys and sorrows. That makes our lives fulfilling. Cycling * The above sentences contained in this Enikki has been translated from Bengali to English. Into the Future The 9th Grand Prix Winner on Three Wheels Sadia Islam Mowtushy Age:11 Girl People’s Republic of Bangladesh “Wrapping Up the Year with Toshikoshi Soba” oba is a Japanese noodle that is eaten in various ways longevity, because it is long and thin. There are many other depending on the season. In summer, soba is served cold explanations and no single theory can claim to be the definitive S and dipped in a chilled sauce; in winter, it comes in a hot truth, but this only adds to the mystique of toshikoshi soba. broth. Soba is often garnished with tasty tidbits, such as tempura shrimp, or with a bit of boiled spinach to add a touch of color. Soba has been a favorite of Japanese people for centuries and the popular buckwheat noodle has even secured a role in various Japanese traditions, including the New Year’s celebration. Japanese people commonly eat soba on New Year’s Eve, when the old year intersects with the new year, and this is known as toshikoshi or “year-crossing” soba. -

Monthly Trading Value of Most Active Stocks (Sep.2011) 1St Section

Monthly Trading Value of Most Active Stocks (Sep.2011) 1st Section Rank Code Issue Trading Value \ mil. 1 3632 Gree,Inc. 621,681 2 9984 SOFTBANK CORP. 525,472 3 7203 TOYOTA MOTOR CORPORATION 508,576 4 6954 FANUC CORPORATION 474,028 5 9501 The Tokyo Electric Power Company,Incorporated 383,303 6 8316 Sumitomo Mitsui Financial Group,Inc. 371,373 7 9433 KDDI CORPORATION 367,528 8 7751 CANON INC. 344,371 9 6301 KOMATSU LTD. 342,788 10 8306 Mitsubishi UFJ Financial Group,Inc. 335,566 11 7267 HONDA MOTOR CO.,LTD. 325,041 12 7201 NISSAN MOTOR CO.,LTD. 300,329 13 8411 Mizuho Financial Group,Inc. 292,432 14 2432 DeNA Co.,Ltd. 280,373 15 8058 Mitsubishi Corporation 273,889 16 2914 JAPAN TOBACCO INC. 268,618 17 8031 MITSUI & CO.,LTD. 257,682 18 6502 TOSHIBA CORPORATION 257,679 19 6758 SONY CORPORATION 247,379 20 6501 Hitachi,Ltd. 245,548 21 9983 FAST RETAILING CO.,LTD. 242,756 22 4502 Takeda Pharmaceutical Company Limited 232,589 23 9437 NTT DOCOMO,INC. 229,511 24 9432 NIPPON TELEGRAPH AND TELEPHONE CORPORATION 199,544 25 8591 ORIX CORPORATION 197,121 26 8604 Nomura Holdings, Inc. 182,408 27 3382 Seven & I Holdings Co.,Ltd. 182,138 28 8035 Tokyo Electron Limited 161,453 29 7202 ISUZU MOTORS LIMITED 161,231 30 7011 Mitsubishi Heavy Industries,Ltd. 159,430 31 6971 KYOCERA CORPORATION 153,831 32 5233 TAIHEIYO CEMENT CORPORATION 152,939 33 6665 Elpida Memory,Inc. 151,463 34 6762 TDK Corporation 150,719 35 8001 ITOCHU Corporation 149,228 36 6752 Panasonic Corporation 148,099 37 4063 Shin-Etsu Chemical Co.,Ltd. -

Financial Crime

Japan’s Shifting Geopolitical and Geo-economic relations in Africa A view from Japan Inc. By Dr Martyn Davies, Managing Director: Emerging Markets & Africa, Frontier Advisory Deloitte and Kira McDonald, Research Analyst, Frontier Advisory Deloitte The Japanese translation was published in changer” in Africa since the turn of the century; Building Hitotsubashi Business Review geopolitical stature and influence in Africa with a (Vol. 63, No. 1, June 2015, pp. 24-41). potential view toward gaining a permanent seat on the United Nations Security Council (UNSC); and the strategic Introduction need for securing resource assets with special emphasis on energy resources and key metals for its industrial Japan has been grappling with defining its Africa economy.1 strategy. Historically, Japanese engagement with Since 2000, Japan’s strategy toward Africa has begun Africa has emphasised aid and development rather to shift. Whereas previously the relationship was than focused pragmatic commercial interest. Japan’s characterised by a donor-recipient model to a more engagement in Africa is seen as benign due in large part commercially-orientated approach, encouraging to its non-involvement in the continent’s colonial history. development through private investment, and However, Japan’s engagement of Africa is undergoing a incorporating a greater focus on business aligned shift due in large part by the increased prominence of the to the interests of Japan Inc. But as Africa itself is African continent and rising competition from emerging rapidly changing, so too much the foreign policy and actors who this century are rapidly accumulating both commercial strategy of Japan toward the continent. geopolitical and geo-economic capital on the continent. -

NIKON REPORT 2018 Unleashing the Limitless Possibilities of Light

NIKON REPORT 2018 Year Ended March 31, 2018 Unlock the future with the power of light Unleashing the limitless possibilities of light. Striving to brighten the human experience. Focused, with purpose, on a better future for all. THIS IS THE ESSENCE OF NIKON. Creation of New Value by Unlocking the Future with the Power of Light Throughout a century since its founding, Nikon has continued to win customer trust by contributing to the development of society with products and solutions based on its core opto-electronics and precision technologies. The technologies, the human resources, and the brand cultivated through this process have become reliable strengths supporting Nikon today. After completing the restructuring that began in November 2016, it will be crucial to further hone these strengths and fulfill our role as the “new eyes for people and industry” in order to create new value and support our growth strategies. Our vision formulated in 2017 will guide us in fostering corporate culture in which each employee is encouraged to think about what is necessary in order to accomplish growth and to tackle the challenges this introspection reveals. With this culture, everyone at Nikon will unite in our quest to consistently create corporate value. Nikon Report 2018 puts a spotlight on the value we have provided thus far and the strengths cultivated over the years. Moreover, the report seeks to communicate the basis for the growth strategies to be implemented after the completion of the restructuring and the tasks that will need to be addressed in order to effectively implement those strategies. -

2018 年度-3/31/19 現在)

寄付ご支援を頂いた企業・団体・個人の方々は下記の通りです。 (2018 年度-3/31/19 現在) $20,000 and up_____________ Mizuho Bank, Ltd. JX Nippon Oil & Energy (Americas) Inc. MUFG Union Bank, N. A. Kaneka America Holding, Inc. SMBC Kawasaki Heavy Industries (U.S.A.), Inc. KBK Inc. $10,000 and up (under $20,000) Kowa American Corp. Kuraray America, Inc. ITOCHU International Inc. Kyocera Document Solutions America, Inc. Marubeni America Corporation Kyocera International Inc. Mitsubishi Corporation (Americas) Kyowa Hakko USA, Inc. Mitsui & Co. (U. S. A.), Inc. Mayer Brown, LLP Nomura America Foundation Mitsubishi Gas Chemical America, Inc. Sumitomo Corporation of Americas Foundation Mitsubishi Imaging (MPM), Inc. Mitsubishi UFJ Trust & Banking Corp. , NY Branch Mitsui Chemicals America, Inc. $5,000 and up (under $10,000) Mitsui Seiki (U.S.A.), Inc. Mitsui Sumitomo Marine Management (U.S.A.), Inc. J. C. C. Fund Miyoshi America, Inc. Nippon Express Foundation, Inc. Mizuho Securities USA Inc. Panasonic Corp. of North America Nikkei America, Inc. Nikko Asset Management Americas, Inc. $1,000 and up (under $5,000) Nikon Americas Inc. Nippon Life Insurance Company Alice Corporation Nippon Steel & Sumitomo Metal U. S. A., Inc. All Nippon Airways Co., Ltd. NOF America Corporation Asahi Kasei America, Inc. The Norinchukin Bank, Ltd. Asset Management One USA Inc. NTT America, Inc. Canon U. S. A., Inc. NYK Line (North America), Inc. Casio America, Inc. ORIX Corporation USA Chugai Pharma U.S.A. Inc. Osaka Gas USA Corporation Citizen Watch Company of America, Inc Relo Redac, Inc. Dainobu, USA Inc. Sapporo USA, Inc. Daiwa Capital Markets America, Inc. SCSK USA Inc. DLI North America Inc. -

Boeing's Partnership with Japan—A Unique Market That's Home to Important Customers, As Well As Expertise in Industry—Is Evolving and Strengthening

Feature Story BOEING FRONTIERS Toward a common benefit Boeing's partnership with Japan—a unique market that's home to important customers, as well as expertise in industry—is evolving and strengthening. Yet one element remains the same: The critical role of personal relationships BY MIK E WI eg AND PHOTO S B Y BO B FE R G U S ON /BO E IN G ike many relationships, the Boeing-Japan relationship had humble beginnings, starting in 1953 with the establishment of Boeing International Corp. Boeing hoped to gain a foothold Lin a promising new market against entrenched competition. The new operation was funded with $1,000 and staffed by five U.S.-based directors. Yet this initial formal presence in Japan was the beginning of a profound partnership and friendship for both the company and Japan. In the past five decades, Boeing and Japan have made aerospace history together—and are setting the pace for defining the future of the industry. “Japan has worked with Boeing over the decades on both commercial and defense pro- grams,” said Hirofumi Katase, former director of the aerospace and defense industry division, manufacturing industries bureau at Japan’s Ministry of Economy, Trade and Industry. “Today, Japanese aerospace industry is jointly developing the 787 Dreamliner and Boeing is offering support to Japan’s Mitsubishi Regional Jet program. We have worked together on many defense programs such as Chinook and Tanker.” Japan’s aviation requirements are unique. As a small island nation with dense population cen- ters and high air-traffic demand, Japanese airlines have the highest flight cycles on some of the densest routes in the industry. -

February 5, 2020 ITOCHU Corporation

February 5, 2020 This document is an English translation of a statement written originally in Japanese. The Japanese original should be considered as the primary version. ITOCHU Corporation (Code No. 8001, Tokyo Stock Exchange, First Section) Representative Director and President and Chief Operating Officer: Yoshihisa Suzuki Contact: Suguru Amano General Manager, Investor Relations Department (TEL. +81-3-3497-7295) Changes in Assignment of Members of the Board ITOCHU Corporation has resolved the following changes at its Board of Directors’ meeting held on February 5, 2020. 1. Reason for Change Due to further strengthen our management structure. 2. Change in Assignment of Members of the Board <As of April 1, 2020> <Current> Yoshihisa Suzuki Member of the Board Member of the Board President & Chief Operating Officer; President & Chief Operating Officer Chief Digital & Information Officer <Attached> Changes in Members of the Board and Executive Officers 1 February 5, 2020 ITOCHU Corporation Changes in Members of the Board and Executive Officers 1. Retiring of Executive Officers 3 persons (As of March 31, 2020) Name As of April 1, 2020 Current Shunsuke Noda Advisory Member Managing Executive Officer Yoshihiro Fukushima Advisory Member Executive Officer Shoji Miura Advisory Member Executive Officer 2. Newly Appointed Executive Officers 2 persons (As of April 1, 2020) Name Current Executive Officer Director, EVP, Dole Asia Holdings Pte. Ltd. Masazumi Nishikage Executive Officer General Manager, Planning & Administration Department, Tadayoshi Yamaguchi ICT & Financial Business Company; CP & CITIC Business Development Department 2 3. Reappointment, Promotion(5 persons), and Changes in Assignment(9 persons) of Executive Officers *Promoted Executive Officer Of the 36 current Executive Officers, all 33 Executive Officers excluding the 3 retiring Executive Officers (See "1. -

Download (42Kb)

Information Society Trends Issue number: 59 - (1.10.96 - 31.10.96) EDITORIAL Europe Union joins world-wide cyberschool drive Promoting new information society tools in the school environment is an issue that has gained significant momentum in the world's richest countries in the last year. This trend comes in recognition of both the contribution of multimedia to the learning process and of the need to prepare the next generation for the information society. Government-led initiatives and pilot projects to put schools on-line have been launched in North America, Japan and Europe at national, regional and local level. A few striking examples include the US Administration's plan to provide free Internet access for all US schools and libraries by the year 2000, Japan's plans to install 900,000 network-equipped PCs in schools by the year 2000, Germany's three-year "Schools on the network" project, Denmark's plan to put all schools on-line by the year 2000 and Finland's "Education, training and research in the information society" strategy. Industry often supports government initiatives through public-private partnerships, for instance in the framework of the UK's "Superhighway in education" plan or the US National Education Technology Funding Corporation, and sometimes launches its own initiatives, such as the $370 million worth US Technology Learning Challenge. Discrepancies are important at global level: in 1995, one third of all US schools were connected to the Internet compared to only 5% in Japan and in the European Union (EU). They also exist within the EU with school connection rates ranging from two-third in Scandinavia to 15% in the UK, 2% in France and Germany and less in Southern Europe. -

ITOCHU Corporation Sustainability Report 2016

Our Initiatives for the Environment As a general trading company, ITOCHU provides various products and services and invests in businesses inside and outside of Japan, and positions global environmental problems as one of the top priority issues in management. In order to contribute to the realization of a sustainable society, ITOCHU is promoting environmental conservation activities. Environmental Activities Policies ITOCHU Corporation positions global warming and other environmental problems as one of the top priority issues in its management policy. In addition, to fulfill our corporate philosophy “Committed to the Global Good,” we have established the ITOCHU Group Environmental Policy. Now, we advance our corporate management and activities on a global scale under this policy, not only to contribute to the prosperity of the present generation, but also from the view point of what we can create to pass on to the next generation, while keeping a strong awareness of global environmental problems. The ITOCHU Group Environmental Policy I . Basic Philosophy Global warming and other environmental issues are affecting the future of mankind. As a global enterprise, ITOCHU Group is positioning these issues as one of the most important management policies. ITOCHU Group contributes to the realization of a sustainable society by promoting “Actively addressing the better global environment” based on The ITOCHU Group Corporate Code of Conduct, in order to achieve the goals of The ITOCHU Group Corporate Philosophy, “Committed to the Global Good”. II . Activity Guidelines In keeping with the basic philosophy presented above, ITOCHU Group pursues a continual improvement of its environmental management system and defines the following guidelines concerning activities of environmental conservation.