BROWN & CONNERY, LLP 360 Haddon Avenue PO Box 539

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ethical and Other Recent Developments in Financial Regulation and Litigation

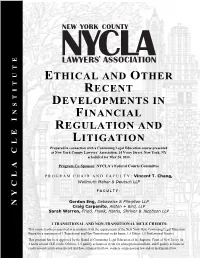

ETHICAL AND OTHER RECENT DEVELOPMENTS IN NSTITUTE FINANCIAL I REGULATION AND LITIGATION Prepared in connection with a Continuing Legal Education course presented CLE at New York County Lawyers’ Association, 14 Vesey Street, New York, NY scheduled for May 24, 2011. Program Co-Sponsor: NYCLA’s Federal Courts Committee PROGRAM CHAIR AND FACULTY: Vincent T. Chang, Wollmuth Maher & Deutsch LLP FACULTY: Gordon Eng, Debevoise & Plimpton LLP NYCLA Craig Carpenito, Alston + Bird, LLP Sarah Warren, Fried, Frank, Harris, Shriver & Jacobson LLP 3 TRANSITIONAL AND NON-TRANSITIONAL MCLE CREDITS: This course has been approved in accordance with the requirements of the New York State Continuing Legal Education Board for a maximum of 3 Transitional and Non-Transitional credit hours; 1.5 Ethics; 1.5 Professional Practice This program has been approved by the Board of Continuing Legal Education of the Supreme Court of New Jersey for 3 hours of total CLE credit. Of these, 1.5 qualify as hours of credit for ethics/professionalism, and 0 qualify as hours of credit toward certification in civil trial law, criminal trial law, workers compensation law and/or matrimonial law. Information Regarding CLE Credits and Certification Ethical and Other Recent Developments in Financial Litigation May 24, 2011, 6:00PM to 9:00PM The New York State CLE Board Regulations require all accredited CLE providers to provide documentation that CLE course attendees are, in fact, present during the course. Please review the following NYCLA rules for MCLE credit allocation and certificate distribution. i. You must sign-in and note the time of arrival to receive your course materials and receive MCLE credit. -

Law School Record, Vol. 48, No. 1 (Fall 2001) Law School Record Editors

University of Chicago Law School Chicago Unbound The nivU ersity of Chicago Law School Record Law School Publications Fall 9-1-2001 Law School Record, vol. 48, no. 1 (Fall 2001) Law School Record Editors Follow this and additional works at: http://chicagounbound.uchicago.edu/lawschoolrecord Recommended Citation Law School Record Editors, "Law School Record, vol. 48, no. 1 (Fall 2001)" (2001). The University of Chicago Law School Record. Book 85. http://chicagounbound.uchicago.edu/lawschoolrecord/85 This Book is brought to you for free and open access by the Law School Publications at Chicago Unbound. It has been accepted for inclusion in The University of Chicago Law School Record by an authorized administrator of Chicago Unbound. For more information, please contact [email protected]. THE U N V E R S T Y 0 F R E c o R D Fall 2001 The University of Chicago Law School Saul Levmore Dean and William B. Graham Professor of Law Jonathan S. Stern Associate Dean for External Affairs Editors Deborah Franczek, '71 2 Kyle Holtan Kathy Schichtel Senior Writer Gerald de Jaager Contributing Writers and Editors Richard Badger, '68; Douglas Baird; Ellen Cosgrove, '91; Nichole Crist; Roberta Dempsey; Diane Downs; Richard Epstein; Marsha Ferziger, '95; Kay Kersch Kirkpatrick; Abner Mikva, '51; Martha Nussbaum; Peter Schuler Class Correspondents Affable Alumni 38 6 Design and Production VisuaLingo Fran Gregory Chief Photographer Michelle Litvin Supporting Photographers Cheri Eisenberg Bruce Powell Publisher The University of Chicago Law School Office of External Affairs ibc 1111 East 60th Street Chicago, Illinois 60637 Telephone: 773-702-9486 Facsimile: 773-702-0356 Email: [email protected] Web site: www.law.uchicago.edu The University of Chicago Law School Record (lSSN 0529-097X) is published for alumni, faculty, and friends of the Law School. -

History of the U.S. Attorneys

Bicentennial Celebration of the United States Attorneys 1789 - 1989 "The United States Attorney is the representative not of an ordinary party to a controversy, but of a sovereignty whose obligation to govern impartially is as compelling as its obligation to govern at all; and whose interest, therefore, in a criminal prosecution is not that it shall win a case, but that justice shall be done. As such, he is in a peculiar and very definite sense the servant of the law, the twofold aim of which is that guilt shall not escape or innocence suffer. He may prosecute with earnestness and vigor– indeed, he should do so. But, while he may strike hard blows, he is not at liberty to strike foul ones. It is as much his duty to refrain from improper methods calculated to produce a wrongful conviction as it is to use every legitimate means to bring about a just one." QUOTED FROM STATEMENT OF MR. JUSTICE SUTHERLAND, BERGER V. UNITED STATES, 295 U. S. 88 (1935) Note: The information in this document was compiled from historical records maintained by the Offices of the United States Attorneys and by the Department of Justice. Every effort has been made to prepare accurate information. In some instances, this document mentions officials without the “United States Attorney” title, who nevertheless served under federal appointment to enforce the laws of the United States in federal territories prior to statehood and the creation of a federal judicial district. INTRODUCTION In this, the Bicentennial Year of the United States Constitution, the people of America find cause to celebrate the principles formulated at the inception of the nation Alexis de Tocqueville called, “The Great Experiment.” The experiment has worked, and the survival of the Constitution is proof of that. -

The Company They Keep: How Partisan

The Company They Keep: How Partisan Divisions Came to the Supreme Court Neal Devins, College of William and Mary Lawrence Baum, Ohio State University Table of Contents Chapter 1: Summary of Book and Argument 1 Chapter 2: The Supreme Court and Elites 21 Chapter 3: Elites, Ideology, and the Rise of the Modern Court 100 Chapter 4: The Court in a Polarized World 170 Chapter 5: Conclusions 240 Chapter 1 Summary of Book and Argument On September 12, 2005, Chief Justice nominee John Roberts told the Senate Judiciary Committee that “[n]obody ever went to a ball game to see the umpire. I will 1 remember that it’s my job to call balls and strikes and not to pitch or bat.” Notwithstanding Robert’s paean to judicial neutrality, then Senator Barack Obama voted against the Republican nominee. Although noting that Roberts was “absolutely . qualified,” Obama said that what mattered was the “5 percent of hard cases,” cases resolved not by adherence to legal rules but decided by “core concerns, one’s broader perspectives of how the world works, and the depth and breadth of one’s empathy.”2 But with all 55 Republicans backing Roberts, Democratic objections did not matter. Today, the dance between Roberts and Senate Democrats and Republicans seems so predictable that it now seems a given that there will be proclamations of neutrality by Supreme Court nominees and party line voting by Senators. Indeed, Senate Republicans blocked a vote on Obama Supreme Court pick Merrick Garland in 2016 so that (in the words of Senate majority leader Mitch McConnell) “the American people . -

Nunc Pro Tunc

THE UNITED STATES Fall 2016 DISTRICT COURT FOR THE DISTRICT OF NEW JERSE Y HISTORICAL SOCIETY NUNC PRO TUNC Inside this Issue: Honoring Our Chiefs Chief Judge Simandle Receives the AFBNJ’s 2016 Brennan Award Portrait Unveiling: The Hon. Garrett E. Brown, Jr. An Exhibit: The Addonizio Trial Trenton Courthouse Jury Room Dedication: The Hon. Anne E. Thompson Remembering: Edgar Y. Dobbins Hon. Jerome B. Simandle Hon. Garrett E. Brown, Jr. The D.N.J.’s First Chief Probation Officer By Wilfredo Torres Celebrating: The 225th Anniversary of the D.N.J. U.S. Attorney’s Office By Mikie Sherrill, Esq. Remembering: Selma, Alabama and the Voting Rights Act of 1965 By Andrea Lewis-Walker 2015 Clarkson S. Fisher Hon. John W. Bissell Hon. Anne E. Thompson Award-Winning Essay: “Taste Tells” ____________________________________________________ By Gregory Mortensen, Esq. Recently our Court’s current and three previous Chief Judges have been honored in various ways for their extraordinary On Behalf of The Historical Society: service to the people of New Jersey — including, for two of Patrick J. Murphy III, Esq. them, having played critical roles as assistant federal prosecutors Editor in a watershed conviction with national impact and historic import. Herein, the Historical Society showcases those honors. NUNC PRO TUNC Page 2 Chief Judge Jerome B. Simandle Receives the AFBNJ’s 2016 Brennan Award On the evening of June 16, 2016, the As- sociation of the Federal Bar of New Jersey be- stowed the William J. Brennan, Jr. Award, its highest honor, upon New Jersey’s two top ju- rists: D.N.J. -

Divided Dreamworlds? the Cultural Cold War in East and West Isbn 978 90 8964 436 7

STUDIES OF THE NETHERLANDS INSTITUTE FOR WAR DOCUMENTATION DIVIDED DREAMWORLDS? STUDIES OF THE DIVIDED NETHERLANDS With its unique focus on how culture Peter Romijn is INSTITUTE DREAMWORLDS? contributed to the blurring of ideological head of the Research FOR WAR boundaries between the East and the West, Department at the Netherlands Institute this volume offers fascinating insights into the DOCUMENTATION THE CULTURAL COLD WAR for War Documentation tensions, rivalries and occasional cooperation (NIOD) and professor IN EAST AND WEST between the two blocs. Encompassing of history at Amsterdam developments across the arts and sciences, University. the authors analyse focal points, aesthetic Giles Scott-Smith is preferences and cultural phenomena through Ernst van der Beugel topics as wide-ranging as East and West Chair in Transatlantic German interior design; the Soviet stance on Diplomatic History at genetics; US cultural diplomacy during and Leiden University and senior researcher at the after the Cold War; and the role of popular Roosevelt Study Center music as a universal cultural ambassador. in Middelburg. Joes Segal is assistant Well positioned at the cutting edge of Cold professor in the War studies, this work illuminates some of the Department of History striking paradoxes involved in the production and Art History at and reception of culture in East and West. Utrecht University. Eds. P. Romijn, G. Scott-Smith andJ.Segal Romijn,G.Scott-Smith Eds. P. ISBN 978 90 8964 436 7 Edited by Peter Romijn Giles Scott-Smith 9 789089 644367 Joes Segal www.aup.nl Divided Dreamworlds? niod-dreamworlds-def.indd 1 21-6-2012 15:04:53 studies of the netherlands institute for war documentation board of editors: Madelon de Keizer Conny Kristel Peter Romijn i Ralf Futselaar — Lard, Lice and Longevity. -

OLC) and Brett Kavanaugh, January 20, 2001, to May 30, 2006

Description of document: Correspondence between the Office of Legal Counsel (OLC) and Brett Kavanaugh, January 20, 2001, to May 30, 2006 Requested date: 16-July-2018 Release 01 date: 03-August-2018 Release 02 date: 17-August-2018 Release 03 date: 31-August-2018 Release 04 date: 14-September-2018 Release 05 date: 17-September-2018 Posted date: 01-April-2019 Note: Records released 03-Aug-2018 begin on PDF page 12 Records released 17-Aug-2018 begin on PDF page 243 Records released 31-Aug-2018 begin on PDF page 435 Records released 14-Sep-2018 begin on PDF page 631 Records released 17-Sep-2018 begin on PDF page 725 Source of document: FOIA Request Office of Legal Counsel Room 5511, 950 Pennsylvania Avenue, NW Department of Justice Washington, DC 20530-0001 Email: [email protected] The governmentattic.org web site (“the site”) is noncommercial and free to the public. The site and materials made available on the site, such as this file, are for reference only. The governmentattic.org web site and its principals have made every effort to make this information as complete and as accurate as possible, however, there may be mistakes and omissions, both typographical and in content. The governmentattic.org web site and its principals shall have neither liability nor responsibility to any person or entity with respect to any loss or damage caused, or alleged to have been caused, directly or indirectly, by the information provided on the governmentattic.org web site or in this file. The public records published on the site were obtained from government agencies using proper legal channels. -

Spring 2013 Vol XV Iss. 1

THE UNITED STATES Spring 2013 DISTRICT COURT FOR THE DISTRICT OF NEW JERSEY Volume XV, Issue 1 HISTORICAL SOCIETY NUNCNUNC PROPRO TUNCTUNC Historical Society’s Inside this Issue: Tribute To New Jersey’s Law Schools By: Keith J. Miller, Esq. Tribute to New Jersey’s On April 18, 2013, the Historical Society conducted a Tribute at the New Law Schools 1 Jersey Law Center recognizing and honoring the history and traditions of New Jersey's three law schools - Rutgers School of Law - Newark, Rutgers School of The Alabama’s 4 Law - Camden, and Seton Hall Law School. The Tribute, which was co- Bell Tolled sponsored by the New Jersey State Bar Association, featured audiovisual presentations on behalf of all three law schools followed by a networking Fisher Award 7 cocktail reception. The Tribute was well-attended by the Historical Society's Winner members and Judicial Advisors, by faculty, students and alumni from the law schools, and by members of the judiciary and legal community. Honoring 8 Barbara Morris The Tribute began with welcoming remarks from Historical Society President Leda Dunn Wettre, followed by introductory remarks from Tribute Chair Keith J. Miller. The keynote speech was given by Chief United States District Court Judge Jerome Simandle, who praised the contributions that all three law schools have made to the legal community in general and to the District of New Jersey in particular. Chief Judge Simandle noted that all three law schools have worked closely with the District Court for many years to facilitate the administration of justice, including participating in numerous programs and providing judicial interns and law clerks for the Judges of the District. -

Why Judges Resign: Influences on Federal Judicial Service, 1789 to 1992

If you have issues viewing or accessing this file contact us at NCJRS.gov. Why Judges Resign: Influences on Federal Judicial Service, 1789 to 1992 146891 U.S. Department of Justice Natlonallnsmute of Justice This document has been reproduced exactly as received from the person or organization originating it. Points of view or opinions stated in this document are those of the autllors and do not necessarily represent the oHicia1 position or policies of the Natlona11nstitute of Justice, Permission to reproduce this • r t 1 material has been gm.nletl.l:'U.Dl.J.C b.v • DomaJ.n, Federal JudJ.cJ.al Center to the National Criminal J~stlce Reference Service (NCJRS). Further reproduction outside of the NCJRS system requires permission of the~owner. :ral Judicial History Office !ral Judicial Center Why Judges Resign: Influences on Federal Judicial Service, 1789 to 1992 By Emily Field Van Tassel With Beverly Hudson Wirtz and Peter Wonders Federal Judicial History Office Federal Judicial Center 1993 Prepared for the National Commission on Judicial Discipline and Removal. Thb Federal Judicial Center publication was undertaken in furtherance of the Cen ter's statutory mission to conduct and stimulate research and development for the improvement of judicial administration. The views expressed are those of the author and not necessarily those of the Federal Judicial Center. Table of Contents 1. Introduction I 2. Overview 5 The Growth of the Federal Judiciary 5 Changes in Judicial Tenure 7 Judicial Resignations as a Percentage of the Total Judiciary: Change Over Time 7 \'V'hy ] udges Resign 10 Age and/or health (including disability and pre-I9I9 retirement) 10 Appointment to other office/elected office 10 Dissatisfaction II Return to private practice, other employment, imdeq uate salary 12- Allegations of misbehavior (including impeachments and convictions) 17 3. -

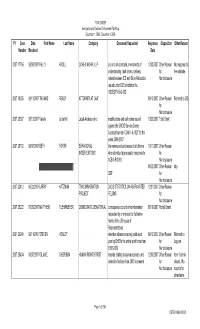

FY Case Number Date Received First Name Last Name Company

FOIA 09-0593 Immigration and Customs Enforcement FOIA Log December 1, 2006 - December 1, 2008 FY Case Date First Name Last Name Company Document Requested Response Disposition Other Reason Number Received Date 2007 17796 09/06/2007 KELLY KROLL COHEN MOHR, LLP any and all contracts, memoranda of 12/03/2007 Other Reason No response to understanding, task orders, delivery for fee estimate orders between ICE and Sirva Relocation Nondisclosure issued under ICE solicitation No. HSCEOP-05-Q-002 2007 18255 09/11/2007 THOMAS READY ATTORNEY AT LAW 09/12/2007 Other Reason Referred to CIS for Nondisclosure 2007 20397 09/13/2007 Valerie Underhill Labat-Anderson Inc. modifications and call orders issued 10/23/2007 Total Grant against the USCIS Service Center Contract Number COW-1-A-1027 for the years 2006-2007 2007 20702 09/07/2007 BETH FORTH BEHAVIORAL the names and addresses of all offerors 10/11/2007 Other Reason INTERVENTIONS who submitted a proposal in response to for ACB-3-R-0033 Nondisclosure (b)(6) 08/22/2007 Other Reason cbp CBP for Nondisclosure 2007 22412 06/22/2007 LARRY KATZMAN TRAC IMMIGRATION DACS STATISTICS ON AGGRAVATED 12/31/2007 Other Reason PROJECT FELONS for Nondisclosure 2007 25222 07/26/2007 MATTHEW FUEHRMEYER DEMOCRATIC SENATORIAL correspondence and other information 08/10/2007 Partial Grant requested by or provided to Katherine Harris of the US house of Representatives 2007 25240 09/11/2007 STEVEN HEALEY retention allowance money paid each 09/12/2007 Other Reason Referred to year by DHS for its entire work force from for Laguna 1998-2003 Nondisclosure 2007 25434 09/07/2007 GILIANE CHERUBIN HUMAN RIGHTS FIRST records relating to asylum seekers and 12/03/2007 Other Reason Item 1 admin detention facilities from 2000 to present for closed. -

2008 Christopher J. Christie US Attorney

United States Department of Justice United States Attorney’s Office District of New Jersey Office Report 2002 - 2008 Christopher J. Christie U.S. Attorney Significant Cases ______________________________________________________________________________ “ Introduction........................................................................................................................i ______________________________________________________________________________ “ 2002 ______________________________________________________________________________ Marty Barnes, Mayor of Paterson - Extortion.....................................................................2 The Daniel Pearl Case -Terrorism...................................................................................... 2 Roger Duronio - Computer “Logic Bomb”.........................................................................2 Forbes and Shelton - Cendant Corp....................................................................................3 Calderon et al. - Human Trafficking...................................................................................4 The Perez Organization - Camden Drugs and Gangs.........................................................4 Greater Newark Safer Cities Initiative Roundup................................................................5 Sara Bost - Irvington Mayor...............................................................................................6 Shipping Company and Captain - Ocean Dumping...........................................................6