Alternative Instruments for Open Market and Discount Window Operations

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Understanding Open Market Operations

Foreword The Federal Reserve Bank of New York is responsible for Michael Akbar Akhtar, vice president of the day-to-day implementation of the nation’s monetary pol- Federal Reserve Bank of New York, leads the reader— icy. It is primarily through open market operations—pur- whether a student, market professional or an interested chases or sales of U.S. Government securities in the member of the public—through various facets of mone- open market in order to add or drain reserves from the tary policy decision-making, and offers a general per- banking system—that the Federal Reserve influences spective on the transmission of policy effects throughout money and financial market conditions that, in turn, the economy. affect output, jobs and prices. Understanding Open Market Operations pro- This edition of Understanding Open Market vides a nontechnical review of how monetary policy is Operations seeks to explain the challenges in formulat- formulated and executed. Ideally, it will stimulate read- ing and implementing U.S. monetary policy in today’s ers to learn more about the subject as well as enhance highly competitive financial environment. The book high- appreciation of the challenges and uncertainties con- lights the broad and complex set of considerations that fronting monetary policymakers. are involved in daily decisions for open market opera- William J. McDonough tions and details the steps taken to implement policy. President Understanding Open Market Operations / i Acknowledgment Much has changed in U.S. financial markets and institu- Partlan for extensive comments on drafts; and to all of tions since 1985, when the last edition of Open Market the Desk staff for graciously and patiently answering my Operations, written by Paul Meek, was published. -

Payment System Disruptions and the Federal Reserve Followint

Working Paper Series This paper can be downloaded without charge from: http://www.richmondfed.org/publications/ Payment System Disruptions and the Federal Reserve Following September 11, 2001† Jeffrey M. Lacker* Federal Reserve Bank of Richmond, Richmond, Virginia, 23219, USA December 23, 2003 Federal Reserve Bank of Richmond Working Paper 03-16 Abstract The monetary and payment system consequences of the September 11, 2001, terrorist attacks are reviewed and compared to selected U.S. banking crises. Interbank payment disruptions appear to be the central feature of all the crises reviewed. For some the initial trigger is a credit shock, while for others the initial shock is technological and operational, as in September 11, but for both types the payments system effects are similar. For various reasons, interbank payment disruptions appear likely to recur. Federal Reserve credit extension following September 11 succeeded in massively increasing the supply of banks’ balances to satisfy the disruption-induced increase in demand and thereby ameliorate the effects of the shock. Relatively benign banking conditions helped make Fed credit policy manageable. An interbank payment disruption that coincided with less favorable banking conditions could be more difficult to manage, given current daylight credit policies. Keywords: central bank, Federal Reserve, monetary policy, discount window, payment system, September 11, banking crises, daylight credit. † Prepared for the Carnegie-Rochester Conference on Public Policy, November 21-22, 2003. Exceptional research assistance was provided by Hoossam Malek, Christian Pascasio, and Jeff Kelley. I have benefited from helpful conversations with Marvin Goodfriend, who suggested this topic, David Duttenhofer, Spence Hilton, Sandy Krieger, Helen Mucciolo, John Partlan, Larry Sweet, and Jack Walton, and helpful comments from Stacy Coleman, Connie Horsley, and Brian Madigan. -

Money Supply ECON 40364: Monetary Theory & Policy

Money Supply ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 59 Readings I Mishkin Ch. 3 I Mishkin Ch. 14 I Mishkin Ch. 15, pg. 341-348 2 / 59 Money I Money is defined as anything that is accepted as payments for goods or services or in the repayment of debts I Money serves three functions: 1. Medium of exchange 2. Unit of account 3. Store of value I Any asset can serve as a store of value (e.g. house, land, stocks, bonds), but most assets do not perform the first two roles of money I Money is a stock concept { how much money you have (in your wallet, in the bank) at a given point in time. Income is a flow concept 3 / 59 Roles of Money I Medium of exchange role is the most important role of money: I Eliminates need for barter, reduces transactions costs associated with exchange, and allows for greater specialization I Unit of account is important (particularly in a diverse economy), though anything could serve as a unit of account I As a store of value, money tends to be crummy relative to other assets like stocks and houses, which offer some expected return over time I An advantage money has as a store of value is its liquidity I Liquidity refers to ease with which an asset can be converted into a medium of exchange (i.e. money) I Money is the most liquid asset because it is the medium of exchange I If you held all your wealth in housing, and you wanted to buy a car, you would have to sell (liquidate) the house, which may not be easy to do, may take a while, and may involve selling at a discount if you must do it quickly 4 / 59 Evolution of Money and Payments I Commodity money: money made up of precious metals or other commodities I Difficult to carry around, potentially difficult to divide, price may fluctuate if precious metal or commodity has consumption value independent of medium of exchange role I Paper currency: pieces of paper that are accepted as medium of exchange. -

Overcoming the Zero Bound with Negative Interest Rate Policy

OVERCOMING THE ZERO BOUND WITH NEGATIVE INTEREST RATE POLICY Marvin Goodfriend Carnegie Mellon University, Tepper School “Removing the Zero Lower Bound on Interest Rates” An Imperial College Business School, Brevan Howard Centre for Financial Analysis, CEPR, and Swiss National Bank Event London, 18 May 2015 1 Overcoming the Zero Bound with Negative Interest Rate Policy • Urgency of the problem • Evolution of monetary policy • Why the zero bound constraint matters • Mechanics of negative nominal interest rate policy • Elevated inflation target not the answer • Conclusion 2 Urgency of the Problem • Irving Fisher’s (1930, 1986) The Theory of Interest pointed out that if a commodity could be stored costlessly over time, then the rate of interest in units of that commodity could never fall below zero • A central bank that pays zero interest on reserves puts a lower bound on the nominal interbank rate of interest • The power of open market operations to lower short-term real interest rates to fight deflation or recession then is limited when nominal rates are already low on average—as is the case when inflation and the inflation premium are stabilized at a 2% inflation target 3 Urgency of the Problem (2) • Quantitative monetary policy appears to have been effective in averting deflation and stimulating demand with near zero interest rates in the US and the UK • But Japan did not exit the zero bound or deflation for two decades even with the help of quantitative policy • The US, the UK, and the Euro area have not yet exited near zero interest -

Investment Insights

CHIEF INVESTMENT OFFICE Investment Insights AUGUST 2017 Matthew Diczok A Focus on the Fed Head of Fixed Income Strategy An Overview of the Federal Reserve System and a Look at Potential Personnel Changes SUMMARY After years of accommodative policy, the Federal Reserve (Fed) is on its path to policy normalization. The Fed forecasts another rate hike in late 2017, and three hikes in each of the next two years. The Fed also plans to taper reinvestments of Treasurys and mortgage-backed securities, gradually reducing its balance sheet. The market thinks differently. Emboldened by inflation persistently below target, it expects the Fed to move significantly more slowly, with only one to three rate hikes between now and early 2019. One way or another, this discrepancy will be reconciled, with important implications for asset prices and yields. Against this backdrop, changes in personnel at the Fed are very important, and have been underappreciated by markets. The Fed has three open board seats, and the Chair and Vice Chair are both up for reappointment in 2018. If the administration appoints a Fed Chair and Vice Chair who are not currently governors, then there will be five new, permanent voting members who determine rate moves—almost half of the 12-member committee. This would be unprecedented in the modern era. Similar to its potential influence on the Supreme Court, this administration has the ability to set the tone of monetary policy for many years into the future. Most rumored candidates share philosophical leanings at odds with the current board; they are generally hawkish relative to current policy, favor rules-based decision-making over discretionary, and are unconvinced that successive rounds of quantitative easing were beneficial. -

How the World Achieved Partial Consensus on Monetary Policy1

How the World Achieved Partial Consensus on Monetary Policy1 James Bullard President and CEO, Federal Reserve Bank of St. Louis Shadow Open Market Committee Meeting Current Monetary Policy: The Influence of Marvin Goodfriend New York, N.Y. March 6, 2020 In 2007, Marvin Goodfriend published a paper titled “How the World Achieved Consensus on Monetary Policy” in the Journal of Economic Perspectives. It is an excellent summary of the sequence of economic ideas influencing and eventually dominating actual monetary policy from Lucas (1972) up to the eve of the global financial crisis. Goodfriend’s explanations and summaries are so lucid, and his examples and thinking so familiar to me that in rereading the article I had the sensation that my life was flashing before my eyes. In the article, Goodfriend builds up the key idea in central banking of the last 50 years—namely, successful monetary policy requires a credible commitment on the part of the central bank to careful, systematic future policy choices. At the end of the article, he allows for some unfinished business and some open issues, among them the question of why credible central banks may end up with inflation that is too low when compared to an intended target. In retrospect, the “World Consensus” article appears a bit triumphal and somewhat premature. The events since its publication seem to suggest that the consensus that appeared to exist at that moment has its own problems. As we meet here today, many central banks have consistently missed their stated inflation targets to the low side for many years. -

Open Market Operations and Money Supply at Zero Nominal Interest Rates

Open Market Operations and Money Supply at Zero Nominal Interest Rates Roberto Robatto∗ University of Chicago October 21, 2012 (first draft: February 2012) Abstract What are the paths of money supply that are consistent with zero nominal interest rates and that can be implemented through open market operations? To answer this question, I present an Irrelevance Proposition for some open market operations that exchange money and one-period bonds at the zero lower bound. The result has implications for the conduct of monetary policy (non-irrelevant open market operations modify the equilibrium) and for the implementation of the Friedman rule (any growth rate of money supply above the negative of the rate of time preferences can implement zero nominal interest rate forever, even a positive growth rate, provided that the government collects \large enough" surpluses). The result holds under several specifications, including models with heterogeneity, non- separable utility, borrowing constraints, incomplete and segmented markets and sticky prices; and generalizes to any situation in which the cost of holding money vs. bonds is zero, such as the payment of interest on money. ∗Email: [email protected]. I am extremely greatful to Fernando Alvarez for his suggestions and guidance. I would like to thank also John Cochrane, Thorsten Drautzburg, Tom Sargent, Harald Uhlig and participants to the AMT, Capital Theory and Economic Dynamics Working Groups at the University of Chicago for their comments. 1 1 Introduction At zero nominal interest rates, money is perfect substitutes for bonds from the point of view of the private sector. Money demand is thus not uniquely determined, therefore the equilibrium in the money market depends on the supply of money. -

Effect of Open Market Operations (OMO) on Economic Development, 1986 -2016

International Journal of Economics and Financial Management Vol. 3 No. 2 2018 ISSN: 2545 - 5966 www.iiardpub.org Effect of Open Market Operations (OMO) on Economic Development, 1986 -2016. Richard Osadume (Ph.D, FCIB) Nigeria Maritime University, Warri, Nigeria [email protected] [email protected] Abstract This Study examined the Effect of Open Market Operations (OMO) on Economic Development (1986-2016). The objective of this study was to examine the Effect of – Treasury Bills rates and Treasury Certificates rates on economic development. The study employed secondary data and used Nigeria as its sample; the investigation employed the OLS, Co-integration, Granger- causality and ECM Analytical techniques, to test the impact of the independent variables (treasury bill rates and treasury certificate rates) on the dependent variable, economic development (proxied by Human Development index) and tested at the 5% level of significance. The findings showed that Open Market Operations captured by Treasury Bills and treasury certificates, both had no significant effect on economic development in the short-run but showed a positive and significant effect in the long-run period on economic development with significant speed of adjustments. The study concludes that Central Bank Open Market Operations represented by Treasury Bills and Treasury Certificates do exert significant effect in the long-run on economic development and recommends amongst others the creation of adequate product awareness by the monetary authorities to raise public patronage of these financial products and also, to allow enough operational time lag to enable relevant formulated policies achieve their desired objectives. Key Word: Treasury Bills; Treasury Certificate Rates; Human Development index; Economic development; Open Market Operations. -

Perspectives on Monetary and Credit Policy

Perspectives on Monetary and Credit Policy November 20, 2012 Jeffrey M. Lacker President Federal Reserve Bank of Richmond Shadow Open Market Committee Symposium New York, N.Y. The Federal Open Market Committee in January formally announced a numerical objective for inflation, a step which has long been argued to be essential to anchoring longer-term expectations about the conduct of monetary policy.1 So it might seem a bit surprising, as this year draws to a close, to find a member of the Committee speaking at an event whose title is “The Fed’s Monetary Policy Adrift.” But on further reflection, I don’t think it should be surprising at all. Both the FOMC’s articulation of an inflation target and the sense that policy is adrift are related, I believe, to the extraordinary circumstances and resulting policy actions of the last few years. In my remarks this morning, I will discuss two dimensions of Federal Reserve policy that came in the wake of the financial crisis and Great Recession: first, the effort to provide stimulus and policy guidance at the zero bound; and second, the expansion of the scope of Fed policy beyond monetary policy to a broader engagement in credit policy. Before I begin, however, I need to recite a disclaimer that should be quite familiar to members of the Shadow Open Market Committee — my remarks reflect my own views and not necessarily those of any 2 other members of the FOMC. Maintaining Credibility Let me begin by noting that when the FOMC announced an explicit numerical objective for inflation this year, we had experienced an extended period of relative monetary stability. -

Interest on Reserves and Monetary Policy

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Research Papers in Economics Marvin Goodfriend Interest on Reserves and Monetary Policy I. Introduction the world’s major central banks implement monetary policy by manipulating short-term interest rates. Yet important onetary policy operating procedures have long been differences remain in the procedures by which short-term rates M debated within the Federal Reserve and among are managed. There is considerable interest in comparing monetary economists at large. For instance, economists have alternatives currently in use and in exploring new procedures disagreed about whether a central bank should utilize bank that might afford benefits in the future.3 reserves or the interest rate as the policy instrument. For the Motivated by these four developments, this paper highlights time being at least, the Fed has settled on an interest rate policy the role of interest on reserves in understanding the leverage instrument and has announced its current federal funds rate that central banks exert over interest rates and explores the target since 1994. The focus on interest rate policy is reflected potential for interest on reserves to improve the in the ubiquitous use of the Taylor rule in monetary policy implementation of monetary policy. I find that interest on analysis. reserves can and should be employed as a policy instrument Oddly enough, just as the longstanding debate over bank equal in importance with open market operations. In effect, my reserves and the federal funds rate was set aside, four paper resolves the historical dispute over bank reserves and developments combined to renew an interest in operating interest rate operating procedures by pointing out how a procedures. -

Managing the Fragility of the Eurozone

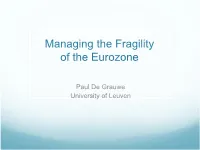

Managing the Fragility of the Eurozone Paul De Grauwe University of Leuven Paradox Gross government debt (% of GDP) 100 90 UK 80 Spain 70 60 50 40 30 20 10 0 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 10-Year-Government Bond Yields UK-Spain 6 5.5 SPAIN 5 4.5 4 percent 3.5 UK 3 2.5 2 Nature of monetary union Members of monetary union issue debt in currency over which they have no control. It follows that: Financial markets acquire power to force default on these countries Not so in countries that are not part of monetary union, and have kept control over the currency in which they issue debt. Consider case of UK and Spain UK Case Suppose investors fear default of UK government They sell UK govt bonds (yields increase) Proceeds of sales are presented in forex market Sterling drops UK money stock remains unchanged maintaining pool of liquidity that will be reinvested in UK govt securities If not Bank of England can be forced to buy UK govt bonds Investors cannot trigger liquidity crisis for UK government and thus cannot force default (Bank of England is superior force) Investors know this: thus they will not try to force default. Spanish case Suppose investors fear default of Spanish government They sell Spanish govt bonds (yields increase) Proceeds of these sales are used to invest in other eurozone assets No foreign exchange market and floating exchange rate to stop this Spanish money stock declines; pool of liquidity for investing in Spanish govt bonds shrinks No Spanish central bank that can be forced to buy Spanish government bonds Liquidity crisis possible: Spanish government cannot fund bond issues at reasonable interest rate Can be forced to default Investors know this and will be tempted to try Situation of Spain is reminiscent of situation of emerging economies that have to borrow in a foreign currency. -

Monetary Policy, Transparency, and Credibility

Monetary Policy, Transparency, and Credibility Federal Reserve Bank of San Francisco, Fourth Floor March 23 - 24, 2007 AGENDA Friday, March 23 Morning Session Chair: John Williams, Federal Reserve Bank of San Francisco 8:10 A.M. Continental Breakfast 8:50 A.M. Welcoming Remarks: Janet Yellen, Federal Reserve Bank of San Francisco 9:00 A.M. Alex Cukierman, Tel-Aviv University The Limits of Transparency Discussants: Petra Geraats, University of Cambridge Hyun Song Shin, Princeton University 10:30 A.M. Break 11:00 A.M. Marvin Goodfriend, Carnegie-Mellon University Bennett McCallum, Carnegie-Mellon University Banking and Interest Rates in Monetary Policy Analysis: A Quantitative Exploration Discussants: Stephen Cecchetti, Brandeis University Huw Pill, European Central Bank 12:30 P.M. Lunch – Market Street Dining Room, Fourth Floor Afternoon Session Chair: Richard Dennis, Federal Reserve Bank of San Francisco 2:00 P.M. Romain Baeriswyl, Ludwig-Maximilians Universität & Credit Suisse Camille Cornand, BETA – Université Louis Pasteur Monetary Policy and its Informative Value Discussants: George-Marios Angeletos, Massachusetts Institute of Technology Christian Hellwig, University of California, Los Angeles 3:30 P.M. Break 4:00 P.M. Michael Bordo, Rutgers University Christopher Erceg, Andrew Levin, Federal Reserve Board Ryan Michaels, University of Michigan Three Great American Disinflations Discussants: Gauti Eggertsson, Federal Reserve Bank of New York John Taylor, Stanford University 5:30 P.M. Reception – West Market Street Lounge, Fourth Floor 6:30 P.M. Dinner – Market Street Dining Room, Fourth Floor Introduction: Janet Yellen, Federal Reserve Bank of San Francisco Speaker: Frederic Mishkin, Federal Reserve Board Saturday, March 4 Morning Session Chair: Glenn Rudebusch, Federal Reserve Bank of San Francisco 8:00 A.M.