Notes on Foreign Currency Adjustments

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

1935 Time Capsule Part 3

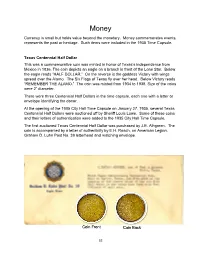

Money Currency is small but holds value beyond the monetary. Money commemorates events, represents the past or heritage. Such items were included in the 1935 Time Capsule. Texas Centennial Half Dollar This was a commemorative coin was minted in honor of Texas’s independence from Mexico in 1836. The coin depicts an eagle on a branch in front of the Lone Star. Below the eagle reads “HALF DOLLAR.” On the reverse is the goddess Victory with wings spread over the Alamo. The Six Flags of Texas fly over her head. Below Victory reads “REMEMBER THE ALAMO.” The coin was minted from 1934 to 1938. Size of the coins were 2” diameter. There were three Centennial Half Dollars in the time capsule, each one with a letter or envelope identifying the donor. At the opening of the 1905 City Hall Time Capsule on January 27, 1935, several Texas Centennial Half Dollars were auctioned off by Sheriff Louis Lowe. Some of these coins and their letters of authentication were added to the 1935 City Hall Time Capsule. The first auctioned Texas Centennial Half Dollar was purchased by J.E. Alhgreen. The coin is accompanied by a letter of authenticity by E.H. Roach, on American Legion, Graham D. Luhn Post No. 39 letterhead and matching envelope. Coin Front Coin Back 32 Letter Front 33 Letter Back 34 The second Texas Centennial Half Dollar was purchased at the same auction by E.E. Rummel. Shown below are the paperwork establishing the authenticity of the purchase by E.H. Roach, on American Legion, Graham D. -

This PDF Is a Selection from an Out-Of-Print Volume from the National Bureau of Economic Research

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: The International Gold Standard Reinterpreted, 1914-1934 Volume Author/Editor: William Adams Brown, Jr. Volume Publisher: NBER Volume ISBN: 0-87014-036-1 Volume URL: http://www.nber.org/books/brow40-1 Publication Date: 1940 Chapter Title: Book III, Part V: The Impact of the World Economic Depression on the International Gold Standard, 1929-1931 Chapter Author: William Adams Brown, Jr. Chapter URL: http://www.nber.org/chapters/c5947 Chapter pages in book: (p. 808 - 1047) PART V The Impact of the World Economic Depression on the International Gold Standard, 1929-1931 S CHAPTER 22 The International Distribution of Credit under the Impact of World-wide Deflationary Forces For about twelve months after the critical decisions of June 1927 the international effects of generally easy money were among the most fundamental causes of a world-wide upswing in business.1 Though prices in gold standard countries were falling gradually, increasing productivity would probably have forced them much lower had it not been for the ex- pansion of credit. There was an upward pressure in many price groups. Profits from security and real estate speculation stimulated demand for many commodities. Low interest rates made it easy to finance valorization schemes and price arrangements and promoted the issue of foreign loans, par.. ticularly in the United States. Foreign loans in turn helped to maintain prices in many debtor countries and also pre- vented the growth of tariffs from checking the expansion of international trade.2 The continued extension of interna- tional credit was a dam that was holding back the onrushing torrent of economic readjustment. -

Christopher Kent: the Resources Boom and the Australian Dollar

Christopher Kent: The resources boom and the Australian dollar Address by Mr Christopher Kent, Assistant Governor (Economic) of the Reserve Bank of Australia, to the Committee for Economic Development of Australia (CEDA) Economic and Political Overview, Sydney, 14 February 2014. * * * I thank Jonathan Hambur, Daniel Rees and Michelle Wright for assistance in preparing these remarks. I would like to thank CEDA for the invitation to speak here today. I thought I would take the opportunity to talk to you about the implications of the resources boom for the Australian dollar. The past decade saw the Australian dollar appreciate by around 50 per cent in trade- weighted terms (Graph 1).1 The appreciation was an important means by which the economy was able to adjust to the historic increase in commodity prices and the unprecedented investment boom in the resources sector.2 Even though there was a significant increase in incomes and domestic demand over a number of years, average inflation over the past decade has remained within the target. Also, growth has generally not been too far from trend. This is all the more significant in light of the substantial swings in the macroeconomy that were all too common during earlier commodity booms.3 The high nominal exchange rate helped to facilitate the reallocation of labour and capital across industries. While this has made conditions difficult in some industries, the appreciation, in combination with a relatively flexible labour market and low and stable inflation expectations, meant that high demand for labour in the resources sector did not spill over to a broad-based increase in wage inflation.4 So the high level of the exchange rate was helpful for the economy as a whole. -

Elimination of the One Cent Coin the Bahamian One Cent Coin Or the “Penny” Is Being Phased

Central Bank of The Bahamas FAQS: Elimination of the One Cent Coin The Bahamian one cent coin or the “penny” is being phased out of circulation. After the end of 2020 it will no longer be legal tender in The Bahamas. It is further proposed that circulation of or acceptance of US pennies will cease at the same time as the Bahamian coin. Why is the one cent coin or penny being phased out? Rising cost of production relative to face value Increased accumulation and non-use of pennies The significant handling cost of pennies When will the Central Bank stop distributing the penny? The Central Bank will stop distributing pennies to commercial banks on the 31st January 2020. Financial institutions will no longer be providing new supplies of the coins to consumers and businesses. Are businesses required to accept pennies after the end of January 2020? NO. Businesses may decide to stop accepting pennies anytime after the end of January 2020. Can businesses continue to accept pennies after the end of December 2020? NO. Businesses will not be able to accept payment or give change in one cent pieces after the end of December 2020. All cash payments will to be rounded to the nearest five cents. How will cash amounts be rounded? Business must round the total amount due to the nearest five cents If your total bill is $9.42 or $9.41. The nearest five cents to either of these would be $9.40 If your total bill is $9.43 or $9.44, the nearest five cents to either of these would be $9.45. -

A History of the Canadian Dollar 53 Royal Bank of Canada, $5, 1943 in 1944, Banks Were Prohibited from Issuing Their Own Notes

Canada under Fixed Exchange Rates and Exchange Controls (1939-50) Bank of Canada, $2, 1937 The 1937 issue differed considerably in design from its 1935 counterpart. The portrait of King George VI appeared in the centre of all but two denominations. The colour of the $2 note in this issue was changed to terra cotta from blue to avoid confusion with the green $1 notes. This was the Bank’s first issue to include French and English text on the same note. The war years (1939-45) and foreign exchange reserves. The Board was responsible to the minister of finance, and its Exchange controls were introduced in chairman was the Governor of the Bank of Canada through an Order-in-Council passed on Canada. Day-to-day operations of the FECB were 15 September 1939 and took effect the following carried out mainly by Bank of Canada staff. day, under the authority of the War Measures Act.70 The Foreign Exchange Control Order established a The Foreign Exchange Control Order legal framework for the control of foreign authorized the FECB to fix, subject to ministerial exchange transactions, and the Foreign Exchange approval, the exchange rate of the Canadian dollar Control Board (FECB) began operations on vis-à-vis the U.S. dollar and the pound sterling. 16 September.71 The Exchange Fund Account was Accordingly, the FECB fixed the Canadian-dollar activated at the same time to hold Canada’s gold value of the U.S. dollar at Can$1.10 (US$0.9091) 70. Parliament did not, in fact, have an opportunity to vote on exchange controls until after the war. -

![September 30, 1949 Letter, Syngman Rhee to Dr. Robert T. Oliver [Soviet Translation]](https://docslib.b-cdn.net/cover/6467/september-30-1949-letter-syngman-rhee-to-dr-robert-t-oliver-soviet-translation-696467.webp)

September 30, 1949 Letter, Syngman Rhee to Dr. Robert T. Oliver [Soviet Translation]

Digital Archive digitalarchive.wilsoncenter.org International History Declassified September 30, 1949 Letter, Syngman Rhee to Dr. Robert T. Oliver [Soviet Translation] Citation: “Letter, Syngman Rhee to Dr. Robert T. Oliver [Soviet Translation],” September 30, 1949, History and Public Policy Program Digital Archive, CWIHP Archive. Translated by Gary Goldberg. https://digitalarchive.wilsoncenter.org/document/119385 Summary: Letter from Syngman Rhee translated into Russian. The original was likely found when the Communists seized Seoul. Syngman Rhee urges Oliver to come to South Korea to help develop the nation independent of foreign invaders and restore order to his country. Credits: This document was made possible with support from the Leon Levy Foundation. Original Language: Russian Contents: English Translation Scan of Original Document continuation of CABLE Nº 600081/sh “30 September 1949 to: DR. ROBERT T. OLIVER from: PRESIDENT SYNGMAN RHEE I have received your letters and thank you for them. I do not intend to qualify Mr. KROCK [sic] as a lobbyist or anything of that sort. Please, in strict confidence get in contact with Mr. K. [SIC] and with Mr. MEADE [sic] and find out everything that is necessary. If you think it would be inadvisable to use Mr. K with respect to what Mr. K told you, we can leave this matter without consequences. In my last letter I asked you to inquire more about K. in the National Press Club. We simply cannot use someone who does not have a good business reputation. Please be very careful in this matter. There is some criticism about the work which we are doing. -

University Archives Inventory

University Archives Inventory Record Group Number: UR001.03 Title: Burney Lynch Parkinson Presidential Records Date: 1926-1969 Bulk Date: 1932-1952 Extent: 42 boxes Creator: Burney Lynch Parkinson Administrative/Biographical Notes: Burney Lynch Parkinson (1887-1972) was an educator from Lincoln, Tennessee. He received his B.S. from Erskine College in 1909, and rose up the administrative ranks from English teacher in Laurens, South Carolina public schools. He received his M.A. from Peabody College in 1920, and Ph.D. from Peabody in 1926, after which he became president of Presbyterian College in Clinton, SC in 1927. He was employed as Director of Teacher Training, Certification, and Elementary Education at the Alabama Dept. of Education just before coming to MSCW to become president in 1932. In December 1932, the university was re-accredited by the Southern Association of Colleges and Schools, ending the crisis brought on the purge of faculty under Governor Theodore Bilbo, but appropriations to the university were cut by 54 percent, and faculty and staff were reduced by 33 percent, as enrollment had declined from 1410 in 1929 to 804 in 1932. Parkinson authorized a study of MSCW by Peabody college, ultimately pursuing its recommendations to focus on liberal arts at the cost of its traditional role in industrial, vocational, and technical education. Building projects were kept to a minimum during the Parkinson years. Old Main was restored and named for Mary Calloway in 1938. Franklin Hall was converted to a dorm, and the Whitfield Gymnasium into a student center with the Golden Goose Tearoom inside. Parkinson Hall was constructed in 1951 and named for Dr. -

E Euro Symbol Was Created by the European Commission

e eu ro c o i n s 1 unity an d d i v e r s i t The euro, our currency y A symbol for the European currency e euro symbol was created by the European Commission. e design had to satisfy three simple criteria: ADF and BCDE • to be a highly recognisable symbol of Europe, intersect at D • to have a visual link with existing well-known currency symbols, and • to be aesthetically pleasing and easy to write by hand. Some thirty drafts were drawn up internally. Of these, ten were put to the test of approval by the BCDE, DH and IJ general public. Two designs emerged from the are parallel scale survey well ahead of the rest. It was from these two BCDE intersects that the President of the Commission at the time, at C Jacques Santer, and the European Commissioner with responsibility for the euro, Yves-ibault de Silguy, Euro symbol: geometric construction made their final choice. Jacques Santer and Yves-ibault de Silguy e final choice, the symbol €, was inspired by the letter epsilon, harking back to classical times and the cradle of European civilisation. e symbol also refers to the first letter of the word “Europe”. e two parallel lines indicate the stability of the euro, as they do in the symbol of the dollar and the yen. e official abbreviation for the euro is EUR. © European Communities, 2008 e eu ro c o i n s 2 unity an d d i v e r s i t The euro, our currency y Two sides of a coin – designing the European side e euro coins are produced by the euro area countries themselves, unlike the banknotes which are printed by the ECB. -

The Drs. Joanne and Edward Dauer Collection of World Banknotes

DALLAS | THE DRS. JOANNE JOANNE DRS. THE DAUER AND EDWARD COLLECTION OF BANKNOTESWORLD WORLD PAPER MONEY PAPER WORLD APRIL 24, 2020 WORLD PAPER MONEY AUCTION #4020 | THE DRS. JOANNE AND EDWARD DAUER COLLECTION OF WORLD BANKNOTES | APRIL 24, 2020 | DALLAS Front Cover Lots: 26088, 26115, 26193, 26006, 26051 Inside Front Cover Lots: 26066, 26075, 26190, 26177, 26068 Inside Back Cover Lots: 26143, 26162, 26083, 26148, 26125 Back Cover Lots: 26191, 26129, 26185, 26181, 26108 Heritage Signature® Auction #4020 World Paper Money The Drs. Joanne and Edward Dauer Collection of World Banknotes April 24, 2020 | Dallas FLOOR Signature® Session PRELIMINARY LOT VIEWING (Floor, Telephone, HERITAGELive!®, Internet, Fax, and Mail) By appointment only. Contact Jose Berumen at 214-409-1299 Heritage Auctions, Dallas • 1st Floor Auction Room or [email protected] (All times subject to change) 3500 Maple Avenue • Dallas, TX 75219 Heritage Auctions, Dallas • 17th Floor 3500 Maple Avenue • Dallas, TX 75219 Session Friday, April 24 • 2:00 PM CT • Lots 26001–26197 Monday, April 6 – Friday, April 10 • 9:00 AM – 5:00 PM CT LOT VIEWING Heritage Auctions, Dallas • 17th Floor LOT SETTLEMENT AND PICK-UP 3500 Maple Avenue • Dallas, TX 75219 Available weekdays 9:00 AM – 5:00 PM CT starting Monday, April 27, by appointment only. Please contact Client Services Tuesday, April 21 • 12:00 PM – 5:00 PM CT at 866-835-3243 to schedule an appointment. Wednesday, April 22 – Friday, April 24 9:00 AM – 5:00 PM CT Lots are sold at an approximate rate of 125 lots per hour, but it is not uncommon to sell 100 lots or 175 lots in any given hour. -

Dollar Shortage and Oil Surplus in 1949-1950

ESSAYS IN INTERNATIONAL FINANCE No. II, November 1950 DOLLAR SHORTAGE AND OIL SURPLUS IN 1949-1950 HORST MENDERSHAUSEN INTERNATIONAL FINANCE SECTION - DEPARTMENT OF ECONOMICS AND SOCIAL INSTITUTIONS PRINCETON UNIVERSITY Princeton, New Jersey The present essay is the eleventh in the series ESSAYS IN INTERNATIONAL FINANCE published by the International Finance Section of the Department of Economics and Social Institutions in Princeton Uni- versity. The author, Dr. Horst Mendershausen, has been associated with the National Bureau of Economic Research, Bennington College, and the United States Military Government for Germany. He is now an economist with the Federal Reserve Bank of New York. Nothing in this study should be considered an expression of the views of that institution. While the Section sponsors the essays of this series, it takes no further responsibility for the opinions therein expressed. The writers are free to develop their topics as they will and their ideas may or may not be shared by the editorial committee of the Section or the members of the Department. • GARDNER PATTERSON, Director International Finance Section DOLLAR SHORTAGE AND OIL SURPLUS IN 1949-1950 BY HORST MENDERSHAUSEN* , I. SURVEY OF ISSUES ECOVERY from the effects of World War II led the Western European countries on to a broad issue: Should they seek eco- nomic viability in a progressive integration of the non-Soviet world or in narrower frameworks implying some discrimination against United States commerce? Since their dollar needs showed a persistent tendency to exceed dollar availabilities during the recovery period and their dollar reserves proved either too small or too volatile, many coun- tries, in particular Britain, found it necessary to make preparations for the latter alternative. -

The Story of Israel As Told by Banknotes

M NEY talks The Story of Israel as told by Banknotes Educational Resource FOR ISRAEL EDUCATION Developed, compiled and written by: Vavi Toran Edited by: Rachel Dorsey Money Talks was created by Jewish LearningWorks in partnership with The iCenter for Israel Education This educational resource draws from many sources that were compiled and edited for the sole use of educators, for educational purposes only. FOR ISRAEL EDUCATION Introduction National Identity in Your Wallet “There is always a story in any national banknote. Printed on a white sheet of paper, there is a tale expressed by images and text, that makes the difference between white paper and paper money.” Sebastián Guerrini, 2011 We handle money nearly every day. But how much do we really know about our banknotes? Which president is on the $50 bill? Which banknote showcases the White House? Which one includes the Statue of Liberty torch? Why were the symbols chosen? What stories do they tell? Banknotes can be examined and deciphered to understand Like other commemoration the history and politics of any nation. Having changed eight agents, such as street times between its establishment and 2017, Israel’s banknotes names or coins, banknotes offer an especially interesting opportunity to explore the have symbolic and political history of the Jewish state. significance. The messages 2017 marks the eighth time that the State of Israel changed the design of its means of payment. Israel is considered expressed on the notes are innovative in this regard, as opposed to other countries in inserted on a daily basis, in the world that maintain uniform design over many years. -

No. 541 BELGIUM, CANADA, DENMARK, FRANCE, ICELAND

No. 541 BELGIUM, CANADA, DENMARK, FRANCE, ICELAND, ITALY, LUXEMBOURG, NETHERLANDS, NORWAY, PORTUGAL, UNITED KINGDOM OF GREAT BRITAIN AND NORTHERN IRELAND and UNITED STATES OF AMERICA North Atlantic Treaty. Signed at Washington, on 4 April 1949 English and French official texts communicated by the Permanent Representa tive of the United States of America at the seat of the United Nations. The registration took place on 7 September 1949. BELGIQUE, CANADA, DANEMARK, FRANCE, ISLANDE, ITALIE, LUXEMBOURG, PAYS-BAS, NORVEGE, PORTUGAL, ROYAUME-UNI DE GRANDE-BRETAGNE ET D©IRLANDE DU NORD et ETATS-UNIS D©AMERIQUE Trait de l©Atlantique Nord. Sign Washington, le 4 avril 1949 Textes officiels anglais et français communiqués par le représentant permanent des Etats-Unis d'Amérique au siège de l'Organisation des Nations Unies. L'enregistrement a eu lieu le 7 septembre 1949. 244 United Nations — Treaty Series_________1949 No. 541. NORTH ATLANTIC TREATY1. SIGNED AT WASH INGTON, ON 4 APRIL 1949 The Parties to this Treaty reaffirm their faith in the purposes and principles of the Charter of the United Nations and their desire to live in peace with all peoples and all governments. They are determined to safeguard the freedom, common heritage and civilization of their peoples, founded on the principles of democracy, individual liberty and the rule of law. They seek to promote stability and well-being in the North Atlantic area. They are resolved to unite their efforts for collective defense and for the preservation of peace and security. They therefore agree to this North Atlantic Treaty: Article 1 The Parties undertake, as set forth in the Charter of the United Nations, to settle any international disputes in which they may be involved by peaceful means in such a manner that international peace and security, and justice, are not endangered, and to refrain in their international relations from the threat or use of force in any manner inconsistent with the purposes of the United Nations.