Genesee Intermediate School District Flint, Michigan Audit Report for The

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

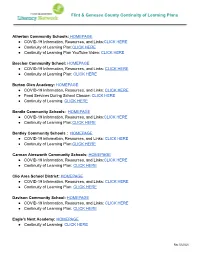

Flint & Genesee County Continuity of Learning Plans

Flint & Genesee County Continuity of Learning Plans Atherton Community Schools: HOMEP AGE ● COVID-19 Information, Resources, and Links:CLICK HERE ● Continuity of Learning Plan:CLICK HERE ● Continuity of Learning Plan YouTube Video: CLICK HERE Beecher Community School: HOMEPAGE ● COVID-19 Information, Resources, and Links: CLICK HERE ● Continuity of Learning Plan: CLICK HERE Burton Glen Academy: HOMEPAGE ● COVID-19 Information, Resources, and Links: CLICK HERE ● Food Services During School Closure: CLICK HERE ● Continuity of Learning: CLICK HERE Bendle Community Schools: HOMEPAGE ● COVID-19 Information, Resources, and Links:CLICK HERE ● Continuity of Learning Plan:CLICK HERE Bentley Community Schools : HOMEP AGE ● COVID-19 information, Resources, and Links: CLICK HERE ● Continuity of Learning Plan:CLICK HERE Carman Ainsworth Community Schools: HOMEPAGE ● COVID-19 Information, Resources, and Links:CLICK HERE ● Continuity of Learning Plan: CLICK HERE Clio Area School District: HOMEP AGE ● COVID-19 Information, Resources, and Links: CLICK HERE ● Continuity of Learning Plan: CLICK HERE Davison Community School: HOMEPAGE ● COVID-19 Information, Resources, and Links: CLICK HERE ● Continuity of Learning Plan: CLICK HERE Eagle's Nest Academy: HOMEPAGE ● Continuity of Learning: CLICK HERE Rev. 5/6/2020 / Flint & Genesee County Continuity of Learning Plans Fenton Community School: HOMEP AGE ● COVID-19 Information, Resources, and Links: CLICK HERE ● Continuity of Learning Plan: CLICK HERE Flex High Michigan: HOMEPAGE ● COVID-19- Information, Resources, -

Districtprintout HB 4411 Enacted.Xlsx

Estimated District Impacts of Major Components of Public Act 48 of 2021, House Bill 4411, for FY 2021-22 Estimated Total $ FY 2021-22 FY 2021-22 Value of Found. Eliminate One- Section 22d Special Ed Bilingual 94% ISD Section ISD Total Recommended Foundation Incr. Not Adj. for Time Funding Isolated and 50% Increase (Est. 56(7) New Operations Estimated County Code District Nam Foundation Increase Enroll. $66pp Sec. 11d Rural Increase* Based off FY 21) Funding 4% Increase Increase ALCONA COUNTY 01010 ALCONA COMMUNITY SCHOOLS $8,700 $589 $393,911 ($45,159) $0 $7,481 $0 $0 $356,233 ALGER COUNTY 02010 AUTRAIN-ONOTA PUBLIC SCHOOLS $8,700 $559 $18,749 ($2,261) $0 $268 $0 $0 $16,756 ALGER COUNTY 02020 BURT TOWNSHIP SCHOOL DISTRICT $10,598 $171 $5,109 ($1,967) $152,592 $55 $0 $0 $155,790 ALGER COUNTY 02070 MUNISING PUBLIC SCHOOLS $8,700 $589 $358,660 ($42,244) $0 $9,355 $0 $0 $325,771 ALGER COUNTY 02080 SUPERIOR CENTRAL SCHOOL DISTRICT $8,700 $589 $191,083 ($21,830) $0 $5,819 $0 $0 $175,073 ALLEGAN COUNTY 03000 ALLEGAN AREA EDUCATIONAL SERVICE AGENCY $0 $0 $0 $0 $0 $61,392 $0 $527,186 $28,058 $616,636 ALLEGAN COUNTY 03010 PLAINWELL COMMUNITY SCHOOLS $8,700 $589 $1,609,236 ($181,543) $0 $32,128 $3,938 $0 $1,463,759 ALLEGAN COUNTY 03020 OTSEGO PUBLIC SCHOOLS $8,700 $589 $1,340,004 ($153,260) $0 $30,814 $785 $0 $1,218,343 ALLEGAN COUNTY 03030 ALLEGAN PUBLIC SCHOOLS $8,700 $589 $1,335,781 ($150,773) $0 $37,292 $3,584 $0 $1,225,884 ALLEGAN COUNTY 03040 WAYLAND UNION SCHOOLS $8,700 $589 $1,739,753 ($197,834) $0 $31,269 $4,691 $0 $1,577,878 ALLEGAN COUNTY -

Student Mobility in Flint Community Schools

Student Mobility in the Flint Community School District By Troy Rosencrants Table of Contents Executive Summary ................................................................................................ i Introduction ............................................................................................................ 1 Data Analysis ......................................................................................................... 2 Data .............................................................................................................. 2 Student Counts ............................................................................................. 2 Student Mobility .......................................................................................... 3 Comparison of ACS data and student counts .............................................. 4 Discussion/Conclusions ......................................................................................... 8 References ............................................................................................................ 10 Appendices ........................................................................................................... 11 Executive Summary . Student mobility can be an issue in many urban areas where the population is predominantly minority and are low-income. Schools districts in Genesee County and, specifically, Flint Community Schools have declined in student population recently. During the period of declining student population -

COVID-19: Community Resources

1 Flex High Michigan Resource Guide for students and families in Genesee County Genesee County Meals To-Go for Students Affected by Covid-19 School Closures Flex High Michigan Resource Book for Genesee County 2 Flex High Michigan Resource Book for Genesee County 3 Food Distribution Sites Throughout Genesee County Special Note: Most school distribution sites are providing meals to all children up to age 18 (or up to age 26 if eligible for special education), regardless of the district they attend. So please feel free to go to the site that is most convenient to you if this is offered there! Because conditions are constantly changing, please check your district’s website and Facebook page often for updates. Genesee Intermediate School District Meal Distribution for Genesee ISD Programs To meet the needs of our students, Genesee Intermediate School District will be distributing meals beginning Monday, March 16 and continuing Mondays through Fridays at the locations and times shown below. Each student will receive two meals each day. Meals are available for all children free of charge. If you are unable to access one of the Genesee ISD meal distribution sites, please call (810) 591-4552. Beecher Dailey Elementary 6236 Neff Road, Mt. Morris 2:00–3:00 p.m. Cathedral of Faith 6031 Dupont St, Flint 12:00–12:45 p.m. Early Learning Center 5575 Van Campen Street, Flint 1:00–1:45 p.m. Educare Flint 1000 Gladwyn Street, Flint 12:00–12:45 p.m. Elmer Knopf Learning Center 1493 W. Maple Ave. Flint 10:30 a.m.–12:30 p.m. -

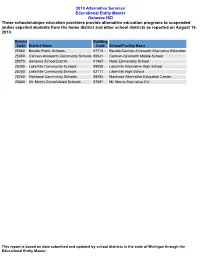

2010 Alternative Services Educational Entity Master Genesee ISD These

2010 Alternative Services Educational Entity Master Genesee ISD These schools/unique education providers provide alternative education programs to suspended and/or expelled students from the home district and other school districts as reported on August 16, 2010. District Building Code District Name Code School/Facility Name 25060 Bendle Public Schools 07710 Bendle/Carman-Ainsworth Alternative Education 25080 Carman-Ainsworth Community Schools 00031 Carman-Ainsworth Middle School 25070 Genesee School District 01867 Haas Elementary School 25280 LakeVille Community Schools 08058 LakeVille Alternative High School 25280 LakeVille Community Schools 02111 LakeVille High School 25260 Montrose Community Schools 09494 Montrose Alternative Education Center 25040 Mt. Morris Consolidated Schools 07691 Mt. Morris Alternative Ed. This report is based on data submitted and updated by school districts in the state of Michigan through the Educational Entity Master. 2010 Alternative Services Educational Entity Master Genesee ISD These schools/unique education providers provide alternative education programs to suspended and/or expelled students from the home district only as reported on August 16, 2010. District Building Code District Name Code School/Facility Name 25130 Atherton Community Schools 00138 Atherton High School 25130 Atherton Community Schools 00139 Atherton Middle School 25080 Carman-Ainsworth Community Schools 05009 Carman-Ainsworth High School 25080 Carman-Ainsworth Community Schools 09054 Stalker Community Education 25140 Davison Community -

Special Education Parent Handbook for Genesee County School Districts Published by the Genesee Intermediate School District

Special Education Parent Handbook for Genesee County School Districts Published by the Genesee Intermediate School District TABLE OF CONTENTS Introduction .................................................................................................................................................................. 5 Genesee Intermediate School District Board of Education ................................................................................... 5 Parent Advisory Committee ......................................................................................................................................... 7 Special Education Overview ........................................................................................................................................ 9 What is Special Education?....................................................................................................................................... 10 Why Does My Child Need an Evaluation?............................................................................................................. 10 What is the Evaluation Process? .......................................................................................................................... 10 How is a Child Evaluated for the Presence of a Disability? ................................................................................. 10 Who Makes the Decision if a Child is Eligible for Services? ................................................................................ 10 How Does -

GISD Special Education Mandatory Plan

Genesee Intermediate School District, Special Education Services Department acknowledges the work of the Steering Committee comprised of the following people: Parent Advisory Committee Brenda Edenburn .................................................... Kearsley Community Schools Ruth Randall .................................................... Swartz Creek Community Schools Donna Root .............................................................. Flushing Community Schools Local Educational Agency Representatives Sheila Cummings .............................................. Lake Fenton Community Schools Larry Simpson ............................................................... Flint Community Schools Cherie Snyder .............................................. Montrose Community School District Genesee Intermediate School District Jan Blanck, Principal ..................................... Early Childhood Programs/Services Kasey Cronin, Director .................................... Special Education Services Center Compliance and Special Services Administration Charles Richards, Teacher Consultant ........... Marion Crouse Instructional Center GENESEE INTERMEDIATE SCHOOL DISTRICT Special Education Mandatory Plan Table of Contents Content Areas: ..................................................................................................................................... 1 a) Advise and Inform Procedures ............................................................................................. 1 b) Activities and Outreach -

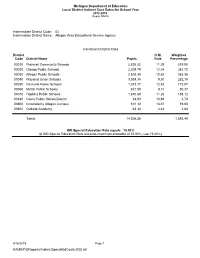

Constituent District Data District Code District Name Pupils O.M. Rate Weighted Percentage 03010 Plainwell Community Schools

Michigan Department of Education Local District Indirect Cost Rates for School Year 2018-2019 Report R0416 Intermediate District Code: 03 Intermediate District Name: Allegan Area Educational Service Agency Constituent District Data District O.M. Weighted Code District Name Pupils Rate Percentage 03010 Plainwell Community Schools 2,825.52 11.29 319.00 03020 Otsego Public Schools 2,309.79 12.24 282.72 03030 Allegan Public Schools 2,503.39 10.52 263.36 03040 Wayland Union Schools 3,034.34 9.30 282.19 03050 Fennville Public Schools 1,342.17 12.82 172.07 03060 Martin Public Schools 621.90 8.10 50.37 03070 Hopkins Public Schools 1,670.69 11.26 188.12 03440 Glenn Public School District 34.00 10.99 3.74 03900 Innocademy Allegan Campus 101.12 18.87 19.08 03902 Outlook Academy 63.34 4.48 2.84 Totals 14,506.26 1,583.49 ISD Special Education Rate equals 10.92% (If ISD Special Education Rate exceeds maximum allowable of 15.00%, use 15.00%) 4/16/2019 Page 1 SAMS/FIDReports/IndirectSpecialEdCosts(ISD).rdl Michigan Department of Education Local District Indirect Cost Rates for School Year 2018-2019 Report R0416 Intermediate District Code: 04 Intermediate District Name: Alpena-Montmorency-Alcona ESD Constituent District Data District O.M. Weighted Code District Name Pupils Rate Percentage 01010 Alcona Community Schools 714.26 9.95 71.07 04010 Alpena Public Schools 3,812.07 9.50 362.15 60010 Atlanta Community Schools 238.87 11.30 26.99 60020 Hillman Community Schools 438.11 13.07 57.26 Totals 5,203.31 517.47 ISD Special Education Rate equals 9.95% (If ISD Special Education Rate exceeds maximum allowable of 15.00%, use 15.00%) 4/16/2019 Page 2 SAMS/FIDReports/IndirectSpecialEdCosts(ISD).rdl Michigan Department of Education Local District Indirect Cost Rates for School Year 2018-2019 Report R0416 Intermediate District Code: 08 Intermediate District Name: Barry ISD Constituent District Data District O.M. -

MIBLSI Identified Partners

MIBLSI Identified Partners MIBLSI has defined partnerships with ISDs, Districts, and Schools to: • Implement an integrated reading and behavior MTSS model • Implement a multi-tiered behavioral framework • Implement practices to increase equity in disciplinary practices and behavioral support • Become a model demonstration site for adolescent reading success • Host MIBLSI Staff as employees of the organization A benefit of the above categories of partnership is priority registration and waived registration fees to select statewide events. Only the ISDs and Districts included on the list below can utilize priority registration and waived registration fees. Individuals who register from organizations not specifically listed below will either have their registration removed until the public window is open or be charged a registration fee. If a district’s ISD is listed as a partner but the district is not, then a fee will be assessed for any applicable trainings. Adrian, School District of the City of Carson City-Crystal Area Schools Akron-Fairgrove Schools Cass City Public Schools Alanson Public Schools Cassopolis Public Schools Alpena-Montmorency-Alcona ESD Cedarville School Atherton Community Schools Central Lake Public Schools Attwood School Central Montcalm Public Schools Baldwin Community Schools Charlevoix-Emmet ISD Baraga Area Schools Chippewa Hills School District Barry ISD Clinton County RESA Beecher Community School District Clio Area School District Bendle Public Schools Coopersville South Elementary School Bentley Community School -

School Districts

Flint River Watershed School Districts Vassar Snover P Kiingston Communiity Schooll Diist. l a Lanway Elmer Twp i Mayviilllle Communiity Schooll Diist. n e v Koylton Twp Dayton Twp o Fremont Twp r P r h G ayville e M i l e l n l Clifford i r p K Marlette Community Schools h Marlette Community Schools p o s s i T a James Twp i n l Mayville C S C r g Vassar Twp r M Tuscola Twp e g m Swan Creek Twp Spaulding Twp Bridgeport Twp Frankenmuth Twp n l s e s o a n o d t Fremont Twp d v i t t s n o E r t l h n a h ll u Mi o n u u i 2 h e r s C Swan Valley School District i l ette Swan Valley School District F i rl H f Ma e fo S Frankenmuth t rd r Marlette t r Marlette a y Marlette Twp c P Brown r Albertson A r P i e ClifR ford a a l D a Curtis g B Briidgeport-Spaulldiing Comm. S/D r i Sarles e l e r o ush y Ter B a Soper a d h K Markle T B e n u i Marlette Community Schools l S Marlette Community Schools n Swaffer c e e a e h o M d c e y s M G r l Mayville Community School Dist. h Mayville Community School Dist. t f ht c Haig o o o e r ennis a wnline I D To a n r C G t v W t p h y r e r s a t TUSCOLA e t Busch h e S g l g Marlette Community Schools l Marlette Community Schools ake i y L S a urph M r y Malone r T 10 q n a e a r St Charles u m Stove h le w p a M p p A Fry a 16 w h m Flynn Twp t L u a U S a t R H L n i n Sloan k l n v n a k e o a e a C a s Sloan l u n i l gton s Millin r r r o r a w e a n m loa Watertown Twp e S a on o Millingt w f r t Burlington Twp e e f SANILAC B o g l H s n B e o S Rathbun i P o l J e l i d McKillop n Millington -

Foundation Allowances

FY 2018-19 Foundation Allowances District Foundation Code County District Name Allowance 01010 Alcona Alcona Community Schools $7,871 02010 Alger Autrain-Onota Public Schools 7,905 02020 Alger Burt Township School District 10,307 02070 Alger Munising Public Schools 7,871 02080 Alger Superior Central School District 7,871 03010 Allegan Plainwell Community Schools 7,871 03020 Allegan Otsego Public Schools 7,871 03030 Allegan Allegan Public Schools 7,871 03040 Allegan Wayland Union Schools 7,871 03050 Allegan Fennville Public Schools 7,871 03060 Allegan Martin Public Schools 7,871 03070 Allegan Hopkins Public Schools 7,871 03080 Allegan Saugatuck Public Schools 8,460 03100 Allegan Hamilton Community Schools 7,871 03440 Allegan Glenn Public School District 8,359 03900 Allegan Innocademy Allegan Campus 7,871 03902 Allegan Outlook Academy 7,871 04010 Alpena Alpena Public Schools 7,871 05010 Antrim Alba Public Schools 7,871 05035 Antrim Central Lake Public Schools 8,178 05040 Antrim Bellaire Public Schools 8,128 05060 Antrim Elk Rapids Schools 7,871 05065 Antrim Ellsworth Community School 7,871 05070 Antrim Mancelona Public Schools 7,871 06010 Arenac Arenac Eastern School District 7,871 06020 Arenac Au Gres-Sims School District 7,871 06050 Arenac Standish-Sterling Community Schools 7,871 07010 Baraga Arvon Township School District 8,409 07020 Baraga Baraga Area Schools 7,871 07040 Baraga L'Anse Area Schools 7,871 08010 Barry Delton Kellogg Schools 7,871 08030 Barry Hastings Area School District 7,871 08050 Barry Thornapple Kellogg School District 7,871 09010 Bay Bay City School District 7,871 09030 Bay Bangor Township Schools 7,871 09050 Bay Essexville-Hampton Public Schools 7,957 09090 Bay Pinconning Area Schools 7,871 09901 Bay Bay-Arenac Community High School 7,871 09902 Bay State Street Academy 7,871 09903 Bay Bay City Academy 7,871 10015 Benzie Benzie County Central Schools 7,871 10025 Benzie Frankfort-Elberta Area Schools 8,331 11010 Berrien Benton Harbor Area Schools 7,871 11020 Berrien St. -

Annual Report 2015

Annual Report 2015 TABLE OF CONTENTS OUR MISSION 2 WHO WE ARE 3 PROGRAM AND SERVICES 4 MESSAGE FROM THE EXECUTIVE DIRECTOR 6 INTRODUCING OUR DEPUTY EXECUTIVE DIRECTOR 7 GCCARD ADVISORY COUNCIL 8 MESSAGE FROM BOARD CHAIRPERSON 9 PROGRAM HIGHLIGHTS 10 HELPING REAL PEOPLE 13 FINANCIAL REPORT 18 A SPECIAL THANK YOU 19 PARTNERS IN PROGRESS 20 An Open Door. A Helping Hand. OUR MISSION GCCARD’s purpose is to break the cycle of poverty by mobilizing and utilizing resources, public and private, in the Genesee County area. We strive to ensure all residents have access to safe, affordable housing, food and medical care. We are dedicated to eliminating poverty through developing employment opportunities and bettering the conditions under which all Genesee County residents live, learn and work. We also administer every program with the maximum feasible participation of residents served. 2 | P a g e An Open Door. A Helping Hand. WHO WE ARE enesee County Community Action Resource G Department (GCCARD) is one of the oldest and largest human service agencies in the county. With an annual operating budget of more than $18 million, GCCARD’s mission is to “help break the cycle of poverty.” GCCARD helps low-income individuals and families achieve higher levels of economic self-sufficiency and stability. We are committed to alleviating the causes and circumstances of poverty. Through the provision of client-centered services, staff members assist clients in realizing their fullest potential. GCCARD is the federally designated anti-poverty organization for Genesee County. We are a member of the national Community Action Partnership, which serves more than 1,000 Community Action Agencies across the United States, and the Michigan Community Action Agency.