FUTURE Plc: HERE's HOPING the PAST IS NOT NECESSARILY an INDICATION of THE…

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SEI Global Investments Fund Plc Unaudited Condensed Financial Statements for the Half Year Ended 31 December 2020

SEI GLOBAL INVESTMENTS FUND PLC Unaudited Condensed Financial Statements for the half year ended 31 December 2020 SEI Global Investments Fund plc Unaudited Condensed Financial Statements for the half year ended 31 December 2020 CONTENTS PAGE Directory 3 General Information 4 Investment Adviser’s Report The SEI Global Select Equity Fund 6 Portfolio of Investments The SEI Global Select Equity Fund 9 Condensed Income Statement 26 Condensed Statement of Financial Position 27 Condensed Statement of Changes in Net Assets Attributable to Redeemable Participating Shareholders 29 Notes to the Condensed Financial Statements 31 Appendix I – Remuneration Disclosures 40 Appendix II – Statement of Changes in Composition of Portfolio 41 Appendix III – Securities Financing Transactions Regulation 42 2 SEI Global Investments Fund plc Unaudited Condensed Financial Statements for the half year ended 31 December 2020 DIRECTORY Board of Directors at 31 December 2020 Michael Jackson (Chairman) (Irish) Kevin Barr (American) Robert A. Nesher (American) Desmond Murray* (Irish) Jeffrey Klauder (American) *Director, independent of the Investment Adviser Manager SEI Investments Global, Limited 2nd Floor Styne House Upper Hatch Street Dublin 2 Ireland Investment Adviser SEI Investments Management Corporation 1 Freedom Valley Drive Oaks, Pennsylvania 19456 U.S.A. Depositary Brown Brothers Harriman Trustee Services (Ireland) Limited 30 Herbert Street Dublin 2 Ireland Administrator SEI Investments – Global Fund Services Limited 2nd Floor Styne House Upper Hatch Street -

20Annual Report 2020 Equiniti Group

EQUINITI GROUP PLC 20ANNUAL REPORT 2020 PURPOSEFULLY DRIVEN | DIGITALLY FOCUSED | FINANCIAL FUTURES FOR ALL Equiniti (EQ) is an international provider of technology and solutions for complex and regulated data and payments, serving blue-chip enterprises and public sector organisations. Our purpose is to care for every customer and simplify each and every transaction. Skilled people and technology-enabled services provide continuity, growth and connectivity for businesses across the world. Designed for those who need them the most, our accessible services are for everyone. Our vision is to help businesses and individuals succeed, creating positive experiences for the millions of people who rely on us for a sustainable future. Our mission is for our people and platforms to connect businesses with markets, engage customers with their investments and allow organisations to grow and transform. 2 Contents Section 01 Strategic Report Headlines 6 COVID-19: Impact And Response 8 About Us 10 Our Business Model 12 Our Technology Platforms 14 Our Markets 16 Our Strategy 18 Our Key Performance Indicators 20 Chairman’s Statement 22 Chief Executive’s Statement 24 Operational Review 26 Financial Review 34 Alternative Performance Measures 40 Environmental, Social and Governance 42 Principal Risks and Uncertainties 51 Viability Statement 56 Section 02 Governance Report Corporate Governance Report 62 Board of Directors 64 Executive Committee 66 Board 68 Audit Committee Report 78 Risk Committee Report 88 Nomination Committee Report 95 Directors' Remuneration -

News, Information, Rumors, Opinions, Etc

http://www.physics.miami.edu/~chris/srchmrk_nws.html ● Miami-Dade/Broward/Palm Beach News ❍ Miami Herald Online Sun Sentinel Palm Beach Post ❍ Miami ABC, Ch 10 Miami NBC, Ch 6 ❍ Miami CBS, Ch 4 Miami Fox, WSVN Ch 7 ● Local Government, Schools, Universities, Culture ❍ Miami Dade County Government ❍ Village of Pinecrest ❍ Miami Dade County Public Schools ❍ ❍ University of Miami UM Arts & Sciences ❍ e-Veritas Univ of Miami Faculty and Staff "news" ❍ The Hurricane online University of Miami Student Newspaper ❍ Tropic Culture Miami ❍ Culture Shock Miami ● Local Traffic ❍ Traffic Conditions in Miami from SmartTraveler. ❍ Traffic Conditions in Florida from FHP. ❍ Traffic Conditions in Miami from MSN Autos. ❍ Yahoo Traffic for Miami. ❍ Road/Highway Construction in Florida from Florida DOT. ❍ WSVN's (Fox, local Channel 7) live Traffic conditions in Miami via RealPlayer. News, Information, Rumors, Opinions, Etc. ● Science News ❍ EurekAlert! ❍ New York Times Science/Health ❍ BBC Science/Technology ❍ Popular Science ❍ Space.com ❍ CNN Space ❍ ABC News Science/Technology ❍ CBS News Sci/Tech ❍ LA Times Science ❍ Scientific American ❍ Science News ❍ MIT Technology Review ❍ New Scientist ❍ Physorg.com ❍ PhysicsToday.org ❍ Sky and Telescope News ❍ ENN - Environmental News Network ● Technology/Computer News/Rumors/Opinions ❍ Google Tech/Sci News or Yahoo Tech News or Google Top Stories ❍ ArsTechnica Wired ❍ SlashDot Digg DoggDot.us ❍ reddit digglicious.com Technorati ❍ del.ic.ious furl.net ❍ New York Times Technology San Jose Mercury News Technology Washington -

Rns Over the Long Term and Critical to Enabling This Is Continued Investment in Our Technology and People, a Capital Allocation Priority

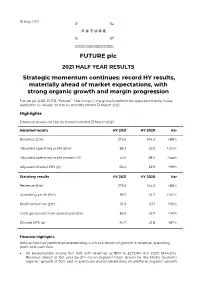

19 May 2021 FUTURE plc 2021 HALF YEAR RESULTS Strategic momentum continues: record HY results, materially ahead of market expectations, with strong organic growth and margin progression Future plc (LSE: FUTR, “Future”, “the Group”), the global platform for specialist media, today publishes its results for the six months ended 31 March 2021. Highlights Financial results for the six months ended 31 March 2021 Adjusted results HY 2021 HY 2020 Var Revenue (£m) 272.6 144.3 +89% Adjusted operating profit (£m)1 89.2 39.9 +124% Adjusted operating profit margin (%) 33% 28% +5ppt Adjusted diluted EPS (p) 65.4 32.9 +99% Statutory results HY 2021 HY 2020 Var Revenue (£m) 272.6 144.3 +89% Operating profit (£m) 59.7 24.7 +142% Profit before tax (£m) 56.9 27.1 +110% Cash generated from operations (£m) 85.9 35.7 +141% Diluted EPS (p) 40.7 21.8 +87% Financial highlights Robust first-half performance extending our track record of growth in revenue, operating profit and cash flow: An exceptionally strong first half, with revenue up 89% to £272.6m (HY 2020: £144.3m). Revenue ahead of last year by 21% on an organic2 basis, driven by the Media division’s organic2 growth of 30% and in particular digital advertising on-platform organic2 growth of 30% and eCommerce affiliates’ organic2 growth of 56%. US achieved revenue growth of 31% on an organic2 basis and UK revenues grew by 5% organically (UK has a higher mix of events and magazines revenues which were impacted more materially by the pandemic). -

GUEST LIST the Shard | 12 March A-B

GUEST LIST The Shard | 12 March A-B First Name Surname Company Name Russell Abbott Synergis Marketing April Adams-Redmond Kerry Foods Mahmood Ahmed HSBC Salim Ahmed GCS Group Rebeca Alamo Quant Marketing Charlotte Aldiss BBC Worldwide Jonathan Allan Channel 4 Television Chris Allin British Gas Tim Ambler London Business School Mark Antrobus GlaxoSmithKline Ian Armstrong Jaguar Cars Saj Arshad Vodafone Danielle Atkins Nokia Hugh Baillie Patsy Baker Bell Pottinger Group Joanna Baldwin Alistair Barr Barr Gazetas Jayne Barr Abellio Adrian Barragan Nokia Simon Bassett EMR Alex Batchelor BrainJuicer Group Katie Beard The Ultimate Experience Adam Beckett AVIVA Michael Bedingfield Royal Automobile Club John Bernard Firefox OS Mark Bernard Richard Bernholt Periproducts Joy Bhattacharya Accenture James Bidwell CASS ART Andy Bird Brand Learning John Birkbeck Capital One Viya Bishay Eurostar Group Mark Bleathman Unilever Vivian Blom TMF Group In association with With thanks to GUEST LIST The Shard | 12 March B-C First Name Surname Company Name Chris Bowry Eurostar Group Emma Bradley BBC Nick Bradley City & Guilds Colin Bradshaw Rapp Russell Braterman Vodafone Francesca Brosan Omobono Lorna Brown John Lewis Lucas Brown Total Media Group Pamela Brown British Gas Rob Bruce Whyte & Mackay Kevin Bryant E.ON UK Richard Burdett Horse & Country TV Matt Burgess Unilever Hugh Burkitt The Marketing Society Ivor Burns Camelot UK Lotteries Joanna Burton Crescent Communications Amanda Campbell Capital Shopping Centres David Campbell World Brands Limited Dominic -

The 2021 Guide to Manuscript Publishers

Publish Authors Emily Harstone Authors Publish The 2021 Guide to Manuscript Publishers 230 Traditional Publishers No Agent Required Emily Harstone This book is copyright 2021 Authors Publish Magazine. Do not distribute. Corrections, complaints, compliments, criticisms? Contact [email protected] More Books from Emily Harstone The Authors Publish Guide to Manuscript Submission Submit, Publish, Repeat: How to Publish Your Creative Writing in Literary Journals The Authors Publish Guide to Memoir Writing and Publishing The Authors Publish Guide to Children’s and Young Adult Publishing Courses & Workshops from Authors Publish Workshop: Manuscript Publishing for Novelists Workshop: Submit, Publish, Repeat The Novel Writing Workshop With Emily Harstone The Flash Fiction Workshop With Ella Peary Free Lectures from The Writers Workshop at Authors Publish The First Twenty Pages: How to Win Over Agents, Editors, and Readers in 20 Pages Taming the Wild Beast: Making Inspiration Work For You Writing from Dreams: Finding the Flashpoint for Compelling Poems and Stories Table of Contents Table of Contents .......................................................................................................... 5 Introduction ................................................................................................................. 13 Nonfiction Publishers.................................................................................................. 19 Arcade Publishing .................................................................................................. -

LINKS: Uu Nuclear Blast Video Clips · Nuclear Blast Bands on Tour · Nuclear Blast Albums in the Charts · New Songs on Spotify Uu

New Release Information uu May THE NIGHT FLIGHT ORCHESTRA Release Date Pre-Order Start Amber Galactic uu 19/05/2017 uu 07/04/2017 uu LIMITED CD DIGIPAK available incl. 1 bonus tracks uu 2-LP BLACK VINYL in Gatefold available incl. 1 bonus tracks uu advertising in many important music magazines APR/MAY 2017 uu album reviews, interviews in all important Metal magazines in Europe’s APR/MAY 2017 issues uu song placements in European magazine compilations uu spotify playlists in all European territories Price Code: CD03 uu retail marketing campaigns NB 4010-0 CD-Digi uu instore decoration: flyers, poster A1 (incl. bonus track) uu Facebook, YouTube, Twitter, Google+ organic promotion uu Facebook ads and promoted posts + Google ads in both the search and display networks, bing ads and gmail ads (tbc) uu Banner advertising on more than 60 most important Metal & Rock websites all over Europe uu additional booked ads on Metal Hammer Germany and UK, and in Price Code: LP17 the Fixion network (mainly Blabbermouth) NB 4010-1 2LP (black in gatefold) uu video and pre-roll ads on You tube uu ad campaigns on iPhones for iTunes and Google Play for Androids uu banners, featured items at the shop, header images and a back- ground on nuclearblast.de and nuclearblast.com uu features and banners in newsletters, as well as special mailings to targeted audiences in support of the release Territory: World uu The band had recently released the first single off the album, ‘Midnight Flyer’ „An album like lemon ice cream – when will it be summer again?“ what really happened. -

How It Works Issue 9

NEW THE MAGAZINE THAT FEEDS MINDS INSIDE INTERVIEW DR YAN WONG TM FROM BBC’S BANG SCIENCE ■ ENVIRONMENT ■ TECHNOLOGY ■ TRANSPORT HISTORY ■ SPACE GOES THE THEORY HEART VOLCANIC BYPASSES ERUPTIONS How modern surgeons Discover the explosive save lives everyday BREAK THE 200MB BARRIER! power beneath Earth SUPERFAST BROADBAND LEARN REVEALED! THE NEXT-GENERATION ABOUT NETWORKS THAT DELIVER ■ CASSINI PROBE WARP-SPEED INTERNET ■ RAINING ANIMALS ■ PLANET MERCURY ■ BATTLE OF BRITAIN THE WORLD’S ■ PLACEBO EFFECT ■ LEANING TOWER OF PISA DEADLIEST ■ THE NERVOUS SYSTEM CHOPPER ■ ANDROID VS iPHONE Inside the Apache ■ AVALANCHES 919 AH-64D Longbow FACTS AND 9 ANSWERS 0 INSIDE £3.99 4 0 0 2 3 7 1 4 0 ISSN 2041-7322 2 7 7 ISSUE NINE ISSUE RACE TO 9 HUMAN SOLAR ROLLER 1,000MPH ALLERGIES© Imagine PublishingFLARES Ltd COASTERS Awesome engineering Why dust,No unauthorisedhair and pollen copyingHow massive or distribution explosions on Heart-stopping secrets of behind the land speed record make us sneeze the Sun affect our planet the world’s wildest rides www.howitworksdaily.com 001_HIW_009.indd 1 27/5/10 16:34:18 © Imagine Publishing Ltd No unauthorised copying or distribution Get in touch Have YOU got a question you want answered by the How It Works team? Get in touch by… Email: [email protected] Web: www.howitworksdaily.com ISSUE NINE Snail mail: How It Works Imagine Publishing, 33 Richmond Hill The magazine that feeds minds! Bournemouth, Dorset, BH2 6EZ ”FEED YOUR MIND!” Welcome to How It Meet the experts The sections explained Works issue -

Leading Music Enthusiast Content Publisher Doubles Video Output

CASE STUDY Leading Music Enthusiast Content Publisher Doubles Video Output with StorNext When a leading creator of specialized music news, enthusiast, and instructional content wanted to increase their output, they hit a major roadblock. Their aging video production SAN, an Xsan inherited through an acquisition, just wasn’t up to a faster tempo. Installing Quantum’s StorNext Pro Foundation turned their workflow from lento to prestissimo and doubled production. StorNext Pro Foundation We do not have a large IT staff, so it was really important to find a solution that would be “turn-key, that could fit in quickly and that would minimize ongoing admin. We needed something that would be easy to install and that would just work once it was in. Anthony Verbanac Director of IT, NewBay Media FEATURED PRODUCTS ” The StorNext Pro Foundation was exactly what we needed...It gives us the capacity we need today, room to grow in the future, and it is compatible with all our applications “and the latest versions of OS X. ” Anthony Verbanac - Director of IT, NewBay Media With over 13 million monthly readers in over previously released material is incorporated into 50 countries around the world, NewBay new offerings, and support has to be provided Media is the industry’s premiere publisher of for YouTube and all the latest Apple, Google, specialized enthusiast content across music, Nook, and Kindle formats. SOLUTION OVERVIEW pro-audio, video, and gaming, which it delivers ∙ StorNext Pro Foundation through a combination of traditional print and AGING SAN LIMITS GROWTH - StorNext® 5 platform new media platforms. -

110% Gaming 220 Triathlon Magazine 3D World Adviser

110% Gaming 220 Triathlon Magazine 3D World Adviser Evolution Air Gunner Airgun World Android Advisor Angling Times (UK) Argyllshire Advertiser Asian Art Newspaper Auto Car (UK) Auto Express Aviation Classics BBC Good Food BBC History Magazine BBC Wildlife Magazine BIKE (UK) Belfast Telegraph Berkshire Life Bikes Etc Bird Watching (UK) Blackpool Gazette Bloomberg Businessweek (Europe) Buckinghamshire Life Business Traveller CAR (UK) Campbeltown Courier Canal Boat Car Mechanics (UK) Cardmaking and Papercraft Cheshire Life China Daily European Weekly Classic Bike (UK) Classic Car Weekly (UK) Classic Cars (UK) Classic Dirtbike Classic Ford Classic Motorcycle Mechanics Classic Racer Classic Trial Classics Monthly Closer (UK) Comic Heroes Commando Commando Commando Commando Computer Active (UK) Computer Arts Computer Arts Collection Computer Music Computer Shopper Cornwall Life Corporate Adviser Cotswold Life Country Smallholding Country Walking Magazine (UK) Countryfile Magazine Craftseller Crime Scene Cross Stitch Card Shop Cross Stitch Collection Cross Stitch Crazy Cross Stitch Gold Cross Stitcher Custom PC Cycling Plus Cyclist Daily Express Daily Mail Daily Star Daily Star Sunday Dennis the Menace & Gnasher's Epic Magazine Derbyshire Life Devon Life Digital Camera World Digital Photo (UK) Digital SLR Photography Diva (UK) Doctor Who Adventures Dorset EADT Suffolk EDGE EDP Norfolk Easy Cook Edinburgh Evening News Education in Brazil Empire (UK) Employee -

Pressreader Magazine Titles

PRESSREADER: UK MAGAZINE TITLES www.edinburgh.gov.uk/pressreader Computers & Technology Sport & Fitness Arts & Crafts Motoring Android Advisor 220 Triathlon Magazine Amateur Photographer Autocar 110% Gaming Athletics Weekly Cardmaking & Papercraft Auto Express 3D World Bike Cross Stitch Crazy Autosport Computer Active Bikes etc Cross Stitch Gold BBC Top Gear Magazine Computer Arts Bow International Cross Stitcher Car Computer Music Boxing News Digital Camera World Car Mechanics Computer Shopper Carve Digital SLR Photography Classic & Sports Car Custom PC Classic Dirt Bike Digital Photographer Classic Bike Edge Classic Trial Love Knitting for Baby Classic Car weekly iCreate Cycling Plus Love Patchwork & Quilting Classic Cars Imagine FX Cycling Weekly Mollie Makes Classic Ford iPad & Phone User Cyclist N-Photo Classics Monthly Linux Format Four Four Two Papercraft Inspirations Classic Trial Mac Format Golf Monthly Photo Plus Classic Motorcycle Mechanics Mac Life Golf World Practical Photography Classic Racer Macworld Health & Fitness Simply Crochet Evo Maximum PC Horse & Hound Simply Knitting F1 Racing Net Magazine Late Tackle Football Magazine Simply Sewing Fast Bikes PC Advisor Match of the Day The Knitter Fast Car PC Gamer Men’s Health The Simple Things Fast Ford PC Pro Motorcycle Sport & Leisure Today’s Quilter Japanese Performance PlayStation Official Magazine Motor Sport News Wallpaper Land Rover Monthly Retro Gamer Mountain Biking UK World of Cross Stitching MCN Stuff ProCycling Mini Magazine T3 Rugby World More Bikes Tech Advisor -

December 2016 Adults Men Women Total ABC1 C2DE 15

NRS Readership Estimates - General Magazines AIR - Latest 12 Months- January - December 2016 Adults Men Women Total ABC1 C2DE 15-34 35+ Total Total UNWEIGHTED SAMPLE 28006 16468 11538 6569 21437 12485 15521 EST.POPULATION 15+ (000s) 52324 28552 23772 16379 35945 25582 26742 (000s) % (000s) % (000s) % (000s) % (000s) % (000s) % (000s) % General Weekly Magazines What's on TV H 2227 4.3 857 3.0 1371 5.8 541 3.3 1687 4.7 727 2.8 1501 5.6 Radio Times H 1840 3.5 1379 4.8 461 1.9 220 1.3 1620 4.5 844 3.3 996 3.7 TV Choice H 1527 2.9 570 2.0 956 4.0 286 1.7 1240 3.5 447 1.7 1079 4.0 TV Times H 976 1.9 417 1.5 559 2.4 257 1.6 719 2.0 383 1.5 593 2.2 Total TV Guide Y 472 0.9 199 0.7 273 1.1 162 1.0 310 0.9 196 0.8 276 1.0 Time Out Y 433 0.8 345 1.2 89 0.4 218 1.3 215 0.6 213 0.8 221 0.8 The Big Issue Y 348 0.7 239 0.8 108 0.5 83 0.5 264 0.7 149 0.6 199 0.7 TV & Satellite Week Y 344 0.7 135 0.5 209 0.9 76 0.5 268 0.7 193 0.8 151 0.6 The Week Y 316 0.6 290 1.0 26 0.1 69 0.4 247 0.7 146 0.6 170 0.6 NME Y 267 0.5 202 0.7 65 0.3 159 1.0 108 0.3 176 0.7 91 0.3 Motorcycle News Y 231 0.4 128 0.4 103 0.4 49 0.3 181 0.5 178 0.7 53 0.2 Country Life Y 214 0.4 140 0.5 74 0.3 43 0.3 171 0.5 94 0.4 120 0.4 Autocar T 214 0.4 119 0.4 95 0.4 88 0.5 126 0.3 175 0.7 38 0.1 Kerrang! T 198 0.4 115 0.4 83 0.3 147 0.9 52 0.1 114 0.4 84 0.3 Angling Times T 181 0.3 77 0.3 104 0.4 47 0.3 134 0.4 165 0.6 16 0.1 Horse and Hound Y 176 0.3 117 0.4 59 0.2 59 0.4 117 0.3 35 0.1 141 0.5 Auto Express T 166 0.3 98 0.3 68 0.3 51 0.3 115 0.3 147 0.6 18 0.1 Match! T 141 0.3 69 0.2 72