Fiat Chrysler Automobiles NV

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Future Mobility

FUTURE MOBILITY Sector report 29 October 2019 – 5:30 PM Automotive – Mobility - Infrastructures CASE: what will change for OEMs CASE (Connectivity, Autonomous, Sharing and Electric) will change the way consumers see mobility and will dramatically transform the industry. Quarterly results will be useful to assess short-term price reactions but, we believe, how every company is positioned in a fast- changing environment cannot be ignored for long-term returns. The industry transformation doesn’t necessarily mean “shrinking”: we believe that the overall size of the profit should rise. But a large amount of business centred on ownership models will be transacted in the future through mobility providers (i.e. services) and current incumbents may not be the winners. We initiate coverages on CNH (NEUTRAL, TP EUR10.3) that aims to be a disruptor in its sector thanks profiting from future mobility trends but it is witnessing an unpredictable AG cycle, Ferrari (BUY, TP EUR163.0) which will use the hybrid technology at its advantages and Piaggio (BUY, TP EUR3.20) where electric will support a new replacement cycle. > Regulators are forcing the transition to electric but pick-up will be slowed down by the lack of infrastructure: EU CO2 targets are forcing carmakers to introduce EVs despite they are still losing money on it and consumers are wobbling. However, slow deployment of charging infrastructure, lack in electricity storage and grids last mile capacity, constraints on battery production and recycling should limit PHEV and BEV to 16% of total registrations by 2025. We believe that electric is a perfect technology for 2 wheelers where “range anxiety” doesn’t apply Massimo Vecchio Senior Analyst and could trigger a long-awaited replacement cycle. -

1230019 Ritchie Bros

Unreserved Public Auction Caorso, IT Timed auction only, see notice >> Tel: .. Fax: .. Auction location: Via Canada snc Angolo SP R, Caorso (PC), Italy facebook.com/ritchiebrositalia KOMATSU PCNLC VOLVO AG UNUSED MANITOU MRT S PRIVILEGE+ FENDT VARIO PROFI IVECO STRALIS X W/ EFFER /S KG . M rbauction.com/caorso © Copyright Ritchie Bros. Auctioneers – CAT K DOOSAN DL KOMATSU WA NEW HOLLAND WB HITACHI ZW CAT C DYNAPAC CAD BOMAG BWDH HAMM HT More items added daily! View the latest listings for this auction at rbauction.com/caorso HITACHI ZX LCN- NEW HOLLAND EC KOMATSU PCNHD KOMATSU PCNLC / HITACHI ZXLCN JCB JSN CAT D LCR JCB JSW KOMATSU PWESK More items added daily! View the latest listings for this auction at rbauction.com/caorso VOLVO ECR D KUBOTA KX KUBOTA KX HITACHI ZX USBLC CASE CXB S KOMATSU PCMR QTY OF UNUSED HITACHI ZXU YR SUNWARD SWTL CAT B More items added daily! View the latest listings for this auction at rbauction.com/caorso UNUSED — MANITOU MRT Easy S DIECI PEGASUS . DIECI PEGASUS . / & MERLO ROTO . MANITOU MTL MANITOU MVT MERLO P. / MERLO P . DIECI APOLLO . More items added daily! View the latest listings for this auction at rbauction.com/caorso / HAULOTTE HAPX / HAULOTTE HAPX / HAULOTTE HTPX JLG SJP JLG AJP / JLG SJ JLG SJ / HAULOTTE HAPX / HAULOTTE HA SPX More items added daily! View the latest listings for this auction at rbauction.com/caorso CLAAS DOMINATOR SL NEW HOLLAND T. JOHN DEERE PREMIUM UNUSED SAME EXPLORER UNUSED SAME EXPLORER UNUSED SAME -

Federico Vidari Resume

FEDERICO VIDARI I use my dierent professional and personal experiences to achieve business goals. Together with a passion for work and continuous change, I practice a holistic approach to generate innovation inside and outside companies. > https://www.linkedin.com/in/federicovidari SUMMARY MY LIFE PHILOSOPHY I have been working in marketing, in particular, digital communication, since 1995. Life is what happens while you're My education Architecture Degree, Politecnico di Milano; busy making your excuses. Erasmus at TUBerlin) has provided me with a highly Simple Plan methodological, results-oriented and client-centred approach to digital design and development, from conception and planning to execution, through iterative revisions. MOST PROUD OF My experience has been consolidated through a wide range of different marketing projects. I am a skilled interlocutor with clients from all backgrounds, and a team leader able to World Citizen generate a high level of engagement in all stakeholders: Lived in Berlin and Aachen DE clients, team and suppliers. Worked in Rio de Janeiro, Berlin, Aachen, Modena, Imola. I am an expert about Business Design and Transformation, Branding, Communication and Digital Strategy, UX/UI Design, Ecommerce, Email Marketing, Social Media Marketing, Social Maserati & Ferrari websites Selling, Sales enablement and digital coaching. Delivered in a complex stakeholders I am Adjunct Professor of Communication MetaDesign and environment Service Design at Politecnico di Milano. % Next Level Fest Organized a Music Festival -

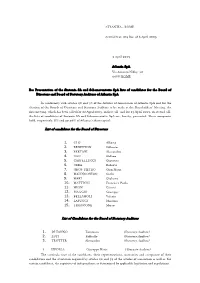

Presentation of the Sintonia SA and Schemaventotto Spa Lists of Candidates for the Board of Directors and Board of Statutory Auditors of Atlantia Spa

ATLANTIA - ROME Arrival Prot. 015 Res. of 6 April 2009 2 April 2009 Atlantia SpA Via Antonio Nibby, 20 00161 ROME Re: Presentation of the Sintonia SA and Schemaventotto SpA lists of candidates for the Board of Directors and Board of Statutory Auditors of Atlantia SpA In conformity with articles 20 and 30 of the Articles of Association of Atlantia SpA and for the election of the Boards of Directors and Statutory Auditors to be made at the Shareholders’ Meeting, the first meeting, which has been called for 22 April 2009, in first call, and for 23 April 2009, in second call, the lists of candidates of Sintonia SA and Schemaventotto SpA are, hereby, presented. These companies hold, respectively, 8% and 30.06% of Atlantia’s share capital; List of candidates for the Board of Directors 1. CLO’ Alberto 2. BENETTON Gilberto 3. BERTANI Alessandro 4. CAO Stefano 5. CASTELLUCCI Giovanni 6. CERA Roberto 7. GROS-PIETRO Gian Maria 8. MALINCONICO Carlo 9. MARI Giuliano 10. MATTIOLI Francesco Paolo 11. MION Gianni 12. PIAGGIO Giuseppe 13. BELLAMOLI Valerio 14. LAPUCCI Massimo 15. TRONCONE Marco List of Candidates for the Board of Statutory Auditors 1. DI TANNO Tommaso (Statutory Auditor) 2. LUPI Raffaello (Statutory Auditor) 3. TROTTER Alessandro (Statutory Auditor) 1. CIPOLLA Giuseppe Maria (Alternate Auditor) The curricula vitae of the candidates, their representations, warranties and acceptance of their candidature and the attestation required by articles 20 and 32 of the articles of association as well as, for certain candidates, the requisites of independence as determined by applicable legislation and regulations. -

18MY Ebrochure

2018 FIAT® 500X Pop, Trekking and Lounge FIATUSA.COM 888-CIAO-FIAT FIAT is a registered trademark of FCA Group Marketing S.p.A., used under license by FCA US LLC. Page A1 FIAT® 500X WILL UNDOUBTEDLY USE ITS ITALIAN CHARM TO WIN OVER YOUR FRIENDS AND FAMILY ALIKE — AND WITH FOUR DOORS AND PLENTY OF ROOM FOR FIVE, IT HAS THE WHEREWITHAL TO INVITE THEM ALONG. IN ALL, THE 500X WILL GO BEYOND BEING A GREAT VEHICLE TO DRIVE, IT WILL BECOME A TRUSTED COMPANION. 02 03 Page A2 Page A3 Page F5X18US4_022 FIAT 500X Pop, Trekking and Lounge models offer a differing mix of utility, agility, effi ciency and sense of fun, uniquely suited to your specifi c driving style. Each one instills a solid feeling of confi dence with its innovative The environments, both inside and outside available All-Wheel Drive that includes the FIAT® 500X, are wide and varied. Personal the fl exible FIAT Dynamic Selector and driving style is encouraged with a generous mix disconnecting rear axle — quickly responding of exterior colors, accessories and interiors. to changes in terrain, weather and driver An available dual-pane power sunroof with preference. Long live spontaneity. a sliding front panel creates a wide, spacious feeling. This is a vehicle that is meant to transport people — and move them, as well. FIAT 500X Trekking shown in Bianco Gelato and Lounge shown in Rame Chiaro. 04 05 Page A4 Page A5 Page • 1.4L 16V MultiAir® Turbo I-4 — • 2.4L 16V Tigershark with MultiAir2 I-4 • 2.4L 16V Tigershark® with MultiAir®2 I-4 160 hp/184 lb-ft of torque with and 9-speed automatic with AutoStick and 9-speed automatic with AutoStick 6-speed manual • AWD System — Available • All-Wheel-Drive (AWD) System — Available • 2.4L 16V Tigershark® with MultiAir2 I-4 — • FIAT Dynamic Selector with 3 modes: • FIAT® Dynamic Selector with 3 modes: 180 hp/175 lb-ft of torque and 9-speed Auto, Sport and Traction+ (available only on Auto, Sport and Traction+ (available only on automatic with AutoStick — Available AWD models) Properly secure all cargo. -

European Commission

C 66/56 EN Offi cial Jour nal of the European Union 26.2.2021 PROCEDURES RELATING TO THE IMPLEMENTATION OF COMPETITION POLICY EUROPEAN COMMISSION Prior notification of a concentration (Case M.10148 — FCA/EEPS/JV) Candidate case for simplified procedure (Text with EEA relevance) (2021/C 66/15) 1. On 18 February 2021, the Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 (1). This notification concerns the following undertakings: — FCA Italy S.p.A. (‘FCA’, Italy), a subsidiary of the Fiat Chrysler Automobiles N.V. Group (‘FCA NV’, The Netherlands), which will incorporate Peugeot S.A. and be renamed as Stellantis N.V. (The Netherlands), — EPS E-mobility S.r.l. (‘EPS E-mobility’), currently owned by ENGIE EPS Italia S.r.l. (‘EEPS’, Italy), a subsidiary of the ENGIE Group (France). FCA and EEPS acquire within the meaning of Article 3(1)(b) and 3(4) of the Merger Regulation joint control of EPS E-mobility. The concentration is accomplished by way of purchase of shares. 2. The business activities of the undertakings concerned are: — for FCA NV: a global automotive group whose activities envisage the design, manufacture and sale of passenger cars and light commercial vehicles (under the Abarth, Alfa Romeo, Chrysler, Dodge, Fiat, Fiat Professional, Jeep, Lancia, Maserati and Ram brands) as well as of components and production systems worldwide, — for EEPS: is the industrial player of the ENGIE group active in the provision of microgrid solutions, energy storage systems for renewable power producers and e-mobility services, — for EPS E-mobility: develops innovative solutions and technologies for electric and hybrid vehicles providing innovative charging solutions. -

Ivecobus Range Handbook.Pdf

CREALIS URBANWAY CROSSWAY EVADYS 02 A FULL RANGE OF VEHICLES FOR ALL THE NEEDS OF A MOVING WORLD A whole new world of innovation, performance and safety. Where technological excellence always travels with a true care for people and the environment. In two words, IVECO BUS. CONTENTS OUR HISTORY 4 OUR VALUES 8 SUSTAINABILITY 10 TECHNOLOGY 11 MAGELYS DAILY TOTAL COST OF OWNERSHIP 12 HIGH VALUE 13 PLANTS 14 CREALIS 16 URBANWAY 20 CROSSWAY 28 EVADYS 44 MAGELYS 50 DAILY 56 IVECO BUS CHASSIS 68 IVECO BUS ALWAYS BY YOUR SIDE 70 03 OUR HISTORY ISOBLOC. Presented in 1938 at Salon de Paris, it was the fi rst modern European coach, featuring a self-supporting structure and rear engine. Pictured below the 1947 model. 04 PEOPLE AND VEHICLES THAT TRANSPORTED THE WORLD INTO A NEW ERA GIOVANNI AGNELLI JOSEPH BESSET CONRAD DIETRICH MAGIRUS JOSEF SODOMKA 1866 - 1945 1890 - 1959 1824 - 1895 1865 - 1939 Founder, Fiat Founder, Société Anonyme Founder, Magirus Kommanditist Founder, Sodomka des établissements Besset then Magirus Deutz then Karosa Isobloc, Chausson, Berliet, Saviem, Fiat Veicoli Industriali and Magirus Deutz trademarks and logos are the property of their respective owners. 05 OVER A CENTURY OF EXPERIENCE AND EXPERTISE IVECO BUS is deeply rooted into the history of public transport vehicles, dating back to when the traction motor replaced horse-drawn power. We are proud to carry on the tradition of leadership and the pioneering spirit of famous companies and brands that have shaped the way buses and coaches have to be designed and built: Fiat, OM, Orlandi in Italy, Berliet, Renault, Chausson, Saviem in France, Karosa in the Czech Republic, Magirus-Deutz in Germany and Pegaso in Spain, to name just a few. -

Artelectric, the New Project by Leasys, Is Born First Partnership Signed with the Reggia Di Venaria

ARTELECTRIC, THE NEW PROJECT BY LEASYS, IS BORN FIRST PARTNERSHIP SIGNED WITH THE REGGIA DI VENARIA ● ArtElectric, the green project by Leasys to support and enhance art and culture by creating tourist itineraries with electric mobility, is born. ● The first partnership with the Reggia di Venaria for the installation of 8 electric vehicle charging stations for Leasys customers has been signed. Turin, 30 July 2020 The first partnership between Leasys, a leading company in the mobility sector that is part of the FCA Bank Group, and the Reggia di Venaria, a Savoy royal residence declared World Heritage Site by UNESCO and managed by the Consorzio delle Residenze Reali Sabaude, has been signed. This partnership is the first step in the new ArtElectric project by Leasys, aimed at supporting and enhancing art and culture by creating tourist itineraries including the Royal Palaces, Art Residences and Italian Historic Houses, by establishing and implementing a widespread network of Leasys charging stations supporting green mobility for the electric and hybrid cars produced by the FCA Group. ArtElectric is part of the Residences of the Royal House of Savoy because of its deep roots in the local area and its relationship with art and culture. Its ambition is to quickly become a project with a national and international scope in which the combination of tourism and art is increasingly linked to green mobility, based on mutual benefits for the places of interest and customers. The partnership between Leasys and the Reggia di Venaria involves the installation of 8 charging stations at the car parks where Leasys customers who hire a car for short- or long- term use, will be able to charge their electric or hybrid cars while visiting the Palace. -

Annual Report

ai158746681363_GAC AR2019 Cover_man 29.8mm.pdf 1 21/4/2020 下午7:00 Important Notice 1. The Board, supervisory committee and the directors, supervisors and senior management of the Company warrant the authenticity, accuracy and completeness of the information contained in the annual report and there are no misrepresentations, misleading statements contained in or material omissions from the annual report for which they shall assume joint and several responsibilities. 2. All directors of the Company have attended meeting of the Board. 3. PricewaterhouseCoopers issued an unqualified auditors’ report for the Company. 4. Zeng Qinghong, the person in charge of the Company, Feng Xingya, the general manager, Wang Dan, the person in charge of accounting function and Zheng Chao, the manager of the accounting department (Accounting Chief), represent that they warrant the truthfulness and completeness of the financial statements contained in this annual report. 5. The proposal for profit distribution or conversion of capital reserve into shares for the reporting period as considered by the Board The Board proposed payment of final cash dividend of RMB1.5 per 10 shares (tax inclusive). Together with the cash dividend of RMB0.5 per 10 shares (including tax) paid during the interim period, the ratio of total cash dividend payment for the year to net profit attributable to the shareholders’ equity of listed company for the year would be approximately 30.95%. 6. Risks relating to forward-looking statements The forward-looking statements contained in this annual report regarding the Company’s future plans and development strategies do not constitute any substantive commitment to investors and investors are reminded of investment risks. -

2018 Annual Report

2018 ANNUAL REPORT 2018 ANNUAL REPORT AND FORM 20-F 2 2018 | ANNUAL REPORT 2018 | ANNUAL REPORT 3 Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes No Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes No Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and emerging growth company” in Rule 12b-2 of the Exchange Act. Large accelerated filer Accelerated filer Non-accelerated filer Emerging growth company If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing: U.S. -

Head of Alfa Romeo Safe Harbor Statement

TIM KUNISKIS | HEAD OF ALFA ROMEO SAFE HARBOR STATEMENT This document and the related presentation contain forward-looking statements. In particular, to compliance with environmental, health and safety regulations; the intense level of these forward-looking statements include statements regarding future financial performance competition in the automotive industry, which may increase due to consolidation; exposure to and the Company‟s expectations as to the achievement of certain targeted metrics, including shortfalls in the funding of the Group‟s defined benefit pension plans; the Group‟s ability to net debt and net industrial debt, revenues, free cash flow, vehicle shipments, capital provide or arrange for access to adequate financing for the Group‟s dealers and retail investments, research and development costs and other expenses at any future date or for customers and associated risks related to the establishment and operations of financial any future period are forward-looking statements. These statements may include terms such services companies including capital required to be deployed to financial services; the as “may”, “will”, “expect”, “could”, “should”, “intend”, “estimate”, “anticipate”, “believe”, Group‟s ability to access funding to execute the Group‟s business plan and improve the “remain”, “on track”, “design”, “target”, “objective”, “goal”, “forecast”, “projection”, “outlook”, Group‟s business, financial condition and results of operations; a significant malfunction, “prospects”, “plan”, or similar terms. Forward-looking statements are not guarantees of future disruption or security breach compromising the Group‟s information technology systems or performance. Rather, they are based on the Group‟s current state of knowledge, future the electronic control systems contained in the Group‟s vehicles; the Group‟s ability to realize expectations and projections about future events and are by their nature, subject to inherent anticipated benefits from joint venture arrangements; the Group‟s ability to successfully risks and uncertainties. -

Copyrighted Material

Part I THE POWER OF A FAMILY COPYRIGHTED MATERIAL cc01.indd01.indd 1111 005/11/115/11/11 22:01:01 PPMM cc01.indd01.indd 1122 005/11/115/11/11 22:01:01 PPMM Chapter 1 The Scattered Pieces short time before he died, Gianni Agnelli had asked his younger brother Umberto, who had come to visit him every A day at Gianni’s mansion on a hill overlooking Turin, to do something very diffi cult. Umberto said he needed to think about it. Now, at the end of January 2003, Umberto had come to give Gianni an answer. Gianni was confi ned to a wheelchair, spending his fi nal days at home. He had once found solace looking out of the window onto his wife Marella’s fl ower gardens below, especially his favorites, the yellow ones. But now it was winter. Gianni looked out at the city of Turin, which was visible across the river through the bare trees. Street after street stretched out toward the horizon in the crisp January air, lined up like an army of troops marching to meet the Alps beyond. It was a clear day, and he could see Fiat’s white Lingotto headquarters, as well as the vast bulk of Fiat’s Mirafi ori car factory on the far side of the city. The factories had been built by their grandfather, Giovanni Agnelli. 13 cc01.indd01.indd 1133 005/11/115/11/11 22:01:01 PPMM 14 the power of a family Gianni wouldn’t admit to his family that he was dying, but they all knew.