Capital and the Debt Trap

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Workers and Labour in a Globalised Capitalism

Workers and Labour in a Globalised Capitalism MANAGEMENT, WORK & ORGANISATIONS SERIES Series editors: Gibson Burrell, School of Management, University of Leicester, UK Mick Marchington, Manchester Business School, University of Manchester and Strathclyde Business School, University of Strathclyde, UK Paul Thompson, Strathclyde Business School, University of Strathclyde, UK This series of textbooks covers the areas of human resource management, employee relations, organisational behaviour and related business and management fields. Each text has been specially commissioned to be written by leading experts in a clear and accessible way. The books contain serious and challenging material, take an analytical rather than prescriptive approach and are particularly suitable for use by students with no prior specialist knowledge. The series is relevant for many business and management courses, including MBA and post-experience courses, specialist masters and postgraduate diplomas, professional courses and final-year undergraduate courses. These texts have become essential reading at business and management schools worldwide. Published titles include: Maurizio Atzeni WORKERS AND LABOUR IN A GLOBALISED CAPITALISM Stephen Bach and Ian Kessler THE MODERNISATION OF THE PUBLIC SERVICES AND EMPLOYEE RELATIONS Emma Bell READING MANAGEMENT AND ORGANIZATION IN FILM Paul Blyton and Peter Turnbull THE DYNAMICS OF EMPLOYEE RELATIONS (3RD EDN) Paul Blyton, Edmund Heery and Peter Turnbull (eds) REASSESSING THE EMPLOYMENT RELATIONSHIP Sharon C. Bolton EMOTION -

Governing Body 323Rd Session, Geneva, 12–27 March 2015 GB.323/INS/5/Appendix III

INTERNATIONAL LABOUR OFFICE Governing Body 323rd Session, Geneva, 12–27 March 2015 GB.323/INS/5/Appendix III Institutional Section INS Date: 13 March 2015 Original: English FIFTH ITEM ON THE AGENDA The Standards Initiative – Appendix III Background document for the Tripartite Meeting on the Freedom of Association and Protection of the Right to Organise Convention, 1948 (No. 87), in relation to the right to strike and the modalities and practices of strike action at national level (revised) (Geneva, 23–25 February 2015) Contents Page Introduction ....................................................................................................................................... 1 Decision on the fifth item on the agenda: The standards initiative: Follow-up to the 2012 ILC Committee on the Application of Standards .................. 1 Part I. ILO Convention No. 87 and the right to strike ..................................................................... 3 I. Introduction ................................................................................................................ 3 II. The Freedom of Association and Protection of the Right to Organise Convention, 1948 (No. 87) ......................................................................... 3 II.1. Negotiating history prior to the adoption of the Convention ........................... 3 II.2. Related developments after the adoption of the Convention ........................... 5 III. Supervision of obligations arising under or relating to Conventions ........................ -

Capitalist Meltdo-Wn

"To face reality squarely; not to seek the line of least resistance; to call things by their right names; to speak t�e truth to the masses, no matter how bitter it may be; not to fear obstacles; to be true in little thi�gs as in big ones; to base one's progra.1!1 on the logic of the class struggle;. to be bold when the hour of action arrives-these are the rules of the Fourth International." 'Inequality, Unemployment & Injustice' Capitalist Meltdo-wn Global capitalism is currently in the grip of the most The bourgeois press is relentless in seizing on even the severe economic contraction since the Great Depression of smallest signs of possible "recovery" to reassure consumers the 1930s. The ultimate depth and duration of the down and investors that better days are just around thecomer. This turn remain to be seen, but there are many indicators that paternalistic" optimism" recalls similar prognosticationsfol point to a lengthy period of massive unemployment in the lowing the 1929 Wall Street crash: "Depression has reached imperialist camp and a steep fall in living standards in the or passed its bottom, [Assistant Secretary of Commerce so-called developing countries. Julius] Klein told the Detroit Board of Commerce, although 2 'we may bump along' for a while in returningto higher trade For those in the neocolonies struggling to eke out a living levels " (New Yo rk Times, 19 March 19 31).The next month, on a dollar or two a day, this crisis will literally be a matter in a major speech approved by President Herbert Hoover, of life and death. -

Assessing Mondragon: Stability & Managed Change in the Face Of

THE WILLIAM DAVIDSON INSTITUTE AT THE UNIVERSITY OF MICHIGAN Assessing Mondragon: Stability & Managed Change in the Face of Globalization By: Saioa Arando, Fred Freundlich, Monica Gago, Derek C. Jones and Takao Kato William Davidson Institute Working Paper Number 100 3 November 2010 Assessing Mondragon: Stability and Managed Change in the Face of Globalization Saioa Arando, Fred Freundlich, Monica Gago, Derek C. Jones and Takao Kato November, 2010 Abstract By drawing on new interview evidence gathered during several field trips and new financial and economic data from both external and internal sources, we document and assess the changing economic importance and performance of the Mondragon group of cooperatives as well as the two largest sectors within the group. Compared to conventional firms in the Basque Country and Spain, and producer co-ops (PCs) and employee owned firms elsewhere, in general we find evidence of growing group importance and strong performance and a similarly strong record for the industrial and retail divisions. These stylized facts do not support hypotheses concerning PCs such as predictions that PCs will restrict employment and become progressively comparatively undercapitalized. In accounting for this record, we highlight key and, at times, not uncontroversial institutional developments in the group during the last 20 years or so that indicate the existence of a continuing capacity for institutional adaptation in Mondragon-- an ongoing ability to innovate and make institutional adjustments to deal with emerging challenges. In addition, we provide more detailed information than before on some key distinguishing institutional mechanisms of the Mondragon group, including the extent of worker-member transfers during economic crises, the patterns of profit pooling and the type and volume of training. -

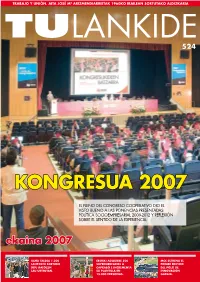

Kongresua 2007

TRABAJO Y UNIÓN. Aita JOSÉ Mª ARIZMENDIARRIEtaK 1960KO IRAILEAN SortutaKO ALDIZKARIA 524 KongrESua 2007 EL PLENO DEL CONGRESO COOPERATIVO DIO EL VISTO BUENO A LAS PONENCIAS PRESENTADAS: POLÍTICA SOCIOEMPRESARIAL 2009-2012 Y REFLEXIÓN SOBRE EL SENTIDO DE LA EXPERIENCIA. ekaina 2007 ULMA TALDEA 1.200 EROSKI ADQUIERe 500 MCC esTRENA el LANPOSTU sORTUKO SUPERMERCADOs A PRIMER edIFICIO DITU dATOZEN CAPRABO E INCREMENTA del POLO de LAU URTEOTAN. SU PLANTILLA eN INNOVACIÓN 15.000 PERSONAS. GARAIA. TRABAJO Y UNIÓN (T. U. LanKIDE), Aita José Mª Arizmendiarrietak JUNIO 2007 1960ko irailean sortutako aldizkaria. 524 argitaratZaiLEA OTALORA. Azatza. 3 editorial 20550 Aretxabaleta. Gipuzkoa. Telefonoa: 943 712 406. El cambio que necesitamos Faxa: 943 712 339 4 Kooperatibetako berriak 8 MCC reconocida en el ZUZENDaria “Día Mundial del Donante de sangre” Javier Marcos Por su estrecha colaboración con la Asociación ([email protected]) de Donantes de Sangre de Álava. 20 el grupo ulma creará 1.200 nuevos ERREDAKZIO-KONTSEILUA empleos entre 2007-2010 En ese periodo invertirá cerca de 500 millones de euros Lehendakaria: con el objetivo de desarrollar sus negocios y lanzar y Juan Mª Otaegi. consolidar nuevas promociones empresariales. Kideak: José Antonio Ajuria. 25 grupo eroski adQuiere el 75% de caprabo Espe Arregi. Y se convierte en uno de los grupos de referencia Juan Cid. en la distribución española, con una red de 2.348 Jesús Miguel Euba. establecimientos, más de 47.000 trabajadores y un volumen Mikel Garcia. de facturación superior a los 8.600 millones de euros. Jesús Ginto. José Mª Larrañaga. Carlos Sarabia. 26 EN portada Carmelo Urdangarín. -

International Journal of Labour Research

Financial crises, defl ation INTERNATIONAL JOURNAL and trade union responses: What are the lessons? 2 / Issue 1 2010 / Volume OF LABOUR RESEARCH 2010 VOLUME 2 / ISSUE 1 American labour and the Great Depression Steve Fraser Financial crises and organized labour: Sweden 1990–94 Ingemar Lindberg and Magnus Ryner The Asian crisis of 1997–98: The case of the Republic of Korea Jin Ho Yoon The Japanese economic crisis of the 1990s Naoto Ohmi The labour market and defl ation in Japan Hansjörg Herr and Milka Kazandziska The Great Recession: A turning point for labour? Frank Hoffer FFinancialinancial ccrises,rises, ddeflefl aationtion aandnd ttraderade uunionnion rresponses:esponses: WWhathat aarere tthehe llessons?essons? INTERNATIONAL JOURNAL OF LABOUR RESEARCH ISSN 2076-9806 2010 / VOLUME 2 / ISSUE 1 Financial crises, defl ation and trade union responses: What are the lessons? Financial crises, defl ILO 110030102finan0030102finan E.inddE.indd 1 117.6.20107.6.2010 111:15:401:15:40 International Journal of Labour Research 2010 Vol. 2 Issue 1 Financial crises, deflation and trade union responses: What are the lessons? INTERNATIONAL LABOUR OFFICE, GENEVA Copyright © International Labour Organization 2010 First published 2010 Publications of the International Labour Office enjoy copyright under Protocol 2 of the Uni- versal Copyright Convention. Nevertheless, short excerpts from them may be reproduced without authorization, on condition that the source is indicated. For rights of reproduction or translation, application should be made to ILO Publications (Rights and Permissions), International Labour Office, CH-1211 Geneva 22, Switzerland, or by email: [email protected]. The International Labour Office welcomes such applications. Libraries, institutions and other users registered with reproduction rights organizations may make copies in accordance with the licences issued to them for this purpose. -

Michigan Laborlabor Law:Law: Whatwhat Everyevery Citizencitizen Shouldshould Knowknow

August 1999 A Mackinac Center Report MichiganMichigan LaborLabor Law:Law: WhatWhat EveryEvery CitizenCitizen ShouldShould KnowKnow by Robert P. Hunter, J. D., L L. M Workers’ and Employers’ Rights and Responsibilities, and Recommendations for a More Government-Neutral Approach to Labor Relations The Mackinac Center for Public Policy is a nonpartisan research and educational organization devoted to improving the quality of life for all Michigan citizens by promoting sound solutions to state and local policy questions. The Mackinac Center assists policy makers, scholars, business people, the media, and the public by providing objective analysis of Michigan issues. The goal of all Center reports, commentaries, and educational programs is to equip Michigan citizens and other decision makers to better evaluate policy options. The Mackinac Center for Public Policy is broadening the debate on issues that has for many years been dominated by the belief that government intervention should be the standard solution. Center publications and programs, in contrast, offer an integrated and comprehensive approach that considers: All Institutions. The Center examines the important role of voluntary associations, business, community and family, as well as government. All People. Mackinac Center research recognizes the diversity of Michigan citizens and treats them as individuals with unique backgrounds, circumstances, and goals. All Disciplines. Center research incorporates the best understanding of economics, science, law, psychology, history, and morality, moving beyond mechanical cost/benefit analysis. All Times. Center research evaluates long-term consequences, not simply short-term impact. Committed to its independence, the Mackinac Center for Public Policy neither seeks nor accepts any government funding. It enjoys the support of foundations, individuals, and businesses who share a concern for Michigan’s future and recognize the important role of sound ideas. -

Austeritarianism in Europe: What Options for Resistance?

Austeritarianism in Europe: what options for resistance? Richard Hyman Introduction In much of Europe, the social rights and social protections won by labour movements have recently been seriously eroded, and are further threatened by neoliberal austerity. Efforts to resist have been largely unsuccessful; but is an effective fight-back possible? In the next section I briefly outline how the ‘new economic governance’ of the European Union (EU) has reinforced this erosion, particularly with the economic crisis and the ensuing pursuit of austerity. I then survey a range of forms of protest and opposition, notably through trade union action (section 2), before turning to a discussion of ‘new’ social movements (section 3). In conclusion I suggest that a nuanced evaluation of success and failure is necessary, and I propose that the articulation of different forms of resistance – cross-nationally and between different actors – is essential in order to stem the neoliberal hegemony. 1. Brussels versus workers’ rights? The sovereign debt crisis was facilitated, and at the same time reinforced by, the embrace of neoclassical fiscal orthodoxy within the institutions of the EU. Deflationary macroeconomic priorities date back to the establishment of EMU. The economic logic of ‘correction’ was simple: deflation in order to achieve ‘internal devaluation’ as a substitute for the unavailable option of currency devaluation. A priority was to attack public sector employment, pay and pensions, and to reduce and privatise public services. The recipe was both socially regressive and – in a context of stagnation or recession – negatively pro-cyclical: austerity fuels recession (ETUI 2013: 8; 2014: 17). Social policy in the European Union: state of play 2015 97 Richard Hyman ................................................................................................................................................................ -

If Not Us, Who?

Dario Azzellini (Editor) If Not Us, Who? Workers worldwide against authoritarianism, fascism and dictatorship VSA: Dario Azzellini (ed.) If Not Us, Who? Global workers against authoritarianism, fascism, and dictatorships The Editor Dario Azzellini is Professor of Development Studies at the Universidad Autónoma de Zacatecas in Mexico, and visiting scholar at Cornell University in the USA. He has conducted research into social transformation processes for more than 25 years. His primary research interests are industrial sociol- ogy and the sociology of labour, local and workers’ self-management, and so- cial movements and protest, with a focus on South America and Europe. He has published more than 20 books, 11 films, and a multitude of academic ar- ticles, many of which have been translated into a variety of languages. Among them are Vom Protest zum sozialen Prozess: Betriebsbesetzungen und Arbei ten in Selbstverwaltung (VSA 2018) and The Class Strikes Back: SelfOrganised Workers’ Struggles in the TwentyFirst Century (Haymarket 2019). Further in- formation can be found at www.azzellini.net. Dario Azzellini (ed.) If Not Us, Who? Global workers against authoritarianism, fascism, and dictatorships A publication by the Rosa-Luxemburg-Stiftung VSA: Verlag Hamburg www.vsa-verlag.de www.rosalux.de This publication was financially supported by the Rosa-Luxemburg-Stiftung with funds from the Ministry for Economic Cooperation and Development (BMZ) of the Federal Republic of Germany. The publishers are solely respon- sible for the content of this publication; the opinions presented here do not reflect the position of the funders. Translations into English: Adrian Wilding (chapter 2) Translations by Gegensatz Translation Collective: Markus Fiebig (chapter 30), Louise Pain (chapter 1/4/21/28/29, CVs, cover text) Translation copy editing: Marty Hiatt English copy editing: Marty Hiatt Proofreading and editing: Dario Azzellini This work is licensed under a Creative Commons Attribution–Non- Commercial–NoDerivs 3.0 Germany License. -

Scottishleftreviewissue 54 September/October 2009 £2.00

scottishleftreview Issue 54 September/October 2009 £2.00 scottishleftreviewIssue 54 September/October 2009 Contents Comment ........................................................2 Dave Watson For sale .........................................................14 Whores and virgins .........................................4 Henry McCubbin Robin McAlpine Occupation or strike? ....................................16 It’s the rich who caused the pain ......................6 Gregor Gall Joe Cox Back to the ‘80s? ...........................................18 Answering the Queen......................................8 Donald Adamxon Mike Danson Representation without manipulation ..........20 Inconvenient truths for the neoliberals. .......10 Lou Howson Andy Cumbers Religion is hell ..............................................22 Us swallowing their medicine ......................12 Stephen Bowman Comment cottish politics can be remarkable - and not in a good way. seems to be unable to see the world in any terms other than SThe Megrahi affair has not cast Scottish politics in a good point-scoring. It would be an interesting academic exercise to light, but not for the usually trumpeted reason. Rather, it just write down every position taken by Iain Gray since assuming shows that sometimes we just can’t see past ourselves to ‘leadership’ of the party and map it against the positions taken anything bigger. by the Daily Record. It is not immediately obvious that there has been any difference. Mapping it in the other direction is equally Let’s start with the obvious point - it is perfectly reasonable to telling - it is not just that the Labour Party is in opposition, it’s have different views on the release or non-release of the man that it is developing a new sort of Total Opposition. No matter convicted of the Lockerbie bombing. It is possible to believe that what happens, Scottish Labour finds reason for outrage at the he was in jail rightfully and it is possible to believe that he was SNP. -

Schooled by Strikes? the Effects of Large-Scale Labor Unrest on Mass Attitudes Towards the Labor Movement

Schooled by Strikes? The Effects of Large-Scale Labor Unrest on Mass Attitudes Towards the Labor Movement Alexander Hertel-Fernandez Associate Professor of International and Public Affairs Columbia University 420 W 118th Street, New York, NY 10027 212-854-5717 [email protected] Suresh Naidu Professor of Economics and International and Public Affairs Columbia University 420 W 118th Street, New York, NY 10027 212-854-0027 [email protected] Adam Reich Associate Professor of Sociology Columbia University 606 W 122nd Street, New York, NY 10027 510-599-3450 [email protected] Forthcoming in Perspective on Politics Acknowledgements: The authors thank Patrick Youngblood for terrific research support and feedback. The AFL-CIO and the Polling Consortium offered valuable data and support. The authors also acknowledge the generous financial support of Columbia University’s Institute for Social and Economic Research and Policy, the Russell Sage Foundation, and the Washington Center for Equitable Growth. Lastly, Eric Blanc, Laura Bucci, Jake Grumbach, Aaron Kaufman, Shom Mazumder, Ethan Porter, Ariel White, and the Perspectives editors and reviewers all offered helpful feedback, as did participants in workshops at George Washington University, MIT, Princeton University, the Russell Sage Foundation, Stanford University, the University of Minnesota, and the Washington Center for Equitable Growth. In October 2017, a West Virginian middle school teacher named Jay O’Neal invited his fellow teachers to join a Facebook group to discuss shared grievances of low pay and cutbacks to their health insurance (Quinn 2018). Facing months of continued resistance from the legislature and governor, teachers in O’Neal’s group proposed what had previously seemed unthinkable: walking out of work. -

The Power Resources Approach: Developments and Challenges

The Power Resources Approach: Developments and Challenges Stefan Schmalz, Friedrich Schiller University, Germany Carmen Ludwig, Justus Liebig University, Germany Edward Webster, University of the Witwatersrand, South Africa Introduction Instead of dismissing labour as a product of the past, the study of labour has been revitalised over the past two decades by approaches that emphasise the ability of organised labour to act strategically. This new branch of research on trade union renewal has challenged the discourse of a general decline of organised labour, focusing instead on innovative organising strategies, new forms of participation and campaigning in both the Global North and the Global South (Turner, Katz and Hurd, 2001; Clawson, 2003; Milkman, 2006; Agarwala, 2013; Murray, 2017). The focus of these studies has not been the institutional setting of labour relations or the overall impact of major trends like globalisation on labour, but rather the strategic choice in responding to new challenges and changing contexts. In the discussion on trade union renewal, the power resources approach (PRA) has emerged as a research heuristic. The PRA is founded on the basic premise that organised labour can successfully defend its interests by collective mobilisation of power resources. This idea has significantly shaped the way scholars are dealing with the issue of union revitalisation and labour conflict, as studies from different world regions have examined union renewal as a process of utilising existing power resources while attempting to develop new ones (Von Holdt and Webster, 2008; Chun, 2009; Dörre, 2010a; McCallum, 2013; Julian, 2014; Melleiro and Steinhilber, 2016; Lehndorff, Dribbusch and Schulten, 2017; Ludwig and Webster, 2017; Xu and Schmalz, 2017).