Regional Investment Blueprint

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Federal Priorities for Western Australia April 2013 Keeping Western Australians on the Move

Federal priorities for Western Australia April 2013 Keeping Western Australians on the move. Federal priorities for Western Australia Western Australia’s rapid population growth coupled with its strongly performing economy is creating significant challenges and pressures for the State and its people. Nowhere is this more obvious than on the State’s road and public transport networks. Kununurra In March 2013 the RAC released its modelling of projected growth in motor vehicle registrations which revealed that an additional one million motorised vehicles could be on Western Australia’s roads by the end of this decade. This growth, combined with significant developments in Derby and around the Perth CBD, is placing increasing strain on an already Great Northern Hwy Broome Fitzroy Crossing over-stretched transport network. Halls Creek The continued prosperity of regional Western Australia, primarily driven by the resources sector, has highlighted that the existing Wickham roads do not support the current Dampier Port Hedland or future resources, Karratha tourism and economic growth, both in terms Exmouth of road safety and Tom Price handling increased Great Northern Highway - Coral Bay traffic volumes. Parabardoo Newman Muchea and Wubin North West Coastal Highway East Bullsbrook Minilya to Barradale The RAC, as the Perth Darwin National Highway representative of Great Eastern Mitchell Freeway extension Ellenbrook more than 750,000 Carnarvon Highway: Bilgoman Tonkin Highway Grade Separations Road Mann Street members, North West Coastal Hwy Mundaring Light Rail PERTH believes that a Denham Airport Rail Link strong argument Goldfields Hwy Fremantle exists for Western Australia to receive Tonkin Highway an increased share Kalbarri Leinster Extension of Federal funding Kwinana 0 20 Rockingham Kilometres for road and public Geraldton transport projects. -

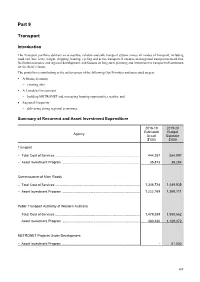

2019-20 Budget Statements Part 9 Transport

Part 9 Transport Introduction The Transport portfolio delivers an accessible, reliable and safe transport system across all modes of transport, including road, rail, bus, ferry, freight, shipping, boating, cycling and active transport. It ensures an integrated transport network that facilitates economic and regional development, and focuses on long-term planning and investment in transport infrastructure for the State’s future. The portfolio is contributing to the achievement of the following Our Priorities and associated targets: • A Strong Economy − creating jobs; • A Liveable Environment − building METRONET and increasing housing opportunities nearby; and • Regional Prosperity − delivering strong regional economies. Summary of Recurrent and Asset Investment Expenditure 2018-19 2019-20 Estimated Budget Agency Actual Estimate $’000 $’000 Transport − Total Cost of Services ........................................................................................... 444,257 554,997 − Asset Investment Program .................................................................................... 35,873 38,284 Commissioner of Main Roads − Total Cost of Services ........................................................................................... 1,346,728 1,489,935 − Asset Investment Program .................................................................................... 1,222,169 1,265,111 Public Transport Authority of Western Australia − Total Cost of Services .......................................................................................... -

Early Voting Centres Now Open

State General Election Saturday 13 March 2021. Early Voting Centres Now Open List of early voting centres as of 29 January 2021. Standard hours of operation for most early voting centres are 8 am - 6 pm Wednesday 24 Feburary to Friday 26 February; Tuesday 2 March - Saturday 6 March and Monday 8 March - Friday 12 March 2021. Hours for some Early Voting Centre locations such as court houses and libraries may vary. Robert Kennedy Wheelchair Access A Accessiblity Equipment Available Vote Assist Electoral Commissioner North Metropolitan Region VICTORIA PARK A Agricultural Region • VisAbility Centre, Handa Hall (within Perron Place), PERTH CBD ESPERANCE 61 Kitchener Ave - 8am to 6pm • 150 St Georges Terrace - 8am to 6pm A • Esperance Courthouse, 100 Dempster Street • Suite G06, 256 Adelaide Terracce (Septimus Roe WILLETTON A Mon - Fri 9.00am - 4.00pm • Unit 2, 179 - 181 High Road - 8am to 6pm Square) - 8am to 6pm GERALDTON A • St Georges Terrace Post Shop, East Metropolitan Region • Shop 1, 89 Durlacher Street - 8am to 6pm 66 St Georges Terrace Mon - Fri 8am to 5pm ARMADALE KATANNING (Only Limited Issue Points) • Unit 2, 36 - 40 Commerce Avenue - 8am to 6pm • Katanning Library, 16-24 Austral Terrace • Cloisters Square Post Shop, Shop 17 BAYSWATER A Mon, Tue, Thu, Fri 10.00am - 5.00pm, Wed 1.00pm - 5.00pm 200 St Georges Terrace (Enter at 863 Hay St, Perth) • Tenancy 2, 68 Beechboro Road South - - Mon - Fri 9am to 5pm (Only Limited Issue Points) 8am to 6pm MERREDIN • Merredin Community Resource Centre, BUTLER A BELMONT 108 Barrack Street - Mon -

RAC Risky Roads Survey Results 2016/17

RAC Risky Roads Survey results 2016/17 Risky Roads is WA's largest road infrastructure survey which asks the community to nominate dangerous roads and intersections around the State. The 2016 survey received over 6,000 nominations. These are the top 10 roads and intersections nominated in metropolitan and regional WA. For information on all Risky Roads campaigns visit riskyroads.com.au For more information, please contact [email protected] State-wide Top ten intersections Rank Intersection Issues 1 Forrest Highway (Australind Bypass) X Hynes Road, Speed of vehicles too high. Inadequate crossing or turning Eaton opportunity. Inadequate traffic light system. 2 Denny Avenue X Streich Avenue, Kelmscott Confusing road or intersection layout. Inadequate traffic light system. Inadequate crossing or turning opportunity. 3 Denny Avenue X Railway Avenue, Kelmscott Confusing road or intersection layout. Inadequate traffic light system. Inadequate crossing or turning opportunity. 4 Edgewater Drive X Ocean Reef Road, Edgewater Inadequate crossing or turning opportunity. Inadequate traffic light system. Speed of vehicles too high. 5 Green Street X Scarborough Beach Road, Mount Confusing road or intersection layout. Inadequate crossing or turning Hawthorn opportunity. Inadequate traffic light system. 6 Albany Highway X S Coast Highway, Orana (Albany) Confusing road or intersection layout. Inadequate crossing or turning Includes Chester Pass X Hanrahan X North Road X Albany Highway roundabout. opportunity. Inadequate traffic light system. 7 Garden Street X Nicholson Road X Yale Road, Confusing road or intersection layout. Inadequate crossing or turning Canning Vale roundabout opportunity. 8 Beaufort Street X Walcott Street , Mount Lawley Inadequate traffic light system. Inadequate crossing or turning opportunity. -

RAC Risky Roads Survey Results 2018/19

RAC Risky Roads Survey results 2018/19 Risky Roads is WA's largest road infrastructure survey which asks the community to nominate dangerous roads and intersections around the State. The 2018 survey received over 6,000 nominations. These are the top 10 roads and intersections nominated in metropolitan and regional WA. For more information, please contact [email protected] Metropolitan Perth Top ten risky roads Rank Road Issues 1 Keirnan Street, Mundijong Poor/no pedestrian access/footpath. Unsafe or poor pedestrian crossing. Poor road surface quality 2 Kwinana Freeway & Canning Highway interchange, Little chance to turn/cross traffic. Lacks median strip/traffic separation. Como Confusing layout 3 Armadale Road, Cockburn to Armadale* Little chance to turn/cross traffic. Area requires lights/roundabout. Vehicles travel over the speed limit 4 Denny Avenue, Kelmscott* Poorly timed traffic light system. Little chance to turn/cross traffic. Confusing layout 5 North Lake Road (South Street to Cockburn Central), Little chance to turn/cross traffic. Area requires lights/roundabout. Kardinya – Cockburn Central Poorly timed traffic light system 6 Albany Highway, Bentley - Cannington Little chance to turn/cross traffic. Area requires lights/roundabout. Poorly timed traffic light system 7 Thomas Road (Tonkin Highway to Kwinana Freeway), Little chance to turn/cross traffic. Narrow road, lanes or bridges. Area Oakford requires lights/roundabout 8 Beaufort Street, Mt Lawley - Inglewood Little chance to turn/cross traffic. Area requires lights/roundabout. Vehicles travel over the speed limit 9 Hartman Drive, Darch Little chance to turn/cross traffic. Area requires lights/roundabout. Lacks median strip/traffic separation 10 (a) Abernethy Road (Warrington Road to South Western Little chance to turn/cross traffic. -

WHEATBELT SNAPSHOT SERIES: LAND BASED TRANSPORT Version 2 July 2014

WHEATBELT SNAPSHOT SERIES: LAND BASED TRANSPORT Version 2 July 2014 PURPOSE OF DOCUMENT This document summarises the Wheatbelt Development Commission’s (WDC) understanding of transport infrastructure issues in the Wheatbelt. It highlights strategic issues for the region and proposes solutions to these problems. It is a working document, and stakeholders are encouraged to contact the WDC if they identify any errors. FACTS The Wheatbelt contains major interregional and interstate transport linkages such as the Great Northern Highway, Great Eastern Highway, Great Southern Highway, Brand Highway and the Albany Highway; and the East West Rail link. There is 45,069km(1) of road in the Wheatbelt servicing a mix of local, tourist and freight traffic (see Appendix 1 for details). An integrated land transport network is a vital aspect of the Wheatbelt economy. Sustainable, effective and efficient transport networks are critical to foster commercial enterprise and safe domestic use. Figure 1: Wheatbelt Region (WDC 2012) Version: 01 – Revision Due 30/06/2014 1 (1) (2) Main Roads, Regional Digest 2011-2012. Strategic Grain Freight Network Committee Report, 2009. KEY TRANSPORT ISSUES and expand industry opportunity in the Wheatbelt, particularly in relation to transport logistics. The Outer Ring Perth to Darwin National Highway (PDNH) (Great Road will reduce the requirement for heavy freight to Northern Highway) traverse the metropolitan area and will also connect to the larger scale Portlink proposal. The scale, stakeholders and The National Land Transport Network forms the backbone of nature of the project makes the development of a single passenger and freight transport in Australia, with the PDNH business case particularly complex, but it can be broken into linking Perth with Northern Western Australia. -

Southern River/Forrestdale/ Brookdale/Wungong D ISTRICT S TRUCTURE P LAN

JANUARY 2001 Southern River/Forrestdale/ Brookdale/Wungong D ISTRICT S TRUCTURE P LAN VERNM O EN G T E O H F T W A E I S L T A E R RN AUST Dlsclaimer Any representation, statement, opinion or advice, expressed or implied in this publication is made in good faith but on the basis that the Ministry for Planning, its agents and employees are not liable (whether by reason of negligence, lack of care or otherwise) to any person from any damage or loss whatsoever which has occurred or may occur in relation to that person taking or not taking (as the case may be) action in respect of any representation, statement, or advice referred to in this document. Professional advice should be obtained before applying the information contained in this document to particular circumstances. © State of Western Australia Published by the Western Australian Planning Commission Albert Facey House 469 Wellington Street Perth, Western Australia 6000 Published January 2001 ISBN 0 7309 9258 6 Internet: http://www.wa.gov.au/planning E-mail: [email protected] Tel: (08) 9264 7777 Fax: (08) 9264 7566 TTY: (08) 9264 7535 Infoline: 1800 626 477 Copies of this document are available in alternative formats on application to the Disabilities Services Coordinator The Ministry for Planning owns all photography in this document unless otherwise stated. SOUTHERN RIVER/FORRESTDALE/BROOKDALE/WUNGONG DISTRICT STRUCTURE PLAN Foreword The Southern River, Forrestdale, Brookdale, Wungong area is complex to plan for future development. It is affected by issues such as a high water table, contaminated sites, uses which have offsite impacts such as poultry farms and kennels, major infrastructure installations such as power lines, gas and water mains, important conservation and environmental sites and land fragmentation. -

SAT JPS Template Ver

[2016] WASAT 22 JURISDICTION : STATE ADMINISTRATIVE TRIBUNAL ACT : PLANNING AND DEVELOPMENT ACT 2005 (WA) CITATION : SITA AUSTRALIA PTY LTD and WHEATBELT JOINT DEVELOPMENT ASSESSMENT PANEL [2016] WASAT 22 MEMBER : MR P McNAB (SENIOR MEMBER) MR J JORDAN (SENIOR SESSIONAL MEMBER) DR A HINWOOD (SESSIONAL MEMBER) HEARD : 18 AND 19 NOVEMBER 2015 DELIVERED : 8 MARCH 2016 FILE NO/S : SAT 127 of 2014 BETWEEN : SITA AUSTRALIA PTY LTD Applicant AND WHEATBELT JOINT DEVELOPMENT ASSESSMENT PANEL Respondent Catchwords: Town planning - Development application - Proposed waste landfill development in rural area - 'Putrescible landfill' - Amended proposal under review - Significant regulation of facility by Department of Environment Regulation (DER) - DER indicating works approval would be given on extensive conditions - Land use classification - Whether proposal 'noxious industry' - Permissible land use under Town Planning Scheme - Significant agreement by all environmental experts on groundwater and hydrological issues Page 1 [2016] WASAT 22 indicating no environmental threat - Significant agreement on planning and local amenity issues indicating approval warranted - Whether approval should be given - Whether approval should be given in the absence of strategic planning for wider regional area including site - Conditional approval given by Tribunal - Appropriate conditions to regulate facility - Observations on duplication and overlapping of planning with other conditions - Role of Shire in formulating conditions • Words and phrases: 'noxious industry' -

Wheatbelt Regional Planning and Infrastructure Framework Part B: Regional Infrastructure Planning

Wheatbelt Regional Planning and Infrastructure Framework Part B Framework Regional Planning and Infrastructure Wheatbelt Regional Planning and Infrastructure Framework Part B: Regional Infrastructure Planning December 2015 December 2015 Wheatbelt Regional Planning and Infrastructure Framework Part B: Regional Infrastructure Planning December 2015 Part B: Regional Infrastructure Planning Wheatbelt Regional Planning and Infrastructure Framework Disclaimer This document has been published by the Department of Planning on behalf of the Western Australian Planning Commission. Any representation, statement, opinion or advice expressed or implied in this publication is made in good faith and on the basis that the government, its employees and agents are not liable for any damage or loss whatsoever which may occur as a result of action taken or not taken, as the case may be, in respect of any representation, statement, opinion or advice referred to herein. Professional advice should be obtained before applying the information contained in this document to particular circumstances. The infrastructure projects identified in the Wheatbelt Regional Planning and Infrastructure Framework are based on existing unaudited information available from State agencies, utilities and departments. The infrastructure listed is not comprehensive and estimates of infrastructure, timeframes and costs are indicative only. Infrastructure identified is based upon the information available at the time of enquiry, and may be subject to review and change to meet new circumstances. -

A ROAD )I);- SAFETY

A ROAD �)i);- SAFETY \'), COUNCIL GOVERNMENT OF WESTERN AUSTRALIA ROAD SAFETY COUNCIL Report on Activities 2018/19 In accordance with section 13 of the Road Safety CouncilAct 2002 The Hon Michelle Roberts BA DipEd MLA Minister for Road Safety Dear Minister Road Safety Council Annual Report on Activities 2018/19 Pursuant to section 13 of the Road Safety CouncilAct 2002, the Road Safety Council submits its report on its activities for the financial year ending 30 June 2019. Yours sincerely lain Cameron MPH, BPE, Dip Ed, FACRS, GAICD Chairman Road Safety Council 2 Contents 1 Overview 2018/19 ................................................................................................ 4 2 Road Safety Council Governance ........................................................................ 5 2.1 Membership of the Road Safety Council ....................................................... 5 2.2 Conflicts of Interest ........................................................................................ 7 2.3 Meetings ............... : ........................................................................................ 7 2.4 Board and Committee Remuneration ............................................................ 7 2.5 Ministerial Directives ........................ .'............................................................. 7 3 Road Trauma Trust Account ................................................................................ 8 4 Measures to improve road safety ........................................................................ -

Descriptions of Where Regional and Other Travel Restriction Boundaries Intersect Highways and Roads for Each Region

Descriptions of where regional and other travel restriction boundaries intersect highways and roads for each region. Provided by the corresponding regional development commissions, 7 April 2020 (This list does not describe locations of roadblocks or checkpoints, which may be slightly different and are decided by WA Police.) Perth-Peel • Perth and Peel are treated as one region under the regional travel bans. The first table below covers Perth’s boundaries with regions to the north and east, while the second table covers Peel’s boundaries to the south and east. Highway Border of Perth Boundary Description (provided and – by Wheatbelt DC) Brand Highway/ Muchea Wheatbelt Heading north, 3km north of South Road Bullsbrook Great Northern Highway Wheatbelt Heading north, 8km from the RAAF Base Pearce Indian Ocean Drive Wheatbelt Heading north, 10km north of the entry to the Yanchep National Park/ Old Yanchep Road turn off Great Eastern Highway Wheatbelt Heading east, 10km north east of The Lakes BP Toodyay Road Wheatbelt Heading east, 16km east of Gidgegannup Albany Highway Wheatbelt Heading south east, 8km from Crossman Brookton Highway Wheatbelt Heading south east, 25km from Karragullen Highway/Road Border of Peel and Peel DC Boundary Description – South Western Highway South West Heading south, 4.6km past the Alcoa Wagerup turn-off (this is close to Kaus Road on the right and Boundary Road on the left) Forrest Highway South West Heading south, 1km south of the Preston Beach turn-off Brockman Road South West Heading south, 1km from the Somers Road – Bancell Road intersection Trotter Road South West Heading south, 1.7km from Somers Road intersection Monarco Road South West Heading south, the boundary is approx. -

Heritage Drive Trails of the Central Great Southern of Western Australia the “Heritage of Endeavour” Project Tourism Development in the Central Great Southern

Heritage Drive Trails of the Central Great Southern of Western Australia The “Heritage of Endeavour” project Tourism Development in the Central Great Southern Michael Hughes, PhD Jim Macbeth, PhD Tourism Research Officer Tourism Program Chair Murdoch University Murdoch University Chief Investigator and Project Manager Jim Macbeth Tourism Program School of Social Sciences and Humanities Murdoch University South Street MURDOCH, Western Australia 6150 Email: [email protected] Website: <tourism.Murdoch.edu.au> © Jim Macbeth Printed and published by Murdoch University 2005 Cover photo by Michael Hughes Entry statement near Woodanilling, on the northwestern edge of the Central Great Southern Project Area ii Heritage Drive Trails of the Central Great Southern of Western Australia Table of Contents Executive Summary ....................................................................................................................... 1 Recommended Tourism Developments ....................................................................................... 2 Drive Trails................................................................................................................................. 4 Conclusion.................................................................................................................................. 4 Recommended Tourism Drive Trails and Attractions Descriptions ............................................... 6 Tourism Drive Trail Runs ..........................................................................................................