— Automotive in Transition Challenges for Strategy and Policy Edited by Andrea Stocchetti, Giulia Trombini, Francesco Zirpoli

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

La Storia Del Logo Fiat

La storia del logo Fiat Fiat Automobiles Nazione Italia Tipologia Società per azioni Fondazione 1899 a Torino Sede principale Torino Gruppo Fiat SpA (tramite Fiat Group Automobiles) Persone chiave Olivier François, Direttore operativo Settore Metalmeccanica (Autoveicoli) Prodotti autovetture Slogan Life is best when driven Sito web www.fiat.it La FIAT (nata come acronimo di Fabbrica Italiana Automobili Torino), nota come Fiat Automobiles negli Stati Uniti, è stata fondata l'11 luglio 1899 a Torino come casa produttrice di automobili, per poi sviluppare la propria attività in numerosi altri settori, dando vita al più importante gruppo finanziario e industriale privato italiano. Dal 1º febbraio 2007 fa parte, insieme ai marchi Alfa Romeo, Lancia, Abarth e Fiat Professional, di Fiat Group Automobiles (abbreviato in FGA) che rappresenta una delle diramazioni del gruppo industriale Fiat SpA. Storia e direzione aziendale L'azienda nacque dalla comune volontà di una decina tra aristocratici, possidenti, imprenditori e professionisti torinesi di impiantare una fabbrica per la produzione di automobili. L'idea di produrre automobili su scala industriale era venuta agli amici Emanuele Cacherano di Bricherasio e Cesare Goria Gatti (già fondatori dell'ACI Automobile Club d'Italia) che avevano precedentemente costituito e finanziato la "Accomandita Ceirano & C.", finalizzata alla costruzione della "Welleyes", un'automobile progettata dall'ing. Aristide Faccioli e costruita artigianalmente da Giovanni Battista Ceirano. Visto il successo ottenuto dalla "Welleyes" alla sua presentazione, Bricherasio e Gatti proposero ad un gruppo di conoscenti di acquisire le esperienze, le maestranze e la competenza della "Accomandita Ceirano & C." per trasferirle su scala industriale, come già avveniva nella fabbriche dell'Europa settentrionale. -

The Automotive Industry in Hungary 217 Andras Tóth and László Neumann 1

uaderni della QFondazione G. Brodolini 45 I Quaderni della Fondazione Giacomo Brodolini presentano i risultati dell’attività di ricerca svolta dalla Fondazione nelle aree che, nel tempo, hanno costituito gli assi fon- damentali delle sue iniziative culturali, occupazione, sviluppo locale, valutazione delle politiche pubbliche, politiche sociali, pari opportunità, storia. Fondazione Giacomo Brodolini 00161 Roma - Via di Villa Massimo 21, int. 3 tel. 0644249625 fax 0644249565 [email protected] www.fondazionebrodolini.it ISBN 978-88-95380-05-6 THE LABOUR IMPACT OF GLOBALIZATION IN THE AUTOMOTIVE INDUSTRY A comparison of the Italian, German, Spanish, and Hungarian Motor Industries edited by Paolo Caputo and Elisabetta Della Corte FondazioneGiacomoBrodolini Index Contributors 9 Introduction 11 Paolo Caputo and Elisabetta Della Corte Labour on the Defensive? The Global Reorganisation of the Value Chain and Industrial Relations in the European Motor Industry 17 Josep Banyuls and Thomas Haipeter 1. Introduction 17 2. Global reorganisation in the motor industry 19 2.1 From internationalisation to globalisation 20 2.2 Internal reorganisation in OEMs 24 2.3 Reorganisation of the value chain 28 3. Confronting the pressures of globalisation: industrial relations systems in flux? 35 3.1 New collective bargaining topics 35 3.2 Collective bargaining in regime competition: between centralisation and decentralisation 39 3.3 Changing actors and strategies 42 3.4 Collective bargaining along the value chain: towards a fragmentation of industrial relations? 46 3.5 Internationalisation of industrial relations 49 4. Conclusion: convergences, divergences and the defensive of work 51 References 56 5 The Automotive Industry in Germany 61 Thomas Haipeter 1. Introduction: Developments of the automotive industry and challenges for the systems of industrial relations 61 2. -

Final Frm Map.Qxd

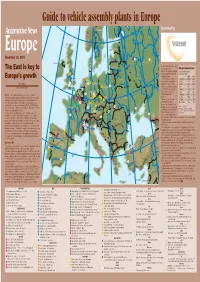

Guide to vehicle assembly plants in Europe NORWAY SWEDEN Sponsored by 33 16 ESTONIA 12 9 November 29, 2004 11 9 LATVIA 18 1 RUSSIA IRELAND DENMARK 21 greater worker flexibility and local U. K. LITHUANIA The East is key to sales growth, says Europe’s top producers 4 35 Felix Kuhnert, an auto consultant Vehicle assembly capacity, 12 for PricewaterhouseCoopers in 7 10 in thousands of units 12 14 7 29 southern Germany. 2004 2009 Europe’s growth “But being present in these 1. Germany 6,190 6,398 9 16 12 1 BELARUS 8 1 markets and the possibility to 2. France 4,356 4,500 7 6 2 7 JESSE SNYDER 5 10 4 export from there is another 3. Spain 3,329 3,318 14 4 NETH. 15 1 14 5 driver,” he said. “However, if you 4. UK 2,632 2,613 AUTOMOTIVE NEWS EUROPE 3 POLAND 6 19 look at the EU capacity trends 5. Russia 1,874 2,113 9 13 13 4 GERMANY through 2007 you also see 6. Italy 1,803 1,802 5 1 11 2 25 significant expansion in 7. Belgium 1,133 1,222 MUNICH – The manufacturing movement to the East continues. 2 5 BELGIUM 5 3 18 8 Germany.” 8. Turkey 1,003 1,105 New and expanded plants in eastern Europe have driven total vehicle 6 3 3 3 17 8 UKRAINE assembly capacity in greater Europe above 26 million units a year. 2 5 LUX. 19 Helped by the 2005 opening of 9. Poland 847 654 6 4 In central and eastern Europe, manufacturers are rapidly adding 31 1 7 CZECH a BMW plant in Leipzig, 10.Czech Rep. -

Slide Del Seminario Dott. Giampietro Varrasso

CLEA Alumni Welcome Back Giampietro Varrasso Pescara, 06 Giugno 2020 Agenda Seminario 06/06/2020 L'università e il post laurea Accenni di storia: da FIAT a FCA FCA in numeri FCA Services: «Shared Services Center» Il mio percorso in FCA Q&A ~ 2 ore 2 Dalla provincia ad un contesto internazionale In cerca di fortuna Post- Laurea a Melbourne, Australia. Fruttivendolo, Fabbrica di bevande 2012 Corso intensivo di Inglese, tramite Ud’A, 2010 @Nazareth College, Rochester, N.Y. 2007 Ritorno in Italia ad Aprile. Ripetizioni di diritto/ economia. Colloqui a Pescara e poi Torino. 2006 Visite Mediche in FIAT a Giugno Erasmus @ BBS «Budapest Business School» da 2002 Settembre 2007 a Luglio 2008. Lavoro come barista Primo Lavoro: 2000 «Carpentiere del Diploma al liceo metallo» c/o Impianto scientifico di Popoli (PE) chimico Bussi sul Tirino e Iscrizione al CLEA durante i mesi estivi 1983-1999: Hic Sunt Leones 3 Dalla fondazione all’era moderna Year 1899 11 Luglio nasce la «Società Anonima Fabbrica Italiana di Automobili» ad opera del conte di Bricherasio e dell’avv. Gatti, già fondatori dell’ACI e del senatore Giovanni Agnelli Inizio dei lavori per la creazione della Fabbrica del Lingotto, completati nel 1923. 1916 Oltre alle automobili, la società inizia la produzione di mezzi di navigazione, camion, trattori e motori per aeroplani 1939 Inaugurata la fabbrica di Mirafiori 1957 Viene presentata la «Nuova 500» 1966 L’avvocato Gianni Agnelli diventa amministratore delegato 1969 La FIAT acquisisce i marchi Autobianchi, Lancia. Inizia partecipazione paritetica in Ferrari 1986 Acquisizione di Alfa Romeo 1993 Maserati entra a far parte del gruppo FIAT 2000 Inizio della crisi, si arrivano a perdere 5 mln di Euro al giorno. -

Europe Swings Toward Suvs, Minivans Fragmenting Market Sedans and Station Wagons – Fell Automakers Did Slightly Better Than Cent

AN.040209.18&19.qxd 06.02.2004 13:25 Uhr Page 18 ◆ 18 AUTOMOTIVE NEWS EUROPE FEBRUARY 9, 2004 ◆ MARKET ANALYSIS BY SEGMENT Europe swings toward SUVs, minivans Fragmenting market sedans and station wagons – fell automakers did slightly better than cent. The only new product in an cent because of declining sales for 656,000 units or 5.5 percent. mass-market automakers. Volume otherwise aging arena, the Fiat the Honda HR-V and Mitsubishi favors the non-typical But automakers boosted sales of brands lost close to 2 percent of vol- Panda, was on sale for only four Pajero Pinin. over familiar sedans unconventional vehicles – coupes, ume last year, compared to 0.9 per- months of the year. In terms of brands leading the roadsters, minivans, sport-utility cent for luxury marques. European buyers seem to pro- most segments, Renault is the win- LUCA CIFERRI vehicles exotic cars and multi- Traditional European-brand gressively walk away from large ner with four. Its Twingo leads the spaces such as the Citroen Berlingo automakers dominate the tradi- sedans, down 20.3 percent for the minicar segment, but Renault also AUTOMOTIVE NEWS EUROPE – by 16.8 percent last year to nearly tional car, minivan and premium volume makers and off 11.1 percent leads three other segments that it 3 million units. segments, but Asian brands control in the upper-premium segment. created: compact minivan, Scenic; TURIN – Automakers sold 428,000 These non-traditional vehicle cat- virtually all the top spots in small, large minivan, Espace; and multi- more specialty vehicles last year in egories, some of which barely compact and large SUV segments. -

Small Suvs, Minicars Make Big Gains in 2006 the Renault Megane CC (Shown) Ended Peugeot’S 5-Year Reign at the Top of Luca Ciferri the Fastest-Growing Segment

AN_070402_18&19good.qxd 13.04.2007 8:58 Uhr Page 18 PAGE 18 · www.autonewseurope.com April 2, 2007 Market analysis by segment, European sales ROADSTER & CONVERTIBLE Small SUVs, minicars make big gains in 2006 The Renault Megane CC (shown) ended Peugeot’s 5-year reign at the top of Luca Ciferri the fastest-growing segment. Changing segments the roadster and convertible seg- Automotive News Europe Minicars, the No. 3 segment last year in ment. Peugeot’s 307 CC was No. 1 in terms of growth, increased 22.1 percent to Europe’s 2006 winners and losers 2004; the 206 CC led the other years. Rising fuel costs, growing concerns about 992,227 units thanks largely to strong Small SUV +63.6 2006 2005 % Change Seg. share % CO2 and a flurry of new products sparked sales of three cars built at Toyota and Upper premium +26.4 Renault Megane 32,344 42,514 -23.9% 13.4% a sales surge for small SUVs and minicars PSA/Peugeot-Citroen’s plant in Kolin, Minicar +22.1 Peugeot 307CC/306C 31,786 39,640 -19.8% 13.1% in Europe last year. Czech Republic. Peugeot 206 CC 29,833 43,518 -31.4% 12.3% The arrival of three new small SUVs Europe’s largest segment, small cars, Small minivan -13.6 VW Eos 21,759 59 – 9.0% helped the segment grow 63.6 percent to rose 7.0 percent to 3,811,009 units. The Premium roadster & convertible -10.9 Opel/Vauxhall Tigra TwinTop 20,406 32,633 -37.5% 8.4% 94,153 units in 2006, according to UK- second-biggest segment – lower-medium Lower medium -8.2 Mazda MX-5 19,288 9,782 97.2% 8.0% based market researcher JATO Dynamics. -

Lancia A112 1978 - 1986

LANCIA A112 1978 - 1986 AER3900 AER3900 AFT3474 AFT3474 AFA2583 AFA2583 Ruitai Description Position Years AER3900 RACK END R/L 1969-2015 AFT3474 TIE ROD END R/L 1969-2015 AFA2583 CONTROL ARM LOW R/L 1969-1996 Ruitai Page 1/65 2018-07-19 LANCIA BETA 1978 - 1986 AER3900 AER3900 AFT3474 AFT3474 AFA2583 AFA2583 Ruitai Description Position Years AER3900 RACK END R/L 1969-2015 AFT3474 TIE ROD END R/L 1969-2015 AFA2583 CONTROL ARM LOW R/L 1969-1996 Ruitai Page 2/65 2018-07-19 LANCIA BETA 1973 - 1982 AFT4442 AFT4442 Ruitai Description Position Years AFT4442 TIE ROD END OUT R/L 1957-2000 Ruitai Page 3/65 2018-07-19 LANCIA BETA COUPE 1973 - 1984 AFT4442 AFT4442 Ruitai Description Position Years AFT4442 TIE ROD END OUT R/L 1957-2000 Ruitai Page 4/65 2018-07-19 LANCIA BETA SPIDER 1973 - 1986 AFT4442 AFT4442 Ruitai Description Position Years AFT4442 TIE ROD END OUT R/L 1957-2000 Ruitai Page 5/65 2018-07-19 LANCIA DEDRA 1973 - 1986 AFT4442 AFT4442 Ruitai Description Position Years AFT4442 TIE ROD END OUT R/L 1957-2000 Ruitai Page 6/65 2018-07-19 LANCIA DEDRA 1989 - 1999 AER3901 AFR3921 AFR4857 AFR4857 AFR3921 AER3901 AFT2189 AFT2188 AEA2590 AEA2598 AFA2594 AFA2593 AEA2597 AEA2589 AEX2648 AFX2596 AFX2595 AEX2648 AFL2486 AFL3930 AFL3930 AFL2486 Ruitai Description Position Years AER3901 RACK END R/L 1974-2015 AFR3921 RACK END R/L 1984-2006 AFR4857 RACK END R/L 1989-2016 AFT2188 TIE ROD END OUT R 1987-2015 AFT2189 TIE ROD END OUT L 1987-2015 AEA2589 CONTROL ARM LOW R 1989-2015 AEA2597 CONTROL ARM LOW R 1987-2003 AFA2593 CONTROL ARM LOW R 1987-1999 AEA2590 -

林肯系列 Lexus Lincoln 工厂号码 原厂号码 适用车型 产品尺寸 参考号码 工厂号码 原厂号码 适用车型 产品尺寸 参考号码 Item No

雷克萨斯系列 林肯系列 LEXUS LINCOLN 工厂号码 原厂号码 适用车型 产品尺寸 参考号码 工厂号码 原厂号码 适用车型 产品尺寸 参考号码 ITEM NO. OEM NO. Application Dimension(L*W*H) Brand NO. ITEM NO. OEM NO. Application Dimension(L*W*H) Brand NO. 88880-33040 88880-33060 R R 东莞市九合滤清器有限公司 东莞市九合滤清器有限公司 DONGGUAN LAST&LONG FILTER CO.,LTD JH-CF10207 88880-33010 LEXUS ES 300 252/262*139*19 TC-1004 DONGGUAN LAST&LONG FILTER CO.,LTD JH-CF10307 90612091-2 LINCOLN MKT3.5L 224*188*24 CF12307 88880-33070 J1342031 88880-33020 R R LINCOLN MKZ 2.5L , 东莞市九合滤清器有限公司 东莞市九合滤清器有限公司 DONGGUAN LAST&LONG FILTER CO.,LTD JH-CF10208 88880-30040 LEXUS GS 300 205*117*20 4531003 DONGGUAN LAST&LONG FILTER CO.,LTD JH-CF10308 AE5Z19N619A ELECTRIC/GAS 3.5L, 210*265*21/38 CF11174 J1342032 MERCURY 24367 MILAN 2.5L, R R 东莞市九合滤清器有限公司 东莞市九合滤清器有限公司 DONGGUAN LAST&LONG FILTER CO.,LTD JH-CF10209 88508-30110 LEXUS LS 298/276*220*62 CA-11960 DONGGUAN LAST&LONG FILTER CO.,LTD JH-CF10309 AE9Z19N619A LINCOLN MKT 2.0L, 218*178*22 CF11176 (UCF30) 430 ADT32521 MKS 3.5L 林肯系列 蓝旗亚系列 LINCOLN LANCIA R R 东莞市九合滤清器有限公司 东莞市九合滤清器有限公司 60812597 CF5823 DONGGUAN LAST&LONG FILTER CO.,LTD JH-CF10301 89031231 LINCOLN 250*182*43 CFA10613 DONGGUAN LAST&LONG FILTER CO.,LTD JH-CF10401 71712595 LANCIA DEDRA 385*170*17 E1921LI XR849205 LS 3.0L V6, PCK8227 60810570 SW 1.6,1.8,1.9,2.0 CU3942 2R8H18D483AA 3.9 V8 LAK250 46409630 WP6866 DCF044K R F50Y19N619A R 东莞市九合滤清器有限公司 东莞市九合滤清器有限公司 CUK2951 DONGGUAN LAST&LONG FILTER CO.,LTD JH-CF10302 F50Z19N619BA LINCOLN 260*126*29 CF105 DONGGUAN LAST&LONG FILTER CO.,LTD JH-CF10402 60653641 LANCIA LYBRA, 288*160*30 E1934LC F80219N619AA -

High Fidelity

LANCIA DELTA INTEGRALE High Fidelity Ein Blick zurück in die “Fiat-Epoche“ von Lancia und die Geschichte des Delta Integrale Text: Alexander Korab Bilder: Mathias Kniepeiss und Wolfgang Buchta Der Lancia Delta Integrale kam vor etwas mehr als 30 Jahren auf den Markt und ist somit ein frischgebackener Oldtimer. Der Name “Integrale“ ist heute zum Mythos ge- worden. In den 80er Jahren, als der Auflösungs- prozess der UdSSR begann, als Personal-Com- puter, Compact-Disk und Mobiltelefon die Welt eroberten, als man zu Hits von Depeche Mode, U2 oder Falco tanzte und die Berliner Mauer fiel, dominierte der Delta die Rallye-Szene wie kein anderes Fahrzeug davor und danach. Auf manchen Sonderprüfungen sind die feschen Allradler noch heute flott unterwegs, obwohl Vincenzo Lancia sie eigentlich schon ein paar Jährchen auf dem (1881-1937) Buckel haben. Um ihre Entstehungsgeschichte näher zu beleuchten, müssen wir doch ein wenig weiter ausholen. Für Fundamentalisten endet die Geschichte von Lancia in der letzten Oktoberwoche des Jahres 1969, als Fiat-Boss Gianni Agnelli die Über- nahme des 1906 gegründeten Traditionsunter- nehmens bekannt gab. Sicherlich, die berühmte “Marke der Ingenieure“ war damit so gut wie tot. Lancia wurde in den mächtigen Fiat-Kon- zern eingegliedert und Neuentwicklungen wie- sen von da an Gemeinsamkeiten mit Fiat-Mo- Gianni Lancia dellen auf. Wer jenes Kapitel der Lancia-Saga (1924-2014) etwas großzügiger betrachtete, durfte sich in den 70er, 80er und 90er Jahren aber über sensa- tionelle Siegesserien im Rallye-Sport freuen. Die Marke der Ingenieure 1937, als Fir- mengründer Vincenzo Lancia starb, galt das Unternehmen mit Sitz in Turin als Nobelmar- ke, welche besonders zuverlässige Automobile mit außergewöhnlicher Technik produzierte. -

New Product 2012 11 1Ed0

Since 1982 February 02 2013 Please visit our webpage www.mobiletron.com for detailed product information. ■ Voltage Regulator (CHARGING SYSTEM) ● VR- H2005-105 ● Replace: ● VR-V3874 ● Replace: DENSO VALEO 126000-3720 593454 593874 YM1666FP5 TOYOTA ● Alternator: 27700-31040 VALEO ● Alternator: SG9B037 SG9B038 SG9B039 DENSO 104210-8040 TOYOTA 27060-31010 Since 1982 February 02 2013 Please visit our webpage www.mobiletron.com for detailed product information. ■ MAF Sensor ( ENGINE MANAGEMENT SYSTEM ) ● MA-B 031 ● Replace: ● MA-B 033 ● Replace: B MW B MW 13621433565 13621433567 B OSC H B OSC H 0-280-217-124 0-280-217-814 ROVER MHK 000230 ● Application: B MW 540 I Saloon 210kW 1996-2003 B MW 740 I Saloon 210kW 1996-2001 B MW X5 4.4I 210kW 2000 B MW X5 4.6 255kW 2002 LANDROVER Range Rover 4.4 210kW 2002 ● MA-B 054 ● Replace: ● MA-B 056 ● Replace: B OSC H B OSC H 0-280-217-517 0-280-217-518 0-280-217-810 MERC EDES-B ENZ FAC ET 0000941048 10.1076 MERC EDES-B ENZ 1130940048 ● Application: MERC EDES-B ENZ C Class C43 AMG M113.944 1997-2000 MERC EDES-B ENZ C Class C55 AMG M113.988 2004-2008 MERC EDES-B ENZ CLK 430 ( 208.370) M113.943 1998-2002 MERC EDES-B ENZ CLK 500 ( 209.375) M113.968 2002 MERC EDES-B ENZ E Class E 430 M113.940 1997-2002 MERC EDES-B ENZ E Class E 500 M113.967 2002 MERC EDES-B ENZ E Class E55 AMG M113.980 1997-2002 MERC EDES-B ENZ E Class E55 AMG M113.990 2002-2006 MERC EDES-B ENZ G Class Cabrio G500 M113.962 1998 MERC EDES-B ENZ G Class G55 AMG M113.993 2004 MERC EDES-B ENZ R Class R500 M113.971 2006 MERC EDES-B ENZ S Class S600 M137.970 1999-2002 MERC EDES-B ENZ SL 500 M113.961 1998-2001 ● MA-B 061 ● Replace: B OSC H 0-280-218-010 ROVER MHK 100800 ● Application: LANDROVER Range Rover 4.0 1998-2002 LANDROVER Range Rover 4.6 1998-2002 LANDROVER Range Rover 4.6 46D 1994-2002 LANDROVER Rnage Rover 3.9 42D 1994-2002 Since 1982 February 02 2013 Please visit our webpage www.mobiletron.com for detailed product information. -

Karl E. Ludvigsen Papers, 1905-2011. Archival Collection 26

Karl E. Ludvigsen papers, 1905-2011. Archival Collection 26 Karl E. Ludvigsen papers, 1905-2011. Archival Collection 26 Miles Collier Collections Page 1 of 203 Karl E. Ludvigsen papers, 1905-2011. Archival Collection 26 Title: Karl E. Ludvigsen papers, 1905-2011. Creator: Ludvigsen, Karl E. Call Number: Archival Collection 26 Quantity: 931 cubic feet (514 flat archival boxes, 98 clamshell boxes, 29 filing cabinets, 18 record center cartons, 15 glass plate boxes, 8 oversize boxes). Abstract: The Karl E. Ludvigsen papers 1905-2011 contain his extensive research files, photographs, and prints on a wide variety of automotive topics. The papers reflect the complexity and breadth of Ludvigsen’s work as an author, researcher, and consultant. Approximately 70,000 of his photographic negatives have been digitized and are available on the Revs Digital Library. Thousands of undigitized prints in several series are also available but the copyright of the prints is unclear for many of the images. Ludvigsen’s research files are divided into two series: Subjects and Marques, each focusing on technical aspects, and were clipped or copied from newspapers, trade publications, and manufacturer’s literature, but there are occasional blueprints and photographs. Some of the files include Ludvigsen’s consulting research and the records of his Ludvigsen Library. Scope and Content Note: The Karl E. Ludvigsen papers are organized into eight series. The series largely reflects Ludvigsen’s original filing structure for paper and photographic materials. Series 1. Subject Files [11 filing cabinets and 18 record center cartons] The Subject Files contain documents compiled by Ludvigsen on a wide variety of automotive topics, and are in general alphabetical order. -

FIAT and ABARTH TRICKS by Greg Schmidt

Fiat & ABARTH tricks by GREG SCHMIDT FIAT and ABARTH TRICKS by Greg Schmidt Copyright 1984 Greg Schmidt Revised 5th produced by Greg Schmidt with thanks to: Adrienne, Trudi, June, and Roy for production support; to Maurice Dhoore for "investigation"; to Chris Butler for the cover page; and Doc Sekito for "Good vibrations". Revised second printing October 1984 with updated pages reformated and printed on a daisywheel printer by Kennerley C. Ashley, D.D.S and bis Radio Shack Model Four computer. Enthusiasts will also want a copy of ABARTH by Pat Braden and Greg .Schmidt, 160 pages, with 220 illustrations, Osprey Publishing Ltd., England 1983. ABARTH is distributed in the USA by Classic Motorbooks (see above & use order #F770A). ABARTH was reviewed in the September 184 issue of Road & Track Magazine on page 28. Note that about 80% of engine rebuilding, conversions & part numbers are contained in ABARTH. From time to time, new/revised materials are produced for this book. If you would like updated pages forwarded to you, please send a pest card with your name, address, and the number of the book that you have (noted in red on page 1) to: FlAT and ABARTH TRlCKS 1512 E. 5th Street #94 Ontario, Calif. 91764 USA (There is no charge for this service) 1 FIAT & ABARTH Tricks l hope the information contained in this book will prove valuable to you. New material, corrections and comments are always welcome. Questions and new materials will be accepted when accompanied by a self-addressed and stamped return envelope. "MORE ABARTH TRICKS" may be forthcoming (see page 82).