Report No. TO-305B Public Disclosure Authorized

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Murrumbidgee Regional Fact Sheet

Murrumbidgee region Overview The Murrumbidgee region is home The river and national parks provide to about 550,000 people and covers ideal spots for swimming, fishing, 84,000 km2 – 8% of the Murray– bushwalking, camping and bird Darling Basin. watching. Dryland cropping, grazing and The Murrumbidgee River provides irrigated agriculture are important a critical water supply to several industries, with 42% of NSW grapes regional centres and towns including and 50% of Australia’s rice grown in Canberra, Gundagai, Wagga Wagga, the region. Narrandera, Leeton, Griffith, Hay and Balranald. The region’s villages Chicken production employs such as Goolgowi, Merriwagga and 350 people in the area, aquaculture Carrathool use aquifers and deep allows the production of Murray bores as their potable supply. cod and cotton has also been grown since 2010. Image: Murrumbidgee River at Wagga Wagga, NSW Carnarvon N.P. r e v i r e R iv e R v i o g N re r r e a v i W R o l g n Augathella a L r e v i R d r a W Chesterton Range N.P. Charleville Mitchell Morven Roma Cheepie Miles River Chinchilla amine Cond Condamine k e e r r ve C i R l M e a nn a h lo Dalby c r a Surat a B e n e o B a Wyandra R Tara i v e r QUEENSLAND Brisbane Toowoomba Moonie Thrushton er National e Riv ooni Park M k Beardmore Reservoir Millmerran e r e ve r i R C ir e e St George W n i Allora b e Bollon N r e Jack Taylor Weir iv R Cunnamulla e n n N lo k a e B Warwick e r C Inglewood a l a l l a g n u Coolmunda Reservoir M N acintyre River Goondiwindi 25 Dirranbandi M Stanthorpe 0 50 Currawinya N.P. -

Riverina Skilled Migration Information for Regional Employers

Riverina Skilled Migration Information for Regional Employers Can I employ a skilled migrant? Assistance is available for Regional employers who wish to sponsor overseas skilled people to fill vacant positions within their business. To be eligible the following conditions must be met: • The employer is willing to sponsor the applicant to come to the region • The employer has been unsuccessful in their attempts to fill the position using the local labour market • The position is full-time and requires at least diploma/trade level qualifications • The terms and conditions of employment are in line with the Market Salary Rate Regional Development Australia (RDA) Riverina can assist you with this process as the Regional Certifying Body for the Riverina region (encompassing the 15 LGA’s of Bland (West Wyalong), Carrathool, Hay, Cootamundra Gundagai, Junee, Griffith, Leeton, Murrumbidgee, Narrandera, Temora, Wagga Wagga, Snowy Valeys (Tumut, Tumbarumba), Lockhart and Coolamon). What sponsorship options do I have? There are two alternatives for regional employer sponsorship: • Skilled Employer Sponsored Regional (Provisional) visa (subclass 494) – This requires a commitment of at least 3 years by the employer and employee. The skilled migrant may apply for permanent residency after meeting the 3 year requirements – Skilled Regional visa (subclass 191) which commences on 16 November 2022. • Temporary Skill Shortage visa (subclass 482 Short or Medium Term) – This is available for a contract employment period of up to 2 or 4 years. The skilled migrant is given temporary residence status in Australia for the duration of the employment contract. Employers can continue sponsoring the skilled migrant by submitting a new 482 or SESR subclass 494 application. -

Water Compliance Report

WATER COMPLIANCE REPORT 2018 - 2019 Water Year Water Report 2018 - 2019 1 ABOUT THIS REPORT COMPLYING WITH Since the Snowy Scheme’s completion in 1974, Snowy Hydro Limited has carefully managed the water that flows through the Scheme’s dams, tunnels, aqueducts and power stations in accordance with our OUR LICENCE water licence. This report outlines how we are managing the water that flows through the Scheme. Snowy Hydro complied with all of the requirements imposed upon the company under the Snowy Hydro operates a complex hydro-electric scheme utilising the water captured by the Scheme Snowy Water Licence during the 2018 - 19 water year, including each water release target to generate energy to meet the market’s needs, while also moving water from east to west to support relating to: irrigation districts. ● The Required Annual Release to the River Murray catchment. Each year, we have to reach certain targets for downstream and environmental water releases. Snowy ● The Required Annual Release to the Murrumbidgee River catchment. Hydro has operational flexibility day-to-day to strategically manage our generation and water releases while at the same time giving long-term security to the downstream users around annual water releases. ● Environmental releases into the Snowy River from Jindabyne Dam. In the Snowy Scheme, water releases and electricity generation are inseparably linked. ● Environmental releases into the Murrumbidgee River from Tantangara Dam. ● Environmental releases into the Goodradigbee River from Goodradigbee Aqueduct. Snowy Hydro is operated under the Snowy Water Licence, issued to us by the NSW Government. The licence has many legally-binding and enforceable obligations on the company. -

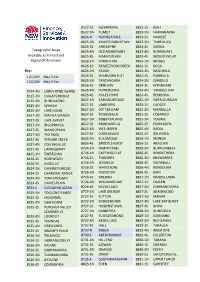

Gauging Station Index

Site Details Flow/Volume Height/Elevation NSW River Basins: Gauging Station Details Other No. of Area Data Data Site ID Sitename Cat Commence Ceased Status Owner Lat Long Datum Start Date End Date Start Date End Date Data Gaugings (km2) (Years) (Years) 1102001 Homestead Creek at Fowlers Gap C 7/08/1972 31/05/2003 Closed DWR 19.9 -31.0848 141.6974 GDA94 07/08/1972 16/12/1995 23.4 01/01/1972 01/01/1996 24 Rn 1102002 Frieslich Creek at Frieslich Dam C 21/10/1976 31/05/2003 Closed DWR 8 -31.0660 141.6690 GDA94 19/03/1977 31/05/2003 26.2 01/01/1977 01/01/2004 27 Rn 1102003 Fowlers Creek at Fowlers Gap C 13/05/1980 31/05/2003 Closed DWR 384 -31.0856 141.7131 GDA94 28/02/1992 07/12/1992 0.8 01/05/1980 01/01/1993 12.7 Basin 201: Tweed River Basin 201001 Oxley River at Eungella A 21/05/1947 Open DWR 213 -28.3537 153.2931 GDA94 03/03/1957 08/11/2010 53.7 30/12/1899 08/11/2010 110.9 Rn 388 201002 Rous River at Boat Harbour No.1 C 27/05/1947 31/07/1957 Closed DWR 124 -28.3151 153.3511 GDA94 01/05/1947 01/04/1957 9.9 48 201003 Tweed River at Braeside C 20/08/1951 31/12/1968 Closed DWR 298 -28.3960 153.3369 GDA94 01/08/1951 01/01/1969 17.4 126 201004 Tweed River at Kunghur C 14/05/1954 2/06/1982 Closed DWR 49 -28.4702 153.2547 GDA94 01/08/1954 01/07/1982 27.9 196 201005 Rous River at Boat Harbour No.3 A 3/04/1957 Open DWR 111 -28.3096 153.3360 GDA94 03/04/1957 08/11/2010 53.6 01/01/1957 01/01/2010 53 261 201006 Oxley River at Tyalgum C 5/05/1969 12/08/1982 Closed DWR 153 -28.3526 153.2245 GDA94 01/06/1969 01/09/1982 13.3 108 201007 Hopping Dick Creek -

Kosciuszko National Park Thredbo–Perisher Area Bike Trails

Photo: Thredbo Valley track (Thredbo Resort) Kosciuszko National Park Thredbo–Perisher area bike trails The Thredbo–Perisher area is one of mountain bike ride. The trail follows the old road to Australia’s premier mountain biking Mount Kosciuszko, which closed to public vehicles destinations. From leisurely cycles, to in 1976 due to safety and environmental concerns. cross-country and adrenaline trails, Pass through snow gums, heath and herb fields there’s something for everyone. and enjoy expansive views of the Main Range. Cross the Snowy River and climb the winding Plan with weather and track conditions in trail to Seamans Hut, which was built in 1929 mind. Snow can fall at any time of year, as a memorial to skiers Laurie Seaman and covering the tracks and bringing freezing Evan Hayes. conditions. Some rides can only be enjoyed when there’s no snow – check with our visitor You’ll need to leave your bike at Rawson Pass and centres before setting out. walk the 1.7km track to the summit – so carry a bike lock. The road has some steep sections but Remember to give way to walkers on all trails. the return leg is mostly downhill. Go slowly and be aware of walkers. ALPINE AREA TRAILS THREDBO AREA TRAILS When the winter snow melts, you’ll discover an ancient landscape of granite tors, glacial Ride beside cool mountain streams to lakes and summer wildflowers. historic huts, experience the thrill of a single track, downhill ride, or explore the Alpine Topographic maps Village of Thredbo. • Perisher Valley 1:25 000 • Youngal 1:25 000 Topographic -

Government Gazette of the STATE of NEW SOUTH WALES Number 52 Friday, 13 April 2007 Published Under Authority by Government Advertising

2217 Government Gazette OF THE STATE OF NEW SOUTH WALES Number 52 Friday, 13 April 2007 Published under authority by Government Advertising SPECIAL SUPPLEMENT New South Wales Shoalhaven Local Environmental Plan 1985 (Amendment No 212)—Heritage under the Environmental Planning and Assessment Act 1979 I, the Minister for Planning, make the following local environmental plan under the Environmental Planning and Assessment Act 1979. (W97/00064/PC) FRANK SARTOR, M.P., MinisterMinister forfor PlanningPlanning e03-407-09.p04 Page 1 2218 SPECIAL SUPPLEMENT 13 April 2007 Shoalhaven Local Environmental Plan 1985 (Amendment No 212)— Clause 1 Heritage Shoalhaven Local Environmental Plan 1985 (Amendment No 212)—Heritage under the Environmental Planning and Assessment Act 1979 1 Name of plan This plan is Shoalhaven Local Environmental Plan 1985 (Amendment No 212)—Heritage. 2Aims of plan This plan aims: (a) to identify and conserve the environmental heritage of the City of Shoalhaven, and (b) to conserve the heritage significance of existing significant fabric, relics, settings and views associated with the heritage significance of heritage items and heritage conservation areas, and (c) to ensure that archaeological sites and places of Aboriginal heritage significance are conserved, and (d) to ensure that the heritage conservation areas throughout the City of Shoalhaven retain their heritage significance. 3 Land to which plan applies This plan applies to all land within the City of Shoalhaven under Shoalhaven Local Environmental Plan 1985. 4 Amendment of Shoalhaven Local Environmental Plan 1985 Shoalhaven Local Environmental Plan 1985 is amended as set out in Schedule 1. Page 2 NEW SOUTH WALES GOVERNMENT GAZETTE No. -

Submission: Inquiry Into Climate Change and the Australian

September 2008 NSW Submission to the Senate Standing Committee on Rural and Regional Affairs and Transport Inquiry into water management in the Coorong and Lower Lakes NSW Water Legislation The management of the surface water and groundwater resources of NSW, including the allocation of water entitlements, is undertaken under the Water Act, 1912 and the Water Management Act 2000. The NSW Government is progressively transitioning water management from the Water Act 1912 to the Water Management Act 2000. The vast majority of water extraction in the NSW portion of the Murray-Darling Basin is covered by statutory water sharing plans under the Water Management Act 2000. The legislation and rules in the water sharing plans provide the framework for the implementation of the COAG-agreed water reforms, including: • the provision of water entitlements specifically for the environment; • the separation of water entitlements from land; and • clearly identified tradeable water entitlements. The priority for water sharing under the legislation is: Priority 1 Water for the environment and basic landholder rights (e.g. domestic and stock rights); Priority 2 Town water supply, domestic and stock and major utility licences (e.g. power generation, major urban water supply); Priority 3 High security licences (e.g. for permanent plantings); Priority 4 General security or unregulated river licences (e.g. for irrigation of annual crops); and Priority 5 Supplementary licences (e.g. to access high flows). However, in times of severe water shortage the priority of water for domestic purposes (i.e. either under a basic landholder right or licence) is elevated above the environment. -

Government Gazette No 164 of Friday 23 April 2021

GOVERNMENT GAZETTE – 4 September 2020 Government Gazette of the State of New South Wales Number 164–Electricity and Water Friday, 23 April 2021 The New South Wales Government Gazette is the permanent public record of official NSW Government notices. It also contains local council, non-government and other notices. Each notice in the Government Gazette has a unique reference number that appears in parentheses at the end of the notice and can be used as a reference for that notice (for example, (n2019-14)). The Gazette is compiled by the Parliamentary Counsel’s Office and published on the NSW legislation website (www.legislation.nsw.gov.au) under the authority of the NSW Government. The website contains a permanent archive of past Gazettes. To submit a notice for gazettal, see the Gazette page. By Authority ISSN 2201-7534 Government Printer NSW Government Gazette No 164 of 23 April 2021 DATA LOGGING AND TELEMETRY SPECIFICATIONS 2021 under the WATER MANAGEMENT (GENERAL) REGULATION 2018 I, Kaia Hodge, by delegation from the Minister administering the Water Management Act 2000, pursuant to clause 10 of Schedule 8 to the Water Management (General) Regulation 2018 (the Regulation) approve the following data logging and telemetry specifications for metering equipment. Dated this 15 day of April 2021. KAIA HODGE Executive Director, Regional Water Strategies Department of Planning, Industry and Environment By delegation Explanatory note This instrument is made under clause 10 (1) of Schedule 8 to the Regulation. The object of this instrument is to approve data logging and telemetry specifications for metering equipment that holders of water supply work approvals, water access licences and Water Act 1912 licences and entitlements that are subject to the mandatory metering equipment condition must comply with. -

Government Gazette of the STATE of NEW SOUTH WALES Number 112 Monday, 3 September 2007 Published Under Authority by Government Advertising

6835 Government Gazette OF THE STATE OF NEW SOUTH WALES Number 112 Monday, 3 September 2007 Published under authority by Government Advertising SPECIAL SUPPLEMENT EXOTIC DISEASES OF ANIMALS ACT 1991 ORDER - Section 15 Declaration of Restricted Areas – Hunter Valley and Tamworth I, IAN JAMES ROTH, Deputy Chief Veterinary Offi cer, with the powers the Minister has delegated to me under section 67 of the Exotic Diseases of Animals Act 1991 (“the Act”) and pursuant to section 15 of the Act: 1. revoke each of the orders declared under section 15 of the Act that are listed in Schedule 1 below (“the Orders”); 2. declare the area specifi ed in Schedule 2 to be a restricted area; and 3. declare that the classes of animals, animal products, fodder, fi ttings or vehicles to which this order applies are those described in Schedule 3. SCHEDULE 1 Title of Order Date of Order Declaration of Restricted Area – Moonbi 27 August 2007 Declaration of Restricted Area – Woonooka Road Moonbi 29 August 2007 Declaration of Restricted Area – Anambah 29 August 2007 Declaration of Restricted Area – Muswellbrook 29 August 2007 Declaration of Restricted Area – Aberdeen 29 August 2007 Declaration of Restricted Area – East Maitland 29 August 2007 Declaration of Restricted Area – Timbumburi 29 August 2007 Declaration of Restricted Area – McCullys Gap 30 August 2007 Declaration of Restricted Area – Bunnan 31 August 2007 Declaration of Restricted Area - Gloucester 31 August 2007 Declaration of Restricted Area – Eagleton 29 August 2007 SCHEDULE 2 The area shown in the map below and within the local government areas administered by the following councils: Cessnock City Council Dungog Shire Council Gloucester Shire Council Great Lakes Council Liverpool Plains Shire Council 6836 SPECIAL SUPPLEMENT 3 September 2007 Maitland City Council Muswellbrook Shire Council Newcastle City Council Port Stephens Council Singleton Shire Council Tamworth City Council Upper Hunter Shire Council NEW SOUTH WALES GOVERNMENT GAZETTE No. -

Snowy Mountains Region Visitors Guide

Snowy Mountains Region Visitors Guide snowymountains.com.au welcome to our year-round The Snowy Mountains is the ultimate adventure four-season holiday destination. There is something very special We welcome you to come and see about the Snowy Mountains. for yourself. It will be an escape that you will never forget! playground It’s one of Australia’s only true year- round destinations. You can enjoy Scan for more things to do the magical winter months, when in the Snowy Mountains or visit snowymountains.com.au/ a snow experience can be thrilling, things-to-do adventurous and relaxing all at Contents the same time. Or see this diverse Kosciuszko National Park ............. 4 region come alive during the Australian Folklore ........................ 5 spring, summer and autumn Snowy Hydro ............................... 6 months with all its wonderful Lakes & Waterways ...................... 7 activities and attractions. Take a Ride & Throw a Line .......... 8 The Snowy Mountains is a natural Our Communities & Bombala ....... 9 wonder of vast peaks, pristine lakes and rushing rivers and streams full of Cooma & Surrounds .................. 10 life and adventure, weaving through Jindabyne & Surrounds .............. 11 unique and interesting landscapes. Tumbarumba & Surrounds ......... 12 Take your time and tour around Tumut & Surrounds .................... 13 our iconic region enjoying fine Our Alpine Resorts ..................... 14 food, wine, local produce and Go For a Drive ............................ 16 much more. Regional Map ............................. 17 Regional Events & Canberra ...... 18 “The Snowy Mountains Getting Here............................... 19 – there’s more to it Call Click Connect Visit .............. 20 than you think!” 2 | snowymountains.com.au snowymountains.com.au | 3 Australian folklore Horse riding is a ‘must do’, when and friends. -

Data Versus Desktop: an Assessment of the Severity of Cold Water Pollution in the Swampy Plains and Murray Rivers Below Khancoban Dam Pope E1 and Nolan A2

Full Paper Pope and Nolan – An assessment of the severity of Cold Water Pollution below Khancoban Dam Data versus Desktop: An assessment of the severity of Cold Water Pollution in the Swampy Plains and Murray Rivers below Khancoban Dam Pope E1 and Nolan A2 1. Snowy Hydro Limited, Cooma NSW 2630. Email: [email protected] 2. Snowy Hydro Limited, Cooma NSW 2630. Email: [email protected] Key Points Cold Water Pollution occurs downstream of Khancoban Dam but effects are not as severe or persistent as expected on the basis of the original desktop study Summer suppression is evident but winter elevation, annual amplitude reduction, seasonal displacement and impacts to diel variation are very minor Causes of cold water releases appear to be a combination of reservoir stratification and releases from Murray 2 Power station with releases from the power station being the dominant cause The presence of Khancoban Reservoir appears to be having a minor impact on the percentage of time that breeding temperature thresholds are exceeded during the breeding seasons of a number of native fish expected to occur in the Swampy Plains and Murray Rivers. Abstract In 2004, Khancoban Dam was listed as one of 9 Dams in NSW considered to cause severe cold water pollution on the basis of a desktop study. This study, based on 5 years of field data, demonstrates that cold water releases do occur from Khancoban but that these events are not as severe or prolonged as expected. On average, there is a difference in temperature of only -2.2°C between monitoring points upstream and downstream of Khancoban Dam during summer. -

Topographic Maps Available As Printed and Digital (PDF) Version

8527-2S BLOWERING 8823-1S KIAH 8527-3N TUMUT 8823-2N NARRABARBA 8624-N NUMBLA VALE 8823-2S NADGEE 8625-3N KALKITE MOUNTAIN 8823-3N TIMBILLICA 8625-3S JINDABYNE 8823-3S GENOA Topographic Maps 8625-4N OLD ADAMINABY 8823-4N BURRAGATE Available as Printed and 8625-4S NIMMO PLAIN 8823-4S MOUNT IMLAY Digital (PDF) version 8626-1N CORIN DAM 8824-1N BROGO 8626-1S RENDEZVOUS CREEK 8824-1S BEGA Key: 8626-2N YAOUK 8824-2N WOLUMLA 1:25,000 Map Titles 8626-2S SHANNONS FLAT 8824-2S PAMBULA 1:50,000 Map Titles 8626-3N TANTANGARA 8824-3N CANDELO 8626-3S DENISON 8824-3S WYNDHAM 0734-4N LORD HOWE ISLAND 8626-4N PEPPERCORN 8824-4N YANKEES GAP 8125-1N DUGAYS BRIDGE 8626-4S RULES POINT 8824-4S BEMBOKA 8125-4N BUNDALONG 8627-1N TAEMAS BRIDGE 8825-1N NERRIGUNDAH 8325-1N WYMAH 8627-1S UMBURRA 8825-1S CADGEE 8325-4N LAKE HUME 8627-2N COTTER DAM 8825-2N WANDELLA 8327-1N WAGGA WAGGA 8627-2S TIDBINBILLA 8825-2S COBARGO 8327-1S LAKE ALBERT 8627-3N BOBBYS PLAINS 8825-3N YOWRIE 8327-2N BIG SPRINGS 8627-3S BRINDABELLA 8825-3S PUEN BUEN 8327-2S MANGOPLAH 8627-4N WEE JASPER 8825-4N BADJA 8327-3N THE ROCK 8627-4S COURAGAGO 8825-4S BELOWRA 8327-3S YERONG CREEK 8633-3N EULOMOGO 8826-1N MONGA 8327-4N COLLINGULLIE 8633-4S BROCKLEHURST 8826-1S ARALUEN 8327-4S URANQUINTY 8724-1N NIMMITABEL 8826-2N BURRUMBELA 8425-1N TINTALDRA 8726-1N CAPTAINS FLAT 8826-2S BENDETHERA 8426-1S ROSEWOOD 8726-1S TINDERRY 8826-3N KRAWARREE 8426-3S JINGELLIC 8726-2N JERANGLE 8826-3S SNOWBALL 8524-1N CHIMNEYS RIDGE 8726-2S WHINSTONE 8826-4N BENDOURA 8524-1S CHARCOAL RANGE 8726-3N COLINTON 8826-4S KAIN