View Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Home + Housewares Guide in an Industry That Changes Daily, It’S Hard to Keep

2019 Pre-Show Edition home + housewares Guide In an industry that changes daily, it’s hard to keep current. The International Home + Housewares Show is the perfect opportunity to get up-to-date: every year close to 60,000 of the world’s most important professionals gather to do business in Chicago. march 2 - 5 Register for badges: www.housewares.org Show Expos . 2-7 City of Chicago . 14-17 Educational Programs . 8-9 Show Planning . 18 Show Destinations . 10-11 Registration Information . 19 Show Events . 12-13 Welcome to Chicago . 20 Show Expos dine + décor Fashion-forward, innovative homegoods • cook + bakeware • tabletop, kitchen for the kitchen and dining room essentials + accents • gift • home décor The 2018 International Home + Housewares Show was a fantastic experience. I would recommend this to anyone in the business. It SOUTH HALL created an amazing atmosphere to network, engage, learn and grow your business. Excellent turnout with a good list of speakers that will benefit every aspect of retailing, and of course, well curated vendors! Exhibitors include: Regina Bonoan, Merchandising Group Manager cook + bakeware Make Room and More (SSI) All-Clad | BergHOFF International | Philippines Chantal Corp. | Corelle Brands | Cristel | CucinaPro | Cuisipro | De Buyer | Fissler | Groupe SEB | Jean Dubost | KRUPS | Search for all Exhibitors and Brands on L'Atelier Du Vin | Lagostina | Le Creuset | Housewares Connect 365 at Lodge Mfg. | Meyer | Nordic Ware | www.housewares.org/housewaresconnect365 Paderno World Cuisine | Rösle | Scanpan | -

Prelim Appendix H Category 6 Petitions

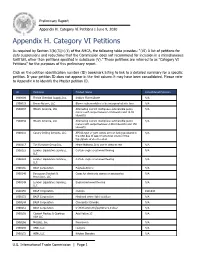

Preliminary Report Appendix H. Category VI Petitions | June 9, 2020 Appendix H. Category VI Petitions As required by Section 3(b)(3)(c)(ii) of the AMCA, the following table provides: “(VI) A list of petitions for duty suspensions and reductions that the Commission does not recommend for inclusion in a miscellaneous tariff bill, other than petitions specified in subclause (V).” These petitions are referred to as "Category VI Petitions” for the purposes of this preliminary report. Click on the petition identification number (ID) bookmark listing to link to a detailed summary for a specific petition. If your petition ID does not appear in the first column it may have been consolidated. Please refer to Appendix A to identify the Master petition ID. ID Petitioner Product Name Consolidated Petitions 1900009 Florida Chemical Supply, Inc. Sodium Fluorosilicate N/A 1900019 Broan-Nutone, LLC Blower subassemblies to be incorporated into fans N/A 1900037 Hitachi America, Ltd. Alternating current multiphase submersible pump N/A motors with output between 3 kilowatts and 14.92 kilowatts 1900038 Hitachi America, Ltd. Alternating current multiphase submersible pump N/A motors with output between 149.2 kilowatts and 150 kilowatts 1900116 Canary Drilling Services, LLC API 6A type of gate valves are not being produced in N/A the USA due to lack of economic source of the type/grade of steel needed 1900117 T.H Furniture Group Inc. Home Mattress,Only use to sleep or rest N/A 1900123 Lumber Liquidators Services, Certain engineered wood flooring N/A LLC 1900124 -

Punt Marks Guide Durobor SA

Reference of glass container manufacturing marks Punt Marks Guide Durobor SA ................................................................................................ 65 Table of Contents Elias Valavanis S.A. Glassworks ............................................................... 66 AGI Glaspac (Div. of HSIL, Formerly Associated Glass Industries, Ltd.) . 5 El Farran Glass Industry ........................................................................... 67 Addis Ababa Bottle & Glass Share Company ........................................... 6 El Nasr Glass & Crystal Co. ....................................................................... 68 Al Tajir Glass Industries LLC ....................................................................... 7 Fábrica de Envases de Vidrio - S.A. de C.V. .............................................. 69 Alembic Limited (Yera Glass) ..................................................................... 8 Fabrica Paraguaya de Vidrio (subsidiary of Ambev S.A.) ....................... 70 Allied Glass Containers Ltd. ....................................................................... 9 Formosan Glass Corporation ................................................................... 71 Amcor ........................................................................................................ 10 Gallo Glass Company ............................................................................... 72 Anadolu Cam Sanayii A.S. - SISECAM ..................................................... 11 Gamin Glass -

Lucy F. Kweskin Matthew A. Skrzynski PROSKAUER ROSE LLP Eleven

20-12097-scc Doc 505 Filed 01/22/21 Entered 01/22/21 18:51:52 Main Document Pg 1 of 186 Hearing Date: February 12, 2021 at 10:00 a.m. (Prevailing Eastern Time) Objection Deadline: February 5, 2021 at 4:00 p.m. (Prevailing Eastern Time) Lucy F. Kweskin Jeff J. Marwil (admitted pro hac vice) Matthew A. Skrzynski Jordan E. Sazant (admitted pro hac vice) PROSKAUER ROSE LLP Brooke H. Blackwell (admitted pro hac vice) Eleven Times Square PROSKAUER ROSE LLP New York, New York 10036 70 West Madison, Suite 3800 Telephone: (212) 969-3000 Chicago, IL 60602 Facsimile: (212) 969-2900 Telephone: (312) 962-3550 Facsimile: (312) 962-3551 Peter J. Young (admitted pro hac vice) PROSKAUER ROSE LLP 2029 Century Park East, Suite 2400 Los Angeles, CA 90067-3010 Telephone: (310) 557-2900 Facsimile: (310) 557-2193 Attorneys for Debtors and Debtors in Possession UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK In re Chapter 11 CENTURY 21 DEPARTMENT STORES LLC, et al., Case No. 20-12097 (SCC) Debtors.1 (Jointly Administered) NOTICE OF APPLICATION OF DEBTORS FOR ENTRY OF AN ORDER AUTHORIZING THE EMPLOYMENT AND RETENTION OF BERDON LLP AS TAX PREPARER AND CONSULTANT EFFECTIVE AS OF THE PETITION DATE PLEASE TAKE NOTICE that a hearing (the “Hearing”) will be held on the Application of Debtors for Entry of an Order Authorizing the Employment and Retention of Berdon LLP as 1 The Debtors in these chapter 11 cases (the “Chapter 11 Cases”), along with the last four digits of each Debtor’s federal tax identification number, as applicable, are Century 21 Department Stores LLC (4073), L.I. -

Final Appendix H Category 6 Petitions

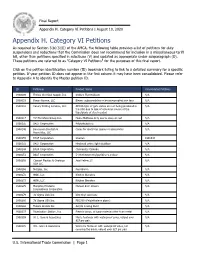

Final Report Appendix H. Category VI Petitions | August 10, 2020 Appendix H. Category VI Petitions As required by Section 3(b)(3)(E) of the AMCA, the following table provides a list of petitions for duty suspensions and reductions that the Commission does not recommend for inclusion in a miscellaneous tariff bill, other than petitions specified in subclause (V) and updated as appropriate under subparagraph (D). These petitions are referred to as "Category VI Petitions" for the purposes of this final report. Click on the petition identification number (ID) bookmark listing to link to a detailed summary for a specific petition. If your petition ID does not appear in the first column it may have been consolidated. Please refer to Appendix A to identify the Master petition ID. ID Petitioner Product Name Consolidated Petitions 1900009 Florida Chemical Supply, Inc. Sodium Fluorosilicate N/A 1900019 Broan-Nutone, LLC Blower subassemblies to be incorporated into fans N/A 1900116 Canary Drilling Services, LLC API 6A type of gate valves are not being produced in N/A the USA due to lack of economic source of the type/grade of steel needed 1900117 T.H Furniture Group Inc. Home Mattress,Only use to sleep or rest N/A 1900135 BASF Corporation Polyisobutylene N/A 1900146 Bensussen Deutsch & Cases for electronic games or accessories N/A Associates, LLC 1900155 BASF Corporation Oxoiron 1901843 1900172 BASF Corporation Hindered amine light stabilizer N/A 1900244 BASF Corporation Chloracetyl Chloride N/A 1900251 BASF Corporation 5-(Methoxymethyl)pyridine-2,3-dicar N/A 1900258 Clariant Plastics & Coatings Acid Yellow 23 N/A USA LLC 1900268 Metglas, Inc. -

Published by the European Container Glass Federation – FEVE AISBL Editor: Alexander Mohr, Phd

NEWSLETTER – June 2011 – N°396 CONTENT EUROPEAN UNION NEWS ...............................................................................................................4 European Commission sets out new rules for phase III of ETS ..................................................................4 Commission weighs product against materials approach to waste directives ..................................................4 Green Week Brussels: Potocnik warns over resource inefficiency ..............................................................5 European Parliament committee backs 30 per cent carbon emissions target ..................................................5 Ireland consults on packaging tax ..................................................................................................5 EC: Waste statistics improve, but quality for most states still only "appropriate" ...............................................6 CONTAINER GLASS INDUSTRY ........................................................................................................6 Global glass packaging market to reach $33.1bn this year ......................................................................6 Europe ...................................................................................................................................7 EU wide consumer survey: Green‐conscious European consumers prefer glass ..............................................7 Ardagh plans stock market listing in US this year: reports .......................................................................7 -

Parenteral Packaging

Interest Group Meeting The Parenteral Drug Association presents: Pre-filled Syringes 11 April 2016 PDA Europe Conference Parenteral Packaging Keep up with the ever advancing pharmaceutical packaging market! 11 April 14 April 14-15 April 14-15 April 14-15 April 14-15 April Molded Glass: Container Closure Container Closure Extractables and Good Glass Handling Drug Delivery From Manufacturing Development Integrity: Leachables Practices in Combination Process to Regulations, Test Parenteral Packaging Products Applications Methods, Application europe.pda.org/ParPack2016 Conference, Exhibition 12-13 April 2016 Register by 12 March 2016 and SAVE! Hilton Molino Stucky Venice | Italy Media Partners Sponsor Welcome Gold sponsor Platinum Sponsor Titanium Sponsor Party SCHEDULE AT A GLANCE 11 April 10:00 – 17:00 Interest Group Meeting Pre-filled Syringes IG Meeting Molded Glass: From Manufacturing 11 April 14:00 – 18:00 Workshop Process to Applications 11 April 19:30 – 22:30 Welcome Party - Skybar Hilton Molino Stucky 12 April 09:00 – 18:15 Conference Conference, 12 April 18:15 – 21:15 Networking Event / Hilton Molino Stucky Exhibition 13 April 07:00 – 15:45 Conference 14 April 09:00 – 17:00 Container Closure Development Training Course 14 April 09:00 – 18:00 Container Closure Integrity: Workshop 15 April 09:00 – 16:30 Regulations, Test Methods, Application 14 April 09:00 – 18:00 Extractables and Leachables Training Course 15 April 09:00 – 16:30 14 April 09:00 – 18:00 Good Glass Handling Practices Workshop 15 April 09:00 – 16:30 in Parenteral Packaging 14 April 09:00 – 17:30 Drug Delivery Combination Products Workshop 15 April 09:00 – 17:30 For latest information, please visit: europe.pda.org/ParPack2016 PDA Europe supports the children's hospice „Sonnenhof” The Sonnenhof Hospice, located near PDA’s office in Berlin, offers support and assistance to families with children suffering from incurable and/or debilitating diseases. -

GID 2016.Pdf

SUPPLIERS & GLASSWORKS COMPLETE GLASS PROFILES DIRECTORY th Special cast irons & alloys 27 annual for glass moulds edition S Suppliers’ Profiles S Yellow Pages S Agents & 2 - Copia omaggio € sales offices "ÉÊUÊÊ S Glassworks’ addresses S Associations *ÃÌiÊÌ>>iÊ-«>ÊÊ-«i`âiÊÊ>LL>iÌÊ«ÃÌ>iÊÊÇä¯ÊÊ Fonderie Valdelsane S.p.A. Strada di Gabbricce, 6 - P.O. BOX 30 - 53035 MONTERIGGIONI (Siena) - ITALY Tel. +39.0577.304730 - Fax. +39.0577.304755 - [email protected] NARIO DE N www.fonderievaldelsane.com FO Supplemento al n. 168 - no. 4/2016 di Glass Machinery Plants & Accessories, Smartenergy S.r.l., Dir. Resp. Marco Pinetti, Supplemento al n. 168 - no. 4/2016 di Glass MachineryDir. Plants & Accessories, Smartenergy S.r.l., At home in the world of glass NIKOLAUS SORG EME MASCHINENFABRIK INTERNATIONAL GmbH FEUERUNGSBAU SORG KERAMIK GmbH & Co KG CLASEN GmbH UND SERVICE GmbH SERVICE GmbH Nikolaus Sorg GmbH & Co. KG | Stoltestraße 23 | 97816 Lohr am Main/Germany | Phone: +49 (0) 9352 507 0 | E-Mail: [email protected] | www.sorg.de , Tomorrow s Technology Today The World’s leading glass companies come to FIC with their Electric Boost/Heating projects E-Glass Installations up to 3,500kW in oxy- Display Glass Numerous installations of fired furnaces for extra tonnage and improving up to 1000kW installed power for TFT/LCD glasses glass quality to eliminate strand breakages. using tin oxide electrode blocks to achieve exceptional glass quality. Container Glass Various installations in flint and coloured glasses, up to 2,500kW for Electric Furnaces Developing new increased output and quality. furnace designs for most glass types, including opal. -

Competitiveness of the Glass Sector

FWC Sector Competitiveness Studies - Competitiveness of the Glass Sector Within the Framework Contract of Sectoral Competitiveness Studies – ENTR/06/054 Final report, 14 October 2008 Client: Directorate-General Enterprise & Industry Notice: This publication was prepared for the European Commission. The views expressed are those of the authors and do not necessarily express the views of the European Commission. ECORYS SCS Group P.O. Box 4175 3006 AD Rotterdam Watermanweg 44 3067 GG Rotterdam The Netherlands T +31 (0)10 453 88 16 F +31 (0)10 453 07 68 E [email protected] W www.ecorys.com Registration no. 24316726 Table of contents Abbreviations and conventions 7 Executive Summary 9 1 Introduction 15 1.1 Background 15 1.2 Purpose 15 1.3 Remaining sections 16 2 Key aspects of the sector 17 2.1 Introduction 17 2.2 Performance 17 2.2.1 Importance of the industry and its different sub-sectors 17 2.2.2 Distribution of production and employment within the EU 21 2.2.3 Location and nature of key industry clusters 27 2.2.4 Productivity 29 2.2.5 Profitability and price-cost margins 30 2.2.6 Exports and trade 32 2.3 Structure 39 2.3.1 Industry structure and size distribution of companies 40 2.3.2 Extent and role of SMEs in sector 42 2.3.3 Identification and ownership of key producers in EU and globally 43 2.4 Processes 48 2.4.1 Production processes 48 2.5 Inputs 49 2.5.1 Raw materials 49 2.5.2 Energy prices 49 2.5.3 Capital 52 2.6 Сonclusions 53 3 Competitive position of the sector 57 3.1 Performance 57 3.1.1 In view of the wide range of sub-sectors, -

Showroom Space Available Leasing Information Where the World’S Best Brands Meet the Industry’S Best Buyers

41Madison.com Showroom Space Available Leasing Information Where the World’s Best Brands Meet the Industry’s Best Buyers. With over 40 years experience as the American headquarters of the luxury Tabletop industry, 41 Madison offers 21 floors of showrooms from over 90 leading manufacturers representing over 200 brands. The featured categories are china, crystal, dinnerware flatware, glassware, hotelware, lighting, gift, objet d’ art, and bespoke pieces. Home of the bi-annual New York Tabletop Show®, the building welcomes retailers, interior designers, chefs, restaurateur, architects, media, and other tabletop professionals from around the globe to meet and experience new offerings from the industry’s finest brands. Lobby Registration Deck Showroom Features and Amenities Include: Newly renovated public areas and Committed and supportive an elegant sense of space throughout. management team with daily liaisons between showrooms. Located in the desired Flatiron District directly across from Madison The office of the Director is available to Square Park and its world-renowned assist exhibitors with their leasing and art exhibitions. marketing needs, as well as help brands promote upcoming markets through Dramatic Manhattan, park and events, newsletters, social media, river views. e-blasts, and public relations counsel. Outstanding design and quality Open daily registration desk. construction of customized spaces. 24 hour security. 41Madison.com 200+ Tabletop Brands Alessi Iittala R Squared Anchor Hocking J. Seignolles RAK Porcelain ARC The -

GM 2013 4.Pdf

9%!2s)335%./s*5,9!5'534 SPECIAL YELLOW PAGES IN RUSSIAN 3)'-! MULLITE FOR THE CRITICAL AREAS OF REGENERATOR 2 - Copia omaggio € CHAMBERS UÊÊ 4)!-! -3#3'## QUALITY-FOCUSED PROVIDER OF INSPECTION SOLUTIONS -%2+!$ HIGH QUALITY PRODUCTION FOR THE TABLEWARE INDUSTRY Issue distributed at: MIR STEKLA MOSCOW RUSSIA 17-20 June GLASS WORLD CAIRO EGYPT 28-30 June Poste Italiane Spa - Sped. in a. p. D.L. 353/2003 (conv. L. 27/02/2004 n° 46) art. 1, comma 1 DCB Milano www.glassonline.com STRADA DI GABBRICCE, 6 - P.O. BOX 30 - 53035 MONTERIGGIONI (Siena) - ITALY Tel. +39-0577-304730 - Fax +39-0577-304755 - [email protected] - www.fonderievaldelsane.com ONEThere’s only WAY to make an high quality product PAS-12 and PAS-9 the new Amig jug forming machines PAS-12 PAS-9 GIANCARLO PEREGO S.P .A. SINCE 1964 YOUR PARTNER IN GLASS FORMING Ⱦɠɚɧɤɚɪɥɨɉɟɪɟɝɨɋɩɚ HI-TECH ɢɳɟɬɚɝɟɧɬɨɜɞɥɹɪɭɫɫɤɨɝɨ ɪɵɧɤɚɡɚɢɧɬɟɪɟɫɨɜɚɧɧɵɦ ɨɛɪɚɳɚɬɶɫɹɤɝɨɫɩɨɞɢɧɭ ȾɚɧɢɷɥɟȻɢɧɹɦɢɧɢ MOULDS ([email protected]) AND SERVICE WORLDWIDE GIANCARLO PEREGO SPA IS LOOKING FOR AGENTS OR REPRESENTATIVES FOR THE RUSSIAN MARKET, IF YOU ARE INTERESTED PLEASE CONTACT MR DANIELE BIGNAMINI ([email protected]) GIANCARLO PEREGO SPA - Via Marchesina, 58 - 20090 Trezzano S.N. (MI) - Italy Tel. +39-02-48400060 Fax +39-02-4453300 E-mail: [email protected] - www.gperego.it A toast to your glass furnace... We are taking care of it ! A detailed understanding of the glassmaker demands and specialisation within the glass furnace refractories field. S.I.G.MA.’s strength, continuous investments, both in the factory and in the laboratory. -

Building on Our New Foundation for Future Growth.” Revenues North American Glass Sales Increased 7.7%, Reaching $562.7 Million

Main Operating Locations Libbey Inc. 2010 Annual Report Corporate Offices North American Other Locations 300 Madison Avenue Building P. O. Box 10060 World Tableware Inc. Toledo, Ohio 43699-0060 300 Madison Avenue On Our 419-325-2100 P.O. Box 10060 www.libbey.com Toledo, Ohio 43699-0060 New Traex Foundation Glassware Manufacturing Locations 101 Traex Plaza Dane, Wisconsin 53529 Toledo For 940 Ash Street Toledo, Ohio 43611 Future Growth Shreveport 4302 Jewella Road Shreveport, Louisiana 71109 Crisa Doblado 1627 Nte. Col. Terminal Monterrey, N.L. Mexico CP 64680 Royal Leerdam Lingedijk 8 4142 LD Leerdam Netherlands Crisal Cristalaria Automatica S.A. Rue de Portugal-Lote 1-Apartado 233 Zona Industrial da Marinha Grande 2431-903 Marinha Grande Portugal Libbey Glassware (China) Co., Ltd. #2211 Aimin Road East Langfang Economic & Technical Development Zone Hebei Province, P.R. China, P.C. 065001 Profile Contents ibbey (NYSE Amex: LBY) is the leading producer the most significant regions of both the Eastern and Western Profile 1 of glass tableware products in the Western Hemi- Hemispheres. Royal Leerdam, located in Leerdam, Nether- Financial Highlights 2 Lsphere, in addition to supplying to key markets throughout lands, is among the world leaders in producing and selling Letter to Shareholders 3 the world. Libbey has the largest manufacturing, distribution glass stemware to retail, foodservice and industrial clients. and service network among North American glass tableware Crisal, located in Marinha Grande, Portugal, manufactures Directors 13 manufacturers. We design and market an extensive line and markets glass tableware, mainly tumblers, stemware Officers 15 of high-quality glass tableware, ceramic dinnerware, metal and glassware accessories complementing Royal Leerdam’s Ten-Year Summary of Selected Financial Data 17 products and providing an expanded presence in Europe.