Research Triangle Regional Public Transportation Authority North Carolina

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

System Every Bus That Travels Through Downtown Stops at One-Way Fare

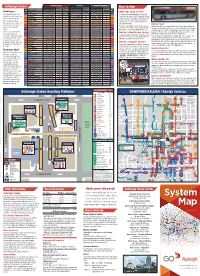

MONDAY–FRIDAY SATURDAY SUNDAY / HOLIDAYS GoRaleigh Routes SPAN FREQUENCY (Minutes) SPAN FREQUENCY SPAN FREQUENCY How To Ride RT # ROUTE NAME (Operating hours) Peak Off-Peak (Operating hours) (Minutes) (Operating hours) (Minutes) RT # Route Types 1 Capital 4:30am–12:10am 15 15 or 60 5:45am–12:08am 30 or 60 5:45am–11:27pm 30 or 60 1 Where do I catch the bus? Most GoRaleigh routes are 2 Falls of Neuse 5:00am–11:25pm 30 30 or 60 5:30am–10:59pm 60 5:30am–10:59pm 60 2 You can catch a GoRaleigh bus at one of the radial routes which begin and 3 Glascock 6:15am–9:44pm 30 60 7:00am–8:42pm 60 7:00am–8:42pm 60 3 many bus stop signs located throughout Raleigh. end in downtown Raleigh. 4 Rex Hospital 4:30am–12:15am 30 30 4:30am–12:15am 30 4:30am–12:15am 30 4 These signs are conveniently located along each 5 Biltmore Hills 5:30am–12:03am 30 60 6:10am–12:12am 60 6:10am–11:12pm 60 5 route. (Please be at your stop a few minutes The “L” routes circulate early–the bus is expected within 5 minutes of 6 Crabtree 5:55am–9:15pm 30 60 7:00am–10:00pm 60 7:00am–10:00pm 60 6 through an area or operate as the scheduled time.) a cross-town route and link 7 South Saunders 5:45am–11:45pm 15 15 or 60 6:00am–11:45pm 30 or 60 6:00am–10:59pm 30 or 60 7 How do I pay? For issues regarding bus stops/shelters, please with one or more radial 7L Carolina Pines 5:45am–11:00pm 30 60 6:45am–9:33pm 60 6:45am–9:33pm 60 7L All GoRaleigh buses are equipped with electronic fareboxes. -

System Map 10.20

JUNE 2021 MEBANE HILLSBOROUGH ORANGE COUNTY ORANGE DURHAM COUNTY City Hall 70 Efland-Cheeks Community Ctr. Downtown Hillsborough WAKE COUNTY WAKE DURHAM COUNTY Walmart 85 85 40 Durham Tech Duke & VA Hospitals Mebane Cone Health Orange County Campus ERWIN RD DURHAM STATION WAKE FOREST Downtown 86 15 Duke University (West Campus) 501 South Square Eubanks Rd 540 1 Bent Tree Plaza 540 CHAPEL Patterson Place DURHAM HILL CARRBORO 147 FRANKLIN ST 540 Downtown 40 Carrboro Collins Crossing Downtown Chapel Hill Triangle Town Center JONES FERRY RD Woodcroft Shopping Ctr. WOODCROFT PKWY Research SOUTH RD Triangle Park RDU International Airport ORANGE COUNTY ORANGE ALAMANCE COUNTY ALAMANCE 54 40 Terminal 2 Terminal 1 UNC Chapel Hill Campus UNC HOSPITALS REGIONAL TRANSIT am CENTER 40 The Streets at Southpoint Cisco pm Morrisville Outlet Mall ORANGE COUNTY pm CHATHAM COUNTY RALEIGH am Perimeter Park State Gov’t. (Halifax Mall) Wake Tech District Dr RTP Campus ZEBULON Meredith College WakeMed Carter-Finley Stadium GORALEIGH Compare Foods STATION BLUE RIDGE RD BLUE TRANSIT HILLSBOROUGH ST CENTER 64 264 NC HWY 55 NC HWY NC State University (Main Campus) Downtown Wendell Major Route Stops CORE ROUTES High House Crossing Park West Village CARY WENDELL Service all day, 7 days a week DEPOT MON - FRI ONLY RD JONES FRANKLIN Park-and-Ride WESTERN BLVD BUCK JONES RD WAKE COUNTY WAKE CHATHAM COUNTY CHATHAM APEX Big Lots Kilmayne Dr Cary Towne Hospital Center REGIONAL ROUTES Crossroads Plaza Service during peak hours only. Monday- Friday Lake Pine Plaza School/University TRYON RD WakeMed Cary Hospital Shopping Center OLD RALEIGH RD Downtown (Compare Foods) CARY REGIONAL EXPRESS ROUTES 401 Airport Service during peak hours only. -

FY 2020 Recommended Wake Transit Work Plan

FY 2020 Recommended Wake Transit Work Plan WAKE COUNTY TRANSIT PLAN: IMPLEMENTATION Fiscal Year (FY) 2020 Recommended Wake Transit Work Plan Table of Contents FY 2020 Wake Transit Work Plan Introduction 3 FY 2020 Operating Budget 6 FY 2020 Triangle Tax District, Wake Operating Fund Budget Ordinance 7 FY 2020 Triangle Tax District, Wake Operating Fund Budget Summary 10 FY 2020 Triangle Tax District, Wake Operating Fund Budget Narrative 11 FY 2020 Triangle Tax District, Wake Operating Fund Budget Detail 15 FY 2020 Operating Project Sheet Summary 16 FY 2020 Operating Project Sheets 21 FY 2020 Capital Budget 38 FY 2020 Triangle Tax District, Wake Capital Fund Budget Ordinance 39 FY 2020 Triangle Tax District, Wake Capital Fund Budget Summary 41 FY 2020 Triangle Tax District, Wake Capital Fund Budget Narrative 42 FY 2020 Triangle Tax District, Wake Capital Fund Budget Detail 46 FY 2020 Capital Project Sheet Summary 47 FY 2020 Capital Plan Project Sheets 52 FY 2020 Financial Model Assumptions Update 90 FY 2020 Financial Model Assumptions Update Narrative 91 FY 2020 Financial Model Assumptions Update Summary 92 Appendix: Multi-Year Operating Program & Capital Improvement Plan 94 WAKE COUNTY TRANSIT PLAN: IMPLEMENTATION FY 2020 Recommended Wake Transit Work Plan The governing boards of GoTriangle, CAMPO, and the Wake County Board of Commissioners adopted the Wake County Transit Plan, including the Wake County Transit Financial Plan and the Transit Governance Interlocal Agreement, which guides the ongoing planning, funding, expansion and construction of the Plan. Included in the governance agreement is the creation of the Transit Planning Advisory Committee (TPAC), a team charged with planning and implementing the adopted Wake Transit Plan. -

Public Involvement Plan August 6, 2020

ORANGE COUNTY TRANSIT PLAN UPDATE Public Involvement Plan August 6, 2020 PREPARED BY: Renaissance Planning Contents INTRODUCTION .......................................................................................................................... 3 PUBLIC INVOLVEMENT EFFORT ............................................................................................... 4 Public Involvement Goals .......................................................................................................... 4 Public Involvement Requirements ............................................................................................. 5 Public Involvement History ........................................................................................................ 7 Project Administration and Decision Making Structure ............................................................. 7 PUBLIC INVOLVEMENT PLAN .............................................................................................. 10 Public Involvement Early Preparation .................................................................................. 10 Public Involvement Program Roles and Responsibilities ..................................................... 11 Outreach Coordination ......................................................................................................... 11 Public Involvement Tools and Techniques .......................................................................... 12 COVID-19 Contingency Plan .................................................................................................. -

Research Triangle Regional Public Transportation Authority North Carolina

RESEARCH TRIANGLE REGIONAL PUBLIC TRANSPORTATION AUTHORITY NORTH CAROLINA . COMPREHENSIVE ANNUAL ·. FINANCIAL REPORT For the Fiscal Year Ended June 30, 2013 Prepared by: Finance Department .I RESEARCH TRIANGLE REGIONAL PUBLIC TRANSPORTATION AUTHORITY FOR THE YEAR ENDED JUNE 30, 2013 TABLE OF CONTENTS INTRODUCTORY SECTION: Letter of Transmittal 4-11 Board of Trustees 12 FY 2013 Senior Staff 13 Certificate of Achievement for Excellence in Financial Reporting 14 FINANCIAL SECTION: Report of Independent Auditor 15-16 Management's Discussion and Analysis 17-26 Basic Financial Statements: Government-Wide Financial Statements: Statement of Net Position 27 Statement of Activities 28 Fund Financial Statements: Balance Sheet-Governmental Funds 29 Reconciliation of the Balance Sheet to the Statement of Net Position - 30 Governmental Funds Statement of Revenues, Expenditures and Changes in · .Fund Balances - Governmental Funds 31 Reconciliation of the Statement of Revenues, Expenditures and Changes in Fund Balances of Governmental Funds to the Statement of Activities 32 Statement of Revenues, Expenditures and Changes in . Fund Balances - Budget and Actual - General Fund 33 Statement of Revenues, Expenditures and Changes in Fund Balances - Budget and Actual - Western Triangle Tax District 34 Statement of Fund Net Position - Proprietary Funds 35 Statement of Revenue, Expenses and Changes in Fund Net Position - Proprietary Funds 36 Statement of Cash Flows - Proprietary Funds 37-38 Notes to the Basic Financial Statements 39-62 Required Supplementary Information: -

Preliminary Study Findings Preliminary Findings Page 438 of 513 FAST Network Team

Page 437 of 513 Preliminary Study Findings Preliminary Findings Page 438 of 513 FAST Network Team Taruna Tayal, PMP Don Bryson, PE Chris Brasier, EI VHB | Project Manager VHB | Principal-in-Charge VHB | Transit Planner Roberta MK Fox, AIA, ASLA Sasha Pejcic, PMP Catalyst Design | Stakeholder Engagement Stantec | Innovative Solutions and Implementation Preliminary Findings Page 439 of 513 FAST Network Overview Business community framework for enhanced transit Expectation that cost-effective, useful travel options will be in place Pushing for rapid implementation of an effective, scalable, regional, multimodal transportation system Preliminary Findings Page 440 of 513 FAST Network Study Purpose Advance ideas for improving and accelerating regional connectivity Accelerate effective, all-day mobility along our freeway and street-system that can expand and improve over time Complement existing and emerging travel options Serve as a valuable template for other regions of the state Page 441 of 513 FAST study approach Preliminary Findings Page 442 of 513 Existing Conditions Regional Freeway System Preliminary Findings Page 443 of 513 Existing Conditions GoTriangle Network Preliminary Findings Page 444 of 513 Transit System Planned BRT Preliminary Findings Page 445 of 513 Transit System Planned Commuter Rail Preliminary Findings Page 446 of 513 Existing System Regional Linkage BRT: High frequency, subregional Commuter rail: Regional, low/moderate frequency FAST: • Provide complementary, effective, regional linkages • Accelerate creation of true -

Clean Air Act Complaint: University of North Carolina at Chapel Hill

IN THE UNITED STATES DISTRICT COURT FOR THE MIDDLE DISTRICT OF NORTH CAROLINA Case No. 1:19-cv-1179 CENTER FOR BIOLOGICAL ) DIVERSITY and SIERRA CLUB, ) ) Plaintiffs, ) ) v. ) COMPLAINT ) UNIVERSITY OF NORTH ) CAROLINA AT CHAPEL HILL, ) ) Defendant. ) ) NATURE OF THE CASE 1. Plaintiffs Center for Biological Diversity and Sierra Club (collectively, “Conservation Groups”) bring this citizen enforcement action to enforce repeated violations by the University of North Carolina at Chapel Hill (“UNC”) of the permit issued under Title V of the Clean Air Act for the operation of air pollution sources on UNC’s campus. In violation of that permit and applicable law, UNC has burned more coal than the permit allows in its coal burning boilers and has failed to maintain records showing that emissions from those boilers and other sources are not causing violations of health- and public welfare-based national ambient air quality standards. 42 U.S.C. § 7401 et seq. 2. The air pollution that UNC emits can cause a wide variety of adverse impacts including asthma attacks, decreased lung function, especially among young 1 Case 1:19-cv-01179 Document 1 Filed 12/03/19 Page 1 of 18 people, and even premature mortality. See, e.g., North Carolina v. TVA, 593 F.Supp.2d 812, 822 (W.D.N.C. 2009) rev’d on other grounds, 615 F.3d 291 (4th Cir. 2010) (In tort case against coal-fired power plants “Court finds that, at a minimum, there is an increased risk of incidences of premature mortality in the general public associated with [air pollution] exposure”). -

July 1, 2017 – June 30, 2018

Fiscal Year 2018 Budget & Capital Investment Plan Fiscal Year 2018 Budget for the Durham-Orange Transit Plan Fiscal Year 2018 Budget for Wake County Transit Plan July 1, 2017 – June 30, 2018 MEBANE Efland-Cheeks Community Ctr. City Hall am 70 ODX pm HILLSBOROUGH Downtown 420 DURHAM COUNTY Regional System Map Hillsborough Mebane Walmart Cone Health ODX 85 400 DRX 405 ODX pm Duke & VA ODX 700 40 85 Hospitals PART 4 Durham Tech Orange Co. Campus ERWIN RD ODX GoDurham 405 420 Durham 400 Station DURHAM COUNTY PART Route 4 continues to DRX Duke Transit 700 Graham, Burlington, and DRX Downtown PART 4 15 WAKE FOREST Greensboro. Visit partnc.org Duke University 501 for more details. 86 COUNTY ORANGE (West Campus) Eubanks Rd South Square 405 am 400 400 1 Route 400 serves CHAPEL Patterson the South Square DURHAM ORANGE COUNTY ORANGE WRX HILL Place area during peak CRX hours only WAKE COUNTY WAKE CARRBORO 40 147 Millbrook Downtown FRANKLIN ST am CRX DRX 700 Exchange Park Carrboro am Collins pm Downtown Woodcroft 70 201 Triangle Town 405 Townridge Shelley Lake Crossing am Chapel Hill Shopping Ctr. Research SPRING FOREST RD Center 540 Shopping Ctr. Sertoma Arts Ctr. JONES FERRY RD pm pm Triangle am WOODCROFT PKWY Park 201 SOUTH RD 201 pm 805 MILLBROOK RD Capital Crossing WRX 400 405 420 Terminal 2 Shopping Ctr. ALAMANCE COUNTY ALAMANCE PART 4 PART 54 CRX 40 CRX 40 800 800 S pm UNC 100 Terminal 1 Chapel Hill RTP Shuttle RDU UNC Campus 800 Chapel Hill Transit International 54 Hospitals 400 PART 4 GoDurham 805 Regional Airport 405 Renaissance The Streets am Transit 100 420 Village at Southpoint US EPA DRX Center CRX 800 S NIEHS pm 105 805 Morrisville 300 ORANGE COUNTY pm Route 800 800 uses I-40 Outlet Mall CHATHAM COUNTY RALEIGH when Route 805 is 100 105 311 Perimeter Park in service am 201 700 300 800 40 CRX 311 805 State Gov’t. -

Durham Area Transit Authority Fixed Route Bus Accessibility, Equipment

Durham Area Transit Authority Fixed Route Bus Accessibility, Equipment Maintenance, Reliability, and Use Review Final Report December 2015 Federal Transit Administration U.S. Department of Transportation Federal Transit Administration FTA Fixed Route Bus Accessibility Equipment Maintenance, Reliability, and Use Review Final Report: DATA December 2015 This page has been intentionally left blank to facilitate duplex printing FTA Fixed Route Bus Accessibility Equipment Maintenance, Reliability, and Use Review Final Report: DATA December 2015 Table of Contents Executive Summary ...................................................................................................................................... 1 1 General Information ................................................................................................................................. 3 2 Jurisdiction and Authorities ..................................................................................................................... 5 3 Purpose and Objectives ............................................................................................................................ 7 3.1 Purpose ............................................................................................................................................ 7 3.2 Objectives ........................................................................................................................................ 7 4 Introduction to the Durham Area Transit Authority ............................................................................... -

Research Triangle Park

Published on NCpedia (https://www.ncpedia.org) Home > Research Triangle Park Research Triangle Park [1] Share it now! Research Triangle Park by Wiley J. Williams, 2006 Computer under construction at an IBM production facility in Research Triangle Park, 1984. Photograph by Billy Barnes. North Carolina Collection, University of North Carolina at Chapel Hill Library. Research Triangle Park, the largest planned research center in the United States, was created in 1959 through the efforts of Governor Luther Hodges [2] and hundreds of scientists, politicians, and business leaders. Located between Raleigh [3] and Durham [4] and the Triangle's three acclaimed universities-the University of North Carolina at Chapel Hill [5], Duke University [6], and North Carolina State University [7]-Research Triangle Park (RTP) in 2006 encompassed 7,000 acres and was home to more than 100 research and development organizations employing 38,000 North Carolinians. Smaller but highly successful research parks also existed in Charlotte [8], Greensboro [9], Rocky Mount, and elsewhere, playing an important role in the diversification of the state's economy. The need for a redirection of economic development away from traditional products such ast extiles [10], tobacco [11], and furniture [12] was envisioned in the early 1950s by some of North Carolina's morep rogressive [13] leaders. In 1952 Howard Odum, a renowned UNC-Chapel Hill sociologist and founder of the university's Institute for Research in Social Science [14], voiced a number of ideas about cooperative research centers that could benefit the state by combining the strengths of its three research universities. State leaders considered how these institutions could become a foundation for economic development. -

Research Triangle Park North Carolina

RESEARCH TRIANGLE PARK NORTH CAROLINA Located in the center of three tier one research KY universities, the Research Triangle Park (RTP) is the VA largest, and one of the most successful, research parks in the United States. Founded in the 1950s, TN Raleigh RTP is now home to more than 200 companies employing north of 50,000 people. Companies in the NC Port of Morehead City SC Park range from IT giants like IBM to entrepreneurial GA ventures hoping to commercialize the world’s next big idea. MAJOR EMPLOYERS Life Sciences n Bayer CropScience Duke University n Biogen 10 miles n GlaxoSmithKline n United Therapeutics Technology UNC Chapel Hill n IBM 12 miles n Cisco Systems RDU Int’l Airport n Freudenberg IT Adjacent n Lenovo n NetApp NC State University 14 miles Downtown Raleigh 17 miles NC Mountains 2.5 hours NC Beaches RTP 2 hours North Carolina FAST FACTS KEY INDUSTRIES n Created in 1959 n 7,000 Acres n Life Sciences n 22.5 Million Sq. Ft. of built space n Technology n 200+ companies employ 50,000 people n CleanTech n 4 of the 5 largest global Ag Biotech firms n Entrepreneurial Ventures The North American Bee Care Center at Bayer CropScience is dedicated to improving honey bee health. IBM became RTP’s first major tenant when they built their 600,000 square foot facility in 1965. The Frontier at RTP is an exceptional resource for entrepreneurs in the region. Companies located in RTP have 46% of the companies in received more than 3200 patents RTP are engaged in the and almost 2000 trademarks. -

Page 1 Within the Proposed Budget for FY2016-17 ($217,203).The Projected Budget for FY2017-18 Is $230,000

CITY OF DURHAM | NORTH CAROLINA Date: May 17, 2016 To: Thomas J. Bonfield, City Manager Through: Keith Chadwell, Deputy City Manager From: Harmon E. Crutchfield, Interim Director of Transportation Subject: Interlocal Agreement for Regional Transit Information Center Executive Summary The City of Durham is seeking approval to execute an Interlocal Agreement to continue to support the partnership of the GoTransit Regional Information Center. Recommendation It is recommended that the City Council resolve that the City Manager be authorized to execute the Fiscal Years 2016-2018 Services Agreement for the GoTransit Regional Information Center among the City of Durham, Town of Cary, Town of Chapel Hill, City of Raleigh and the Research Triangle Regional Public Transportation Authority d/b/a GoTriangle. Background The GoTransit Regional Information Center is a cooperative effort between Cary, Chapel Hill, GoDurham, GoRaleigh and GoTriangle to allow anyone to make one call for information on public transportation and ridesharing services throughout the Triangle. The City of Durham has been a partner of the Information Center since 2007 and the partnership has allowed for greater hours of phone coverage, better training of Customer Information Associates and clearer communication with customers. Issues/Analysis The Interlocal Agreement establishes the services to be performed and the cost-split among the five partnering entities. The services include handling customer information calls, maintaining the data in the customer information systems, and managing the real-time bus location contract. The cost-sharing for call handling staff is based on call volumes of recent years and shared among five agencies. The costs of the data maintenance staff person is split three ways among Durham, Raleigh and GoTriangle.