Research Triangle Regional Public Transportation Authority North Carolina

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

HON. JESSE HELMS ÷ Z 1921–2008

im Line) HON. JESSE HELMS ÷z 1921–2008 VerDate Aug 31 2005 15:01 May 15, 2009 Jkt 043500 PO 00000 Frm 00001 Fmt 6686 Sfmt 6686 H:\DOCS\HELMS\43500.TXT CRS2 PsN: SKAYNE VerDate Aug 31 2005 15:01 May 15, 2009 Jkt 043500 PO 00000 Frm 00002 Fmt 6686 Sfmt 6686 H:\DOCS\HELMS\43500.TXT CRS2 PsN: SKAYNE (Trim Line) (Trim Line) Jesse Helms LATE A SENATOR FROM NORTH CAROLINA MEMORIAL ADDRESSES AND OTHER TRIBUTES IN THE CONGRESS OF THE UNITED STATES E PL UR UM IB N U U S VerDate Aug 31 2005 15:01 May 15, 2009 Jkt 043500 PO 00000 Frm 00003 Fmt 6687 Sfmt 6687 H:\DOCS\HELMS\43500.TXT CRS2 PsN: SKAYNE congress.#15 (Trim Line) (Trim Line) Courtesy U.S. Senate Historical Office Jesse Helms VerDate Aug 31 2005 15:01 May 15, 2009 Jkt 043500 PO 00000 Frm 00004 Fmt 6687 Sfmt 6688 H:\DOCS\HELMS\43500.TXT CRS2 PsN: SKAYNE 43500.002 (Trim Line) (Trim Line) S. DOC. 110–16 Memorial Addresses and Other Tributes HELD IN THE SENATE AND HOUSE OF REPRESENTATIVES OF THE UNITED STATES TOGETHER WITH A MEMORIAL SERVICE IN HONOR OF JESSE HELMS Late a Senator from North Carolina One Hundred Tenth Congress Second Session ÷ U.S. GOVERNMENT PRINTING OFFICE WASHINGTON : 2009 VerDate Aug 31 2005 15:01 May 15, 2009 Jkt 043500 PO 00000 Frm 00005 Fmt 6687 Sfmt 6686 H:\DOCS\HELMS\43500.TXT CRS2 PsN: SKAYNE (Trim Line) (Trim Line) Compiled under the direction of the Joint Committee on Printing VerDate Aug 31 2005 15:01 May 15, 2009 Jkt 043500 PO 00000 Frm 00006 Fmt 6687 Sfmt 6687 H:\DOCS\HELMS\43500.TXT CRS2 PsN: SKAYNE (Trim Line) (Trim Line) CONTENTS Page Biography ................................................................................................. -

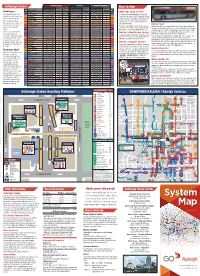

System Every Bus That Travels Through Downtown Stops at One-Way Fare

MONDAY–FRIDAY SATURDAY SUNDAY / HOLIDAYS GoRaleigh Routes SPAN FREQUENCY (Minutes) SPAN FREQUENCY SPAN FREQUENCY How To Ride RT # ROUTE NAME (Operating hours) Peak Off-Peak (Operating hours) (Minutes) (Operating hours) (Minutes) RT # Route Types 1 Capital 4:30am–12:10am 15 15 or 60 5:45am–12:08am 30 or 60 5:45am–11:27pm 30 or 60 1 Where do I catch the bus? Most GoRaleigh routes are 2 Falls of Neuse 5:00am–11:25pm 30 30 or 60 5:30am–10:59pm 60 5:30am–10:59pm 60 2 You can catch a GoRaleigh bus at one of the radial routes which begin and 3 Glascock 6:15am–9:44pm 30 60 7:00am–8:42pm 60 7:00am–8:42pm 60 3 many bus stop signs located throughout Raleigh. end in downtown Raleigh. 4 Rex Hospital 4:30am–12:15am 30 30 4:30am–12:15am 30 4:30am–12:15am 30 4 These signs are conveniently located along each 5 Biltmore Hills 5:30am–12:03am 30 60 6:10am–12:12am 60 6:10am–11:12pm 60 5 route. (Please be at your stop a few minutes The “L” routes circulate early–the bus is expected within 5 minutes of 6 Crabtree 5:55am–9:15pm 30 60 7:00am–10:00pm 60 7:00am–10:00pm 60 6 through an area or operate as the scheduled time.) a cross-town route and link 7 South Saunders 5:45am–11:45pm 15 15 or 60 6:00am–11:45pm 30 or 60 6:00am–10:59pm 30 or 60 7 How do I pay? For issues regarding bus stops/shelters, please with one or more radial 7L Carolina Pines 5:45am–11:00pm 30 60 6:45am–9:33pm 60 6:45am–9:33pm 60 7L All GoRaleigh buses are equipped with electronic fareboxes. -

System Map 10.20

JUNE 2021 MEBANE HILLSBOROUGH ORANGE COUNTY ORANGE DURHAM COUNTY City Hall 70 Efland-Cheeks Community Ctr. Downtown Hillsborough WAKE COUNTY WAKE DURHAM COUNTY Walmart 85 85 40 Durham Tech Duke & VA Hospitals Mebane Cone Health Orange County Campus ERWIN RD DURHAM STATION WAKE FOREST Downtown 86 15 Duke University (West Campus) 501 South Square Eubanks Rd 540 1 Bent Tree Plaza 540 CHAPEL Patterson Place DURHAM HILL CARRBORO 147 FRANKLIN ST 540 Downtown 40 Carrboro Collins Crossing Downtown Chapel Hill Triangle Town Center JONES FERRY RD Woodcroft Shopping Ctr. WOODCROFT PKWY Research SOUTH RD Triangle Park RDU International Airport ORANGE COUNTY ORANGE ALAMANCE COUNTY ALAMANCE 54 40 Terminal 2 Terminal 1 UNC Chapel Hill Campus UNC HOSPITALS REGIONAL TRANSIT am CENTER 40 The Streets at Southpoint Cisco pm Morrisville Outlet Mall ORANGE COUNTY pm CHATHAM COUNTY RALEIGH am Perimeter Park State Gov’t. (Halifax Mall) Wake Tech District Dr RTP Campus ZEBULON Meredith College WakeMed Carter-Finley Stadium GORALEIGH Compare Foods STATION BLUE RIDGE RD BLUE TRANSIT HILLSBOROUGH ST CENTER 64 264 NC HWY 55 NC HWY NC State University (Main Campus) Downtown Wendell Major Route Stops CORE ROUTES High House Crossing Park West Village CARY WENDELL Service all day, 7 days a week DEPOT MON - FRI ONLY RD JONES FRANKLIN Park-and-Ride WESTERN BLVD BUCK JONES RD WAKE COUNTY WAKE CHATHAM COUNTY CHATHAM APEX Big Lots Kilmayne Dr Cary Towne Hospital Center REGIONAL ROUTES Crossroads Plaza Service during peak hours only. Monday- Friday Lake Pine Plaza School/University TRYON RD WakeMed Cary Hospital Shopping Center OLD RALEIGH RD Downtown (Compare Foods) CARY REGIONAL EXPRESS ROUTES 401 Airport Service during peak hours only. -

FY 2020 Recommended Wake Transit Work Plan

FY 2020 Recommended Wake Transit Work Plan WAKE COUNTY TRANSIT PLAN: IMPLEMENTATION Fiscal Year (FY) 2020 Recommended Wake Transit Work Plan Table of Contents FY 2020 Wake Transit Work Plan Introduction 3 FY 2020 Operating Budget 6 FY 2020 Triangle Tax District, Wake Operating Fund Budget Ordinance 7 FY 2020 Triangle Tax District, Wake Operating Fund Budget Summary 10 FY 2020 Triangle Tax District, Wake Operating Fund Budget Narrative 11 FY 2020 Triangle Tax District, Wake Operating Fund Budget Detail 15 FY 2020 Operating Project Sheet Summary 16 FY 2020 Operating Project Sheets 21 FY 2020 Capital Budget 38 FY 2020 Triangle Tax District, Wake Capital Fund Budget Ordinance 39 FY 2020 Triangle Tax District, Wake Capital Fund Budget Summary 41 FY 2020 Triangle Tax District, Wake Capital Fund Budget Narrative 42 FY 2020 Triangle Tax District, Wake Capital Fund Budget Detail 46 FY 2020 Capital Project Sheet Summary 47 FY 2020 Capital Plan Project Sheets 52 FY 2020 Financial Model Assumptions Update 90 FY 2020 Financial Model Assumptions Update Narrative 91 FY 2020 Financial Model Assumptions Update Summary 92 Appendix: Multi-Year Operating Program & Capital Improvement Plan 94 WAKE COUNTY TRANSIT PLAN: IMPLEMENTATION FY 2020 Recommended Wake Transit Work Plan The governing boards of GoTriangle, CAMPO, and the Wake County Board of Commissioners adopted the Wake County Transit Plan, including the Wake County Transit Financial Plan and the Transit Governance Interlocal Agreement, which guides the ongoing planning, funding, expansion and construction of the Plan. Included in the governance agreement is the creation of the Transit Planning Advisory Committee (TPAC), a team charged with planning and implementing the adopted Wake Transit Plan. -

Public Involvement Plan August 6, 2020

ORANGE COUNTY TRANSIT PLAN UPDATE Public Involvement Plan August 6, 2020 PREPARED BY: Renaissance Planning Contents INTRODUCTION .......................................................................................................................... 3 PUBLIC INVOLVEMENT EFFORT ............................................................................................... 4 Public Involvement Goals .......................................................................................................... 4 Public Involvement Requirements ............................................................................................. 5 Public Involvement History ........................................................................................................ 7 Project Administration and Decision Making Structure ............................................................. 7 PUBLIC INVOLVEMENT PLAN .............................................................................................. 10 Public Involvement Early Preparation .................................................................................. 10 Public Involvement Program Roles and Responsibilities ..................................................... 11 Outreach Coordination ......................................................................................................... 11 Public Involvement Tools and Techniques .......................................................................... 12 COVID-19 Contingency Plan .................................................................................................. -

Preliminary Study Findings Preliminary Findings Page 438 of 513 FAST Network Team

Page 437 of 513 Preliminary Study Findings Preliminary Findings Page 438 of 513 FAST Network Team Taruna Tayal, PMP Don Bryson, PE Chris Brasier, EI VHB | Project Manager VHB | Principal-in-Charge VHB | Transit Planner Roberta MK Fox, AIA, ASLA Sasha Pejcic, PMP Catalyst Design | Stakeholder Engagement Stantec | Innovative Solutions and Implementation Preliminary Findings Page 439 of 513 FAST Network Overview Business community framework for enhanced transit Expectation that cost-effective, useful travel options will be in place Pushing for rapid implementation of an effective, scalable, regional, multimodal transportation system Preliminary Findings Page 440 of 513 FAST Network Study Purpose Advance ideas for improving and accelerating regional connectivity Accelerate effective, all-day mobility along our freeway and street-system that can expand and improve over time Complement existing and emerging travel options Serve as a valuable template for other regions of the state Page 441 of 513 FAST study approach Preliminary Findings Page 442 of 513 Existing Conditions Regional Freeway System Preliminary Findings Page 443 of 513 Existing Conditions GoTriangle Network Preliminary Findings Page 444 of 513 Transit System Planned BRT Preliminary Findings Page 445 of 513 Transit System Planned Commuter Rail Preliminary Findings Page 446 of 513 Existing System Regional Linkage BRT: High frequency, subregional Commuter rail: Regional, low/moderate frequency FAST: • Provide complementary, effective, regional linkages • Accelerate creation of true -

July 1, 2017 – June 30, 2018

Fiscal Year 2018 Budget & Capital Investment Plan Fiscal Year 2018 Budget for the Durham-Orange Transit Plan Fiscal Year 2018 Budget for Wake County Transit Plan July 1, 2017 – June 30, 2018 MEBANE Efland-Cheeks Community Ctr. City Hall am 70 ODX pm HILLSBOROUGH Downtown 420 DURHAM COUNTY Regional System Map Hillsborough Mebane Walmart Cone Health ODX 85 400 DRX 405 ODX pm Duke & VA ODX 700 40 85 Hospitals PART 4 Durham Tech Orange Co. Campus ERWIN RD ODX GoDurham 405 420 Durham 400 Station DURHAM COUNTY PART Route 4 continues to DRX Duke Transit 700 Graham, Burlington, and DRX Downtown PART 4 15 WAKE FOREST Greensboro. Visit partnc.org Duke University 501 for more details. 86 COUNTY ORANGE (West Campus) Eubanks Rd South Square 405 am 400 400 1 Route 400 serves CHAPEL Patterson the South Square DURHAM ORANGE COUNTY ORANGE WRX HILL Place area during peak CRX hours only WAKE COUNTY WAKE CARRBORO 40 147 Millbrook Downtown FRANKLIN ST am CRX DRX 700 Exchange Park Carrboro am Collins pm Downtown Woodcroft 70 201 Triangle Town 405 Townridge Shelley Lake Crossing am Chapel Hill Shopping Ctr. Research SPRING FOREST RD Center 540 Shopping Ctr. Sertoma Arts Ctr. JONES FERRY RD pm pm Triangle am WOODCROFT PKWY Park 201 SOUTH RD 201 pm 805 MILLBROOK RD Capital Crossing WRX 400 405 420 Terminal 2 Shopping Ctr. ALAMANCE COUNTY ALAMANCE PART 4 PART 54 CRX 40 CRX 40 800 800 S pm UNC 100 Terminal 1 Chapel Hill RTP Shuttle RDU UNC Campus 800 Chapel Hill Transit International 54 Hospitals 400 PART 4 GoDurham 805 Regional Airport 405 Renaissance The Streets am Transit 100 420 Village at Southpoint US EPA DRX Center CRX 800 S NIEHS pm 105 805 Morrisville 300 ORANGE COUNTY pm Route 800 800 uses I-40 Outlet Mall CHATHAM COUNTY RALEIGH when Route 805 is 100 105 311 Perimeter Park in service am 201 700 300 800 40 CRX 311 805 State Gov’t. -

1 WAKE COUNTY BOARD of COMMISSIONERS Regular

WAKE COUNTY BOARD OF COMMISSIONERS Regular Meeting August 6, 2012 2:00 P.M. Room 700, Wake County Courthouse Meeting Called to Order: Chairman Paul Coble Members present were: Chairman Paul Y. Coble, Vice Chair Phil Matthews and Commissioners Joe Bryan, Tony Gurley, Ervin Portman, Betty Lou Ward, James West Others attending were: David C. Cooke, County Manager, Susan J. Banks, Clerk to the Board, Scott Warren, County Attorney, Denise Hogan, Deputy Clerk, Johnna Rogers and Joe Durham, Deputy County Managers. Pledge of Allegiance Invocation: Commissioner Joe Bryan Items of Business Approval of Agenda County Manager David Cooke asked to remove item #9 from the agenda. Chairman Coble asked to pull item #7 from the consent agenda for discussion. Betty Lou Ward motioned, seconded by Tony Gurley, to approval the agenda with the removal of item #9, Wide Area Network Infrastructure contract from the agenda and remove item #7 from the consent agenda for discussion. The motion passed unanimously. Approval of the Minutes of the Commissioners' Regular Meeting on July 2, 2012 Tony Gurley motioned, seconded by Phil Matthews, to approve the Minutes of the Commissioners’ Regular Meeting on July 2, 2012. The motion passed unanimously. Proclamation Honoring Dr. William Weston Hedrick for Providing Over 50 Years of Medical Care to the People of Wake County 1 Chairman Coble said that Dr. William Weston Hedrick for providing over 50 years of medical care to the people of Wake County. Chairman Coble read aloud the proclamation. Betty Lou Ward motioned, seconded by Tony Gurley, to approve the Proclamation Honoring Dr. William Weston Hedrick for Providing Over 50 Years of Medical Care to the People of Wake County. -

Durham Cary Raleigh Chapel Hill Morrisville

! ! !!!! !! !! !! ! ! !! ! !! ! ! ! !! !! ! ! ! ! !! ! ! ! ! !! ! ! ! ! !! ! ! !! ! ! ! ! !! !! ! !! ! ! ! ! ! !! ! ! !! ! !! !! ! !! ! ! !!! ! ! !! ! ! ! !! ! ! ! ! ! ! ! !! EXISTING TRANSIT ! ! ! !! !! ! ! ! ! ! ! ! ! !!! !! !! !! ! ! !! ! !! ! !! !!!!! !! ! !! ! ! ! !!! ! ! !! ! ! ! ! ! !! !!! ! ! ! ! The Triangle Bikeway study area is served by the regional transit authority, GoTrian- ! ! ! ! ! ! ! ! !! !! ! gle; four local transit agencies: Chapel Hill Transit, GoDurham, GoCary, and GoRa- !! ! ! !!!!!!! ! ! ! !! ! !!!! ! ! ! ! ! !! leigh; and North Carolina State University’s WolfLine transit system. 40 ! ! !! ! ! ! ! ! ! ! ! ! ! !! !! !! ! ! ! ! ! ! ! ! ! !! !! ! !! !! !! ! ! ! ! NC-147 GoTriangle routes in the study area are anchored by the Regional Transit Center, which ! ! ! ! ! ! !!! ! ! ! ! ! ! ! ! ! is located along the proposed Triangle Bikeway corridor on Slater Rd in Durham’s ! ! ORANGE COUNTY !! ! ! ! ! DURHAM COUNTY !! !! Imperial Center and is adjacent to Research Triangle Park. The following GoTrian- ! ! NC-15-501 ! ! !! ! CHAPEL ! ! ! ! ! ! !! ! ! !! gle routes serve the Triangle Bikeway corridor: CRX – Chapel Hill-Raleigh Express, ! !! ! ! ! ! ! ! !! ! !! ! ! ! !!! ! ! ! ! ! ! ! DRX – Durham-Raleigh Express, 100 – Raleigh/RDU Airport/Regional Transit Center, ! ! !! ! ! ! ! ! ! ! ! ! HILL ! ! DURHAM ! ! ! !! !! !! ! 310 – Cary/Wake Tech RTP/Regional Transit Center, 700 – Durham/Regional Transit ! ! ! ! ! ! ! ! ! ! ! ! ! !!! ! ! Center, 800S – Southpoint/Chapel Hill, and 805 – Chapel Hill/Woodcroft/Regional ! !! ! ! -

Fy 2018 Gotriangle

ANNUAL REPORT GOTRIANGLE FY 2018 TABLE OF CONTENTS MESSAGE FROM OUR CHAIR �������������������������������������������������������������������������������������������������������������������������������������������3 MESSAGE FROM OUR PRESIDENT & CEO ���������������������������������������������������������������������������������������������������������������������5 ABOUT US �����������������������������������������������������������������������������������������������������������������������������������������������������������������������������7 OUR FAMILY �������������������������������������������������������������������������������������������������������������������������������������������������������������������������9 OUR TRANSIT PARTNERS ������������������������������������������������������������������������������������������������������������������������������������������������ 11 OUR UNIVERSITY & BUSINESS ALLIANCES ��������������������������������������������������������������������������������������������������������������� 13 TRACKING BUS RIDERSHIP �������������������������������������������������������������������������������������������������������������������������������������������� 15 GOTRIANGLE SYSTEMWIDE TOTALS ��������������������������������������������������������������������������������������������������������������������������� 17 GO FORWARD �������������������������������������������������������������������������������������������������������������������������������������������������������������������� 19 DURHAM -

FY 2014 Operating and Capital Budget

M as on R 401 St Marys Rd G d ues 56 s R 39 SYSTEM MAPd B d iv M R i i o 561 n lt r S s o o n n o R b w R x Durham Ave d H d o ill R 50 R d Downtown Durham N Downtown Raleigh 15 W. Morgan 86 Gregson St. 157 Morris d Fuller 581 56 57 R DURHAM COUNTY Roney s GRANVILLE COUNTY ry Gate 1 Rd 85 401 Ma t Foster 56 Maxway Shopping S Main St GRANVILLE COUNTY FRANKLIN COUNTY Cornelius St Center 56 Revere Rd DRX AM DRX PM Durham Carolina L Arts CouncilTheatre Delway St a St. Gregson 70 Corbin St tta Innity Rd d Amtrak Main St R R Manning ORANGE COUNTY d d Convention . Hillsborough DURHAM COUNTY stead Rd r Um St. Duke N d King St fo 400 Chapel Hill St. Center v x l O DRX PM Chapel Hill St. WRX Wake Forest Rd B Nash St Nash 405 Courthouse 70 ld l Pettigrew St a O DRX AM t i Churton St Churton DRX 96 d Red Mill Rd p D R a d u WRX n R C r e on h r Hamlin Rd GRANVILLECorcoran COUNTY BUS e a 501 a r h Hebron Rd m St. Duke S Willard St. Willard Halifax St Halifax 86 G S Jackson St St Blount t f H 70 n ort F WAKE COUNTY Peace St C o on r a R e Jackson St Peace St s o e d s e a l w e o e a T l M R P Rd Guess y Ramsuer i 420 ll R Durham d Tech OCC 85 Eno River State Park Vickers Av. -

11:00 AM to 1:00 PM

CHAPEL HILL TRANSIT Town of Chapel Hill 6900 Millhouse Road Chapel Hill, NC 27514-2401 phone (919) 969-4900 fax (919) 968-2840 www.townofchapelhill.org/transit CHAPEL HILL TRANSIT PUBLIC TRANSIT COMMITTEE NOTICE OF COMMITTEE MEETING AND AGENDA APRIL 28, 2015 – 11:00 A.M. to 1:00 P.M. CHAPEL HILL TRANSIT – FIRST FLOOR CONFERENCE ROOM PAGE # 1. Approval of March 24, 2105 Meeting Summary 1 2. Employee Recognition 3. Consent Items A. March Financial Report 4 4. Discussion Items A. FY2015-16 Budget Development 6 i. NU Route Cost Sharing ii. Capital Investment B. Service Requests 11 5. Information Items A. Long Range Financial Sustainability Study 36 B. Obey Creek Development Update 71 C. Safety/Risk Management Initiatives Update 81 D. March Performance Report 82 6. Departmental Monthly Reports A. Operations 84 B. Director 86 7. Future Meeting Items 89 8. Partner Items 9. Next Meeting – May 19, 2015 (11:00 a.m. – 1:00 p.m.) 10. Adjourn Chapel Hill Transit – Serving Chapel Hill, Carrboro and the University of North Carolina at Chapel Hill MEETING SUMMARY OF A REGULAR MEETING OF THE PUBLIC TRANSIT COMMITTEE 1ST FLOOR TRAINING ROOM, CHAPEL HILL TRANSIT Tuesday, March 24, 2015 at 11:00 AM Present: Jim Ward, Chapel Hill Town Council Ed Harrison, Chapel Hill Town Council Damon Seils, Carrboro Alderman Bethany Chaney, Carrboro Alderman Cheryl Stout, UNC Public Safety Than Austin, UNC Transportation Planner Julie Eckenrode, Assistant to Carrboro Town Manager Absent: Matt Czajkowski, Chapel Hill Town Council, Meredith Weiss, UNC Finance and Administration