The Performance of Acquisitions by High Default Risk Bidders

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Kevin Demirci Properties Limited Proposed Student Accommodation

Kevin Demirci Properties Limited Proposed student accommodation of 328 bedrooms and ancillary land uses, at land at Jockey Street, Swansea TRANSPORT ASSESSMENT October 2019 Applicant: Kevin Demirci Properties Limited Project no: T19.123 Document ref no: T19.123.D1 Document issue date: 22nd October 2019 Project name: Proposed student accommodation, Jockey Street, Swansea Offices at: Unit 9, Oak Tree Court Suite D, Mulberry Drive, Urban Village, Cardiff Gate Business Park, High Street, Cardiff, CF23 8RS Swansea, SA1 1NW Tel: 029 2073 2652 Tel: 01792 480535 K Watkins / P O’Connor CONTENTS 1.0 Introduction ................................................................................................... 1 2.0 Policy context ................................................................................................ 4 3.0 Existing situation ............................................................................................ 9 4.0 Development proposals ............................................................................... 21 5.0 Transport characteristics .............................................................................. 25 6.0 Summary and conclusions ............................................................................ 28 Figures Figure 3.1 Site location and local highway network Figure 3.2 Local public transport infrastructure Figure 3.3 Local amenities Figure 3.4 Cycling infrastructure Figure 3.5 Map of Personal Injury Collision data Figure 4.1 Proposed site access visibility splays Appendices Appendix -

Swansea Business Campus

Swansea Business Campus International Brochure About the University Swansea Campus The University of Wales Trinity Saint David (UWTSD) Founded in 1853, the Swansea was formed on 18 November 2010 through the campuses have a reputation for merger of the University of Wales Lampeter and innovative industry-led and Trinity University College Carmarthen, under career-driven programmes. Lampeter’s Royal Charter of 1828. On the 1 August 2013, Swansea Vibrant City Centre Campuses Metropolitan University became part of UWTSD. The University of Swansea, with its city-centre students easy access to shopping, Wales merged into the UWTSD campuses dedicated to art and recreation and relaxation in 2017. His Royal Highness, the design, business and management, opportunities plus a magnificent Prince of Wales is its Royal Patron. education, communities and beach and the stunning Gower Today, the University of Wales performance as well as architecture, coast just a few miles up the road. Trinity Saint David is a dynamic and computing and engineering, gives ambitions institution providing high quality education and research. ALEX Building, Swansea Campus The University is focussed on The University of Wales Trinity Saint enterprise and innovation, enabling David has been ranked top 20 best UK our staff and students to transform universities for academic experiences ideas into real opportunities and in The Times Higher Education solutions for business. Student Experience Survey 2017. The university is investing 300 UWTSD ranked 4th in the UK & 1st million pounds in the Swansea in Wales for ‘Teaching Quality’ in Waterfront Innovation Quarter, Business Studies. The University a multi-functional development in has also been ranked 4th for good Swansea’s former docks area which personal relationship with teaching will be made up of purpose-built staff, and joint 1st in Wales. -

Learning for Employment

Future Directions for Higher Education in Wales: Learning for Employment Contents 6. Introduction 7. Section 1: Authentic learning 8. BSc Applied Psychology award (case study G8) 9. Graduate Entry Medicine: Learning Opportunities in the Clinical Setting (LOCS) (case study S1) 11. GBS Sport (case study G6) 12. Enhancing employability: a case study of work-based learning as a complementary learning tool (case study CM11) 15. Developing coaching communities through rugby and football (case study G7) 17. Promoting employability and internationalisation for Modern Foreign Language students: a collaborative project between Cardiff University and Caldicot Comprehensive School (case study C7) 20. Supporting Computer Clubs for Girls (case study SM9) 21. Community Counselling Service (case study SM11) 23. School of Sport Student Volunteering module (case study CM6) 26. Working with parents: trainee teachers and the community (case study N4) 27. Problem Solver Initiative: Aberystwyth Magistrates’ Court (case study A4) 29. Live design (case study CM12) 31. Unknown Pleasures (case study SM2) 33. Production Based Project (case study SM10) 35. Section 2: Careers awareness and application skills 36. Newport BA (Hons) Education employability (case study N5) 37. PDP in Business Practice (case study N7) 40. Undergraduate student personal development planning (PDP) (case study A6) 41. Putting employability on the map: using online learning and assessment to promote professional development (case study CM5) 43. Assessment activity for final-year students in the Department of Sport and Exercise Science (case study A1) 44. Marketing, Promotion and Exhibition (Faculty of Art & Design, SMU) (case study SM5) 46. Support in application for gap in academic study and the University Partnership Programme (in partnership with the ICAEW) (case study C8) 48. -

Chude Member¾ 嗖

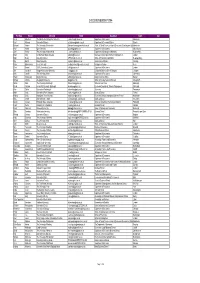

CHUDE MEMBERSHIP 2014 First Name Surname University E-Mail Department Town Sign Kevin Albertson The Manchester Metropolitan University [email protected] Department of Economics Manchester Paul Allanson University of Dundee [email protected] Department of Economic Studies Dundee Edmund Amann The University of Manchester [email protected] School of Social Sciences, Head of Economics (Teaching and Operations)Manchester Paul Anand Open University [email protected] Department of Economics Milton Keynes John Anchor The University of Huddersfield [email protected] Department of Strategy and Marketing Huddersfield Brian Ardy London South Bank University [email protected] Business, Computing & Information Management. London Mark Bailey University of Ulster [email protected] School of Economics and Politics Newtownabbey Ray Barrell Brunel University [email protected] Economics and Finance Uxbridge Robin Bladen-Hovell Keele University [email protected] Management School Keele Chris Bramall SOAS, University of London [email protected] Department of Economics London Jim Campbell Glasgow Caledonian University [email protected] Caledonian Business School Glasgow Glasgow Alan Carruth The University of Kent [email protected] Department of Economics Canterbury Shanti Chakravarty Bangor University [email protected] Bangor Business School Bangor Michael Christie Aberystywth University [email protected] School of Management and Business Aberystwyth Simon Clark The University of Edinburgh [email protected] -

Study Abroad at the University of Wales .Pdf

Study in Wales for the experience of a lifetime Lampeter’s relatively small size ensures Study abroad programme at students benefit from a close community atmosphere. When you just want to relax University of Wales Trinity outside and enjoy this rural idyll, there’s just the right spot. A river runs through the Saint David: campus, offering a lovely location in which to study and chat to friends. You won’t find hectic city life here. What The University of Wales Trinity Saint David has longstanding links with North you will discover is a vibrant small town that America, China, Japan, and Malaysia for study abroad. Our Study Abroad offers much more than you might expect. In Programme began in 1976 and, since then, the University has welcomed the 18th century Lampeter was an students to Wales from colleges and universities either on study abroad or for important place for the drovers who full-time undergraduate study. gathered herds of livestock to be walked all the way to the markets of south-east England. It must have been a busy place then and it is now. Just take a step outside the University’s gates and you are in Our campuses: the town. When you feel like exploring the wider area Lampeter Campus a trip to Carmarthen offers plenty of shops, restaurants, places of interest and entertainment and easy access to When you see the original campus and personal learning experience, having Swansea,Cardiff and London by train. buildings, you would be forgiven for found auniversity where they are known and thinking you have stumbled upon an valued as individuals. -

Big Data, Big Results How Data Can Advance Your Enterprise

Adolygiad Busnes De Cymru Vol 8 Issue 1 2021 Vol Big Data, Big Results How data can advance your enterprise Pandemic report: Tim O’Sullivan on NHS Wales’ fight against COVID-19 ShipShape VC’s Daniel Sawko wants your startup to harness the power of big data Welcoming a new Dean to UWTSD: meet pioneering Professor Wendy Dearing Swansea Business School Ysgol Fusnes Abertawe | SOUTH WALES BUSINESS REVIEW ADOLYGIAD BUSNES DE CYMRU | PRODUCTION TEAM Spring 2021 inside Volume 8 Issue 1 Editor: Kathryn Penaluna Editorial: Editorial Board: Sammy Jones Margaret Inman GET YOUR START IN ALL EYES ON CARDIGAN Big Data, 3 Editorial: 10 16 Nik White BIG DATA, BIG RESULTS DATA WITH A DATA APPRENTICESHIP POB LLYGAD AR ABERTEIFI Design & Print: 18 UWTSD TEL Department 4 The Big Big Results Interview: 12 In Conversation: 20 A TEN-MINUTE GUIDE TIM O'SULLIVAN STARTUP CHAMPION TO BIG DATA WITH DANIEL SAWKO NIK WHITEHEAD 6 FUTURE-PROOFING WITH HOZAH 14 USING DATA TO MANAGE 22 INTRODUCING PROFESSOR PEOPLE WELL WENDY DEARING 8 Review: LEARNING TABLEAU 2020 Kath Penaluna Editor Data drives so much of our world invisibly - and if you don’t know how to harness its power to inform, inspire and ignite your business, you can start to feel left behind. Luckily, there are a growing number of data pioneers in South Wales that are leading the way towards a better-informed, data-driven future. In this issue, we’re highlighting just a few homegrown talents using data to make South Wales a hotspot for innovation in investments, tourism and healthcare - to name just a few areas of expertise. -

Wales Graduation

DR MICHAEL CHAN PRESENTED DIPLOMAS TO 96 MBA AND 104 BA (HONS) GRADUATES AT THE GRADUATION CEREMONY OF THE UNIVERSITY OF WALES, UK The Graduation Ceremony of University of Wales, UK was successfully held on Sunday, 8 December 2012 at Chan Tak Tai Auditorium of The Lingnan University. At the graduation ceremony, 96 graduates of the Master of Business Administration, 104 graduates of the Bachelor of Arts (Hons) in Business Management programme as well as 4 Best Student Awards were presented by: • Dr Michael Chan, Executive Committee and Council Member of The Hong Kong Management Association and Executive Chairman of Café de Coral Holdings Ltd; • Mr Stephen Griffiths, Assistant Dean, Faculty of Business & Management, Swansea Metropolitan, and Head of Centre for International Development, Swansea Business School; • Mr John Poulton, Head of Glyndwr University London; and • Dr Victor Lee, Executive Director, The Hong Kong Management Association. During the ceremony, Dr Victor Lee shared with the graduates a simple message, “stay hungry, stay foolish” from the late Mr Steve Jobs. He further explained and said, “By staying hungry for knowledge, we never become complacent about what we have learnt; and staying foolish with a humble mind, we never stop questing for better ways to meeting challenges. …… Knowledge is power, power that enables you to face challenges ahead and weather storms in life!” University of Wales, UK Founded by Royal Charter in 1893, the University of Wales is the degree-awarding body for the majority of higher education students in Wales, and also for more than 120 other higher education institutions both within the United Kingdom and overseas, with which it also enjoys close links. -

Managing Diversity - Issues on the Coal Face

Wales Journal of Learning and Teaching in Higher Education 2020, Volume 2, 6-11 pp ISSN 2396-7285 (online) Edited by Simon K. Haslett Managing diversity - issues on the coal face. Antje Cockrill Swansea Business School, University of Wales Trinity Saint David, High Street, Swansea, SA1 1 NE, UK. Summary - Crynodeb Welsh higher education is increasingly focused on widening access and attracting more diverse student groups, in addition to increasing globalisation of the UK HE sector. The recruitment of diverse student cohorts impacts on teaching and learning experiences by presenting a range of challenges and opportunities. This paper presents and discusses the outcomes of a workshop entitled ‘Managing Diversity’ that was held at the Wales NEXUS Conference 2019. This workshop had the aim of exploring the experiences of staff who teach diverse student groups. The focus was on identifying challenges and opportunities, with a view of finding strategies to reduce challenges and exploit opportunities. Staff identified several key areas of challenge – issues related to staff self-awareness and self-reflection, challenges related to the management of learning in diverse groups, issues directly related teaching and learning tools, and resource related concerns. Key opportunities included the very real possibility of staff and students learning from each other’s experiences and to grow personally. Potential research was also seen as a positive aspect of diverse student groups. In addition, staff discussed a range of teaching tools able to aid the process of turning challenges into opportunities for enrichment. Mae addysg uwch yng Nghymru yn canolbwyntio’n gynyddol ar ehangu mynediad a denu grwpiau o fyfyrwyr mwy amrywiol, yn ogystal â chynyddu globaleiddio yn sector addysg uwch y DU. -

ABS PILLARS Whole

THE HIGH VALUE OF BUSINESS SCHOOLS TO THE ECONOMY AND SOCIETY 21ST CENTURY CURRICULUM WORKING SMARTER, LEANER AND GREENER INTERNATIONALISATION OF BUSINESS SCHOOLS THE HIGH VALUE OF BUSINESS SCHOOLS TO UNIVERSITIES PILLARS OF THE SUSTAINABLE ECONOMY PILLARS OF THE SUSTAINABLE 2010/11 OUR ROLE The Association of Business Schools (ABS) is the representative body and authoritative voice for all the leading business schools of UK universities, higher education institutions and independent management colleges. With over 100 members, ABS promotes the study of business and management to help improve the quality and effectiveness of managers in the UK and internationally. Formed in 1992, ABS works with similar organisations in Europe and around the world to influence the international management education community. OUR MISSION To promote the interests of our members and the business and management education, training, research and development they provide, nationally and internationally, so as to improve the quality and effectiveness of management, entrepreneurship and leadership for the benefit of society at large. The Association of Business Schools 137 Euston Road, London NW1 2AA Tel +44 (0)20 7388 0007 Fax +44 (0)20 7388 0009 Email [email protected] Web www.the-abs.org.uk PILLARS FOREWORD PROFESSOR HUW MORRIS 2-3 OF THE SUSTAINABLE THE YEAR IN FOCUS 4-8 ECONOMY A snapshot of some recent highlights, key developments 2010/11 and achievements of members CASE STUDIES > The High Value of Business Schools to Universities 10-11 > Internationalisation -

University of Wales: Trinity Saint David Charity Number: 1149535

University of Wales: Trinity Saint David Charity number: 1149535 Consolidated Financial Statements For the year ended 31 July 2020 UNIVERSITY OF WALES: TRINITY SAINT DAVID CONTENTS Pages Members 1 Administration details and professional advisors 2 Introduction by the Vice-Chancellor and the Chair of Council 4 Operating and financial review 6 Statement of corporate governance 21 Independent auditor’s report to the council of University of Wales: Trinity Saint David 26 Consolidated and University statements of comprehensive income 29 Consolidated and University statements of changes in reserves 30 Consolidated and University statements of financial position 31 Consolidated statement of cash flows 32 Statement of accounting policies 33 Notes to the accounts 40 UNIVERSITY OF WALES: TRINITY SAINT DAVID MEMBERS AND EXTERNAL ADVISORS The Trustees of the University who served during the year are listed below: The Venerable Randolph Thomas (Chair) Prof Medwin Hughes (Vice-Chancellor) Mrs Maria Stedman Mr Eifion Griffiths Mr Andrew Curl Mrs Pam Berry Mr Andrew Gibson Mrs Emma Hughes Mr Tony Ball Mrs Margaret Evans Mr Arwel Ellis Owen Dr Liz Siberry Ms Tania Davies Siân Eirian Mrs Eirlys Pritchard Jones Mr Rowland Jones Mr Geraint Roberts Victoria Provis Dr Gareth Hughes Ms Becky Ricketts (Resigned 30.06.2020) Ms Martha Warren (Resigned 30.06.2020) Mr James Mills (Appointed 01.07.2020) Miss Georgia Thomas (Appointed 01.07.2020) 1 UNIVERSITY OF WALES: TRINITY SAINT DAVID MEMBERS AND EXTERNAL ADVISORS Administrative Details Charity Number 1149535 -

Welsh Economic Review Welsh Economic Review

Welsh Economic Review Welsh Economic Review © Welsh Economy Research Unit 2006 ISSN 0965-2450 The Welsh Economic Review is produced twice yearly, by the Welsh Economy Research Unit (WERU) at Cardiff Business School. The aim of the Review is to provide an authoritative and objective analysis of the Welsh economy in a manner that promotes understanding and informs decision-making. The core section of the Review is written by members of WERU, with feature articles contributed by academics or practitioners within or outside Wales. The Review is circulated widely within Wales, to both private and public sector organisations, including the education sector and the Welsh Assembly Government. Notes for Contributors Authors should send papers for potential publication in the Welsh Economic Review to the Editor at the address given below, preferably via e-mail in a Word for Windows format. Papers are welcome on any topic that would be of general interest to the readership, and should be written in a style suitable for non-specialist readers. Papers should be approximately 3,000-4,000 words, and any graphs or figures should be accompanied by the underlying data to allow reproduction. Articles will be refereed within WERU. The Copyright for articles published in the Welsh Economic Review will be retained by WERU. Dr Jane Bryan, Editor, Welsh Economic Review , Welsh Economy Research Unit, Cardiff Business School, Aberconway Building, Colum Drive, Cardiff, CF10 3EU. Tel 029 2087 4173 Fax 020 2087 4419 e-mail [email protected] £35 Welsh Economic Review In November 2005 the Welsh Assembly published the consultation document ‘Wales: A Vibrant Economy’, which acknowledges that it is time to examine whether its economic development strategy is still fit for purpose. -

Thesis Submitted to Cardiff Metropolitan University in Partial Fulfilment of The

Enhancing International Students’ Experience in the UK through the Development of a Higher Education Co-opetition Framework: An Examination into Welsh Universities’ International Collaboration and Student Recruitment Activities Thesis submitted to Cardiff Metropolitan University in partial fulfilment of the requirement for the degree of Doctorate of Business Administration (DBA) This research was undertaken under the auspices of Cardiff School of Management | Cardiff Metropolitan University Director of Studies: Dr Jason Williams | Supervisor: Professor Tom Crick MBE Yi He (Edward) BEng (Hons) MBA (Dist) MRes CEng MIET May 2018 DECLARATION This work has not previously been accepted in any substance for any degree and it is not being concurrently submitted in candidature for any degree. Signed ………………………………… (Candidate) Date …………………………………… Statement 1 This work is the result of my own investigations, except where otherwise stated. Where correction services have been used, the extent and nature of the correction is clearly marked in a footnote(s). Other sources are acknowledged by footnotes giving explicit references. A bibliography is appended. Signed ………………………………… (Candidate) Date …………………………………… Statement 2 I hereby give consent for my dissertation, if accepted, to be available for photocopying and for inter-library loan, and for the title and summary to be made available to outside organisations. Signed ………………………………… (Candidate) Date …………………………………… I CYDNABYDDIAETHAU / ACKNOWLEDGEMENTS Yn gyntaf, hoffwn ddiolch i'm cyfarwyddwr astudiaethau, Dr Jason Williams, a'r goruchwyliwr, yr Athro Tom Crick MBE, am eich hyfforddiant, arweiniad a chefnogaeth aruthrol trwy gydol fy astudiaeth. Yn ail, hoffwn ddiolch i'r Athro Andrew Thomas, yr Athro Eleri Jones, Dr Richard Neil, Dr Claire Haven-Tang a'r tîm cefnogi ymchwil yn Ysgol Rheolaeth Caerdydd am eich help a'ch cyngor gwych.