1 Before the Hearing Examiner of the City Of

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Shigeru Ban, on Structural Design

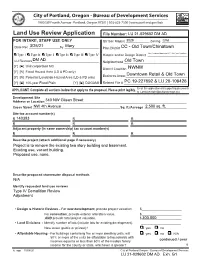

Land Use Review Application File Number: FOR INTAKE, STAFF USE ONLY Qtr Sec Map(s) _____________ Zoning ______________ Date Rec _________________by ___________________ Plan District _____________________________________ Type I Type Ix Type II Type IIx Type III Type IV Historic and/or Design District ______________________ LU Reviews _____________________________________ Neighborhood ___________________________________ [Y] [N] Unincorporated MC District Coalition _________________________________ [Y] [N] Flood Hazard Area (LD & PD only) [Y] [N] Potential Landslide Hazard Area (LD & PD only) Business Assoc __________________________________ [Y] [N] 100-year Flood Plain [Y] [N] DOGAMI Related File # ___________________________________ Email this application and supporting documents APPLICANT: Complete all sections below that apply to the proposal. Please print legibly. to: [email protected] Development Site Address or Location ______________________________________________________________________________ Cross Street ________________________________________________Sq. ft./Acreage _______________________ Site tax account number(s) R R R R R R Adjacent property (in same ownership) tax account number(s) R R R Describe project (attach additional page if necessary) Describe proposed stormwater disposal methods Identify requested land use reviews • Design & Historic Reviews - For new development, provide project valuation. $______________________ For renovation, provide exterior alteration value. $______________________ AND -

A Different Kind of Gentrification: Seattle and Its Relationship with Industrial Land

A Different Kind of Gentrification: Seattle and its Relationship with Industrial Land David Tomporowski A thesis submitted in partial fulfillment of the requirements for the degree of Master of Urban Planning University of Washington 2019 Committee: Edward McCormack Christine Bae Program Authorized to Offer Degree: Department of Urban Design and Planning College of Built Environments ©Copyright 2019 David Tomporowski University of Washington Abstract A Different Kind of Gentrification: Seattle and its Relationship with Industrial Land David Tomporowski Chair of the Supervisory Committee: Edward McCormack Department of Civil and Environmental Engineering / Department of Urban Design and Planning Industry in Seattle often talks about how they are facing their own kind of gentrification. Rising property values, encroaching pressure for different land uses, and choking transportation all loom as reasons for industrial businesses to relocate out of the city. This research explores this phenomenon of industrial gentrification through a case study of Seattle’s most prominent industrial area: the SODO (“South Of Downtown”) neighborhood. My primary research question asks what the perception and reality of the state of industrial land designation and industrial land use gentrification in Seattle is. Secondary research questions involve asking how industrial land designation and industrial land use can be defined in Seattle, what percentage of land is zoned industrial in the SODO neighborhood, and what percentage of the land use is considered industrial in the SODO neighborhood. Finally, subsequent effects on freight transportation and goods movement will be considered. By surveying actual industrial land use compared to i industrially-zoned land, one can conclude whether industry’s complaints are accurate and whether attempts to protect industrial land uses are working. -

2.86-Acres | 124395 Sf

2.86-acres | 124,395 sf REQUEST FOR PROPOSALS: unique development opportunity premier seattle land site located in south lake union INVESTMENT CONTACTS: Lori Hill Rob Hielscher Bob Hunt Managing Director Managing Director Managing Director Capital Markets International Capital Public Institutions +1 206 971 7006 +1 415 395 4948 +1 206 607 1754 [email protected] [email protected] [email protected] 601 Union Street, Suite 2800, Seattle, WA 98101 +1 206 607 1700 jll.com/seattle TABLE OF CONTENTS Section I The Offering 4 Introduction Investment Highlights Site Summary Objectives and Requirements Transaction Guidelines Section II Project Overview & Development Potential 17 South Lake Union Map and Legend Project Overview Zoning Zoning Map seattle Development Considerations Development Potential Section III RFP Process and Requirements 34 Solicitation Schedule Instructions and Contacts RFP Requirements Evaluation Process Post Selection Process Disclosures Section IV Market Characteristics 50 Market Overview Market Comparables Neighborhood Summary Regional Economy Section V Appendices 74 NORTH See page 75-76 for List of Appendix Documents Copyright ©2018 Jones Lang LaSalle. All rights reserved. Although information has been obtained from sources deemed reliable, Owner, Jones Lang LaSalle, and/or their representatives, brokers or agents make no guarantees as to the accuracy of the information contained herein, and offer the property without express or implied warranties of any kind. The property may be withdrawn without notice. If the recipient of this information has signed a confidentiality agreement regarding this matter, this information is subject to the terms of that agreement. Section I THE OFFERING 4 | Mercer Mega Block | Request for Proposals 520 REPLACE MERCER STREET LAKE UNION DEXTER AVE N ROY STREET ROY 99 NORTH Last large undeveloped site in South Lake Union | Mercer Mega Block | Request for Proposals 5 THE OFFERING INTRODUCTION MERCER MEGA BLOCK JLL is pleased to present the Mercer Mega Block, a 2.86-acre site acquisition opportunity. -

Major Offices, Including T- Mobile’S Headquarters Within the Newport Corporate Center, Due to Its Easy Access Along the I-90 Corridor

Commercial Revalue 2018 Assessment roll OFFICE AREA 280 King County, Department of Assessments Seattle, Washington John Wilson, Assessor Department of Assessments King County Administration Bldg. John Wilson 500 Fourth Avenue, ADM-AS-0708 Seattle, WA 98104-2384 Assessor (206)263-2300 FAX(206)296-0595 Email: [email protected] http://www.kingcounty.gov/assessor/ Dear Property Owners, Our field appraisers work hard throughout the year to visit properties in neighborhoods across King County. As a result, new commercial and residential valuation notices are mailed as values are completed. We value your property at its “true and fair value” reflecting its highest and best use as prescribed by state law (RCW 84.40.030; WAC 458-07-030). We continue to work hard to implement your feedback and ensure we provide accurate and timely information to you. We have made significant improvements to our website and online tools to make interacting with us easier. The following report summarizes the results of the assessments for your area along with a map. Additionally, I have provided a brief tutorial of our property assessment process. It is meant to provide you with background information about the process we use and our basis for the assessments in your area. Fairness, accuracy and transparency set the foundation for effective and accountable government. I am pleased to continue to incorporate your input as we make ongoing improvements to serve you. Our goal is to ensure every single taxpayer is treated fairly and equitably. Our office is here to serve you. Please don’t hesitate to contact us if you ever have any questions, comments or concerns about the property assessment process and how it relates to your property. -

1411 4Th Ave Seattle, WA 98101 Igniting Innovation and Imagination in the Heart of Seattle’S CBD

1411 4th Ave Seattle, WA 98101 Igniting Innovation and Imagination in the Heart of Seattle’s CBD Our historical location at 1411 4th Ave spans eleven floors of flexible office space in the heart of downtown Seattle. Close proximity to bus lines, the University Street Station light rail, and Pier 50 ferry terminal make getting here, and anywhere else in the city, easy. Some of Seattle’s best restaurants, cafés, bars, and attractions are within walking distance of the office, making your work day that much better. Whether you’re juicy burger or juice bar, happy hour or 5-star cuisine, in need of a single desk or an entire suite, you’ll find a progressive, welcoming community here that supports who you are and where you’re going. Examples of WeWork spaces 1411 4th Ave | 2 1411 4th Ave | 3 Where Historic Beauty Meets Modern Workspace The arresting art deco façade of this historic 1929 landmark building gives way to light-filled, modern workspace that welcomes members from across industries. Comprised of unique visual elements and curated art, our workplace is designed to capture the innovative, industrious spirit that is ingrained in the building. Amenities include a meditation room, a new mothers’/wellness room, unlimited micro-roasted coffee, and premium conference rooms and lounges that cultivate a collaborative, supportive community. Bike storage and showers onsite make bike commutes and midday workouts easier. And our dog-friendly policy means your four-legged muse can come to work every day. Whether you’re flying solo and need a single desk or have a large team and need a suite, you’ll find space here that motivates you to push harder and inspires you to go further. -

Seattle Times Building Complex—Printing Plant 1930-31; Addition, 1947

Seattle Times Building Complex—Printing Plant 1930-31; Addition, 1947 1120 John Street 1986200525 see attached page D.T. Denny’s 5th Add. 110 7-12 Onni Group Vacant 300 - 550 Robson Street, Vancouver, BC V6B 2B7 The Blethen Corporation (C. B. Blethen) (The Seattle Times) Printing plant and offices Robert C. Reamer (Metropolitan Building Corporation) , William F. Fey, (Metro- politan Building Corporation) Teufel & Carlson Seattle Times Building Complex—Printing Plant Landmark Nomination, October 2014 LEGAL DESCRIPTION: LOTS 7 THROUGH 12 IN BLOCK 110, D.T. DENNY’S FIFTH ADDITION TO NORTH SEAT- TLE, AS PER PLAT RECORDED IN VOLUME 1 OF PLATS, PAGE 202, RECORDS OF KING COUNTY; AND TOGETHER WITH THOSE PORTIONS OF THE DONATION CLAIM OF D.T. DENNY AND LOUIS DENNY, HIS WIFE, AND GOVERNMENT LOT 7 IN THE SOUTH- EAST CORNER OF SECTION 30, TOWNSHIP 25, RANGE 4 EAST, W. M., LYING WEST- ERLY OF FAIRVIEW AVENUE NORTH, AS CONDEMNED IN KING COUNTY SUPERIOR COURT CAUSE NO. 204496, AS PROVIDE BY ORDINANCE NO. 51975, AND DESCRIBED AS THAT PORTION LYING SOUTHERLY OF THOMAS STREET AS CONVEYED BY DEED RECORDED UNDER RECORDING NO. 2103211, NORTHERLY OF JOHN STREET, AND EASTERLY OF THE ALLEY IN SAID BLOCK 110; AND TOGETHER WITH THE VACATED ALLEY IN BLOCK 110 OF SAID PLAT OF D.T. DENNY’S FIFTH ADDITION, VACATED UNDER SEATTLE ORDINANCE NO. 89750; SITUATED IN CITY OF SEATTLE, COUNTY OF KING, STATE OF WASHINGTON. Evan Lewis, ONNI GROUP 300 - 550 Robson Street, Vancouver, BC V6B 2B7 T: (604) 602-7711, [email protected] Seattle Times Building Complex-Printing Plant Landmark Nomination Report 1120 John Street, Seattle, WA October 2014 Prepared by: The Johnson Partnership 1212 NE 65th Street Seattle, WA 98115-6724 206-523-1618, www.tjp.us Seattle Times Building Complex—Printing Plant Landmark Nomination Report October 2014, page i TABLE OF CONTENTS 1. -

AMAZON 601 Pine Project Package 6-25-20

PINE FLAGSHIP RETAIL IN THE HEART OF DOWNTOWN SEATTLE Convention Center Expansion (opening 2022) Hyatt Regency 1,260 rooms 105,000 sf Exhibition 7TH AVENUE ART ST ART ART ST ART W W 6TH AVENUE Y Y A A STE STE W W 383,000 SF OLIVE OLIVE City Flagship Store PIKE STREET PIKE STREET PINE STREETPINE STREET Center 5TH AVENUE STREETCAR 4TH AVENUE 3RD AVENUE 340 units Condo Planned Chromer 500 units 2ND AVENUE fice f VIRGINIA ST VIRGINIA woPine T The Emerald 125,000 SF o 38 stories of condos 1ST AVENUE Seattle Art Museum are all a short walk from 601 Pine. all a short walk from Seattle Art Museum are world-renowned Pike Place Market, The Paramount Theater, the Washington State Convention & Trade Center and the Trade Convention & State the Washington The Paramount Theater, Place Market, Pike world-renowned crossroads of the urban core, Seattle’s shopping, cultural, financial and entertainment districts and Capitol Hill. The entertainment districts cultural, financial and shopping, Seattle’s core, of the urban crossroads of workers and visitors from around the globe to experience this one-of-a-kind urban setting. 601 Pine is situated at the around of workers and visitors from sports, art and cultural events and a variety of retail and dining options, Downtown Seattle draws a diverse cross section cross a diverse Seattle draws Downtown dining options, and retail of cultural events and a variety and art sports, community, 29 parks, a focus on environmental sustainability, state-of-the-art venues for conventions, professional conventions, professional state-of-the-art venues for sustainability, focus on environmental a 29 parks, community, centers for commerce, development and culture. -

Downtown Seattle

Commercial Revalue 2015 Assessment Roll AREA 30 King County, Department of Assessments Seattle, Wa. Lloyd Hara, Assessor Department of Assessments Accounting Division Lloyd Hara 500 Fourth Avenue, ADM-AS-0740 Seattle, WA 98104-2384 Assessor (206) 205-0444 FAX (206) 296-0106 Email: [email protected] http://www.kingcounty.gov/assessor/ Dear Property Owners: Property assessments for the 2015 assessment year are being completed by my staff throughout the year and change of value notices are being mailed as neighborhoods are completed. We value property at fee simple, reflecting property at its highest and best use and following the requirement of RCW 84.40.030 to appraise property at true and fair value. We have worked hard to implement your suggestions to place more information in an e-Environment to meet your needs for timely and accurate information. The following report summarizes the results of the 2015 assessment for this area. (See map within report). It is meant to provide you with helpful background information about the process used and basis for property assessments in your area. Fair and uniform assessments set the foundation for effective government and I am pleased that we are able to make continuous and ongoing improvements to serve you. Please feel welcome to call my staff if you have questions about the property assessment process and how it relates to your property. Sincerely, Lloyd Hara Assessor Area 30 Map The information included on this map has been compiled by King County staff from a variety of sources and is subject to change without notice. -

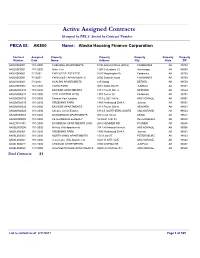

Active Contracts to Be Posted On

Active Assigned Contracts Grouped by PBCA Sorted by Contract Number PBCA ID:AK800 Name: Alaska Housing Finance Corporation Contract Assigned Property Property Property Property Property Number Date Name Address City State ZIP AK020002001 11/1/2000 CHENANA APARTMENTS 5190 Amherst Drive (office) FAIRBANKS AK 99709 AK020003001 11/1/2000 Glen, The 1200 Columbine Ct Anchorage AK 99508 AK020004001 7/1/2001 EXECUTIVE ESTATES 1620 Washington Dr Fairbanks AK 99709 AK020005001 7/1/2001 PARKWEST APARTMENTS 2006 Sandvik Road FAIRBANKS AK 99709 AK020006001 7/1/2001 AYALPIK APARTMENTS 105 Atsaq BETHEL AK 99559 AK020007002 12/1/2004 COHO PARK 3601 AMALGA ST JUNEAU AK 99801 AK02M000010 11/1/2000 BAYSIDE APARTMENTS 1011 Fourth Street SEWARD AK 99664 AK02M000011 11/1/2000 LITTLE DIPPER APTS 1910 Turner St Fairbanks AK 99701 AK02M000012 11/1/2000 Chester Park Estates 1019 E 20TH AVE ANCHORAGE AK 99501 AK02M000016 11/1/2000 GRUENING PARK 1800 Northwood Dr # A Juneau AK 99801 AK02M000022 11/1/2000 BAYSIDE APARTMENTS 1011 Fourth Street SEWARD AK 99664 AK02M000023 11/1/2000 Chester Creek Estates 5814 E NORTHERN LIGHTS ANCHORAGE AK 99504 AK02R000003 11/1/2000 WOODRIDGE APARTMENTS 903 Cook Street KENAI AK 99611 AK02R000004 11/1/2000 PETERSBURG ELDERLY 16 North 12th ST PETERSBURG AK 99833 AK02T851001 11/1/2000 DAYBREAK APARTMENTS (CMI) 2080 HEMMER RD PALMER AK 99645 AK06E000005 11/1/2000 McKay Villa Apartments 3741 Richmond Avenue ANCHORAGE AK 99508 AK06L000001 11/1/2000 GRUENING PARK 1800 Northwood Dr # A Juneau AK 99801 AK06L000003 11/1/2000 NORTH WIND APARTMENTS -

Seattle Commercial Core Neighborhood Plan Land Use and Urban Design Summary

Seattle Commercial Core Neighborhood Plan Land Use and Urban Design Summary February 1999 Seattle Commercial Core Neighborhood Plan Presentation Summary Prepared by Commercial Core MAKERS architecture Planning Committee and urban design Kate Joncas, Co-Chair Gerald Hansmire, Jerry Ernst, Co-Chair Lead Consultant Nancy Bagley Catherine Maggio, Jean Bateman Project Manager Brad Bigelow Dave Boyd Jill Curtis Stefani Wildhaber Barbra Edl Nakano Dennis Tom Gerlach Landscape Architects Mark Hewitt Kenichi Nakano Bob Hinckley Theresa Neylon Paul Kalanick Paul Lambros Ravenhurst Development Lois Laughlin Corporation Karin Link Darrel Vange Ed Marquand Jan O’Conner Adrienne Quinn Ray Serebrin Greg Smith Jan Stimach Catherine Stanford Bernie Walter Sponsored by Xy of Seattle City of Seattle Neighborhood Planning Office Strategic Planning Office John Eskelin Dennis Meier Robert Scully Contents Vision ................................................................................................................. 1 Purpose and Context ........................................................................................ 3 Seattle’s Comprehensive Plan ................................................................................................... 3 Downtown Urban Center Plan .................................................................................................... 3 Commercial Core Neighborhood Plan ........................................................................................ 4 Goals and Policies ........................................................................................... -

20000 SF+ Non-Residential Multifamily Buildings

Seattle Energy Benchmarking Ordinance | 20,000 SF+ Non‐Residential Multifamily Buildings ‐ Required to Report Dec 2015 Data IMPORTANT: This list may not indicate all buildings on a parcel and/or all buildings subject to the ordinance. Building types subject to the ordinance as defined in the Director's Rule need to report, regardless of whether or not they are listed below. The Building Name, Building Address and Gross Floor Area were derived from King County Assessor records and may differ from the actual building. Please confirm the building information prior to benchmarking and email corrections to: [email protected]. SEATTLE GROSS FLOOR BUILDING NAME BUILDING ADDRESS BUILDING ID AREA (SF) 1MAYFLOWER PARK HOTEL 405 OLIVE WAY, SEATTLE, WA 98101 88,434 2 PARAMOUNT HOTEL 724 PINE ST, SEATTLE, WA 98101 103,566 3WESTIN HOTEL 1900 5TH AVE, SEATTLE, WA 98101 961,990 5HOTEL MAX 620 STEWART ST, SEATTLE, WA 98101 61,320 8WARWICK SEATTLE HOTEL 401 LENORA ST, SEATTLE, WA 98121 119,890 9WEST PRECINCT (SEATTLE POLICE) 810 VIRGINIA ST, SEATTLE, WA 98101 97,288 10 CAMLIN WORLDMARK HOTEL 1619 9TH AVE, SEATTLE, WA 98101 83,008 11 PARAMOUNT THEATER 901 PINE ST, SEATTLE, WA 98101 102,761 12 COURTYARD BY MARRIOTT ‐ ALASKA 612 2ND AVE, SEATTLE, WA 98104 163,984 13 LYON BUILDING 607 3RD AVE, SEATTLE, WA 98104 63,712 15 HOTEL MONACO 1101 4TH AVE, SEATTLE, WA 98101 153,163 16 W SEATTLE HOTEL 1112 4TH AVE, SEATTLE, WA 98101 333,176 17 EXECUTIVE PACIFIC PLAZA 400 SPRING ST, SEATTLE, WA 98104 65,009 18 CROWNE PLAZA 1113 6TH AVE, SEATTLE, WA 98101 -

1998 Seattle NATCA Convention Complete Transcript

*************************************** * * * * * * * * * NATCA * * * * * * 7TH BIENNIAL CONVENTION * * * * * * SEATTLE, WASHINGTON * * * * * * SEPTEMBER 5-8 * * * * * * 1998 * * * * * * * * * *************************************** A COURT REPORTING SERVICE CERTIFIED COURT REPORTERS 1620 FIRST INTERSTATE CENTER 999 THIRD AVENUE SEATTLE, WASHINGTON 98104 FAX (206) 389-9329 PHONE(206) 624-0316 [email protected] REPORTED BY: PAUL J. FREDERICKSON, CCR, RPR SEPTEMBER 5, 1998 [9:25 a.m.] PRESIDENT McNALLY: Okay. If everybody will take their seats, please. The Seventh Biennial Convention of the National Air Traffic Controllers Association will come to order. I would like to welcome everybody here in Seattle. Welcome. [Applause.] PRESIDENT McNALLY: If I can, I would like to do just a few brief introductions, and then we have some speakers. Hopefully the time will work. What I would like to do is take the opportunity to introduce members of your executive board at this time. So what I'm going to do is I'm going to go alphabetical by last name, not by region. I would like to introduce to you Mike Blake, New England Vice President, Regional Vice President. [Applause.] PRESIDENT McNALLY: And of course the nickname for Mike these days is the "Northeastern Region Rep." I would like to introduce Eastern Region Vice President, Joe Fruscella. [Applause.] PRESIDENT McNALLY: And, of course, the nickname for him is the "Southern New England Region Rep" these days. Those are jokes here, guys. [Laughter.] PRESIDENT McNALLY: Okay. The next introduction is James Ferguson, Northwest Mountain Regional Vice President. [Applause.] PRESIDENT McNALLY: And he's known for "Stay out of my backyard." Okay. We have Gus Guerra, Western Pacific Regional Vice President.