Helios Apartments (Hartsville)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Shigeru Ban, on Structural Design

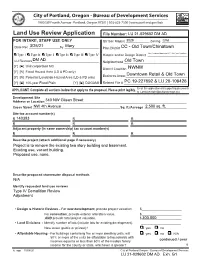

Land Use Review Application File Number: FOR INTAKE, STAFF USE ONLY Qtr Sec Map(s) _____________ Zoning ______________ Date Rec _________________by ___________________ Plan District _____________________________________ Type I Type Ix Type II Type IIx Type III Type IV Historic and/or Design District ______________________ LU Reviews _____________________________________ Neighborhood ___________________________________ [Y] [N] Unincorporated MC District Coalition _________________________________ [Y] [N] Flood Hazard Area (LD & PD only) [Y] [N] Potential Landslide Hazard Area (LD & PD only) Business Assoc __________________________________ [Y] [N] 100-year Flood Plain [Y] [N] DOGAMI Related File # ___________________________________ Email this application and supporting documents APPLICANT: Complete all sections below that apply to the proposal. Please print legibly. to: [email protected] Development Site Address or Location ______________________________________________________________________________ Cross Street ________________________________________________Sq. ft./Acreage _______________________ Site tax account number(s) R R R R R R Adjacent property (in same ownership) tax account number(s) R R R Describe project (attach additional page if necessary) Describe proposed stormwater disposal methods Identify requested land use reviews • Design & Historic Reviews - For new development, provide project valuation. $______________________ For renovation, provide exterior alteration value. $______________________ AND -

2.86-Acres | 124395 Sf

2.86-acres | 124,395 sf REQUEST FOR PROPOSALS: unique development opportunity premier seattle land site located in south lake union INVESTMENT CONTACTS: Lori Hill Rob Hielscher Bob Hunt Managing Director Managing Director Managing Director Capital Markets International Capital Public Institutions +1 206 971 7006 +1 415 395 4948 +1 206 607 1754 [email protected] [email protected] [email protected] 601 Union Street, Suite 2800, Seattle, WA 98101 +1 206 607 1700 jll.com/seattle TABLE OF CONTENTS Section I The Offering 4 Introduction Investment Highlights Site Summary Objectives and Requirements Transaction Guidelines Section II Project Overview & Development Potential 17 South Lake Union Map and Legend Project Overview Zoning Zoning Map seattle Development Considerations Development Potential Section III RFP Process and Requirements 34 Solicitation Schedule Instructions and Contacts RFP Requirements Evaluation Process Post Selection Process Disclosures Section IV Market Characteristics 50 Market Overview Market Comparables Neighborhood Summary Regional Economy Section V Appendices 74 NORTH See page 75-76 for List of Appendix Documents Copyright ©2018 Jones Lang LaSalle. All rights reserved. Although information has been obtained from sources deemed reliable, Owner, Jones Lang LaSalle, and/or their representatives, brokers or agents make no guarantees as to the accuracy of the information contained herein, and offer the property without express or implied warranties of any kind. The property may be withdrawn without notice. If the recipient of this information has signed a confidentiality agreement regarding this matter, this information is subject to the terms of that agreement. Section I THE OFFERING 4 | Mercer Mega Block | Request for Proposals 520 REPLACE MERCER STREET LAKE UNION DEXTER AVE N ROY STREET ROY 99 NORTH Last large undeveloped site in South Lake Union | Mercer Mega Block | Request for Proposals 5 THE OFFERING INTRODUCTION MERCER MEGA BLOCK JLL is pleased to present the Mercer Mega Block, a 2.86-acre site acquisition opportunity. -

AMAZON 601 Pine Project Package 6-25-20

PINE FLAGSHIP RETAIL IN THE HEART OF DOWNTOWN SEATTLE Convention Center Expansion (opening 2022) Hyatt Regency 1,260 rooms 105,000 sf Exhibition 7TH AVENUE ART ST ART ART ST ART W W 6TH AVENUE Y Y A A STE STE W W 383,000 SF OLIVE OLIVE City Flagship Store PIKE STREET PIKE STREET PINE STREETPINE STREET Center 5TH AVENUE STREETCAR 4TH AVENUE 3RD AVENUE 340 units Condo Planned Chromer 500 units 2ND AVENUE fice f VIRGINIA ST VIRGINIA woPine T The Emerald 125,000 SF o 38 stories of condos 1ST AVENUE Seattle Art Museum are all a short walk from 601 Pine. all a short walk from Seattle Art Museum are world-renowned Pike Place Market, The Paramount Theater, the Washington State Convention & Trade Center and the Trade Convention & State the Washington The Paramount Theater, Place Market, Pike world-renowned crossroads of the urban core, Seattle’s shopping, cultural, financial and entertainment districts and Capitol Hill. The entertainment districts cultural, financial and shopping, Seattle’s core, of the urban crossroads of workers and visitors from around the globe to experience this one-of-a-kind urban setting. 601 Pine is situated at the around of workers and visitors from sports, art and cultural events and a variety of retail and dining options, Downtown Seattle draws a diverse cross section cross a diverse Seattle draws Downtown dining options, and retail of cultural events and a variety and art sports, community, 29 parks, a focus on environmental sustainability, state-of-the-art venues for conventions, professional conventions, professional state-of-the-art venues for sustainability, focus on environmental a 29 parks, community, centers for commerce, development and culture. -

Active Contracts to Be Posted On

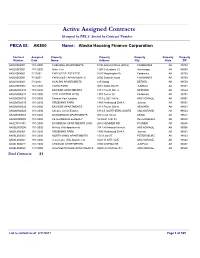

Active Assigned Contracts Grouped by PBCA Sorted by Contract Number PBCA ID:AK800 Name: Alaska Housing Finance Corporation Contract Assigned Property Property Property Property Property Number Date Name Address City State ZIP AK020002001 11/1/2000 CHENANA APARTMENTS 5190 Amherst Drive (office) FAIRBANKS AK 99709 AK020003001 11/1/2000 Glen, The 1200 Columbine Ct Anchorage AK 99508 AK020004001 7/1/2001 EXECUTIVE ESTATES 1620 Washington Dr Fairbanks AK 99709 AK020005001 7/1/2001 PARKWEST APARTMENTS 2006 Sandvik Road FAIRBANKS AK 99709 AK020006001 7/1/2001 AYALPIK APARTMENTS 105 Atsaq BETHEL AK 99559 AK020007002 12/1/2004 COHO PARK 3601 AMALGA ST JUNEAU AK 99801 AK02M000010 11/1/2000 BAYSIDE APARTMENTS 1011 Fourth Street SEWARD AK 99664 AK02M000011 11/1/2000 LITTLE DIPPER APTS 1910 Turner St Fairbanks AK 99701 AK02M000012 11/1/2000 Chester Park Estates 1019 E 20TH AVE ANCHORAGE AK 99501 AK02M000016 11/1/2000 GRUENING PARK 1800 Northwood Dr # A Juneau AK 99801 AK02M000022 11/1/2000 BAYSIDE APARTMENTS 1011 Fourth Street SEWARD AK 99664 AK02M000023 11/1/2000 Chester Creek Estates 5814 E NORTHERN LIGHTS ANCHORAGE AK 99504 AK02R000003 11/1/2000 WOODRIDGE APARTMENTS 903 Cook Street KENAI AK 99611 AK02R000004 11/1/2000 PETERSBURG ELDERLY 16 North 12th ST PETERSBURG AK 99833 AK02T851001 11/1/2000 DAYBREAK APARTMENTS (CMI) 2080 HEMMER RD PALMER AK 99645 AK06E000005 11/1/2000 McKay Villa Apartments 3741 Richmond Avenue ANCHORAGE AK 99508 AK06L000001 11/1/2000 GRUENING PARK 1800 Northwood Dr # A Juneau AK 99801 AK06L000003 11/1/2000 NORTH WIND APARTMENTS -

Mid-Rise/Mixed-Use Design Studio

Mid-Rise/Mixed-Use Design Studio 1 Radius SLU Roof Deck 2 We know urban mid-rise. For over 30 years Weber Thompson has been designing highly successful mid-rise multifamily projects within the city’s urban fabric. We understand the market forces, city requirements and complicated technical necessities this type of building demands. This depth of experience allows us to focus on the design and craft a high quality building without busting the budget or schedule. Most of the mid-rise multifamily projects we design have a context – they exist within a community and among buildings that establish design constraints and opportunities. What we design are very much neighborhood buildings. Design in context, sensitive to the scale and character of surrounding buildings, will be essential as your project evolves from planning to architectural design. 3 Pike Motorworks 4 MEET OUR Mid-Rise Team Amanda Keating AIA, LEED® AP BD+C SENIOR PRINCIPAL / PRINCIPAL IN CHARGE Amanda bridges the gap between aesthetic judgment and technical understanding. She manages the design, documentation and construction administration of large-scale, mixed use projects with the firm’s mid-rise group. Amanda is renowned for her thoughtful, even-keeled approach and calm management style. She is also a core member of Weber Thompson’s highly energized Sustainabiliteam. Jeff Reibman AIA, NCARB, LEED® AP BD+C SENIOR PRINCIPAL / PRINCIPAL IN CHARGE For over 20 years Jeff has been working in the Seattle area with a focus on residential design of every kind. Throughout his career, he has developed his expertise in creative land use solutions and complex entitlement processes. -

Market Programs Packet

Market Programs Committee Meeting Agenda DUE TO THE EXTRAORDINARY PUBLIC HEALTH CIRCUMSTANCES RELATED TO THE ONGOING COVID- 19 (CORONAVIRUS) OUTBREAK, PARTICIPATION IN THIS MEETING WILL BE VIRTUAL OR TELEPHONIC. ALL PDA COUNCILMEMBERS WILL PARTICIPATE REMOTELY. Date: Tuesday, November 3, 2020 Time: 4:00 p.m. – 6:00 p.m. Location: https://us02web.zoom.us/j/89598090263?pwd=KzZaWXZnRTJqSWVTa0lhckZUWUhzZz09 OR dial +1 253 215 8782, Meeting ID: 895 9809 0263, password: 956553 Committee Members: Patrice Barrentine (Chair), Paul Neal (Vice-Chair), David Ghoddousi, Colleen Bowman, Mark Brady, Gordie McIntyre 4:00pm I. Administrative Chair A. Approval of Agenda B. Approval of the Market Programs Committee Meeting Minutes for October 13, 2020 4:05pm II. Announcements and/or Community Comments Chair 4:15pm III. Programs and Marketing Report Amy Wallsmith, Madison Bristol, Tanya Sinkovits 4:50pm IV. Reports and Discussion Items A. Upcoming Farm Survey Carter Grant B. Fall & Holiday Programming Amy Wallsmith 5:45pm V. Public Comment Chair 5:50pm VI. Concerns of Committee Members Chair 6:00pm VII. Adjournment Chair Pike Place Market Preservation & Development Authority (PDA) · [email protected] · pikeplacemarket.org P: 206.682.7453 · F: 206.625.0646 · 85 Pike Street, Room 500 · Seattle, WA 98101 Page 1 Page 2 Market Programs Committee z Meeting Minutes DUE TO THE EXTRAORDINARY PUBLIC HEALTH CIRCUMSTANCES RELATED TO THE ONGOING COVID-19 (CORONAVIRUS) OUTBREAK, PARTICIPATION IN THIS MEETING WILL BE VIRTUAL OR TELEPHONIC. ALL PDA COUNCILMEMBERS -

632970 1.Pdf

Downtown Seattle is the central, driving force for the vitality of the city, state and region. It is among the top international centers for commerce, development and culture. With a growing high-tech, biotech, global health and philanthropic community, 29 parks, a focus on environmental sustainability, state-of-the-art venues for conventions, professional sports, art and cultural events and a variety of retail and dining options, Downtown Seattle draws a diverse cross section of workers and visitors from around the globe to experience this one-of-a-kind urban setting. The Meridian is positioned at the heart of this urban core and at the crossroads of Seattle’s main shopping, culture, financial and entertainment districts. The world-renowned Pike Place Market, Benaroya Symphony Hall, The Paramount Theater, The Fifth Avenue Theater, Seattle Art Museum, Pacific Place, The Washington State Convention Center, and over 6,400 hotel rooms are all located within a three block walk of the site. DOWNTOWN SEATTLE RETAILSTREETDowntown CORE MAP MAP Seattle Core Map Consisting of 24 blocks of retail containing more than 1.5 million square feet, Seattle’s downtown core has one of the lowest retail vacancy rates in the country. The Meridian is located between the Washington State Convention Center and Pacific Place in the Pike/Pine Corridor, Seattle’s premier shopping area. Providing unmatched access to the downtown shopper. The Meridian’s neighbors include Nordstrom’s Flagship store, Macy’s Redevelopment, City Target, Zara, Anthropologie, Sephora, Urban -

Malaysia Real Estate Highlights

RESEARCH REAL ESTATE HIGHLIGHTS 2ND HALF 2018 Photo by KUALA LUMPUR PENANG JOHOR BAHRU KOTA KINABALU HIGHLIGHTS KUALA LUMPUR HIGH END CONDOMINIUM MARKET There were noticeably more completions and launches during the review period. ECONOMIC AND MARKET 53,033 units following the completion of INDICATORS four projects during the review period. They are Ruma Residences (199 units), Prices of high-end condominiums Malaysia’s economy recorded sustained Pavilion Suites (383 units), Premium / serviced apartments remained growth at 4.4% in the 3Q2018 (2Q2018: Residences @ KL Gateway (466 units) resilient in the secondary market. 4.5%), driven mainly by expansion in and Dorsett Residences Sri Hartamas As for the lettings market, there domestic demand and higher private (707 units). was a marginal rental decline in investment. The country’s GDP for the Damansara Heights. whole year of 2018 is expected to be in By 1H2019, the scheduled completions the region of 4.8%. of Inwood Residences @ Pantai Sentral Park (211 units), One Kiara – Block A Slight upward revision in stamp The headline inflation at 0.5% in 3Q2018 (118 units), Residensi Sefina (245 units) duty and real property gains tax was the lowest since 1Q2015 (0.7%) and Opus KL (357 units) will collectively (RPGT) rates as announced in following the 3-month tax holiday from contribute an additional 931 units to the Budget 2019 unlikely to have June until September. Overall headline existing stock. significant impact on the high- inflation is expected to ease to 2.0% this end condominium market. year (2017: 3.7%). During the review period, there were noticeably more previews and launches The labour market conditions continued compared to 1H2018. -

Seattle New Construction & Proposed Multifamily Projects 3Q17

Seattle New Construction & Proposed Multifamily Projects 3Q17 ID PROPERTY UNITS 167 2218 1st Avenue 66 1 Stratus 430 168 2801 Elliott Avenue 61 2 AMLI Arc 393 169 3031 Western Avenue 100 5 Cora 75 137 232 170 307 Broad 149 9 Broadcast 74 171 408 Aurora Avenue North 78 11 Helios 398 172 427 9th Avenue North 242 12 Cascade 477 173 4th & Bell Tower 287 Total Lease-Up 1,847 174 5th & Lenora 470 15 John Street & Fairview Avenue North 1128 175 5th & Virginia 431 176 600 Wall Street 370 16 Esterra Park Blocks 5, 6A and 9 658 70 20 Alexan Central Park 193 177 601 Aurora Avenue North 123 21 Arrive 339 135 134 178 901 Harrison Street 292 25 AVA at Esterra Park 323 179 Altitude Residences 236 26 Danforth, The 265 180 Antioch University Site 1036 28 Bellevue Vuecrest 137 181 Block V 638 29 425 Fairview 430 182 Communita Atelier 98 30 Sitka 384 183 Emerald, The 266 141 31 Hugo House 80 139 140 184 F. X. McRory Building Redevelopment 55 32 Broadstone First Hill 350 136 233 185 Mercer Blocks, Block 25 West 83 34 Redmond 148 244 186 Mercer Blocks, Block 31 81 285 307 289 35 970 Denny 461 286 185 184 187 Rainier Square Redevelopment 200 36 McKenzie 450 142 176 188 Seattle Times Building 433 197 46 Anthology 400 284 59 189 Shilla Tower 286 47 2100 East Madison 50 304 190 St. Johns 430 48 2220 East Union 144 5 170 181 171 161 191 Third & Lenora 384 138 305 28 51 Valdok, The 177 192 722 East Pike Street 90 72 60 53 Metro 112 Phase II 57 177 193 800 Columbia Street 274 59 Westridge Phase II 50 283 29 194 Crosby Capitol Hill 50 195 Esker 70 60 624 Yale 206 -

1 Before the Hearing Examiner of the City Of

1 2 3 4 5 6 7 8 9 10 11 12 BEFORE THE HEARING EXAMINER OF THE CITY OF SEATTLE 13 14 15 In re Proposed Final Assessment Roll for Case Nos. CWF-0318, 0410, 0411, 0412, 0413, 16 Local Improvement District No. 6751 0414, 0415, 0416, 0417, 0418, 0420, 0421, 0422, 17 (“Waterfront LID”) 0423, 0425, 0426, 0427, 0429, 0430, 0431, 0432, 18 0433, 0434, 0435, 0436, 0437, 0438, 0439, 0440, 19 Parcel Nos.: 0441 20 21 6094670010; 6094670020; 6094670030; WITNESS AND EXHIBIT LIST FOR 22 6094680050; 0660000740; 0660000708; HEARING ON APRIL 14, 2020 23 2285130010; 6792120010; 6195000030; 24 0942000430; 6792120020; 7683890010; 25 1976200070; 1976200075; 1976200076; 26 7666202465; 7666202345; 1975700365; 27 0696000015; 1974700175; 1117080020; 28 1975700235; 0696000055; 0660000540 29 0660000545; 066000-0575; 2538831460; 30 2538831480; 0939000240; 1974600025; 31 1974600035 32 33 34 35 36 Witness List – April 14, 2020 37 38 Name Email Address 39 40 41 John Gordon Testifying regarding his appraisal [email protected] 42 of the Seattle Tower I (Sound 43 Hotel and Arrive Apartments), 44 Marriott Seattle Waterfront, and 45 the Four Seasons 46 47 Perkins Coie LLP WITNESS AND EXHIBIT LIST - 1 The PSE Building 10885 N.E. Fourth Street, Suite 700 Bellevue, WA 98004-5579 147861867.1 Phone: 425.635.1400 Fax: 425.635.2400 1 Brian Testifying regarding the Helios [email protected] 2 Apartments 3 O’Connor 4 5 Anthony Testifying regarding the impact of [email protected] 6 COVID-19 7 Gibbons 8 9 10 11 Exhibit List – April 14, 2020 12 13 Exhibit Description 14 15 16 85 Appraisal Review for the Seattle Tower I building, the Sound Hotel and Arrive 17 Apartments, Case No. -

Vanguard U.S. Sector Index Funds Annual Report August 31, 2020

Annual Report | August 31, 2020 Vanguard U.S. Sector Index Funds Vanguard Communication Services Index Fund Vanguard Consumer Discretionary Index Fund Vanguard Consumer Staples Index Fund Vanguard Energy Index Fund Vanguard Financials Index Fund Vanguard Health Care Index Fund Vanguard Industrials Index Fund Vanguard Information Technology Index Fund Vanguard Materials Index Fund Vanguard Utilities Index Fund See the inside front cover for important information about access to your fund’s annual and semiannual shareholder reports. Important information about access to shareholder reports Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of your fund’s annual and semiannual shareholder reports will no longer be sent to you by mail, unless you specifically request them. Instead, you will be notified by mail each time a report is posted on the website and will be provided with a link to access the report. If you have already elected to receive shareholder reports electronically, you will not be affected by this change and do not need to take any action. You may elect to receive shareholder reports and other communications from the fund electronically by contacting your financial intermediary (such as a broker-dealer or bank) or, if you invest directly with the fund, by calling Vanguard at one of the phone numbers on the back cover of this report or by logging on to vanguard.com. You may elect to receive paper copies of all future shareholder reports free of charge. If you invest through a financial intermediary, you can contact the intermediary to request that you continue to receive paper copies. -

Lead Plaintiff's Motion for Final Approval Of

Case 1:18-cv-06965-JGK Document 136 Filed 04/01/21 Page 1 of 37 UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK Case No. 1:18-CV-06965-JGK IN RE HELIOS AND MATHESON ANALYTICS, INC. SECURITIES CLASS ACTION LITIGATION DECLARATION OF SHANNON L. HOPKINS IN SUPPORT OF (1) LEAD PLAINTIFF’S MOTION FOR FINAL APPROVAL OF CLASS ACTION SETTLEMENT AND PLAN OF ALLOCATION AND FINAL CERTIFICATION OF SETTLEMENT CLASS, AND (2) LEAD COUNSEL’S MOTION FOR AN AWARD OF ATTORNEYS’ FEES, REIMBURSEMENT OF EXPENSES, AND INCENTIVE AWARDS TO LEAD PLAINTIFF Case 1:18-cv-06965-JGK Document 136 Filed 04/01/21 Page 2 of 37 TABLE OF CONTENTS I. PRELIMINARY STATEMENT ........................................................................................ 1 II. FACTUAL AND PROCEDURAL BACKGROUND........................................................ 6 A. Summary of the Claims and Allegations ............................................................................ 6 B. Procedural History .............................................................................................................. 8 C. Mediation and Settlement Negotiations ............................................................................ 13 III. SUMMARY OF THE SETTLEMENT, PLAN OF ALLOCATION, AND NOTICE PROGRAM ....................................................................................................................... 14 A. Summary of the Settlement Terms ................................................................................... 14 B. The Court Has Preliminarily