South Carolina State University Intercollegiate Athletics Program

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2016-17 Hampton University Men's Basketball

Men’s Basketball Quick Facts Location ........................................................................................... Hampton, Va. Enrollment ......................................................................................................4,768 2016-17 Hampton University Conference ......................................................................Mid-Eastern Athletic ..................................................................................NCAA Division I Arena ................................................................Hampton Convocation Center Men’s Basketball AffiliationNickname .................................................................................................... Pirates President .........................................................................Dr. William R. Harvey Athletic Director ..............................................................Eugene Marshall, Jr. Game #29 - March 3, 2017 Hampton vs. Coppin State Head Coach ............................................................................ Edward Joyner, Jr. Sports Information Director • Maurice Williams • Men’s Basketball Contact Record at Hampton ...............................................................................133-122 [email protected] • Office (757) 727-5757 Hampton (13-15, 10-5 MEAC) vs. 2016-17 Men’s Basketball Coppin State (8-22, 7-8 MEAC) Schedule and Results Physical Education Complex • Baltimore, Md. Date Opponent Time/Result Record Thursday, March 2, 2017 • 7:30 p.m. (EST) NOVEMBER -

To Download Homecoming Brochure

RiNesha Smith Miss Homecoming H Celebrating MECOMING the Legacy of Garnet and Blue: Doing it B.I.G. Believe. Invest. Grow. HOMECOMING 2016 Celebrating the Legacy of Garnet and Blue: Doing it B.I.G. – Believe. Invest. Grow. Sunday, October 16, 2016 9pm-12am 3pm All Black Soiree Alumni Tent Party 6pm I.P. Stanback Museum and Planetarium Featuring Classes in Reunion Gospel Explosion DJ Expensive Life Kennel Club (Oliver C. Dawson Stadium) MLK Auditorium Franklin Pressley (803) 516-4826 Cost: $5.00 Franklin Pressley (803) 516-4826 Kemberly Greene (803) 813-1374 Thursday, October 20, 2016 www.alumnireunionparty.com 9pm Homecoming Kickoff Meltdown 7pm 4:30pm Homecoming Concert Student Center--The Plaza Stellar Alumni Calendar Unveiling DJ Richie--*Give Away Prizes* SHM Memorial Center Fine Arts Center Franklin Pressley (803) 516-4826 Artist: Boosie & 21 Savage Dr. Barbara A. Vaughan Recital Hall DJ B Lord Iva Gardner (803) 516-4616 Monday, October 17, 2016 Franklin Pressley (803) 516-4826 $5.00 SC State students 7pm $20.00 General Admission 6pm Ice Skating | Casino Night Delta Sigma Theta Sorority Fall ‘86 SHM Memorial Center Friday, October 21, 2016 30th Line Reunion DJ Tone Student Center Franklin Pressley (803) 516-4826 8:30am Bulldog Lounge SC State University Former Athletes Iva Gardner (803) 516-4616 Tuesday, October 18, 2016 Golf Tournament Orangeburg Country Club 7pm 2pm Kenita Pitts (803) 516-4576 STATE Club Oyster Roast Homecoming “Meltdown” www.scsuathletics.com and Fish Fry Student Center--The Plaza I.P. Stanback Museum DJ Sly Planet -

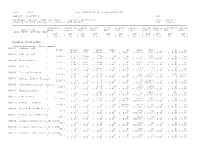

Fall 2016 Building Data Summary Research Universities Institution Name Bldg ID Building Name Site ID Cnsyr Cond Bldg

Fall 2016 Building Data Summary Research Universities Institution Name Bldg ID Building Name Site ID CnsYr Cond Bldg. Cost Repl Cost Linear Feet Gross Area Net Area E&G Repl Cost* E&G Gross Area E&G Linear Feet* % E&G* E&G Maint Cost* Ownership Status Clemson University 1 Tillman Hall 50104 1894 70 $4,659,000 $26,522,287 955 95,705 48,052 $26,522,287 95,705 955 100% $795,669 Owned Fee Simple Clemson University 3 Godfrey Hall 50104 1898 54 $2,632,000 $10,076,799 321 43,620 26,521 $10,076,799 43,620 321 100% $302,304 Owned Fee Simple Clemson University 4 Holtzendorf Y 50104 1915 48 $233,000 $9,014,025 677 42,408 25,561 $9,014,025 42,408 677 100% $270,421 Owned Fee Simple Clemson University 5 Mell Hall 50104 1939 50 $263,000 $917,686 296 10,452 4,773 $109,926 1,252 35 12% $3,298 Owned Fee Simple Clemson University 6 Dillard Building 50104 1953 64 $203,000 $2,393,887 432 25,148 16,716 $2,393,887 25,148 432 100% $71,817 Owned Fee Simple Clemson University 7 Central Energy Facility 50104 1950 54 $858,000 $50,044,641 420 16,744 16,267 $50,044,641 16,744 420 100% $1,501,339 Owned Fee Simple Clemson University 8 Telecommunications Service 50104 1950 80 $38,000 $2,585,234 178 4,300 3,120 $1,241,514 2,065 85 48% $37,245 Owned Fee Simple Clemson University 9 Physical Plant 50104 1928 50 $12,000 $2,611,800 412 21,525 15,400 $2,611,800 21,525 412 100% $78,354 Owned Fee Simple Clemson University 10 Fike Center 50104 1930 89 $1,215,375 $46,222,300 1,397 152,880 123,411 $46,222,300 152,880 1,397 100% $1,386,669 Owned Fee Simple Clemson University 12 Football -

2016-17 Savannah State Women's Basketball

2016-17 Savannah State Women's Basketball MEDIA RELATIONS Assistant Media Relations Director / WBB Contact Will Toman | [email protected] 912-358-3448 3219 College Street, Tiger Arena Savannah, Ga. 31404 Game 28 Savannah State (10-17, 7-7 MEAC) at North Carolina Central (6-20, 5-9 MEAC) Feb. 27, 2017 - 5:30 p.m. McDougald-McLendon Arena Durham, N.C. TALE OF THE TAPE: GP MEAC FG-FGA Pct. 3F-3PA Pct. Ft-Fta. Pct. RBS Avg. A TO BLK S PPG Savannah State: 27 7-7 512-1514 .338 119-459 .259 279-443 .630 1013 37.5 263 468 147 212 52.7 North Carolina Central: 26 5-9 430-1459 .295 100-360 .278 326-461 .707 986 37.9 230 468 60 214 49.5 SCHEDULE / RESULTS COVERAGE: Overall Record: 10-17 MEAC: 7-7 RADIO: N/A Home: 8-6 Away: 2-11 Neutral: 0-0 TV: N/A LIVE WEB STREAM: NCCUEaglePride.com Date Opponent Time / Results LIVE STATS: NCCUEaglePride.com Nov. 3 Middle Georgia St. (EXH) W, 67-50 TWITTER: @savstatetigers | #HailSSU Nov. 7 Armstong State (EXH) L, 68-72 (OT) Nov. 11 at Seton Hall L, 60-74 GAME NOTES: Nov. 13 Columbia College W, 68-52 Nov. 15 Alabama State W, 54-39 > Senior center Tiyonda Davis holds the school record Nov. 22 at Iowa State L, 51-74 in blocks with 289 career blocks and in rebounds with Nov. 26 at Kennesaw State L, 60-72 941 career boards. The Athens, Ga., native also ranks Nov. 29 Jacksonville L, 40-55 Dec. -

Game 23 | Monday, Feb. 12 | 4 Pm | Norfolk

GAME 23 | MONDAY, FEB. 12 | 4 P.M. | NORFOLK, VA. (JOSEPH G. ECHOLS MEMORIAL HALL) Norfolk State Spartans (13-9, 6-4 MEAC) Delaware State Lady Hornets (4-19, 3-7 MEAC) Head Coach: Larry Vickers (Norfolk State ‘07) Head Coach: Barbara Burgess (Delaware State ‘90) Record at NSU: 31-32 (3rd Season) VS Record at DU: 16-67 (3rd season) Career Record: 31-32 (3rd Season) Career Record: 16-67 (3rd season) Record vs. DSU: 2-1 Record vs. NSU: 1-2 GAME INFORMATION NSU Schedule/Results (13-9, 6-4 MEAC) Date/Time: Monday, February 12 | 4 p.m. Site: Norfolk, Va. | Joseph G. Echols Memorial Hall (4,500) November (2-4) Video: http://nsuspartans.com/watch/?Live=690&type=Live Sun. 12 VCU .................................. W, 66-52 Radio: Hot 91.1 FM, http://hot91.nsu.edu:8000/128 (Ross Gordon, Play-by-Play) Fri. 17 Navy .................................. L, 70-51 Live Stats: http://www.sidearmstats.com/nsu/wbball/ Tue. 21 Loyola (Md.) ..................... L, 61-58 Series Information: NSU trails 20-23 Fri. 24 Bowling Green! ................. L, 59-50 Sat. 25 St. Francis Brooklyn! ........ W, 52-51 The Opening Tip: Norfolk State snapped a 20-game road losing streak to Hampton with a 63-48 Wed. 29 High Point ......................... L, 59-56 result at the Convocation Center on Saturday. The Spartans last won in Hampton on Jan. 31, 1995. Overall, it is just the seventh win against the Lady Pirates since the turn of the century. December (5-1) Sat. 2 East Carolina .................... L, 51-46 • Alexys Long scored a game-high 19 points against HU and was dialed in, going 8-of-10 from the field Tue. -

2008-09 Opponents

NSUNSU OPPONENTSOPPONENTS 2008-092008-09 Women’sWomen’s BasketballBasketball 2008-09 OPPONENTS University of Miami Stetson University William & Mary Old Dominion University Nov. 14 Nov. 16 Nov. 20 Nov. 30 at BankUnited Center, Noon at Edmunds Center, 2 p.m. at Kaplan Arena, 7 p.m. at Ted Constant Convocation Center, 2 p.m. GENERAL INFORMATION GENERAL INFORMATION GENERAL INFORMATION Location: Coral Gables, Fla. Location: Deland, Fla. Location: Williamsburg, Va. GENERAL INFORMATION Founded: 1925 Founded: 1883 Founded: 1693 Location: Norfolk, Va. Enrollment: 15,449 Enrollment: 2,492 Enrollment: 7,625 Founded: 1930 Mascot: Hurricanes Mascot: Hatters Mascot: Tribe Enrollment: 20,802 Colors: Orange, Green and White Colors: Hunter Green and White Colors: Green, Gold, and Silver Mascot: Monarchs Affiliation: NCAA Division I Affiliation: NCAA Division I Affiliation: NCAA Division I Colors: Slate Blue, Sky Blue and Silver Conference: Atlantic Coast Conference Conference: Atlantic Sun Conference: Colonial Athletic Association Affiliation: NCAA Division I Arena: BankUnited Center Arena: Edmunds Center Arena: Kaplan Arena Conference: Colonial Athletic Association Capacity: 7,000 Capacity: 5,000 Capacity: 8,600 Arena: Ted Constant Convocation Center President: Dr. Donna E. Shalala President: Dr. H. Douglas Lee President: W. Taylor Reveley III Capacity: 8,600 Athletics Director: Kirby Hocutt Athletics Director: Jeff Altier Athletics Director: Terry Driscoll Interim President: John Broderick Athletics Department: (305) 284-2689 Athletics Department: (386) -

Doing It BIG Believe. Invest. Grow

RiNesha Smith Miss Homecoming H Celebrating MECOMING the Legacy of Garnet and Blue: Doing it B.I.G. Believe. Invest. Grow. HOMECOMING 2016 Celebrating the Legacy of Garnet and Blue: Doing it B.I.G. – Believe. Invest. Grow. Sunday, October 16, 2016 9pm-12am 3pm All Black Soiree Alumni Tent Party 6pm I.P. Stanback Museum and Planetarium Featuring Classes in Reunion Gospel Explosion DJ Expensive Life Kennel Club (Oliver C. Dawson Stadium) MLK Auditorium Franklin Pressley (803) 516-4826 Cost: $5.00 Franklin Pressley (803) 516-4826 Kemberly Greene (803) 813-1374 Thursday, October 20, 2016 www.alumnireunionparty.com 9pm Homecoming Kickoff Meltdown 7pm 4:30pm Homecoming Concert Student Center--The Plaza Stellar Alumni Calendar Unveiling DJ Richie--*Give Away Prizes* SHM Memorial Center Fine Arts Center Franklin Pressley (803) 516-4826 Artist: Boosie & 21 Savage Dr. Barbara A. Vaughan Recital Hall DJ B Lord Iva Gardner (803) 516-4616 Monday, October 17, 2016 Franklin Pressley (803) 516-4826 $5.00 SC State students 7pm $20.00 General Admission 6pm Ice Skating | Casino Night Delta Sigma Theta Sorority Fall ‘86 SHM Memorial Center Friday, October 21, 2016 30th Line Reunion DJ Tone Student Center Franklin Pressley (803) 516-4826 8:30am Bulldog Lounge SC State University Former Athletes Iva Gardner (803) 516-4616 Tuesday, October 18, 2016 Golf Tournament Orangeburg Country Club 7pm 2pm Kenita Pitts (803) 516-4576 STATE Club Oyster Roast Homecoming “Meltdown” www.scsuathletics.com and Fish Fry Student Center--The Plaza I.P. Stanback Museum DJ Sly Planet -

Company Overview

Organizational Review PREPARED FOR: Michael Smith, Interim AD January 2, 2014 www.CollegiateConsulting.com 3101 Towercreek Parkway, Suite 175, Atlanta, GA 30339 Collegiate Consulting Report TABLE OF CONTENTS EXECUTIVE SUMMARY ............................................................. 3 RECOMMENDATIONS SUMMARY .............................................. 7 INSTITUTIONAL OVERVIEW ..................................................11 FLORIDA A&M UNIVERSITY ATHLETICS .................................12 MID-EASTERN ATHLETIC CONFERENCE ..................................13 Overview .............................................................................................. 13 Institutional Statistics ............................................................................. 14 Sport Sponsorship .................................................................................. 15 Competitiveness .................................................................................... 18 Travel Analysis ...................................................................................... 19 SOUTHWESTERN ATHLETIC CONFERENCE ..............................21 Overview .............................................................................................. 21 Institutional Statistics ............................................................................. 21 Sports Sponsorship ................................................................................ 23 Competitiveness ................................................................................... -

Combined Stats

SOUTH CAROLINA STATE UNIVERSITY MEN’S BASKETBALL 2007 GAME NOTES South Carolina State University Bulldogs vs University of North Carolina Chapel Hill Tuesday, November 20, 2007 7:30 PM Dean Smith Center Chapel Hill North Carolina SOUTH CAROLINA STATE UNIVERSITY BULLDOGS MEN’S BASKETBALL William Hamilton SID :: [email protected] :: 803-536-8759- (office) :: 803-378-6165 (cell) SC STATE 2007 QUICK FACTS 2007-08 SC STATE SCHEDULE/RESULTS Day Date Opponent Time/Results General Fri 11/9/07 @ South Carolina L 62-97 School South Carolina State University Sun 11/11/07 @ Old Dominion L 54-64 Founded 1896 WED 11/14/07 JACKSONVILLE L, 64-76 Tues 11/20/07 @ North Carolina 7:00 PM Enrollment 4,700 Fri 1/23/07 vs Iona% 1PM Colors Garnet & Blue Sat 1/24/17 vs Hartford/Jackson St% 12/2:30PM President Dr. Andrew Hugine, Jr. Sat. 12/1/07 Winston-Salem State Univ. 4:00 PM Alma Mater South Carolina State University, 1971 TUES 12/4/07 VMI 7:30PM Mascot/Nick Name Bulldog/Bulldogs Sat 12/8/07 Savannah State 6 pm Arena Smith-Hammond-Middleton Sat 12/15/07 @ North Carolina State 2:30pm Capacity 3,200 Mon 12/17/07 @ UNC Ashville 7:00 PM Affiliation NCAA Division I THUR 12/20/07 ALLEN UNIVERISTY 7:00 PM Conference Mid-Eastern Athletic Sat 12-29/07 James Madison 5:00 PM Athletics Director Charlene Johnson Sun 12/30/07 Mercer/Coll. of Charleston 5/7:30 PM SAT. 1/12/08 *DELAWARE STATE 4:00 PM Alma Mater South Carolina State, 1980 MON. -

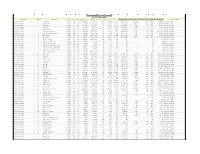

Fall 2010 S.C. COMMISSION on HIGHER EDUCATION PROGRAM : CHES607GDP PAGE: 1 ASSIGNABLE AREA by ROOM USE CODES

Fall 2010 S.C. COMMISSION ON HIGHER EDUCATION PROGRAM : CHES607GDP PAGE: 1 ASSIGNABLE AREA BY ROOM USE CODES (By Site Identifiers) DATE: 05/10/11 FUNCTION USE CODE FOR HOSPITAL EXCLUDED FROM REPORT TIME: 14:42:11 ________________________________________________________________________________________________________________________________ |ASSIGNABLE |CLASS RM|LABORAT |OFFICE |STUDY |SPECIAL |GENERAL |SUPPORT|HEALTH|RESIDENTIL|UNCLAS| INSTITUTION |AREA |FACIL. |FACIL. |FACIL. |FACIL. |FACIL. |FACIL. |FACIL. |FACIL.|FACIL. |FACIL.| BLDG-IDENT BUILDING NAME | ASF | ASF | ASF | ASF | ASF | ASF | ASF | ASF | ASF | ASF | ASF | | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | ________________________________________________________________________________________________________________________________ RESEARCH UNIVERSITIES Clemson University (Main Campus) 000001 Tillman Hall | 53800 | 10445| 4023| 26973| 1971| 0| 9856| 532| 0| 0| 0| ( 19.4) ( 7.4) ( 50.1) ( 3.6) ( 0.0) ( 18.3) ( 0.9) ( 0.0) ( 0.0) ( 0.0) 000003 Godfrey Hall | 28858 | 3161| 24093| 579| 0| 0| 0| 1025| 0| 0| 0| ( 10.9) ( 83.4) ( 2.0) ( 0.0) ( 0.0) ( 0.0) ( 3.5) ( 0.0) ( 0.0) ( 0.0) 000004 Holtzendorf Y | 25723 | 4582| 4781| 8699| 0| 0| 5060| 2601| 0| 0| 0| ( 17.8) ( 18.5) ( 33.8) ( 0.0) ( 0.0) ( 19.6) ( 10.1) ( 0.0) ( 0.0) ( 0.0) 000005 Mell Hall | 5130 | 0| 0| 4747| 0| 0| 272| 111| 0| 0| 0| ( 0.0) ( 0.0) ( 92.5) ( 0.0) ( 0.0) ( 5.3) ( 2.1) ( 0.0) ( 0.0) ( 0.0) 000006 Dillard Building | 16419 | 2622| 0| 3170| 0| 0| 705| 6351| 0| 240| 3331| ( 15.9) ( 0.0) ( -

Fall 2014 Building Data Summary Research Universities Institution Name Bldg ID Building Name Site ID Cnsyr Cond Bldg

Fall 2014 Building Data Summary Research Universities Institution Name Bldg ID Building Name Site ID CnsYr Cond Bldg. Cost Repl Cost Linear Feet Gross Area Net Area E&G Repl Cost* E&G Gross Area E&G Linear Feet* % E&G* E&G Maint Cost* Ownership Status Clemson University 1 Tillman Hall 50104 1894 70 $4,659,000 $26,522,287 955 95,705 48,052 $26,522,287 95,705 955 100% $795,669 Owned Fee Simple Clemson University 3 Godfrey Hall 50104 1898 54 $2,632,000 $10,076,799 321 43,620 26,521 $10,076,799 43,620 321 100% $302,304 Owned Fee Simple Clemson University 4 Holtzendorf Y 50104 1915 48 $233,000 $9,014,025 677 42,408 25,561 $9,014,025 42,408 677 100% $270,421 Owned Fee Simple Clemson University 5 Mell Hall 50104 1939 50 $263,000 $917,686 296 10,452 4,773 $109,926 1,252 35 12% $3,298 Owned Fee Simple Clemson University 6 Dillard Building 50104 1953 64 $203,000 $2,393,887 432 25,148 16,800 $2,393,887 25,148 432 100% $71,817 Owned Fee Simple Clemson University 7 Central Energy Facility 50104 1950 54 $858,000 $50,044,641 420 16,744 16,267 $50,044,641 16,744 420 100% $1,501,339 Owned Fee Simple Clemson University 8 Telecommunications Service 50104 1950 80 $38,000 $2,585,234 178 4,300 3,120 $1,241,514 2,065 85 48% $37,245 Owned Fee Simple Clemson University 9 Physical Plant 50104 1928 50 $12,000 $2,611,800 412 21,525 15,400 $2,611,800 21,525 412 100% $78,354 Owned Fee Simple Clemson University 10 Fike Center 50104 1930 89 $1,215,375 $46,222,300 1,397 152,880 123,411 $46,222,300 152,880 1,397 100% $1,386,669 Owned Fee Simple Clemson University 12 Football -

2016-17 Hampton University Men's Basketball

Men’s Basketball Quick Facts Location ........................................................................................... Hampton, Va. Enrollment ......................................................................................................4,768 2016-17 Hampton University Conference ......................................................................Mid-Eastern Athletic ..................................................................................NCAA Division I Arena ................................................................Hampton Convocation Center Men’s Basketball AffiliationNickname .................................................................................................... Pirates President .........................................................................Dr. William R. Harvey Athletic Director ..............................................................Eugene Marshall, Jr. Game #30 - March 9, 2017 Hampton vs. Maryland E. Shore Head Coach ............................................................................ Edward Joyner, Jr. Sports Information Director • Maurice Williams • Men’s Basketball Contact Record at Hampton ...............................................................................134-122 [email protected] • Office (757) 727-5757 #4 Hampton (14-15) vs. 2016-17 Men’s Basketball #5 Maryland Eastern Shore (13-19) Schedule and Results Norfolk Scope Arena • Norfolk, Va. Date Opponent Time/Result Record Thursday, March 9, 2017 • 8:00 p.m. (EST) NOVEMBER Fri.