Train Schedule Sri Lanka Colombo to Badulla

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sri Lanka Railways

SRI LANKA RAILWAYS PROCUREMENT NOTICE 3,850 CUBES OF TRACK BALLAST TO LOWER DISTRICT PROCUREMENT NO - SRS/F.7739 01. The Chairman, Department Procurement Committee (Major), Sri Lanka Railways, will receive sealed bids from the suppliers for the supply of Track Ballast to the following places on National Competitive Bidding Basis. These bids will be evaluated and awarded separately for each item mentioned below: Item Delivery period Place Cubes No. (Months) 1. Kalutara South 500 04 2. Train Halt No. 01 1,000 06 3. 20M. 35Ch. - 20M. 40Ch. 500 04 (Between Pinwatte & Wadduwa Railway Stations) 4. Pinwatte (18M. 60Ch) 200 02 5. Panadura (near Railway Bridge) 200 02 6. Moratuwa Railway Yard 200 02 7. Angulana Railway Station, Colombo 200 02 End 8. Ratmalana Railway Station 250 03 9. Nawinna Railway Station (Kelani 300 03 Valley Line) 10. Malapalla (Kelani Valley Line) 200 02 11. Watareka (Kelani Valley Line) 100 01 12. Liyanwala (Kelani Valley Line) 200 02 02. Bids shall be submitted only on the forms obtainable from the Office of the Superintendent of Railway Stores, up to 3.00 p.m. on 23.09.2020 on payment of a non-refundable document fee of Rs.7,000.00 (Rupees Seven Thousand) only. 03. Bids will be closed at 2.00 p.m. on 24.09.2020. 04. The bidders shall furnish a bid security amounting Rs.300,000.00 (Sri Lankan Rupees Three Hundred Thousand) only as part of their bid. 05. Bids will be opened immediately after the closing time at the Office of the Superintendent of Railway Stores. -

CHAP 9 Sri Lanka

79o 00' 79o 30' 80o 00' 80o 30' 81o 00' 81o 30' 82o 00' Kankesanturai Point Pedro A I Karaitivu I. Jana D Peninsula N Kayts Jana SRI LANKA I Palk Strait National capital Ja na Elephant Pass Punkudutivu I. Lag Provincial capital oon Devipattinam Delft I. Town, village Palk Bay Kilinochchi Provincial boundary - Puthukkudiyiruppu Nanthi Kadal Main road Rameswaram Iranaitivu Is. Mullaittivu Secondary road Pamban I. Ferry Vellankulam Dhanushkodi Talaimannar Manjulam Nayaru Lagoon Railroad A da m' Airport s Bridge NORTHERN Nedunkeni 9o 00' Kokkilai Lagoon Mannar I. Mannar Puliyankulam Pulmoddai Madhu Road Bay of Bengal Gulf of Mannar Silavatturai Vavuniya Nilaveli Pankulam Kebitigollewa Trincomalee Horuwupotana r Bay Medawachchiya diya A d o o o 8 30' ru 8 30' v K i A Karaitivu I. ru Hamillewa n a Mutur Y Pomparippu Anuradhapura Kantalai n o NORTH CENTRAL Kalpitiya o g Maragahewa a Kathiraveli L Kal m a Oy a a l a t t Puttalam Kekirawa Habarane u 8o 00' P Galgamuwa 8o 00' NORTH Polonnaruwa Dambula Valachchenai Anamaduwa a y O Mundal Maho a Chenkaladi Lake r u WESTERN d Batticaloa Naula a M uru ed D Ganewatta a EASTERN g n Madura Oya a G Reservoir Chilaw i l Maha Oya o Kurunegala e o 7 30' w 7 30' Matale a Paddiruppu h Kuliyapitiya a CENTRAL M Kehelula Kalmunai Pannala Kandy Mahiyangana Uhana Randenigale ya Amparai a O a Mah Reservoir y Negombo Kegalla O Gal Tirrukkovil Negombo Victoria Falls Reservoir Bibile Senanayake Lagoon Gampaha Samudra Ja-Ela o a Nuwara Badulla o 7 00' ng 7 00' Kelan a Avissawella Eliya Colombo i G Sri Jayewardenepura -

SUSTAINABLE URBAN TRANSPORT INDEX Sustainable Urban Transport Index Colombo, Sri Lanka

SUSTAINABLE URBAN TRANSPORT INDEX Sustainable Urban Transport Index Colombo, Sri Lanka November 2017 Dimantha De Silva, Ph.D(Calgary), P.Eng.(Alberta) Senior Lecturer, University of Moratuwa 1 SUSTAINABLE URBAN TRANSPORT INDEX Table of Content Introduction ........................................................................................................................................ 4 Background and Purpose .............................................................................................................. 4 Study Area .................................................................................................................................... 5 Existing Transport Master Plans .................................................................................................. 6 Indicator 1: Extent to which Transport Plans Cover Public Transport, Intermodal Facilities and Infrastructure for Active Modes ............................................................................................... 7 Summary ...................................................................................................................................... 8 Methodology ................................................................................................................................ 8 Indicator 2: Modal Share of Active and Public Transport in Commuting................................. 13 Summary ................................................................................................................................... -

Urban Transport System Development Project for Colombo Metropolitan Region and Suburbs

DEMOCRATIC SOCIALIST REPUBLIC OF SRI LANKA MINISTRY OF TRANSPORT URBAN TRANSPORT SYSTEM DEVELOPMENT PROJECT FOR COLOMBO METROPOLITAN REGION AND SUBURBS URBAN TRANSPORT MASTER PLAN FINAL REPORT TECHNICAL REPORTS AUGUST 2014 JAPAN INTERNATIONAL COOPERATION AGENCY EI ORIENTAL CONSULTANTS CO., LTD. JR 14-142 DEMOCRATIC SOCIALIST REPUBLIC OF SRI LANKA MINISTRY OF TRANSPORT URBAN TRANSPORT SYSTEM DEVELOPMENT PROJECT FOR COLOMBO METROPOLITAN REGION AND SUBURBS URBAN TRANSPORT MASTER PLAN FINAL REPORT TECHNICAL REPORTS AUGUST 2014 JAPAN INTERNATIONAL COOPERATION AGENCY ORIENTAL CONSULTANTS CO., LTD. DEMOCRATIC SOCIALIST REPUBLIC OF SRI LANKA MINISTRY OF TRANSPORT URBAN TRANSPORT SYSTEM DEVELOPMENT PROJECT FOR COLOMBO METROPOLITAN REGION AND SUBURBS Technical Report No. 1 Analysis of Current Public Transport AUGUST 2014 JAPAN INTERNATIONAL COOPERATION AGENCY (JICA) ORIENTAL CONSULTANTS CO., LTD. URBAN TRANSPORT SYSTEM DEVELOPMENT PROJECT FOR COLOMBO METROPOLITAN REGION AND SUBURBS Technical Report No. 1 Analysis on Current Public Transport TABLE OF CONTENTS CHAPTER 1 Railways ............................................................................................................................ 1 1.1 History of Railways in Sri Lanka .................................................................................................. 1 1.2 Railway Lines in Western Province .............................................................................................. 5 1.3 Train Operation ............................................................................................................................ -

Evaluation of Agriculture and Natural Resources Sector in Sri Lanka

Evaluation Working Paper Sri Lanka Country Assistance Program Evaluation: Agriculture and Natural Resources Sector Assistance Evaluation August 2007 Supplementary Appendix A Operations Evaluation Department CURRENCY EQUIVALENTS (as of 01 August 2007) Currency Unit — Sri Lanka rupee (SLR) SLR1.00 = $0.0089 $1.00 = SLR111.78 ABBREVIATIONS ADB — Asian Development Bank GDP — gross domestic product ha — hectare kg — kilogram TA — technical assistance UNDP — United Nations Development Programme NOTE In this report, “$” refers to US dollars. Director General Bruce Murray, Operations Evaluation Department (OED) Director R. Keith Leonard, Operations Evaluation Division 1, OED Evaluation Team Leader Njoman Bestari, Principal Evaluation Specialist Operations Evaluation Division 1, OED Operations Evaluation Department CONTENTS Page Maps ii A. Scope and Purpose 1 B. Sector Context 1 C. The Country Sector Strategy and Program of ADB 11 1. ADB’s Sector Strategies in the Country 11 2. ADB’s Sector Assistance Program 15 D. Assessment of ADB’s Sector Strategy and Assistance Program 19 E. ADB’s Performance in the Sector 27 F. Identified Lessons 28 1. Major Lessons 28 2. Other Lessons 29 G. Future Challenges and Opportunities 30 Appendix Positioning of ADB’s Agriculture and Natural Resources Sector Strategies in Sri Lanka 33 Njoman Bestari (team leader, principal evaluation specialist), Alvin C. Morales (evaluation officer), and Brenda Katon (consultant, evaluation research associate) prepared this evaluation working paper. Caren Joy Mongcopa (senior operations evaluation assistant) provided administrative and research assistance to the evaluation team. The guidelines formally adopted by the Operations Evaluation Department (OED) on avoiding conflict of interest in its independent evaluations were observed in the preparation of this report. -

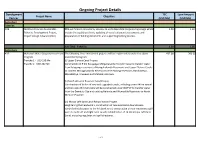

Ongoing Project Details

Ongoing Project Details Development TEC Loan Amount Project Name Objective Partner (USD Mn) (USD Mn) Agriculture Fisheries ADB Northern Province Sustainable PDA will finance consultancy services to undertake detail engineering design which 1.59 1.30 Fisheries Development Project, include the updating of cost, updating of social safeguard assessments and Project Design Advance (PDA) preparation of bidding documents and supporting bidding process. Sub Total - Fisheries 1.59 1.30 Agriculture ADB Mahaweli Water Security Investment The following three investment projects will be implemented under the above 432.00 360.00 Program investment program. Tranche 1 - USD 190 Mn (i) Upper Elahera Canal Project Tranche 2- USD 242 Mn Construction of 9 km Kaluganga-Morgahakanda Transfer Canal to transfer water from Kaluganga reservoir to Moragahakanda Reservoirs and Upper Elehera Canals to connect Moragahakanda Reservoir to the existing reservoirs; Huruluwewa, Manakattiya, Eruwewa and Mahakanadarawa. (ii) North Western Province Canal Project Construction of 96 km of new and upgraded canals, including a new 940 m tunnel and two new 25 m tall dams will be constructed under NWPCP to transfer water from the Dambulu Oya and existing Nalanda and Wemedilla Reservoirs to North Western Province. (iii) Minipe Left Bank Canal Rehabilitation Project Heightening the headwork’s, construction of new automatic downstream- controlled intake gates to the left bank canal; construction of new emergency spill weirs to both left and right bank canals; rehabilitation of 74 km Minipe Left Bank Canal, including regulator and spill structures. 1 of 24 Ongoing Project Details Development TEC Loan Amount Project Name Objective Partner (USD Mn) (USD Mn) IDA Agriculture Sector Modernization Objective is to support increasing Agricultural productivity, improving market 125.00 125.00 Project access and enhancing value addition of small holder farmers and agribusinesses in the project areas. -

Environmental Screening Peport

Environmental Screening Report Construction of Pocket Parks at Beach Road, Russell Square & Rasaavinthoddam at Jaffna Project Management Unit Strategic Cities Development Project Ministry of Megapolis & Western Development July 2019 1 Table of Contents 1. Project Identification 03 2. Project Location 03 3. Project Justification 03 4. Project Description 09 5. Description of the Existing Environment 16 6. Public Consultation 18 7. Environmental Effects and Mitigation Measures 19 7a. Screening for Potential Environmental Impacts 19 7b. Environmental Management Plan 23 8. Cost of Mitigation 36 9. Conclusion and Screening Decision 37 10. EMP implementation responsibilities and costs 38 11. Screening Decision Recommendation 38 12. Details of Persons Responsible for the Environmental Screening 39 Annexes Annex 1: Project Location Map Annex 2: Physiographic Locations of Jaffna Peninsula Annex 3: Geology and Soil Map of the Project Area Annex 4: Map of wetlands in Jaffna Peninsula Annex 5: Geology and conditions of ground water in Jaffna Peninsula Annex 6: Design Layouts Annex 7: Summary of Procedures to obtain Mining License for Borrow Pit & Quarry Operation and Management Guidelines Annex 8: Waste Management General Guidelines Annex 9: Environmental Pollution Control Standards Annex 10: Factory Ordinance and ILO Guidelines Annex 11: Chance Find Procedures Annex 12: Terms of Reference for Recruitment of Safeguard Officer 2 Strategic Cities Development Project Environmental Screening Report 1. Project Identification Project Title Construction -

Tides of Violence: Mapping the Sri Lankan Conflict from 1983 to 2009 About the Public Interest Advocacy Centre

Tides of violence: mapping the Sri Lankan conflict from 1983 to 2009 About the Public Interest Advocacy Centre The Public Interest Advocacy Centre (PIAC) is an independent, non-profit legal centre based in Sydney. Established in 1982, PIAC tackles barriers to justice and fairness experienced by people who are vulnerable or facing disadvantage. We ensure basic rights are enjoyed across the community through legal assistance and strategic litigation, public policy development, communication and training. 2nd edition May 2019 Contact: Public Interest Advocacy Centre Level 5, 175 Liverpool St Sydney NSW 2000 Website: www.piac.asn.au Public Interest Advocacy Centre @PIACnews The Public Interest Advocacy Centre office is located on the land of the Gadigal of the Eora Nation. TIDES OF VIOLENCE: MAPPING THE SRI LANKAN CONFLICT FROM 1983 TO 2009 03 EXECUTIVE SUMMARY ....................................................................................................................... 09 Background to CMAP .............................................................................................................................................09 Report overview .......................................................................................................................................................09 Key violation patterns in each time period ......................................................................................................09 24 July 1983 – 28 July 1987 .................................................................................................................................10 -

Activities and Experiences

Activities and Experiences KADURUKETHA WELLAWAYA Content Paddy Farming & Harvesting Festivals 1 Birdwatching 3 Tree Trail at Kaduruketha 5 Night Walk at Jetwing Kaduruketha 7 Village Walk 9 Cycling to Elle Wala Waterfall and Bathing in the Natural Pool 11 Archaeology Experience - Buduruwagala, Yudhaganawa, Maligavila & Biso Kotuwa 15 Adventure at Diyaluma & Udadiyaluma with Picnic Service 17 Elephants at Udawalawe National Park & the Elephant Transit Home (ETH) 19 Exploring Ella 21 Tea Fields & Factories up to Lipton Seat 23 Elephants at Handapanagala Tank 25 Leopard Safari at Weheragala (Yala block V) 27 Responsible Tourism 29-31 Paddy Farming & Harvesting Festivals Sri Lanka’s primary form of agriculture is rice production. Rice paddy is cultivated during Maha and Yala seasons. In view of the fact that paddy cultivation was pivotal to the survival of the community, all activities connected to paddy cultivation were treated with the highest honour and respect. Kaduruketha farmers also have their farming and harvesting festival with many customs and rituals and guests at Jetwing Kaduruketha will have the rare opportunity of witnessing and participating in these festivals. Yala season Farming festival – April Harvesting festival – July Maha season Farming festival – November Harvesting festival – February 1 Birdwatching Jetwing Kaduruketha is located in an intermediate zone which has created good climatic conditions for a mix of dry zone and wet zone flora and fauna. The land extent of Jetwing Kaduruketha is 60 acres, 50 of which are devoted to paddy cultivation, however 10 acres comprise of lush vegetation with many utility trees and forest trees; habitats for many birds including some endemics such as Sri Lanka grey hornbill, Sri Lanka hanging-parrot, Sri Lanka emerald-collared parakeet, Sri Lanka small barbet etc. -

International Conference on Land Transportation, Locomotive Heritage and Road Culture

The International Conference on Land Transportation, Locomotive Heritage and Road Culture Abstract Volume Centre for Heritage Studies University of Kelaniya Sri Lanka 2017 The International Conference on Land Transportation, Locomotive Heritage and Road Culture Abstract Volume 14th – 15th December 2017 Centre for Heritage Studies University of Kelaniya Sri Lanka Editorial Advisors Prof. D.M. Semasinghe Prof. Patrick Ratnayake Vice Chancellor, Dean, Faculty of Humanities, University of Kelaniya University of Kelaniya Prof. Lakshman Senevirathne Prof. N.P. Sunil Chandra Deputy Vice Chancellor, Chairman, Research Council, University of Kelaniya University of Kelaniya Prof. A.H.M.H. Abayarathna Dean, Faculty of Social Sciences, University of Kelaniya Editorial Consultants Prof. Malinga Amarasinghe Dr. J.M. Sudharmawathie Department of Archaeology, Head, Department of History, University of Kelaniya University of Kelaniya Prof. Mapa Thilakarathna Dr. Kaushalya Perera Department of Mass Communication, Head, University of Kelaniya Department of English Language Teaching, University of Kelaniya Ms. Nadheera Hewawasan Deputy Director, Centre for Heritage Studies, University of Kelaniya Editor – in – Chief Prof. Anura Manatunga Director, Centre for Heritage Studies, University of Kelaniya Editors Mr. Thilina Wickramaarachchi Dr. Waruni Tennakoon Department of English Language Teaching, Head, Department of English, University of Kelaniya Buddhist and Pali University of Sri Lanka Ms. Arundathie Abeysinghe Sri Lankan Airlines Editorial Coordinator Ms. Piyumi Embuldeniya Research Assistant, Centre for Heritage Studies, University of Kelaniya Board of Editors Ms. Apeksha Embuldeniya Ms. B.A.I.R. Weerasinghe Assistant Lecturer, Assistant Lecturer, Department of Social Statistics, Department of English Language Teaching, University of Kelaniya University of Kelaniya Ms. Kanchana Dehigama Ms. P.D.S.N. Dissanayake Senior Assistant Librarian, Assistant Lecturer, University of Peradeiya Department of English Language Teaching, University of Kelaniya Ms. -

Cargills (Ceylon)

Cargills (Ceylon) CARG – Rs.193.0 Disclaimer: CT CLSA Securities (Pvt) Ltd is an associate of C T Holdings PLC, the parent of CARG Chayanika Ranasinghe Key Highlights Email : [email protected] Phone : +94 77 2379731 3Q18 Results Update . 3Q18 recurring net profit of Rs.636mn (largely unchanged YoY), broadly in line with our expectations. Earnings are adjusted for CARG‟s proportion of the Rs.481mn capital gain received by associate Cargills Bank from disposal of subsidiary Colombo Trust Finance (CALF) . CARG group net profit forecasts broadly maintained at Rs.2,535mn for FY18E (+20% YoY) and Rs.3,055mn for FY19E (+21% YoY), particularly driven by the Retail and Restaurants sectors. Retail sector to marginally overtake FMCG earnings contribution in FY19E given the significant expansion plans in the pipeline - targeting to double its retail network in the medium term . On 01 Feb 2018, CARG announced a capitalisation of reserves amounting to Rs.6.4bn (out of reserves of Rs.9.4bn as at 30 Sep 2017), via the issuance of 32mn shares in the proportion of 01:07 at a consideration of Rs.200.0 per share; XC : 20 Mar 2018 . The CARG share has outperformed the market rising +13% both during the past 3 months and 12 months (vs. the ASI‟s gains of +1% and +2% respectively during the same period) ASI . CARG is trading at PER multiples of 19.5X FY18E and 16.2X FY19E whilst offering ROEs of 17- CARG 130 1,200 19% (up from low single digits in FY15) Share Volume ('000) - RHS 10 April 2018 1,000 Our estimated Sum-of-the-parts (SOTP) valuation suggests that CARG is currently trading at a 120 . -

The Term Level Crossing (Also Called a Railroad Crossing, Road Through Railroad, Train Crossing Or Grade Crossing) Is a Crossing

CHAPTER 3 DATA COLLECTION 3.1 Railway Network in Sri Lanka Data obtained from SLR related to the rail network is summarized and illustrated in table given below. Table 3.1 Summary of existing Rail Network Rail Line Length No s . Protected Level Km Crossings Main line 291(Colombo-Badulla) 67 Puttalam line 120(Ragama-Puttalam) 152 KV line 59(Colombo- 69 Avissawella) Matale line 34(Kandy – Matale) 11 Coast line 160 (Colombo- Matara) 189 Trincoalee line 70(Galoya – 23 Trincomalee) Batticaloa line 212(Mahawa- Baticaloa) 34 Nothern line 184(Polgahawela- 78 Vavuniya) Total 623 Source: Sri Lanka Railways. Note: Number of level crossings in above table includes only the controlled crossings. 3.1.1 The systems adopted for data collection The data collection in this research involved field visits, surveys, interviews, collecting data from SLR sources, literature reviews etc. Under field visits around 125 rails crossings were observed in Colombo Area, Southern Province, Upcountry Area, Trincomalee District and photographs were taken at locations contributed for delay as well as in good sections (very few). Special attention was given on main line as it involves multi tracks in most of the locations. Evaluation of parameters influencing delay at level crossings. Page 24 of 62 In addition to the photographs, all the important points / issues related to delay and safety such as surface defects, visibility problem, alignment related issues were noted down in each locations. Random interviews were made with road users, residents of surrounding areas, gate keepers, rail passengers and officials of SLR whenever required. In collecting data especially on approaches (to address alignment related issues) to the crossings in order to ensure the starting delay of vehicles just after the rail gate is open (after the gate closer for rail passing) was also noted down.