Comprehensive Annual Financial Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

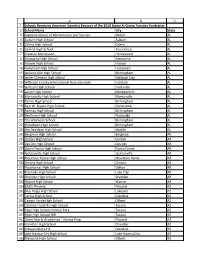

Schools Receiving American Scientist Because of the 2019 Sigma Xi

A B C 1 Schools Receiving American Scientist Because of the 2019 Sigma Xi Giving Tuesday Fundraiser 2 School Name City State 3 Alabama School of Mathematics and Science Mobile AL 4 Auburn High School Auburn AL 5 Calera High School Calera AL 6 Central High School Tuscaloosa AL 7 Creative Montessori Homewood AL 8 Enterprise High School Enterprise AL 9 Hoover High School Hoover AL 10 Hueytown High School Hueytown AL 11 Jackson-Olin High School Birmingham AL 12 James Clemens High School Madison City AL 13 Jefferson County International Bacculaureate Irondale AL 14 Jemison High School Huntsville AL 15 Lanier High School Montgomery AL 16 Montevallo High School Montevallo AL 17 Parker High School Birmingham AL 18 Paul W. Bryant High School Cottondale AL 19 Ramsay High School Birmingham AL 20 Reeltown High School Notasulga AL 21 The Altamont School Birmingham AL 22 Woodlawn High School Birmingham AL 23 Wp Davidson High School Mobile AL 24 Bergman High School Bergman AR 25 Clinton High School Clinton AR 26 Des Arc High School Des Arc AR 27 Green Forest High School Green Forest AR 28 Jacksonville High School Jacksonville AR 29 Mountain Home High School Mountain Home AR 30 Omaha High School Omaha AR 31 Pocahontas High School Dalton AR 32 Riverside High School Lake City AR 33 Sheridan High School Sheridan AR 34 Wynne High School Wynne AR 35 BASIS Phoenix Phoenix AZ 36 Blue Ridge High School Lakeside AZ 37 Cactus High School Glendale AZ 38 Campo Verde High School Gilbert AZ 39 Catalina Foothills High School Tucson AZ 40 Edge High School Himmel Park Tucson AZ 41 Edge High School NW Tucson AZ 42 Great Hearts Academies - Veritas Prep Phoenix AZ 43 Hamilton High School Chandler AZ 44 Independence HS Glendale AZ 45 Lake Havasu City High School Lake Havasu City AZ 46 Mesquite High School Gilbert AZ A B C 47 Show Low High School Show Low AZ 48 Veritas Preparatory Academy Phoenix AZ 49 American Heritage School Plantation FL 50 Apopka High School Apopka FL 51 Booker T. -

Download Electronic Document

City Manager’s Office 215 E. McKinney St., Denton, TX 76201 (940) 349-8307 MEMORANDUM DATE: November 2, 2018 TO: The Honorable Mayor Watts and Council Members FROM: Todd Hileman, City Manager SUBJECT: Friday Staff Report I. Council Schedule A. Meetings 1. City Council Luncheon Meeting on Monday, November 5, 2018 at 11:00 a.m. in the Airport Meeting Room at Denton Enterprise Airport, 5000 Airport Road, Denton, Texas. 2. Committee on the Environment Meeting on Monday, November 5, 2018 at 2:00 p.m. in the City Council Work Session Room. 3. Traffic Safety Commission Meeting on, Monday, November 5, 2018 at 5:30 p.m. in the City Council Work Session Room. 4. Audit/Finance Committee Meeting on Tuesday, November 6, 2018 at 11:00 a.m. in the City Hall Conference Room. 5. Work Session of the City Council on Tuesday, November 6, 2018 at 2:00 p.m. in the City Council Work Session Room followed by a Regular Meeting in the Council Chambers at 6:30 p.m. 6. No Agenda Committee Meeting on Wednesday, November 7, 2018. 7. Development Code Review Committee Meeting on Friday, November 9, 2018 at 11:00 a.m. in the City Council Work Session Room. B. Upcoming Events 1. NLC City Summit, November 7-10, 2018 in Los Angeles, CA. 2. Denton County Days, February 18-20, 2019 in Austin, TX. OUR CORE VALUES Integrity Fiscal Responsibility Transparency Outstanding Customer Service II. General Information & Status Update A. Zero Energy Housing - At the Oct. 16 City Council meeting, Council Member Hudspeth requested information about the new zero energy housing development in Frisco that has recently been publicized through various media outlets. -

C.H. Collins Athletic Complex Stadium Information and Regulations

Denton Independent School District C.H. Collins Athletic Complex Stadium Information and Regulations Welcome to the C.H. Collins Athletic Complex A facility that reflects the successes of past, present, and future students As a successful coach and high school administrator, C.H. Collins, Sr., has been described as a legend in Denton’s history because of the impact he made on so many lives. Coach Collins loved sports and playing sports was the gateway for him to further his education and expand his horizons. In high school, he was awarded a scholarship to Jarvis Christian College in Hawkins, Texas. Mr. Collins had a love of music and sang in the college choir. It was singing that brought C.H. and his wife, Esta, together. The two were married for 54 years and had four children. Coach Collins came to Denton ISD in 1954 as the football, basketball and track coach for the Fred Moore High School Dragons. He was a winning coach – consistently taking his teams to district and regional competitions, plus three state finals. The NFL named two of his players, Carl Garrett and Don Woods, as Rookie of the Year. One of his most successful tributes occurred in 1967 when Coach Collins helped integrate Fred Moore High School with Denton High and he continued his coaching career at Denton High. After the successful integration, he became Dean of Men at Denton High until he retired in 1986. After Mr. Collins died in 1996, the Board of Trustees of Denton ISD named the new athletic facility after him to honor this outstanding coach. -

Alumni and Students to Stage Homecoming Nov. 11

■i CAMPUS NEWS COMPLETELY COVERED BY DEPARTMENT OF JOURNALISM STUDENTS ■ i Frogland Awaits You, Exet! Official Student Body Publication of Texat Chritlian Vnivertity VOL. XXXI. FORT WORTH. TEXAS, FRIDAY, NOVEMBER 4, 1932 NO. 7 Alumni and Students to Stage Homecoming Nov. 11 Members of All Principals in Homecoming Celebration to Be Held Next Week-End Horned Frog-Longhorn Grid Tilt Classes to Help Will Be Main Attraction of Day; In Building Fire Many Other Festivities Planned Baxter Urges Frosh and Pep Rally, Burning of Bonfire, Band Concerts, Upperclassmen to Special Assembly in Chapel and Co-operate. Luncheon All on Program. By JOE SARGENT. Obtains Two Trucks With the Frog-Longhorn football game as the principal at- traction of the day and an ex-lettermen's. banquet, a mammoth Yell Leaders Head Groups in pep rally and bonfire burning, special band concerts, a special Gathering Combustible chapel program and an ex-students' luncheon as other events on Material. the program, past and present students of Texas Christian Uni- versity will celebrate the University's Upperclassmen will have to co-op- annual Homecoming Day Friday, Nov. crate with the freshmen in building Plans Made for 11. the bonfire this year, Ben Baxter, President Edward McShane Wait*, heed yell leader, told the University IMF- Piece Band Dr. Edwin A. Elliott, president of the men at a meeting held Wednesday Ex-Students' Association, and Marion morning. Musicians Journey to Hicks, president of the student body, The small number of freshmen are urging all ex-students of the Uni- makes it necessary for members of Fair—Concerts to versity to attend and take part in the other classes to aid in the gathering Be Given. -

Denton High School

DHS PTSA Newsletter Denton High School "In the Ultimate Pursuit of Excellence in Education" A N I NTERNATIONAL B ACCALAUREATE W O R L D S CHOOL DHS PTSA Newsletter 3rd Six Weeks Edition January 2011 DISD—Denton High Muncy’s Message School 1007 Fulton Street Happy New Year, Broncos! Denton, TX 76201 (940) 369-2000 With the turkey season comfortably behind us, and the winter break coming in with a bite, it is Fax (940) 369-4953 safe to say that it is officially fire place weather. I enjoy this time of year. I am a believer that www.dentonisd.org when it’s cold outside, the hearts of those around us warm the air for our enjoyment. TABLE OF CONTENTS At DHS every year, our Student Council/Renaissance hosts a campus wide adopt-a-school Volunteer Information...page 2 Book Cents ……………..page 2 Christmas party for the kids at The Ann Windle School for Young Children. Second block 9th Grade Officers …….. page 2 classes collect money, buy gifts, prepare food and invite the little ones from AWS into their class. New School Nurse …….. page 2 It is one of the greatest rewards to see the joy on the faces of our guests as they tear into the PTSA Reflections Contest Winners…………page 2 presents that are laid out in front of them. The little ones anxiously throw the clothes to the side Financial Aid Workshop.…p.3 and dig in for the toys with anticipation and excitement. Without a doubt, this event is one of the Grad Night …………….page 3 most anticipated parties on campus annually. -

Denton High School Bronco Band Handbook

Denton High School Bronco Band Handbook 2017 - 2018 - DHS Band Mission Statement - The DHS Band is a family of students brought together by a common goal: success. Our passion and dedication allows us to excel not only in music but also in life by surpassing all obstacles and becoming role models for our peers. In a supportive community, we continue to set new standards and uphold the PRIDE of Bronco Country. ~ 2 ~ Director Contact Information Brian Wilson Director of Bands 940-369-2219 [email protected] Jesse Woolery Associate Director of Bands 940-369-2209 [email protected] Phillip Elder Director of Percussion 940-369-2225 [email protected] Ashley Maldonado Color Guard Director 214-310-8814 [email protected] ~ 3 ~ GENERAL BAND PROCEDURES This handbook will spell out in detail several rules and guidelines that are necessary to have a successful band program. However, listed below are some general guidelines to follow in all situations. 1. All rehearsals are mandatory. 2. Gum, food, and drinks, other than bottled water, are prohibited in the band hall. 3. Be on time, if not early, to all band rehearsals and performances. 4. Respect other band members, parents, and directors. 5. Respect the property of the school and of others. 6. Always portray a positive attitude in your words and actions. 7. Give 110% effort 110% of the time. ~ 4 ~ ATTENDANCE POLICY WORK SCHEDULES, FAMILY TRIPS, AND OTHER ACTIVITIES must not interfere with the rehearsal and performance schedule provided at the beginning of the school year. Students who enroll in other school activities such as athletics, choir, theatre, etc. -

JP Morgan Hilltopsecurities Raymond James

Enhanced/Unenhanced Ratings: Fitch “Applied For” S&P “Applied For” (See “RATINGS” and “THE PERMANENT SCHOOL FUND GUARANTEE PROGRAM”) PRELIMINARY OFFICIAL STATEMENT Dated: April 8, 2016 NEW ISSUE: BOOK-ENTRY-ONLY In the opinion of Bond Counsel, interest on the Bonds will be excludable from gross income for federal income tax purposes under statutes, regulations, published rulings and court decisions existing on the date thereof, subject to the matters described under “TAX MATTERS” herein, including the alternative minimum tax on corporations. y offers to buy be accepted prior to the to prior accepted y offers to buy be $118,784,195.95* offer to buy nor shall there be any sale of be any sale of shall there to buy nor offer DENTON INDEPENDENT SCHOOL DISTRICT (A political subdivision of the State of Texas located in Denton County, Texas) UNLIMITED TAX REFUNDING BONDS, SERIES 2016 Dated Date: April 1, 2016 Due: August 15, as shown on page 2 Interest Accrual Date: Date of Delivery The Denton Independent School District (the “District”) is issuing its $118,784,195.95* Unlimited Tax Refunding Bonds, Series 2016 (the “Bonds”) in accordance with the Constitution and general laws of the State of Texas, including, particularly, Chapter 1207, Texas Government Code, as amended, and a bond order (the “Bond Order”) passed by the Board of Trustees (the “Board”) of the District on February 23, 2016 in which the Board delegated pricing of the Bonds and certain other matters to a “Pricing Officer” who will approve and execute a “Pricing Certificate” which will complete the sale of the Bonds (the Bond Order and the Pricing Certificate are jointly referred to as the “Order”). -

AVCA High School All-Region

AVCA High School All-Region Region First Name Last Name Height Position High School Name City State College Commitment 1 Zoe Lowe 5'10" OH Bristol Eastern High School Bristol CT Florida Southern 1 Sydney Yim 6'0" S/RS Newburyport High School Newburyport MA Purdue University 1 Annika Hester 6'4" OH Falmouth High School Falmouth ME San Diego State 1 Clare Isaksen 5'9" S Burnt Hills-Ballston Lake High School Burnt Hills NY 1 Olivia Walczak 5'11" OH Clarence High School Clarence NY 1 Sally Tietjen 5'9" OH Smithtown High School Smithtown NY 2 Rachel Richardson 5'9" OH St. John's College High School Washington DC Duke University 2 Mary Grace Goyena 6'0" OH Mount de Sales Academy Catonsville MD Georgetown University 2 Lauren Wilcock 5'11" OH Mendham High School Mendham NJ University of South Carolina 2 Brenna Campbell 5'6" S Clarion Area High School Clarion PA McDaniel College 2 Erica Selfridge 5'8" OH Clarion Area High School Clarion PA 2 Cassidy Snider 6'0 OH Conneaut Area Senior High Linesville PA Clarion University 2 Sydnee Ashbrook 5'10" MB North Star High School Boswell PA Mercyhurst University 2 Makayla Jackson 6'2" MB Plum High School Pittsburgh PA University of Pittsburgh 2 Sarah White 6'0 S/RS Seneca Valley High School Harmony PA Ohio State University 2 Kacy Sekunda 5'10" S/RS State College High School Huntingdon PA Loyola University-Maryland 2 Sophie Brenner 5'11" OH Unionville High School Kennett Square PA Loyola University-Maryland 2 Grace Frigaard 6'0" OH James Wood High School Winchester VA 2 Lainie Putt 5'10" RS James Wood High School Winchester VA St. -

2012-2013 Student Resource Guide.Indd

Listed in this pamphlet are counseling and support organizations, agencies, and individuals, public and private, who perform a variety of services in or near the Denton area. This list is offered strictly as a resource and should not be con- sidered a recommendation, referral, or endorsement to any particular service provider. This list is not all inclusive and is offered only for your convenience. For more information regarding the list of services offered in this pamphlet, please contact: Larry Mankoff, Supervisor Student and Employee Assistance Programs (940) 369-0598 or email: [email protected] Enlistados en este folleto hay servicios de consulta y organizaciones de asistencia, agencias e individuos, públicos y privados, los cuáles desempeñan una variedad de servicios en o cerca del área de Denton. Para más información, por favor llame a la Oficina de Servicios Sociales al (940) 369-0598. ON-LINE ACCESS TO THIS DOCUMENT This document can also be viewed with active links on the Denton ISD Counseling Services Webpage by following the steps below: • Go to the DISD homepage at www.dentonisd.org • Click the top tab that says “Departments” • Click Counseling Services • Click Community Support Programs For more information please visit the following website: www.dentonisd.org Revised for the 2012-2013 school year TABLE OF CONTENTS Page Community Mental Health and Substance Abuse Services ............................4 • Centro de Consejeria • Chrysalis – eating disorders • Cook Children’s Behavioral Health • Counseling Center of Denton -

2021 Baseball Game Notes

COLLEGE WORLD SERIES 2014, 2016, 2018, 2019 BIG 12 TITLES 1997, 1998, 2016, 2017, 2019 2021 BASEBALL GAME NOTES 2021 Schedule / Results Shriners Hospitals for Children College Classic FEBRUARY (3-3) March 5-7 • Minute Maid Park • Houston, Texas College Baseball Showdown (Arlington, Tx) #10 TEXAS TECH RED RAIDERS TEXAS STATE BOBCATS 20 ^ vs. #8 Arkansas FloBaseball L, 13-9 2021 Record ____ 5-3 Overall • 0-0 Big 12 Record _______ 4-6 Overall • 0-0 Sun Belt 21 ^ vs. #6 Ole Miss FloBaseball L, 5-4 Home/Away/Neutral _____5-0 / 0-0 / 0-3 Home/Away/Neutral _____3-3 / 0-3 / 1-0 22 ^ vs. #8 Mississippi State FloBaseball L, 11-5 Rankings: ___D1: 10 • BA: 12 • NCBWA: 15 Rankings: _ D1: NR • BA: NR • Coaches: NR 26 HOUSTON BAPTIST ESPN+ W, 18-3 (7) _________ CB: 10 • PG: 8 • Coaches: 11 _________CB: NR • PG: NR • NCBWA: NR 27 HOUSTON BAPTIST ESPN+ W, 8-1 Head Coach ________________Tim Tadlock Head Coach _______________Steven Trout 28 HOUSTON BAPTIST ESPN+ W, 11-2 Career Record ________ 741-282 (18th) Career Record ____________52-35 (3rd) Record at Texas Tech ___ 306-155 (9th) Record at Texas St. _______ 18-10 (2nd) MARCH (2-0) SAM HOUSTON STATE BEARKATS TEXAS A&M-CC ISLANDERS 2 TEXAS SOUTHERN W, 14-2 Record ______ 1-4 Overall • 0-0 Southland Record ______ 4-4 Overall • 0-0 Southland 3 TEXAS SOUTHERN ESPN+ W, 15-0 Home/Away/Neutral _____1-2 / 0-1 / 0-1 Home/Away/Neutral _____4-2 / 0-2 / 0-0 Shriners College Classic (Houston) Rankings: _ D1: NR • BA: NR • Coaches: NR Rankings: _ D1: NR • BA: NR • Coaches: NR 5 ! vs. -

Denton High School 2019

Grade Point Average College Placement Approximately 70% of our graduates will go on to higher Denton High School GPA will be calculated for the foundation courses as follows: education. Denton High graduates will continue their formal education with 40% attending four-year institutions and 30% 4 - Language Arts courses going on to community colleges, 2% attending technical 4 - Science courses (1 each/Biology, Chemistry, Physics, and 1 additional course) schools, and 2% entering the armed services. 4 - Social Studies courses 4 - Math courses (highest 8 semesters) National Merit 2 - World Language (highest 4 semesters of same course) The senior class of 2019 had seven National Merit Commended Scholars, one National Hispanic Recognition GPA foundation courses will be calculated whether Program Scholar, twenty-two AP Scholars, eight AP Scholars the student took the class during the regular school year, in with Honors, and six AP Scholars with Distinction. summer school, by correspondence, by course exam, or by dual enrollment. GPA and rank are calculated on a 4-point scale with a 1-point bonus for IB, Honors, AP, and Dual credit classes. Only 18 (36 semesters) academic foundation courses are used in the calculation. Only courses taken during 9th through Denton High School 12th grade will be computed in a student’s GPA. Earned GPA from courses completed within the prescribed 18 is Joel Hays, Principal used to rank students through the 6th & 7th semesters. Highest GPA in present senior class is 5.0. Scott Nedrow, Instructional Associate Principal Kimberly Thaggard, Assistant Principal (A-C) An International Baccalaureate World School Joanne Keeler, Assistant Principal (D-H) Frank Perez, Assistant Principal (I-N) Grade Points Earned Matt Smith, Assistant Principal (O-R) Mark Goggins, Assistant Principal (S-Z) No. -

Denton County Community Services Directory

Denton County Community Services Directory 2013 Edition Information & Referral Helpline Call 211 or 1-800-548-1873 (answered 24 hours a day, 7 days a week) Sponsored by: and SPECIAL THANKS TO THE UNIVERSITY OF NORTH TEXAS COLLEGE OF PUBLIC AFFAIRS AND COMMUNITY SERVICE FOR THEIR GENEROUS FINANCIAL SUPPORT . The College of Public Affairs and Community Service’s mission is to strengthen communities through education, scholarship and engagement. With seven academic departments and several centers, institutes and professional programs, PACS is transforming the quality of life and becoming the “go-to” resource for community issues in Texas. Students from our college are prepared for a variety of careers in the public, private and nonprofit sectors. Our alumni can be found working in a wide range of settings such as, Federal Emergency Management Administration, Child Protective Services, Texas Scottish Rite Hospital for Children, U.S. Department of State, Peace Corps, Texas Youth Commission and many others. United Way of Denton County, Inc. All listings provided in this directory are for information only and their inclusion does not constitute endorsement. Every effort has been made to identify all governmental and not for profit agencies and organizations in Denton County, providing programs and services on a regular basis. Agencies wishing to be con- sidered for inclusion should apply in writing to: Information & Referral Helpline 625 Dallas Dr., Suite 525 Denton, TX 76205 A special thank-you to our book sponsors: AlphaGraphics and UNT College of Public Affairs and Community Service If you are interested in becoming a sponsor, please contact us at 940-566-5851 ext.