Introduction

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Civil Disobedience from a Biblical Perspective

LIBERTY UNIVERISTY Submitted to Professor Fischer for the Journal of Statesmanship and Public Policy by Gabriel Z. Reed December 7th, 2020 Gabriel Z. Reed is an undergraduate student at Liberty University studying International Relations focusing on Strategic Intelligence, minoring in History. He intends to pursue a Master’s Degree in History at Liberty University. He served as a research assistant for the Family Foundation, and has a background in the ecclesiastical field. Introduction To say that civil disobedience is a complicated topic is to severely understate the topic. It is a subject matter that has derived many different and disparate opinions, points of view, and public policies. Specifically, within America today, we observe calls for civil disobedience from both sides of the political spectrum, over several divergent political ideals. These issues are, primarily, driven from both sides’ desire to provide protection and provision for the oppressed and those who cannot necessarily speak for themselves. The definition of who is necessarily oppressed and whom their oppressors are varies from person to person, regardless of political affiliation. At the present moment, the general consensus from either side of the fence appears to be that we are existing in an increasingly flawed system, and that there appears to be fewer and fewer ways to address it within the bounds of our current legal system. This has led both sides to take drastic measures increasingly outside the rule of law in order for their voices to be heard. For Judeo- Christians, this causes no small amount of conflict. What manner of steps should those of the mind to intervene for whatever issue they feel is pressing be capable of doing, within the moral framework of their own worldview? In this essay, these issues shall be examined, both with regards to our own American and Western history, and when it comes to Biblical viewpoints on such pressing matters. -

Black Anarchism, Pedro Riberio

TABLE OF CONTENTS 1. Introduction.....................................................................................................................2 2. The Principles of Anarchism, Lucy Parsons....................................................................3 3. Anarchism and the Black Revolution, Lorenzo Komboa’Ervin......................................10 4. Beyond Nationalism, But not Without it, Ashanti Alston...............................................72 5. Anarchy Can’t Fight Alone, Kuwasi Balagoon...............................................................76 6. Anarchism’s Future in Africa, Sam Mbah......................................................................80 7. Domingo Passos: The Brazilian Bakunin.......................................................................86 8. Where Do We Go From Here, Michael Kimble..............................................................89 9. Senzala or Quilombo: Reflections on APOC and the fate of Black Anarchism, Pedro Riberio...........................................................................................................................91 10. Interview: Afro-Colombian Anarchist David López Rodríguez, Lisa Manzanilla & Bran- don King........................................................................................................................96 11. 1996: Ballot or the Bullet: The Strengths and Weaknesses of the Electoral Process in the U.S. and its relation to Black political power today, Greg Jackson......................100 12. The Incomprehensible -

Love Your Enemies

By President Dallin H. Oaks First Counselor in the First Presidency said, Thou shalt love thy neighbour, and hate thine enemy. Love Your Enemies “But I say unto you, Love your enemies, bless them that curse you, do good to them that hate you, and pray for them which despitefully use Knowing that we are all children of God gives us a you, and persecute you” (Matthew 5:43–44).1 vision of the worth of others and the ability to rise For generations, Jews had been taught to hate their enemies, and they above prejudice. were then suffering under the domi- nation and cruelties of Roman occu- pation. Yet Jesus taught them, “Love your enemies” and “do good to them The Lord’s teachings are for eternity spilled over into political statements that . despitefully use you.” and for all of God’s children. In this and unkind references in our Church What revolutionary teachings for message I will give some exam- meetings. personal and political relationships! ples from the United States, but the In a democratic government we But that is still what our Savior com- principles I teach are applicable will always have differences over mands. In the Book of Mormon we everywhere. proposed candidates and policies. read, “For verily, verily I say unto you, We live in a time of anger and However, as followers of Christ we he that hath the spirit of contention hatred in political relationships and must forgo the anger and hatred with is not of me, but is of the devil, who policies. -

Selected Chronology of Political Protests and Events in Lawrence

SELECTED CHRONOLOGY OF POLITICAL PROTESTS AND EVENTS IN LAWRENCE 1960-1973 By Clark H. Coan January 1, 2001 LAV1tRE ~\JCE~ ~')lJ~3lj(~ ~~JGR§~~Frlt 707 Vf~ f·1~J1()NT .STFie~:T LA1JVi~f:NCE! i(At.. lSAG GG044 INTRODUCTION Civil Rights & Black Power Movements. Lawrence, the Free State or anti-slavery capital of Kansas during Bleeding Kansas, was dubbed the "Cradle of Liberty" by Abraham Lincoln. Partly due to this reputation, a vibrant Black community developed in the town in the years following the Civil War. White Lawrencians were fairly tolerant of Black people during this period, though three Black men were lynched from the Kaw River Bridge in 1882 during an economic depression in Lawrence. When the U.S. Supreme Court ruled in 1894 that "separate but equal" was constitutional, racial attitudes hardened. Gradually Jim Crow segregation was instituted in the former bastion of freedom with many facilities becoming segregated around the time Black Poet Laureate Langston Hughes lived in the dty-asa child. Then in the 1920s a Ku Klux Klan rally with a burning cross was attended by 2,000 hooded participants near Centennial Park. Racial discrimination subsequently became rampant and segregation solidified. Change was in the air after World "vV ar II. The Lawrence League for the Practice of Democracy (LLPD) formed in 1945 and was in the vanguard of Post-war efforts to end racial segregation and discrimination. This was a bi-racial group composed of many KU faculty and Lawrence residents. A chapter of Congress on Racial Equality (CORE) formed in Lawrence in 1947 and on April 15 of the following year, 25 members held a sit-in at Brick's Cafe to force it to serve everyone equally. -

Ch 4, Launching the Peace Movement, and Skim Through Ch

-----------------~-----~------- ---- TkE u. s. CENT'R.A.L A.MERIC.A. PE.A.CE MOVEMENT' CHRISTIAN SMITH The University of Chicago Press Chicago and London List of Tables and Figures ix Acknowledgments xi Acronyms xiii Introduction xv portone Setting the Context 1. THE SOURCES OF CENTRAL AMERICAN UNREST 3 :Z. UNITED STATES INTERVENTION 18 J. Low-INTENSITY WARFARE 33 porttwo The Movement Emerges -'. LAUNCHING THE PEACE MOVEMENT 5 9 5. GRASPING THE BIG PICTURE 87 '. THE SOCIAL STRUCTURE OF MORAL OUTRAGE 13 3 '1'. THE INDIVIDUAL ACTIVISTS 169 porlthreeMaintaining the Struggle 8, NEGOTIATING STRATEGIES AND COLLECTIVE IDENTITY 211 1'. FIGHTING BATTLES OF PUBLIC DISCOURSE 231 1 O. FACING HARASSMENT AND REPRESSION 280 11. PROBLEMS FOR PROTESTERS CLOSER TO HOME 325 1%. THE MOVEMENT'S DEMISE 348 portfour Assessing the Movement 1J. WHAT DID THE MOVEMENT ACHIEVE? 365 1-'. LESSONS FOR SOCIAL-MOVEMENT THEORY 378 ii CONTENTS Appendix: The Distribution and Activities of Central America Peace Movement Organizations 387 Notes 393 Bibliography 419 ,igures Index 453 Illustrations follow page 208. lobles 1.1 Per Capita Basic Food Cropland (Hectares) 10 1.2 Malnutrition in Central America 10 7.1 Comparison of Central America Peace Activists and All Adult Ameri cans, 1985 171 7.2 Occupational Ratio of Central America Peace Movement Activist to All Americans, 1985 173 7.3 Prior Social Movement Involvement by Central American Peace Activists (%) 175 7.4 Central America Peace Activists' Prior Protest Experience (%) 175 7.5 Personal and Organizational vs. Impersonal -

Render Unto Caesar

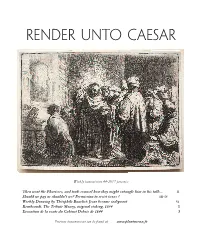

RENDER UNTO CAESAR Weekly transmission 44-2017 presents: Then went the Pharisees, and took counsel how they might entangle him in his talk... II Should we pay or shouldn't we? Permission to resist taxes ? III-IV Weekly Drawing by Théophile Bouchet: Jesus became indignant VI Rembrandt. The Tribute Money, original etching, 1634 1 Evocation de la vente du Cabinet Debois de 1844 3 Previous transmissions can be found at: www.plantureux.fr Matthew 22:15-22 — KJV [King James Version] 15. Then went the Pharisees, and took counsel how they might entangle him in his talk. 16. And they sent out unto him their disciples with the Herodians, saying, Master, we know that thou art true, and teachest the way of God in truth, neither carest thou for any man: for thou regardest not the person of men. 17. Tell us therefore, What thinkest thou? Is it lawful to give tribute unto Caesar, or not? 18. But Jesus perceived their wickedness, and said, Why tempt ye me, ye hypocrites? 19. Shew me the tribute money. And they brought unto him a penny. 20. And he saith unto them, Whose is this image and superscription? 21. They say unto him, Caesar's. Then saith he unto them, Render therefore unto Caesar the things which are Caesar's; and unto God the things that are God's. 22. When they had heard these words, they marvelled, and left him, and went their way. The e-bulletins present articles as well as selections of books, albums, photographs and documents as they have been handed down to the actual owners by their creators and by amateurs from past generations. -

Thoughts from Render Unto Caesar Serving the Nation by Living Our Catholic Beliefs in the Political Life by Frank Caliva

Thoughts from Render Unto Caesar Serving the Nation by Living Our Catholic Beliefs in the Political Life by Frank Caliva Discussions about politics and public life are often tricky, as many young people have strong opinions that reflect the deep political divisions in our country. Discussions can quickly turn emotional, and disagreements can move almost without warning from the abstract to the personal. Nevertheless, it is important for youth ministers to address our faith and public life, for at least two reasons. First, we live in the shadow of our nation’s capital, and political awareness is incredibly high among teens in the Diocese of Arlington. Second, and more importantly, this discussion is important because the act of participating in our own governance is not just a political right or a civic duty – it’s a moral responsibility.1 In 2008, during the hotly contested presidential election, the Most Rev. Charles J. Chaput, Archbishop of Denver, wrote a small but powerful book entitled, Render Unto Caesar. The book explores the complex relationship between our Catholic creed and our political beliefs. The idea that there is any relationship between faith and politics makes a lot of people, particularly in modern day America, very nervous. We have a long and proud tradition of religious freedom and tolerance in the United States, and this is a good thing. But in our concern about preventing one religion from dominating, perhaps we have gone to the other extreme, in which faith is entirely excluded from public life. Archbishop Chaput argues that this does not make a lot of sense if we take our faith seriously: People who take God seriously will not remain silent about their faith. -

“WHAT WE ARE to RENDER to CAESAR and GOD” (Matthew 22:15-22)

“WHAT WE ARE TO RENDER TO CAESAR AND GOD” (Matthew 22:15-22) The two subjects we’re told to avoid talking about is politics and religion. You can talk about the weather, you can talk about the grandkids, but stay away from politics and religion. We all know that talking about religion can stir up tension. You can be talking to someone about how the fishing is or the storm front that’s moving in, and things are breezy and light. But bring up God and suddenly the walls go up. How about politics? Right now, politics that may be even more divisive than religion, and arguing over politics is nothing new. In 1858 – just a few years before the Civil War – things got heated at a late-night session of congress where slavery and state’s rights were being debated. A Republican from Pennsylvania and a Democrat from South Carolina began insulting each other – imagine that – and soon they were shouting at each other, and then one of them threw a punch and a fist fight broke out right on the floor of the congress. 30 other congressmen left their seats and joined in on the fight before the sergeant-of-arms was able to break it up. Two years before that, a senator from South Carolina walked up to a fellow senator from Massachusetts on the senate floor and started beating him with a cane, and nearly killed him. Political tensions are nothing new, and many see parallels between our political divide today and that of the days leading up to the Civil War. -

The Greatest Commandment Matthew 22: 34-46; Psalm 90: 1-6, 13-17; I Thes

The Greatest Commandment Matthew 22: 34-46; Psalm 90: 1-6, 13-17; I Thes. 2: 1-8 It’s been a long campaign season. We should be used to incidents like this - people trying to trip up the opponent with trick questions. Well, we can’t even get away from it even in the bible – can we? But before we tackle today’s story, let’s once again take a step back. I have been following the lectionary the past number of messages and concentrating on gospel passages from Matthew. Mostly we have heard Jesus telling parables about the kingdom of heaven, the reign of God. We end up with lessons like: • The first shall be last and the last shall be first. • It is better to actually do the work than to have the right beliefs about the work. • The great banquet is prepared and all are invited. These parables and lessons are good news for many of those who are following Jesus, for the disciples and others in the large crowds that surround Jesus. But these are not comforting parables or visions for the Pharisees and Sadducees. Part of the time they don’t understand what Jesus is talking about. When they do understand, they don’t like what they hear. The establishment (in this case the religious leaders) is not big on being dissed in public. To save face the Pharisees and Sadducees try to get back at Jesus. We didn’t get to these readings, but you probably remember the stories. Earlier in Matthew 22, the Pharisees try out some trick questions on Jesus. -

Bedau’S Introduction Sets out the Issues and Shows How the Various Authors Shed Light on Each Aspect of Them

CIVIL DISOBEDIENCE in focus How can civil disobedience be defined and distinguished from revolution or lawful protest? What, if anything, justifies civil disobedience? Can nonviolent civil disobedience ever be effective? The issues surrounding civil disobedience have been discussed since at least 399 BC and, in the wake of such recent events as the protest at Tiananmen Square, are still of great relevance. By presenting classic and current philosophical reflections on the issues, this book presents all the basic materials needed for a philosophical assessment of the nature and justification of civil disobedience. The pieces included range from classic statements by Plato, Thoreau, and Martin Luther King, to essays by leading contemporary thinkers such as Rawls, Raz, and Singer. Hugo Adam Bedau’s introduction sets out the issues and shows how the various authors shed light on each aspect of them. Hugo Adam Bedau is Austin Fletcher Professor of Philosophy at Tufts University. ROUTLEDGE PHILOSOPHERS IN FOCUS SERIES General Editor: Stanley Tweyman York University, Toronto GÖDEL’S THEOREM IN FOCUS Edited by S. G. Shanker J. S. MILL: ON LIBERTY IN FOCUS Edited by John Gray and G. W. Smith DAVID HUME: DIALOGUES CONCERNING NATURAL RELIGION IN FOCUS Edited by Stanley Tweyman RENÉ DESCARTES’ MEDITATIONS IN FOCUS Edited by Stanley Tweyman PLATO’S MENO IN FOCUS Edited by Jane M. Day GEORGE BERKELEY: ALCIPHRON IN FOCUS Edited by David Berman ARISTOTLE’S DE ANIMA IN FOCUS Edited by Michael Durrant WILLIAM JAMES: PRAGMATISM IN FOCUS Edited by Doris Olin JOHN LOCKE’S LETTER ON TOLERATION IN FOCUS Edited by John Horton and Susan Mendus CIVIL DISOBEDIENCE in focus Edited by Hugo Adam Bedau London and New York First published 1991 by Routledge 11 New Fetter Lane, London EC4P 4EE This edition published in the Taylor & Francis e-Library, 2002. -

ISSN: 2320-5407 Int. J. Adv. Res. 8(05), 471-476

ISSN: 2320-5407 Int. J. Adv. Res. 8(05), 471-476 Journal Homepage: - www.journalijar.com Article DOI: 10.21474/IJAR01/10950 DOI URL: http://dx.doi.org/10.21474/IJAR01/10950 RESEARCH ARTICLE THOREAU’S CIVIL DISOBEDIENCE: A VOICE OF NON-VIOLENT RESISTANCE TO DISSENT AN UNJUST POLITICAL CONTEXT Dr. C. Masilamani Asst. Professor of English Kristu Jayanti College Bangalore, India-560077. …………………………………………………………………………………………………….... Manuscript Info Abstract ……………………. ……………………………………………………………… Manuscript History This article reviews Henry David Thoreau‟s social and political Received: 12 March 2020 philosophy of Civil Disobedience, which rebels against government‟s Final Accepted: 14 April 2020 brutality and it suggests fighting against tyranny to get freedom, Published: May 2020 breaking with conventional customs, rejecting the social traditions and values and unjust law and policies affecting the democrats. This study Key words:- Civil Disobedience, Political also reviews some of the writings of political situations which display Philosophy, Transcendentalism, Slavery, the political meanings and aspirations. The purpose of the article is to Literature of Politics, Mass of Men, explore the power and importance of individual over groups, especially Rebellion, Rationalism, and Non-Violent government through Thoreau‟s Civil Disobedience. In addition, it also Resistance tries to discuss how people‟s taxes are misused by the government for an unnecessary war and dispute with other countries instead of taking good care their own citizens. Therefore, this article seeks to discuss and eventually justify the relevance of civil disobedience as a catalyst of positive change for the stability and sustainability of the democratic process and system of government in a state. It also evaluates his open call for every citizen to sacrifice oneself for the nation‟s cause not to pay taxes and avoid colluding with government by refusing to play an active role. -

The Peace Tax Seven Are

conscience issue 125 summer 2004 update newsletter of conscience THE PEACE TAX CAMPAIGN The Peace Tax Seven are Go! The Peace Tax Seven, a group of conscientious objectors and war tax resisters, have sent their “Letter before Action” to Gordon Brown; the first step on the long road to a Judicial Review. The Seven are seeking a Judicial Review of current tax law, which makes them complicit in killing if they carry out their civic duty and pay their taxes or makes them criminals if they follow their conscience and refuse to pay taxes conscience for war and war preparations. The “Letter before Action” informs the government of their intention to seek a Judicial Review and sets out their reasons for doing so. The government has 28 days to respond to photos | Oliver Haslam/ the letter. Once they have this response The conscience “Peace Tax Collectors” set up their office at the Glastonbury festival this year the Peace Tax Seven can move on to (see page 2 for the full story). the next step of the process, which is to seek a pre-emptive costs order. If the in the public interest that the legal case Judicial Review goes against the Peace against the war be heard and that the Tax Seven, they would be liable for groups taking the case should not have the government’s costs as well as their to risk bankruptcy for this to happen. own; if they are granted a pre-emptive If the Seven are also successful conscience costs order this will place a cap on their in persuading a judge that their case is campaigns for the liability for the government’s costs.