Terrorist Exploitation of Zakat and Its Complications in the War on Terror

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Virtual Currencies and Terrorist Financing : Assessing the Risks And

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT FOR CITIZENS' RIGHTS AND CONSTITUTIONAL AFFAIRS COUNTER-TERRORISM Virtual currencies and terrorist financing: assessing the risks and evaluating responses STUDY Abstract This study, commissioned by the European Parliament’s Policy Department for Citizens’ Rights and Constitutional Affairs at the request of the TERR Committee, explores the terrorist financing (TF) risks of virtual currencies (VCs), including cryptocurrencies such as Bitcoin. It describes the features of VCs that present TF risks, and reviews the open source literature on terrorist use of virtual currencies to understand the current state and likely future manifestation of the risk. It then reviews the regulatory and law enforcement response in the EU and beyond, assessing the effectiveness of measures taken to date. Finally, it provides recommendations for EU policymakers and other relevant stakeholders for ensuring the TF risks of VCs are adequately mitigated. PE 604.970 EN ABOUT THE PUBLICATION This research paper was requested by the European Parliament's Special Committee on Terrorism and was commissioned, overseen and published by the Policy Department for Citizens’ Rights and Constitutional Affairs. Policy Departments provide independent expertise, both in-house and externally, to support European Parliament committees and other parliamentary bodies in shaping legislation and exercising democratic scrutiny over EU external and internal policies. To contact the Policy Department for Citizens’ Rights and Constitutional Affairs or to subscribe to its newsletter please write to: [email protected] RESPONSIBLE RESEARCH ADMINISTRATOR Kristiina MILT Policy Department for Citizens' Rights and Constitutional Affairs European Parliament B-1047 Brussels E-mail: [email protected] AUTHORS Tom KEATINGE, Director of the Centre for Financial Crime and Security Studies, Royal United Services Institute (coordinator) David CARLISLE, Centre for Financial Crime and Security Studies, Royal United Services Institute, etc. -

On the Norms of Charitable Giving in Islam: a Field Experiment

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Lambarraa, Fatima; Riener, Gerhard Working Paper On the norms of charitable giving in Islam: A field experiment DICE Discussion Paper, No. 59 Provided in Cooperation with: Düsseldorf Institute for Competition Economics (DICE) Suggested Citation: Lambarraa, Fatima; Riener, Gerhard (2012) : On the norms of charitable giving in Islam: A field experiment, DICE Discussion Paper, No. 59, ISBN 978-3-86304-058-1, Heinrich Heine University Düsseldorf, Düsseldorf Institute for Competition Economics (DICE), Düsseldorf This Version is available at: http://hdl.handle.net/10419/59571 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend -

Blood Money in Sudan and Beyond: Restorative Justice Or Face-Saving Measure?

BLOOD MONEY IN SUDAN AND BEYOND: RESTORATIVE JUSTICE OR FACE-SAVING MEASURE? A Thesis submitted to the Faculty of The School of Continuing Studies and of The Graduate School of Arts and Sciences in partial fulfillment of the requirements for the degree of Doctor of Liberal Studies By Jacqueline H. Wilson, M.S. Georgetown University Washington, D. C. March 25, 2014 Copyright © 2014 by Jacqueline H. Wilson All Rights Reserved ii BLOOD MONEY IN SUDAN AND BEYOND: RESTORATIVE JUSTICE OR FACE-SAVING MEASURE? Jacqueline H. Wilson, M.S. Mentor/Chair John O. Voll, Ph.D. ABSTRACT This thesis assesses the restorative justice aspects of blood money processes used around the world but focuses primarily on Sudan and South Sudan. It examines sulha, judiya (Darfur), galad (eastern Sudan) and other processes using a mixed methods approach and a multi-site ethnography methodology. The paper scrutinizes these processes from foundational agreements, information gathering and truth-telling, through selecting a third party, and examines truces, exile, women’s roles, compensation agreements, closing rituals, and implementation measures. The paper documents contemporary challenges facing these blood money processes such as collective responsibility, global trends like urbanization, widespread killing and retaliation that rises to a feud, situations where killer and killed are unknown to each other, and situations where blood money is paid by outsiders. I identify shortcomings within these processes relative to international legal norms and human values, as well as areas where they are consistent. Using a restorative justice analytical framework, I determine whether blood money processes are restorative and constitute justice, and ask whether these iii traditional mechanisms are sufficiently robust to stop the cycle of violence. -

Survey of Terrorist Groups and Their Means of Financing

SURVEY OF TERRORIST GROUPS AND THEIR MEANS OF FINANCING HEARING BEFORE THE SUBCOMMITTEE ON TERRORISM AND ILLICIT FINANCE OF THE COMMITTEE ON FINANCIAL SERVICES U.S. HOUSE OF REPRESENTATIVES ONE HUNDRED FIFTEENTH CONGRESS SECOND SESSION SEPTEMBER 7, 2018 Printed for the use of the Committee on Financial Services Serial No. 115–116 ( U.S. GOVERNMENT PUBLISHING OFFICE 31–576 PDF WASHINGTON : 2018 VerDate Mar 15 2010 14:03 Dec 06, 2018 Jkt 000000 PO 00000 Frm 00001 Fmt 5011 Sfmt 5011 G:\GPO PRINTING\DOCS\115TH HEARINGS - 2ND SESSION 2018\2018-09-07 TIF TERRO mcarroll on FSR431 with DISTILLER HOUSE COMMITTEE ON FINANCIAL SERVICES JEB HENSARLING, Texas, Chairman PATRICK T. MCHENRY, North Carolina, MAXINE WATERS, California, Ranking Vice Chairman Member PETER T. KING, New York CAROLYN B. MALONEY, New York EDWARD R. ROYCE, California NYDIA M. VELA´ ZQUEZ, New York FRANK D. LUCAS, Oklahoma BRAD SHERMAN, California STEVAN PEARCE, New Mexico GREGORY W. MEEKS, New York BILL POSEY, Florida MICHAEL E. CAPUANO, Massachusetts BLAINE LUETKEMEYER, Missouri WM. LACY CLAY, Missouri BILL HUIZENGA, Michigan STEPHEN F. LYNCH, Massachusetts SEAN P. DUFFY, Wisconsin DAVID SCOTT, Georgia STEVE STIVERS, Ohio AL GREEN, Texas RANDY HULTGREN, Illinois EMANUEL CLEAVER, Missouri DENNIS A. ROSS, Florida GWEN MOORE, Wisconsin ROBERT PITTENGER, North Carolina KEITH ELLISON, Minnesota ANN WAGNER, Missouri ED PERLMUTTER, Colorado ANDY BARR, Kentucky JAMES A. HIMES, Connecticut KEITH J. ROTHFUS, Pennsylvania BILL FOSTER, Illinois LUKE MESSER, Indiana DANIEL T. KILDEE, Michigan SCOTT TIPTON, Colorado JOHN K. DELANEY, Maryland ROGER WILLIAMS, Texas KYRSTEN SINEMA, Arizona BRUCE POLIQUIN, Maine JOYCE BEATTY, Ohio MIA LOVE, Utah DENNY HECK, Washington FRENCH HILL, Arkansas JUAN VARGAS, California TOM EMMER, Minnesota JOSH GOTTHEIMER, New Jersey LEE M. -

A Commentary on the Prosecution of Benevolence International Foundation Matthew .J Piers

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by DigitalCommons@Pace Pace Law Review Volume 25 Issue 2 Spring 2005 Article 7 The Anti-Terrorist Financing Guidelines: The Impact on International Philanthropy April 2005 Malevolent Destruction of a Muslim Charity: A Commentary on the Prosecution of Benevolence International Foundation Matthew .J Piers Follow this and additional works at: http://digitalcommons.pace.edu/plr Recommended Citation Matthew J. Piers, Malevolent Destruction of a Muslim Charity: A Commentary on the Prosecution of Benevolence International Foundation , 25 Pace L. Rev. 339 (2005) Available at: http://digitalcommons.pace.edu/plr/vol25/iss2/7 This Article is brought to you for free and open access by the School of Law at DigitalCommons@Pace. It has been accepted for inclusion in Pace Law Review by an authorized administrator of DigitalCommons@Pace. For more information, please contact [email protected]. Malevolent Destruction of a Muslim Charity: A Commentary on the Prosecution of Benevolence International Foundation Matthew J. Piers Three years ago we, as a nation, suffered a ghastly act of mass murder and terrorism apparently perpetrated by the self-proclaimed Islamic fundamentalist group, al Qaeda. A remarkable thing occurred in the wake of this tragedy: the United States, already feared and respected as the world's sole remaining super power, became the object of a tidal wave of international support and sympathy. Perhaps never before in our nation's relatively short history have so many hands and hearts reached out to us. The potential to build on this historic outpouring of support and sympathy, both domestically and internationally, was enormous. -

Moral Aspect of Qard

International Journal of Islamic and Middle Eastern Finance and Management Analysing the moral aspect of qard: a shariah perspective Mohammad Abdullah Article information: To cite this document: Mohammad Abdullah , (2015),"Analysing the moral aspect of qard: a shariah perspective", International Journal of Islamic and Middle Eastern Finance and Management, Vol. 8 Iss 2 pp. 171 - 184 Permanent link to this document: http://dx.doi.org/10.1108/IMEFM-11-2013-0116 Downloaded on: 10 June 2015, At: 04:29 (PT) References: this document contains references to 40 other documents. To copy this document: [email protected] The fulltext of this document has been downloaded 17 times since 2015* Users who downloaded this article also downloaded: Ak Md Hasnol Alwee Pg Md Salleh, (2015),"Integrating financial inclusion and saving motives into institutional zakat practices: A case study on Brunei", International Journal of Islamic and Middle Eastern Finance and Management, Vol. 8 Iss 2 pp. 150-170 http://dx.doi.org/10.1108/ IMEFM-12-2013-0126 Catherine S F Ho, (2015),"International comparison of Shari’ah compliance screening standards", International Journal of Islamic and Middle Eastern Finance and Management, Vol. 8 Iss 2 pp. 222-245 http://dx.doi.org/10.1108/IMEFM-07-2014-0065 Bassam Mohammad Maali, Muhannad Ahmad Atmeh, (2015),"Using social welfare concepts to guarantee Islamic banks’ deposits", International Journal of Islamic and Middle Eastern Finance and Management, Vol. 8 Iss 2 pp. 134-149 http://dx.doi.org/10.1108/IMEFM-12-2013-0125 Access to this document was granted through an Emerald subscription provided by Downloaded by Mr Mohammad Abdullah At 04:29 10 June 2015 (PT) Token:JournalAuthor:A812B4BB-195C-4D2C-8A6D-BDAE44C3DDDE: For Authors If you would like to write for this, or any other Emerald publication, then please use our Emerald for Authors service information about how to choose which publication to write for and submission guidelines are available for all. -

Qard-Al-Hassan As a Tool for Poverty Alleviation: a Case Study of the Fael Khair Waqf Program in Bangladesh

Journal of Islamic Monetary Economics and Finance, Vol. 5, No.4 (2019), pp. 829-848 p-ISSN: 2460-6146, e-ISSN: 2460-6618 QARD-AL-HASSAN AS A TOOL FOR POVERTY ALLEVIATION: A CASE STUDY OF THE FAEL KHAIR WAQF PROGRAM IN BANGLADESH Farah Muneer1 and Foyasal Khan2 1 Institute for Inclusive Finance and Development (InM), Bangladesh, [email protected] 2 Department of Economics, International Islamic University Malaysia (IIUM), Malaysia, [email protected] ABSTRACT The central focus of the Islamic economic system is on socioeconomic justice and the overall welfare of society, especially at the bottom of the pyramid segment. Qard-al- Hassan, alongside zakat and sadaqah, is one of the instruments for the redistribution of income and wealth from the rich to the poor in Islam. In 2007, Bangladesh was struck by super cyclone SIDR, leaving 3,406 people dead. Moreover, SIDR caused unprecedented damage to homes, crops and livelihoods. The Fael Khair Waqf (FKW) Program came as a response to the urgent need to assist the victims of the cyclone and initiated an interest-free micro-loan (Qard-al-Hassan) scheme to restore the livelihoods of a large segment of the victims and to lift them out of poverty. While investigating the effectiveness of Qard-al-Hassan in poverty reduction, this paper also examines the FKW program as a case study. Analysis was conducted of 1600 households using an independent sample t-test and logistic regression to investigate to what extent the program has been effective in reducing poverty. The findings of the logistic analysis are that the probability of being poor for FKW participants is around 1.46 times lower than for non-participants. -

Marriage Treasure Ownership in Arabic and Nusantara Fiqh Perspectives

ADDIN, Volume 12, Number 2, Agustus 2018 MARRIAGE TREASURE OWNERSHIP IN ARABIC AND NUSANTARA FIQH PERSPECTIVES Nur Khoirin YD UIN Walisongo Semarang, Central Java, Indonesia Abstract One of the problems that often arise after the divorce is the ownership of assets acquired during marriage, whether it belongs to the husband, wife, or both of them. According to the Compilation of Islamic Law or the fiqh of the results of ijtihad fuqaha Nusantara, the assets obtained in marriage, except those obtained through inheritance or grants from parents/family, are joint property of husband and wife (gono gini). One party may not use it except getting agreement from the other parties. And if marriage breaks, either because of divorce or death, then it must be divided into two. In the books of Arabic Fiqh, there is no joint property because marriage does not cause a mixture of wealth. 1onetheless, in the EooNs of fiTh provides the possession of wife>s assets, such as dowry, livelihood, mut>ah, iwadl and tirkah. If the provision of fiqh is carried out consistently, then when a divorce occurs, the husband must leave the house, because all the property has become the property of his wife through a way of life. But this is certainly not fair. Therefore the determination of the existence of joint property in marriage is a moderate opinion and a benefit. Keywords: 2wnership, 3roperty, 0arriage, AraEic FiTh, 1usantara FiTh. 555 Nur Khoirin YD A. Introduction The status of marital property ownership is an issue that still needs more in-depth study. There is confusion between the Arabic Fiqh1 and Nusantara Fiqh 2 about it. -

JIHAD Pag 1-10 Revazut.Qxd

JIHADUL ISLAMIC DE LA "|NFRÂNGEREA TERORII" {I "R+ZBOIUL SFÂNT" LA "SPERAN}A LIBERT+}II" JIHADUL ISLAMIC 1 Foto coperta I • SHEIKH MAWLANA MUHAMMAD HISHAM COD CNCSIS 270 ANDREESCU, ANGHEL Jihadul Islamic de la ''|nfrângerea terorii'' [i ''R=zboiul Sfânt''ANDREESCU, la ''speran]a ANGHEL libert=]ii'' / Anghel Andreescu, NicolaeJihadul Radu. Islamic - Bucure[ti: de la ''|nfrângerea Editura Ministerului terorii'' [i ''R=zboiulInternelor [iSfânt'' Reformei la Administrative,''speran]a libert=]ii'' 2008 / Anghel Andreescu, Bibliogr.Nicolae Radu. - Bucure[ti: Editura Ministerului Internelor ISBN[i Reformei 978-973-745-011-1 Administrative, 2008 Bibliogr. I.ISBN Radu, 978-973-745-011-1 Nicolae 329.7(¡411.21)I. Radu, Nicolae Jihad 329.7(¡411.21) Jihad Opera]ii editoriale: colectiv Editura MIRA Tip=rit: Tipografia Codex Anghel ANDREESCU, Nicolae RADU 2 Chestor general de poli]ie Comisar [ef prof. univ. dr. Anghel ANDREESCU conf. univ. dr. Nicolae RADU JIHADULJIHADUL ISLAMICISLAMIC DE LA "|NFRÂNGEREA TERORII" {I "R+ZBOIUL SFÂNT" LA "SPERAN}A LIBERT+}II" BUCURE{TI – 2008 – JIHADUL ISLAMIC 3 Cuprins Gând pentru toleran]= . 9 Prefa]= . 11 Introducere . 15 Introduction . 29 Introduction . 43 Lista abrevieri . 59 Capitolul 1 De la Islam la cunoa[terea Jihadului . 65 Cât de bine cunoa[tem Islamul? . 65 Unicitatea lui Allah . 79 |n numele credin]ei . 96 Calea spre Mecca . 98 Ebraismul confirmat . 103 Moartea Profetului . .104 Urma[ii lui Mahomed . 106 Dinastia Abbasida [i civiliza]ia islamic= . 109 |n=l]are [i dec=dere . 110 {ii]i [i suni]i . 111 Religia \ntre [ii]i [i suni]i . 113 Cartea Sfânt= a Islamului . 115 Nemurirea sufletului . -

Buffy & Angel Watching Order

Start with: End with: BtVS 11 Welcome to the Hellmouth Angel 41 Deep Down BtVS 11 The Harvest Angel 41 Ground State BtVS 11 Witch Angel 41 The House Always Wins BtVS 11 Teacher's Pet Angel 41 Slouching Toward Bethlehem BtVS 12 Never Kill a Boy on the First Date Angel 42 Supersymmetry BtVS 12 The Pack Angel 42 Spin the Bottle BtVS 12 Angel Angel 42 Apocalypse, Nowish BtVS 12 I, Robot... You, Jane Angel 42 Habeas Corpses BtVS 13 The Puppet Show Angel 43 Long Day's Journey BtVS 13 Nightmares Angel 43 Awakening BtVS 13 Out of Mind, Out of Sight Angel 43 Soulless BtVS 13 Prophecy Girl Angel 44 Calvary Angel 44 Salvage BtVS 21 When She Was Bad Angel 44 Release BtVS 21 Some Assembly Required Angel 44 Orpheus BtVS 21 School Hard Angel 45 Players BtVS 21 Inca Mummy Girl Angel 45 Inside Out BtVS 22 Reptile Boy Angel 45 Shiny Happy People BtVS 22 Halloween Angel 45 The Magic Bullet BtVS 22 Lie to Me Angel 46 Sacrifice BtVS 22 The Dark Age Angel 46 Peace Out BtVS 23 What's My Line, Part One Angel 46 Home BtVS 23 What's My Line, Part Two BtVS 23 Ted BtVS 71 Lessons BtVS 23 Bad Eggs BtVS 71 Beneath You BtVS 24 Surprise BtVS 71 Same Time, Same Place BtVS 24 Innocence BtVS 71 Help BtVS 24 Phases BtVS 72 Selfless BtVS 24 Bewitched, Bothered and Bewildered BtVS 72 Him BtVS 25 Passion BtVS 72 Conversations with Dead People BtVS 25 Killed by Death BtVS 72 Sleeper BtVS 25 I Only Have Eyes for You BtVS 73 Never Leave Me BtVS 25 Go Fish BtVS 73 Bring on the Night BtVS 26 Becoming, Part One BtVS 73 Showtime BtVS 26 Becoming, Part Two BtVS 74 Potential BtVS 74 -

The Jihadist Threat in France CLARA BEYLER

The Jihadist Threat in France CLARA BEYLER INCE THE MADRID AND LONDON BOMBINGS, Europeans elsewhere— fearful that they may become the next targets of Islamist terrorism— are finally beginning to face the consequences of the long, unchecked Sgrowth of radical Islam on their continent. The July bombings in London, while having the distinction of being the first suicide attacks in Western Eu- rope, were not the first time terrorists targeted a major European subway system. Ten years ago, a group linked to the Algerian Armed Islamic Group (Groupe Islamique Armé—GIA) unleashed a series of bombings on the Paris metro system. Since 1996, however, France has successfully avoided any ma- jor attack on its soil by an extremist Muslim group. This is due not to any lack of terrorist attempts—(only last September, France arrested nine members of a radical Islamist cell planning to attack the metro system)—but rather to the efficiency of the French counterterrorist services.1 France is now home to between five to six million Muslims—the sec- ond largest religious group in France, and the largest Muslim population in any Western European country.2 The majority of this very diverse population practices and believes in an apolitical, nonviolent Islam.3 A minority of them, however, are extremists. Islamist groups are actively operating in France to- day, spreading radical ideology and recruiting for future terrorist attacks on French soil and abroad. The purpose of this paper is to provide an overview of France’s Islamist groups, the evolving threats they have posed and continue to pose to French society, and the response of the French authorities to these threats. -

Holy Land Foundation for Relief and Development: Criminalizing Support for Non-Designated Charities

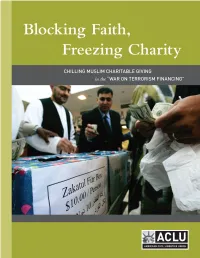

Blocking Faith, Freezing Charity CHILLING MUSLIM CHARITABLE GIVING in the “WAR ON TERRORISM FINANCING” Blocking Faith, Freezing Charity: Chilling Muslim Charitable Giving in the “War on Terrorism Financing” PUBLISHED: June 2009 FRONT COVER PHOTOGRAPH: Alex Wong/Getty Images Members of a Muslim congregation in Virginia give Zakat donations for the needy before they enter a mosque for a service to mark the conclusion of the holy month of Ramadan, the height of annual Muslim charitable giving. Zakat is one of the core “five pillars” of Islam and a religious obligation for all observant Muslims. BACK COVER PHOTOGRAPHS: LEFT: Brandon Dill/Memphis Commercial Appeal RIGHT: LIFE for Relief and Development THE AMERICAN CIVIL LIBERTIES UNION is the nation’s premier guardian of liberty, working daily in courts, legislatures and communities to defend and preserve the individual rights and freedoms guaranteed by the Constitution, the laws and treaties of the United States. OFFICERS AND DIRECTORS Susan N. Herman, President Anthony D. Romero, Executive Director Richard Zacks, Treasurer ACLU NATIONAL OFFICE 125 Broad Street, 18th Fl. New York, NY 10004-2400 (212) 549-2500 www.aclu.org Contents I. EXECUTIVE SUMMARY AND INTRODUCTION ................................................................................ 7 a. Introduction .............................................................................................................................7 b. Executive Summary .................................................................................................................9