Mergers &Acquisitions in China in the 21 Century

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SUNAC CHINA HOLDINGS LIMITED 融創中國控股有限公司 (Incorporated in the Cayman Islands with Limited Liability) (Stock Code: 01918)

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt about any aspect of this circular or as to the action to be taken, you should consult your licensed securities dealer or registered institution in securities, bank manager, solicitor, professional accountant or other professional advisers. If you have sold or transferred all your shares in Sunac China Holdings Limited, you should at once hand this circular together with the enclosed form of proxy to the purchaser(s) or transferee(s) or to the bank, licensed securities dealer or registered institution in securities or other agent through whom the sale or transfer was effected for transmission to the purchaser(s) or transferee(s). Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this circular, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. This circular appears for information purposes only and does not constitute an invitation or offer to acquire, purchase or subscribe for any securities. SUNAC CHINA HOLDINGS LIMITED 融創中國控股有限公司 (incorporated in the Cayman Islands with limited liability) (Stock Code: 01918) (1) CONNECTED TRANSACTION — PROPOSED SHARE ISSUANCE UNDER SPECIFIC MANDATE AND (2) APPLICATION FOR WHITEWASH WAIVER Independent Financial Adviser to the Independent Board Committee and the Independent Shareholders Capitalised terms used on this cover shall have the same meanings as those defined in the section headed “Definition” in this circular, unless the context requires otherwise. -

* This Document Is Important and Requires Your

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in doubt as to any aspect of this document, you should consult your licensed securities dealer, bank manager, Sch I front page solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in Henderson China Holdings Limited, you should at once hand this document and the accompanying forms of proxy to the purchaser or transferee or to the bank, licensed securities dealer or other agent through whom the sale or transfer was effected for transmission to the purchaser or transferee. The Stock Exchange of Hong Kong Limited takes no responsibility for the contents of this document, makes no representation as to its accuracy or completeness and expressly disclaims any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this document. * (Stock Code: 0246) PROPOSED PRIVATISATION BY BY WAY OF A SCHEME OF ARRANGEMENT (UNDER SECTION 99 OF THE COMPANIES ACT 1981 OF BERMUDA) INVOLVING THE CANCELLATION OF ALL THE ISSUED SHARES OF HK$1.00 EACH IN HENDERSON CHINA HOLDINGS LIMITED HELD BY THE SCHEME SHAREHOLDERS (AS DEFINED HEREIN) Financial Adviser to Henderson Land Development Company Limited Sch I Para 1 Independent financial adviser to the Independent Board Committee (as defined herein) of Henderson China Holdings Limited A letter from the board of directors of Henderson China Holdings Limited is set out on pages 8 to 17 of this document. An explanatory statement regarding the Proposal (as defined herein) is set out on pages 46 to 63 of this document. -

Three Red Lines” Policy

Real Estate Developers with High Leverage to See Inventory Quality Tested Under Broader “Three Red Lines” Policy October 28, 2020 In our view, the widening of regulations aimed at controlling real estate developers’ interest- ANALYSTS bearing debt would further reduce the industry’s overall credit risk in the long term. However, the nearer term may see less headroom for highly leveraged developers to finance in the capital Xiaoliang Liu, CFA market, pushing them to sell off inventory to ease liquidity pressure. Beijing +86-10-6516-6040 The People’s Bank of China said in September that measures aimed at monitoring the funding [email protected] and financial management of key real estate developers will steadily be expanded. Media reports suggest that the new regulations would see a cap of 15% on annual growth of interest-bearing Jin Wang debt for all property developers. Developers will be assessed against three indicators, which are Beijing called “red lines”: whether asset liability ratios (excluding advance) exceeded 70%; whether net +86-10-6516-6034 gearing ratio exceeded 100%; whether cash to short-term debt ratios went below 1.0. Developers [email protected] which breached all three red lines won’t be allowed to increase their debt. If only one or two of the red lines are breached, such developers would have their interest-bearing debt growth capped at 5% and 10% respectively. The first half of the year saw debt grow rapidly among developers. In a sample of 87 real estate developers that we are monitoring, more than 40% saw their interest-bearing debt grow at a faster rate than 15% year over year as of the end of June (see the chart below). -

ANNUAL REPORT ADDITIONAL INFORMATION All Figures in This Document Are Expressed in Canadian Dollars, Unless Otherwise Indicated

2009 ANNUAL REPORT ADDITIONAL INFORMATION All figures in this document are expressed in Canadian dollars, unless otherwise indicated. This publication, as well as the 2009 Annual Report, are available at www.lacaisse.com. Information: 514 842-3261 [email protected] Ce document, de même que le Rapport annuel 2009, sont disponibles en français sur www.lacaisse.com. Legal Deposit – Bibliothèque et Archives nationales du Québec, 2010 50% Annual Report 2009 – Additional Information I. Tables of returns 1. Auditors’ Report ................................................................................................. 1 2. General Notes .................................................................................................... 2 3. Short Term Investments ....................................................................................... 4 4. Real Return Bonds ............................................................................................... 6 5. Long Term Bonds ................................................................................................. 8 6. Bonds .............................................................................................................. 10 7. Bonds - Fixed Income .......................................................................................... 12 8. Canadian Equity ................................................................................................ 14 9. Publicly Traded Canadian Equity Markets ............................................................. -

Pacer Emerging Markets Cash Cows 100 ETF Schedule of Investments July 31, 2020 (Unaudited) Shares Value

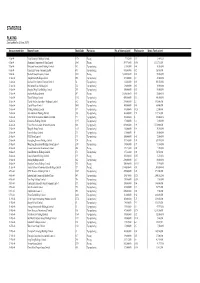

Page 1 of 5 Pacer Emerging Markets Cash Cows 100 ETF Schedule of Investments July 31, 2020 (Unaudited) Shares Value COMMON STOCKS - 91.4% Bermuda - 0.9% Nine Dragons Paper Holdings Ltd. 8,922 $ 9,336 Brazil - 11.1% Ambev SA - ADR 7,396 19,821 BRF SA - ADR (a) 2,000 7,960 CCR SA 2,652 7,651 Cosan SA 386 6,660 CPFL Energia SA 1,795 10,787 Engie Brasil Energia SA 740 6,527 JBS SA 4,938 20,513 Petrobras Distribuidora SA 1,561 6,823 TIM Participacoes SA - ADR 510 7,619 Vale SA - ADR 1,878 21,860 116,221 Cayman Islands - 3.4% SINA Corp./China (a) 222 8,958 Tongcheng-Elong Holdings Ltd. (a) 1,612 2,957 Xiaomi Corp. - Class B (a)(b) 12,393 23,698 35,613 Chile - 0.7% Cencosud SA 4,410 7,683 China - 12.8% Air China Ltd. - Class H 29,824 18,509 Anhui Conch Cement Co. Ltd. - Class H 2,910 21,984 Beijing Capital International Airport Co Ltd. - Class H 5,986 3,947 China Communications Services Corp Ltd. - Class H 8,207 5,316 China Eastern Airlines Corp. Ltd. - Class H 52,387 18,588 China Shenhua Energy Co Ltd. - Class H 12,317 20,533 China Telecom Corp. Ltd. - Class H 65,857 19,629 Great Wall Motor Co. Ltd. - Class H 20,076 19,609 Sinopec Shanghai Petrochemical Co. Ltd. 26,213 5,851 133,966 Colombia - 1.8% Ecopetrol SA - ADR 1,602 18,647 Greece - 0.9% Hellenic Telecommunications Organization SA 483 7,112 OPAP SA 283 2,544 9,656 Hong Kong - 8.5% China Medical System Holdings Ltd. -

Baker Institute Policy Report Published by the James A

ISSN 1941-6466 BAKER INSTITUTE POLICY REPORT PUBLISHED BY THE JAMES A. BAKER III INSTITUTE FOR PUBLIC POLICY OF RICE UNIVERSITY NUMBER 57 JANUARY 2014 BUILDING A TRANSPARENT WEB: TRANSNATIONAL SOCIAL MEDIA, CYBERSECURITY, AND SINO –U.S. TRADE Overview practices. In 2007, when the United States leveraged its initial WTO complaint against China, the Social media sites, while currently treated as an terms of the debate were substantially different “audiovisual product”1 by the Chinese government than they are now. Seven years ago, audiovisual under the World Trade Organization’s (WTO) materials were much more easily decoupled from trade policy, have outgrown this construct and their digital distribution sites.5 However, in the instead have become the “ports”2 of the twenty- current environment, delivery portals are so first century. Taking into consideration the global deeply entwined with the dispersal of content trade significance of social media as a locus of that it has become nearly impossible to make international trade in advertising, information, cogent international policy based on distinctions and increasingly other types of commercial goods, between digital “audiovisual products” and it is essential that the United States continues to digital distribution sites.6,7 Indeed, because these pursue WTO action to encourage China to open sites have become so central to the experience trade in social media infrastructure. This, in turn, of media consumption, as well as a host of other would ensure long-term global competitiveness in activities ranging from commerce to social life, it the information communication and technology is essential to take into account these complexities sector. -

For Personal Use Only Use Personal For

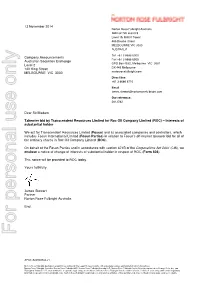

13 November 2014 Norton Rose Fulbright Australia ABN 32 720 868 049 Level 15, RACV Tower 485 Bourke Street MELBOURNE VIC 3000 AUSTRALIA Tel +61 3 8686 6000 Company Announcements Fax +61 3 8686 6505 Australian Securities Exchange GPO Box 4592, Melbourne VIC 3001 Level 2 120 King Street DX 445 Melbourne MELBOURNE VIC 3000 nortonrosefulbright.com Direct line +61 3 8686 6710 Email [email protected] Our reference: 2813782 Dear Sir/Madam Takeover bid by Transcendent Resources Limited for Roc Oil Company Limited (ROC) – interests of substantial holder We act for Transcendent Resources Limited ( Fosun ) and its associated companies and controllers, which includes Fosun International Limited ( Fosun Parties ) in relation to Fosun’s off-market takeover bid for all of the ordinary shares in Roc Oil Company Limited ( ROC ). On behalf of the Fosun Parties and in accordance with section 671B of the Corporations Act 2001 (Cth), we enclose a notice of change of interests of substantial holder in respect of ROC ( Form 604 ). This notice will be provided to ROC today. Yours faithfully James Stewart Partner Norton Rose Fulbright Australia Encl. For personal use only APAC-#24924633-v1 Norton Rose Fulbright Australia is a law firm as defined in the Legal Profession Acts of the Australian states and territory in which it practises. Norton Rose Fulbright Australia, Norton Rose Fulbright LLP, Norton Rose Fulbright Canada LLP, Norton Rose Fulbright South Africa (incorporated as Deneys Reitz Inc) and Fulbright & Jaworski LLP, each of which is a separate legal entity, are members of Norton Rose Fulbright Verein, a Swiss Verein. -

China Reits Property Landlords to Shine 19

SECTOR BRIEFING number DBS Asian Insights DBS Group59 Research • May 2018 China REITs Property Landlords to Shine 19 DBS Asian Insights SECTOR BRIEFING 59 02 China REITs Property Landlords to Shine Ken HE Equity Analyst DBS (Hong Kong) [email protected] Carol WU Head of Greater China Research DBS (Hong Kong) [email protected] Danielle WANG CFA Equity Analyst DBS (Hong Kong) [email protected] Derek TAN Equity Analyst DBS Group Research [email protected] Jason LAM Equity Analyst DBS (Hong Kong) [email protected] Produced by: Asian Insights Office • DBS Group Research go.dbs.com/research @dbsinsights [email protected] Goh Chien Yen Editor-in-Chief Jean Chua Managing Editor Martin Tacchi Art Director 19 DBS Asian Insights SECTOR BRIEFING 59 03 04 Executive Summary 08 China REITs Are Lagging Edging Towards Onshore REITs Major Obstacles in Fostering 18 an Onshore REIT Regime CMBS/CMBNs Are Growing Faster C-REITs Are Imminent Which Asset Type Will Benefit 28 More? Modern Logistics Properties The Rise of Active Property Asset Management Which Developer Will Benefit From the Establishment of C-REITs? 49 Appendix DBS Asian Insights SECTOR BRIEFING 59 04 Executive Summary No REIT regime yet he real estate investment trust (REIT) has become an important investment vehicle as evidenced by its separation from the financial sector in the Global Industry Classification Standard as a sector on its own. Major Asian countries/regions have joined western countries to kickstart local versions of REITs, leaving China the last Tbig economy that has yet to have such an investment vehicle. Two major technical In our view, removing legislative obstacles (publicly traded funds are not allowed to obstacles hold commercial properties) is the first step that the government needs to take towards establishing a modern REIT regime. -

PLACING (Last Updated on 22 June 2007)

STATISTICS PLACING (Last updated on 22 June 2007) Announcement date Name of issuer Stock Code Particulars No. of shares placed Placing price Gross Funds raised (HK$) 5-Jan-04 Vitop Bioenergy Holdings Limited 1178 Placing 7,752,000 0.31 2,403,120 6-Jan-04 Aluminum Corporation of China Limited 2600 Placing 549,976,000 5.658 3,111,764,208 7-Jan-04 Perfectech International Holdings Limited 765 Top-up placing 21,000,000 0.68 14,280,000 8-Jan-04 China Eagle Group Company Limited 493 Top-up placing 473,000,000 0.12 56,760,000 9-Jan-04 Medtech Group Company Limited 1031 Placing 5,000,000,000 0.01 50,000,000 12-Jan-04 Tongda Group Holdings Limited 698 Top-up placing 227,500,000 0.2 45,500,000 13-Jan-04 Kowloon Development Company Limited 34 Top-up placing 83,000,000 6.85 568,550,000 13-Jan-04 Millennium Sense Holdings Ltd 724 Top-up placing 30,000,000 0.63 18,900,000 13-Jan-04 Shanghai Ming Yuan Holdings Limited 233 Top-up placing 100,000,000 0.55 55,000,000 13-Jan-04 Starbow Holdings Limited 397 Placing 2,000,000,000 0.01 20,000,000 13-Jan-04 Titan (Holdings) Limited 1192 Top-up placing 450,000,000 0.92 414,000,000 15-Jan-04 Chaoda Modern Agriculture (Holdings) Limited 682 Top-up placing 280,000,000 2.5 683,000,000 15-Jan-04 Capital Prosper Limited 1003 Top-up placing 140,000,000 0.05 68,000,000 15-Jan-04 Paliburg Holdings Limited 617 Top-up placing 180,000,000 0.128 22,500,000 15-Jan-04 Asia Aluminum Holdings Limited 930 Top-up placing 332,000,000 1.56 517,920,000 15-Jan-04 Silver Grant International Industries Limited 171 Top-up placing 165,000,000 -

Dozens of Outspoken, Popular Blogs Shut in China 15 July 2010, by CARA ANNA , Associated Press Writer

Dozens of outspoken, popular blogs shut in China 15 July 2010, By CARA ANNA , Associated Press Writer microblog was closed. Both men are well-known for taking on sensitive issues. Chinese officials fear that public opinion might spiral out of control as social networking - and social unrest - boom among its 420 million Internet users. China maintains the world's most extensive Internet monitoring and filtering system, and it unplugged Twitter and Facebook last year. Blogger Yao Yuan listed at least 61 closed Sohu blogs, including his own, on a separate, unblocked In this photo taken Wednesday, July 14, 2010, a blog Thursday. He called the closings mass Chinese man uses a computer at an Internet cafe in murder. Beijing, China. China's Twitter-like microblogs are facing new threats of censorship. The country's top microblogs "If Internet users don't speak out, all sites will be either are down for maintenance or now display a "beta" cracked down on in the future," said Yao, who owns tag to indicate they are in a testing phase, though they have been operating for months. (AP Photo/Ng Han an Internet-promotion company in Shanghai. Guan) "Ordinary people will forever lose their freedom to speak online, and the government can rest without worrying anymore." (AP) -- Dozens of blogs by some of China's most Microblogs can quickly aggregate critical voices, outspoken users have been abruptly shut down which is why authorities have been increasing while popular Twitter-like services appear to be the controls, said Xiao Qiang, director of the China newest target in government efforts to control Internet Project at the University of California- social networking. -

Social Media Contracts in the US and China

DESTINED TO COLLIDE? SOCIAL MEDIA CONTRACTS IN THE U.S. AND CHINA* MICHAEL L. RUSTAD** WENZHUO LIU*** THOMAS H. KOENIG**** * We greatly appreciate the editorial and research aid of Suffolk University Law School research assistants: Melissa Y. Chen, Jeremy Kennelly, Christina Kim, Nicole A. Maruzzi, and Elmira Cancan Zenger. We would also like to thank the editors at the University of Pennsylvania Journal of International Law. ** Michael Rustad is the Thomas F. Lambert Jr. Professor of Law, which was the first endowed chair at Suffolk University Law School. He is the Co-Director of Suffolk’s Intellectual Property Law Concentration and was the 2011 chair of the American Association of Law Schools Torts & Compensation Systems Section. Pro- fessor Rustad has more than 1100 citations on Westlaw. His most recent books are SOFTWARE LICENSING: PRINCIPLES AND PRACTICAL STRATEGIES (Lexis/Nexis, 3rd ed. forthcoming 2016), GLOBAL INTERNET LAW IN A NUTSHELL (3rd ed., West Academic Publishers, 2015), and GLOBAL INTERNET LAW (HORNBOOK SERIES) (West Academic Publishers, 2d ed. 2015). Professor Rustad is editor of COMPUTER CONTRACTS (2015 release), a five volume treatise published by Matthew Bender. *** Wenzhuo Liu, LL.B., LL.M, J.D., obtained China’s Legal Professional Qual- ification Certificate in 2011. In 2014, she became a member of the New York state bar. She earned an LL.M degree from the University of Wisconsin Law School in Madison, Wisconsin in 2012 and a J.D. degree from Suffolk University Law School in Boston. She was associated with Hunan Haichuan Law Firm in Changsha, China. Ms. Liu wrote a practice pointer on Software Licensing and Doing Business in China in the second and third editions of MICHAEL L. -

Real Estate and Construction-210204-EN

Real Estate and Construction Beijing Guangzhou Hong Kong Shanghai Shenzhen 27/F, North Tower 17/F, International Finance 26/F, One Exchange Square 24/F, HKRI Centre Two, 17/F, Tower One, Kerry Plaza Beijing Kerry Centre Place, 8 Huaxia Road, 8 Connaught Place, Central HKRI Taikoo Hui 1 Zhong Xin Si Road 1 Guanghua Road Zhujiang New Town Hong Kong 288 Shi Men Yi Road Futian District Chaoyang District Guangzhou 510623, China Shanghai 200041, China Shenzhen 518048, China Beijing 100020, China Tel: +86 10 5769 5600 Tel: +86 20 3225 3888 Tel: +852 3976 8888 Tel: +86 21 2208 1166 Tel: +86 755 8159 3999 Fax:+86 10 5769 5788 Fax:+86 20 3225 3899 Fax:+852 2110 4285 Fax:+86 21 5298 5599 Fax:+86 755 8159 3900 www.fangdalaw.com Real Estate and Construction 01 Real Estate and Construction Practice Fangda’s Real Estate and Construction Practice Team excels at providing one-stop and full-scale services to leading real estate market players, including real estate developers, real estate private equity sponsors, institutional investors, financial institutions and other corporations and individuals in complicated domestic and cross-border real estate transactions. Our lawyers are frequently appointed as arbitrators in real estate and construction-related disputes. Our strength in this area includes a combination of understanding the traditions of the Chinese market and practice and our abundant experience in serving international clients, complemented by services for non-contentious and contentious cases. We are one of the few firms based in China that can provide integrated real estate and construction related legal services, and present practical advice based on our knowledge and experience in the local market.