Insight India an Overview of Trends in Select Sectors and Markets August 2010

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Separate Financial Statements Fiscal Year 2019

201Separate financial9 statements PPorscheorsche TaycanTaycan TurboTurbo S 3 Content Group management report and management report of Porsche Automobil Holding SE 6 Fundamental information about the group 10 Report on economic position 12 Significant events and developments at the Porsche SE Group 12 Significant events and developments at the Volkswagen Group 20 Business development 24 Results of operations, financial position and net assets 31 Porsche Automobil Holding SE (financial statements pursuant to the German Commercial Code) 37 Sustainable value enhancement in the Porsche SE Group 41 Overall statement on the economic situation of Porsche SE and the Porsche SE Group 43 Remuneration report 44 Opportunities and risks of future development 52 Publication of the declaration of compliance and corporate governance report 78 Subsequent events 79 Forecast report and outlook 80 Glossary 85 4 Financials 86 Balance sheet of Porsche Automobil Holding SE 90 Income statement of Porsche Automobil Holding SE 91 Notes to the consolidated fi nancial statements 92 Independent auditor’s report 212 Responsibility statement 220 5 VVolkswagenolkswagen IID.3D.3 6 1 Group management report and management report of Porsche Automobil Holding SE 7 8 Group management report and management report of Porsche Automobil Holding SE 6 Fundamental information about the group 10 Report on economic position 12 Significant events and developments at the Porsche SE Group 12 Significant events and developments at the Volkswagen Group 20 Business development 24 Results -

Blood Tests • Diagnostics • Wellness

Ref: MHL/Sec&Legal/2020-21/138 Date: October 1, 2020 To, Head, Listing Compliance Department Head Listing Compliance Department BSE Limited National Stock Exchange of India Limited Phiroze Jeejeebhoy Towers Dalal Street, Exchange Plaza, Plot No. C/1. G Block, Mumbai - 400 001. Bandra -Kurla Complex, Bandra (East), Mumbai- 400051 Scrip Code: 542650 Scrip Symbol: METROPOLIS Sub: Intimation of Credit Rating. Dear Sir/Madam, Pursuant to Regulation 30 of the SEBI (Listing Obligations and Disclosure Requirements), Regulations, 2015, we wish to inform you that CRISIL, a Credit Rating Agency has reaffirmed its ‘CRISIL AA-/Stable’ rating on the Non-Convertible Debentures and the long-term loan facility of the Company and has also reassigned its ‘CRISIL A1+’ rating to the short-term bank facility of the Company. Further, please note that the Company has neither issued the Non-Convertible Debentures nor availed the long-term or short-term bank facility as aforesaid till date. The rating rationale dated September 30, 2020 received from CRISIL on October 1, 2020 and accepted by the Company is enclosed herewith for your kind reference. The above is for your information and records. Yours Faithfully For Metropolis Healthcare Limited Poonam Tanwani Company Secretary & Compliance Officer Membership No. A19182 Encl. a/a BLOOD TESTS • DIAGNOSTICS • WELLNESS Metropolis Healthcare Limited Registered & Corporate Office: 250 D, Udyog Bhavan, Hind Cycle Marg, Worli, Mumbai - 400 030. CIN: L73100MH2000PLC192798 Tel No.: 8422 801 801 Email: [email protected] -

Bricks and Mortar

MORE THAN BRICKS AND MORTAR Infrastructure-as-asset-class: Financing development or developing finance? A Critical Look at Private Equity Infrastructure Funds1 by Nicholas Hildyard The Corner House2 1 Sources for further information, including hyperlinks, have been given throughout this report where possible. Website addresses were correct at the time of writing. Please notify The Corner House of any broken link: enquiries AT thecornerhouse.org.uk 2 The author would like to thank Isabella Besedova, Theodoros Chronopoulos, Peter Frankental, Jutta Kill, Tom Lines, Larry Lohmann, Doug Norlen, Sarah Sexton, Antonio Tricarico and Beck Wallace for their invaluable comments on early drafts of this paper. 1 “When the capital development of a country becomes the by-product of the activities of a casino, the job is likely to be ill-done.” John Maynard Keynes, General Theory of Employment, Interest and Money, 1936 “The last quarter century of ‘deregulation’ involved the introduction of a vast array of new legal mechanisms and regulations by national governments to protect the interests of investors and shareholders. This must be dismantled; and new legal mechanisms and regulations must be introduced nationally to subordinate investment capital to democratic requirements established in international human rights standards.” Peter Rossman and Gerard Greenfield, Financialization: New Routes to Profit, New Challenges for Trade Unions, 20061 Introduction Political discourse is often conducted in code. Where policy proposals or actions are likely to engender strong opposition or cause affront to the public, euphemisms are used (“collateral damage” for “dead civilians”, “land disturbance” for “mining”, “environmental enhancement” for “canalising rivers”)2 or concepts are employed that direct the conversation elsewhere. -

Infrastructure Development Finance Company Limited

PROSPECTUS – TRANCHE 2 Dated January 4, 2011 INFRASTRUCTURE DEVELOPMENT FINANCE COMPANY LIMITED (Infrastructure Development Finance Company Limited (the “Company”), with CIN L65191TN1997PLC037415, incorporated in the Republic of India with limited liability under the Companies Act, 1956, as amended (the “Companies Act”)) Registered Office: KRM Tower, 8th Floor, No.1 Harrington Road, Chetpet, Chennai 600 031 Tel: (91 44) 4564 4000; Fax: (91 44) 2854 7597 Corporate Office: Naman Chambers, C-32, G-Block, Bandra-Kurla Complex Bandra (East), Mumbai 400 051 Tel: (91 22) 4222 2000; Fax: (91 22) 2654 0354 Compliance Officer and Contact Person: Mahendra N. Shah, Company Secretary E-mail: [email protected]; Website: www.idfc.com PUBLIC ISSUE BY INFRASTRUCTURE DEVELOPMENT FINANCE COMPANY LIMITED (“COMPANY” OR “ISSUER”) OF LONG TERM INFRASTRUCTURE BONDS OF FACE VALUE OF RS. 5,000 EACH, IN THE NATURE OF SECURED, REDEEMABLE, NON-CONVERTIBLE DEBENTURES, HAVING BENEFITS UNDER SECTION 80 CCF OF THE INCOME TAX ACT, 1961 (THE “BONDS”), NOT EXCEEDING RS. 34,000 MILLION FOR THE FINANCIAL YEAR 2010 - 2011. THE BONDS WILL BE ISSUED IN ONE OR MORE TRANCHES SUBJECT TO THE OVERALL LIMIT OF RS. 34,000 MILLION FOR THE FINANCIAL YEAR 2010- 2011 UNDER THE SHELF PROSPECTUS FILED WITH THE STOCK EXCHANGES AND SEBI ON SEPTEMBER 23, 2010. THE SECOND TRANCHE OF THE BONDS FOR AN AMOUNT NOT EXCEEDING RS. 29,289.64 MILLION (THE “ISSUE”) SHALL BE ISSUED ON THE TERMS SET OUT IN THIS PROSPECTUS TRANCHE – 2. The Issue is being made pursuant to the provisions of Securities and Exchange Board of India (Issue and Listing of Debt Securities) Regulations, 2008, as amended (the “SEBI Debt Regulations”). -

Download PDF, 19 Pages, 505.25 KB

VOLKSWAGEN AKTIENGESELLSCHAFT Shareholdings of Volkswagen AG and the Volkswagen Group in accordance with sections 285 and 313 of the HGB and presentation of the companies included in Volkswagen's consolidated financial statements in accordance with IFRS 12 as of 31.12.2019 Exchange rate VW AG 's interest Equity Profit/loss (1€ =) in capital in % in thousands, in thousands, Name and domicile of company Currency Dec. 31, 2019 Direct Indirect Total local currency local currency Footnote Year I. PARENT COMPANY VOLKSWAGEN AG, Wolfsburg II. SUBSIDIARIES A. Consolidated companies 1. Germany ASB Autohaus Berlin GmbH, Berlin EUR - 100.00 100.00 16,272 1,415 2018 AUDI AG, Ingolstadt EUR 99.64 - 99.64 13,701,699 - 1) 2019 Audi Berlin GmbH, Berlin EUR - 100.00 100.00 9,971 - 1) 2018 Audi Electronics Venture GmbH, Gaimersheim EUR - 100.00 100.00 60,968 - 1) 2019 Audi Frankfurt GmbH, Frankfurt am Main EUR - 100.00 100.00 8,477 - 1) 2018 Audi Hamburg GmbH, Hamburg EUR - 100.00 100.00 13,425 - 1) 2018 Audi Hannover GmbH, Hanover EUR - 100.00 100.00 16,621 - 1) 2018 AUDI Immobilien GmbH & Co. KG, Ingolstadt EUR - 100.00 100.00 82,470 3,399 2019 AUDI Immobilien Verwaltung GmbH, Ingolstadt EUR - 100.00 100.00 114,355 1,553 2019 Audi Leipzig GmbH, Leipzig EUR - 100.00 100.00 9,525 - 1) 2018 Audi München GmbH, Munich EUR - 100.00 100.00 270 - 1) 2018 Audi Real Estate GmbH, Ingolstadt EUR - 100.00 100.00 9,859 4,073 2019 Audi Sport GmbH, Neckarsulm EUR - 100.00 100.00 100 - 1) 2019 Audi Stuttgart GmbH, Stuttgart EUR - 100.00 100.00 6,677 - 1) 2018 Auto & Service PIA GmbH, Munich EUR - 100.00 100.00 19,895 - 1) 2018 Autonomous Intelligent Driving GmbH, Munich EUR - 100.00 100.00 250 - 1) 2018 Autostadt GmbH, Wolfsburg EUR 100.00 - 100.00 50 - 1) 2018 B. -

Intimation of Annual Report and AGM Notice 2020

Ref: MHL/Sec&Legal/2021-22/29 Date: July 18, 2021 To, Head, Listing Compliance Department Head, Listing Compliance Department BSE Limited National Stock Exchange of India Limited Phiroze Jeejeebhoy Towers Exchange Plaza, Plot No. C/1. G Block, Dalal Street, Mumbai - 400 001. Bandra -Kurla Complex, Bandra (East), Mumbai- 400051. Scrip Code: 542650 Scrip Symbol: METROPOLIS Sub: Copy of Annual Report of the Company for the Financial Year 2020-2021 along with the Notice convening the 21st Annual General Meeting Ref: Our earlier letter dated July 05, 2021 having reference no. MHL/Sec&Legal/2021-22/23 Dear Sir/Madam, With reference to the captioned subject, our earlier letter dated July 05, 2021 having reference no. MHL/Sec&Legal/2021-22/23 wherein we had informed the Exchange about the 21st Annual General Meeting (‘AGM’) of the Company. In continuation to the same and as required under Regulations 30 and 34 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, we submit herewith the Annual Report of the Company for the Financial Year 2020-2021 along with the Notice convening the 21st AGM of the Company scheduled to be held on Wednesday, August 11, 2021 at 9.30 A.M. (IST) through Video Conferencing / Other Audio Visual Means (‘VC / OAVM’) in compliance with the General Circular No. May 05, 2020 read with Circulars dated April 08,2020, April 13, 2020 and January 13, 2021 issued by the Ministry Corporate Affairs and Circular dated May 12,2020 and January 15, 2021 issued by the Securities and Exchange Board of India. -

CDC Group Plc Financial Review 2009 Our Mission Is to Foster Growth in Sustainable Businesses, Helping to Raise Living Standards in Developing Countries

CDC Group plc Financial Review 2009 Our mission is to foster growth in sustainable businesses, helping to raise living standards in developing countries. Our investment policy is to make more than 75% of new investments in low income countries* and to invest more than 50% of our funds in sub-Saharan Africa. Contents 2 Statement from the Chairman 4 Our Business 12 Statement from the Chief Executive 14 Board of Directors 16 Business Review – Africa 18 Business Review – Asia 20 Performance Review 28 CDC Universe * Those with an annual gross national income (GNI) per capita of less than US$905. CDC Group plc Financial Review 2009 1 2009 Highlights £359m New investments in developing countries, 61% in Africa £207m Total return after tax £742m1 Other capital mobilised £162m Portfolio cash generated for re-investment in developing countries £1,411m Portfolio of fund investments £207m New commitments to funds in a difficult period for fundraising £1,561m Outstanding commitments to funds 794 Underlying portfolio companies located in 71 countries CDC’s Investment Code Process externally audited for the first time 1 See page 22 for an explanation of how mobilisation is measured. 2 CDC Group plc Financial Review 2009 Statement from the Chairman Richard Gillingwater CBE In the deepest recession that we’ve 2009 also saw the first year of had in many decades in developed CDC’s new investment policy, markets, the emerging markets which the organisation has fully in which CDC invests its capital embraced. The new policy, which showed some positive growth and takes us through to the end of a steady return to financial stability 2013, targets 75% of CDC’s new in 2009. -

Best Foot Forward

July/August 2011 • Issue 52 i n fo c u s parag saxena | new silk route Best foot forward March 2011 • Issue 48 Saxena: confident in future LP support New Silk Route gained a lot of unwanted publicity earlier this year when it emerged that one of its founders was being charged by the SEC in the Galleon insider trading scandal. But co-founder Parag Saxena says the growth capital firm has worked to move forward and remind LPs private equity is a team sport. By Christopher Witkowsky f the partners at New Silk Route needed evidence that the immediate task of formulating a cohesive message for LPs. firm’s limited partners were happy with the performance of the Suddenly, their job became not just about finding the best fund, a big vote of confidence came in May when close to 100 investments, but about reassuring and shoring up a base of LPs that Ipercent of LPs met a capital call. consisted of large institutions experienced in the asset class and The firm had for months been dealing with fallout related to not in the mood to deal with scandal, especially in an uncertain co-founder Rajat Gupta, who was caught up in a wide-ranging economic environment. insider trading investigation involving hedge fund giant Galleon At a recent meeting in the firm’s New York office Saxena Group. Gupta was accused in early March by the US Securities declines to discuss Gupta’s case in any detail, but says he and other and Exchange Commission of sharing confidential information to firm principals reached out to LPs when the SEC charges were Galleon’s founder Raj Rajaratnam, which the hedge fund executive made public. -

Blood Tests • Diagnostics • Wellness

Ref: MHL/Sec&Legal/2020-21/130 Date: August 24, 2020 To, Head, Listing Compliance Department Head Listing Compliance Department BSE Limited National Stock Exchange of India Limited Phiroze Jeejeebhoy Towers Dalal Street, Exchange Plaza, Plot No. C/1. G Block, Mumbai - 400 001. Bandra -Kurla Complex, Bandra (East), Mumbai- 400051. Scrip Code: 542650 Scrip Symbol: METROPOLIS Subject: Copy of Annual Report of the Company for the Financial Year 2019-2020 along with the Notice convening the 20th Annual General Meeting Ref.: Our earlier letter dated August 19, 2020 having reference no. MHL/Sec&Legal/2020-21/128 Dear Sir/Madam, With reference to the captioned subject, our earlier letter dated August 19, 2020 having reference no. MHL/Sec&Legal/2020-21/128 wherein we had informed the Exchange about the 20th Annual General Meeting (‘AGM’) of the Company. In continuation to the same and as required under Regulations 30, 34 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, we submit herewith the Annual Report of the Company for the Financial Year 2019-2020 along with the Notice convening the 20th AGM of the Company scheduled to be held on Wednesday, September 16, 2020 at 9.00 A.M. (IST) through Video Conferencing / Other Audio Visual Means (‘VC / OAVM’) in compliance with the General Circular No. 14/ 2020 dated April 08,2020, General Circular No. 17 /2020 dated April 13, 2020, General Circular No. 20/2020 dated May 05,2020 issued by Ministry Corporate Affairs and Circular No. SEBI/HO/CFD/CMD1/CIR/P/2020/79 dated May 12,2020 issued by SEBI. -

LTG Pool.Xlsx

Long-Term Growth Pool Asset Allocation & Expenses As of July 2013 45% Equity Target Allocation Fee (%) 100% 17% US. Large Capitalization Vanguard 500 5.1% 0.05 Adage Capital 3.4% 0.50 Dodge & Cox 4.3% 0.52 U.S. Large Cap Touchstone Sands Instl Growth 2.1% 0.75 90% Capital Counsel 2.1% 0.80 4% U.S. Mid Capitalization Times Square 2.0% 0.80 U.S. Mid Cap Cooke & Bieler 2.0% 0.79 80% 4% U.S. Small Capitalization U.S. Small Cap Advisory Research 2.0% 1.00 Artisan Partners 2.0% 1.00 10% International Developed Markets International 70% Artisan Partners 3.0% 1.00 Equity Silchester 3.0% 0.98 Gryphon International 3.0% 0.90 Vanguard 1.0% 0.07 Emerging 5% Emerging Markets Markets Westwood Global 3.0% 1.25 60% Opportunistic/ Dimensional Fund Advisors 2.0% 0.62 Special Situation 5% Opportunistic/Special Situation Various managers and strategies 5.0% 1.50 U.S. Aggregate 50% 25% Fixed Income Bonds 10% U.S. Aggregate Bonds PIMCO Total Return 5.0% 0.46 Income Research & Management 5.0% 0.35 TIPS 4% Treasury Inflation Protected Securities 40% Vanguard 4.0% 0.09 U.S. High Yield 4% US High Yield Bonds Post Advisory 4.0% 0.75 Global Bonds 7% Global Bonds Colchester Global 3.5% 0.55 30% GMO 3.5% 0.43 Direct Hedge 30% Alternatives1 Funds 9% Direct Hedge Funds Various managers and strategies 9.0% 1.50 20% Fund of Hedge 6% Fund of Hedge Funds Funds Various managers and strategies 6.0% 1.00 2 5% Private Equity Private Equity Various managers and strategies 5.0% 1.75 10% 5% Private Real Assets/Real Estate Real Assets Various managers and strategies 5.0% 2.00 Real Estate 5% Commodities Wellington 5.0% 0.90 Commodities 0% Asset Weighted Total 100% 0.89 Custodian Bank 0.03 Investment Consulting and Administration 0.07 Total Investment Expenses* 0.99 1 Expenses shown do not include carried interest or the expense of individual managers within fund of funds. -

Crowdfunding As a Marketing Toll

Master’s Degree in Innovation and Marketing Final Thesis Crowdfunding as a marketing toll Supervisor Francesca Checchinato Graduand Mattia Bartoli 867875 Academic Year 2019 / 2020 1 INDEX INTRODUCTION ........................................................................................................................................... 4 CHAPTER 1: CROWDFUNDING ................................................................................................................ 6 1.1 THE BACKGROUND AT THE BASE OF THE PHENOMENON ...................................................... 6 1.2 CROWDFUNDING .............................................................................................................................. 11 1.3 CULTURAL BACKGROUND BEHIND CROWDFUNDING ........................................................... 13 1.3.1 STRONG AND WEAK TIES ................................................................................................................. 13 1.3.2 THE LONG TAIL .............................................................................................................................. 15 1.3 HISTORY AND EVOLUTION OF CRODWFUNDING .................................................................... 18 1.4 DIFFERENT CROWDFUNDING MODELS ...................................................................................... 22 1.5.1 DONATION-BASED CROWDFUNDING ............................................................................................... 23 1.5.2 REWARD-BASED CROWDFUNDING ................................................................................................. -

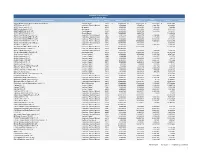

HIERS Performance Report by Investment

Statement of Investments (1) As of June 30, 2017 Total Investment Name Investment Strategy Vintage Committed Paid-In Capital (2) Valuation Net IRR Distributions Abraaj Global Growth Markets Strategic Fund, L.P. Growth Equity 2015 $ 45,000,000 $ 30,442,233 $ 6,226,973 $ 34,191,582 ABRY Partners VII, L.P. Corporate Finance/Buyout 2011 3,500,000 3,569,519 3,861,563 2,239,428 ABRY Senior Equity III, L.P. Mezzanine 2010 5,000,000 4,618,602 7,138,392 322,958 ABRY Senior Equity IV, L.P. Mezzanine 2012 6,503,582 6,227,869 1,900,948 6,205,777 ABS Capital Partners VI, L.P. Growth Equity 2009 4,000,000 3,906,193 1,775,815 1,812,911 ABS Capital Partners VII, L.P. Growth Equity 2012 10,000,000 9,054,134 - 11,860,984 Advent International GPE V-B, L.P. Corporate Finance/Buyout 2012 2,801,236 2,583,570 3,290,856 248,977 Advent International GPE V-D, L.P. Corporate Finance/Buyout 2005 3,179,324 3,038,405 7,175,404 245,538 Advent International GPE VI-A, L.P. Corporate Finance/Buyout 2008 9,500,000 9,500,000 14,172,848 5,876,065 Advent International GPE VII-B, L.P. Corporate Finance/Buyout 2012 30,000,000 27,000,000 11,400,028 32,412,380 Advent International GPE VIII-B, L.P. Corporate Finance/Buyout 2016 36,000,000 8,424,000 - 8,986,703 Alta Partners VIII, L.P.