The Assessment of Customer Response on Electronic

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Philippe EE Financing

THE EXPERIENCE OF PROPARCO IN BANGLADESH CLEAN ENERGY EFFICIENCY FINANCING ENERGY SUMMIT 2019 SUNDAY MARCH 10TH 2019 #EntreprendreEnCommun #BusinessInCommon PROPARCO SNAPSHOT PROPARCO AT A GLANCE THE FRENCH DFI SERVING THE PRIVATE SECTOR AND SUSTAINABLE DEVELOPMENT A SUBSIDIARY OF THE AGENCE FRANÇAISE DE DÉVELOPPEMENT (AFD) AFD is a public financial institution implementing French government's policies, aimed at poverty alleviation and sustainable development DEVOTED TO PRIVATE SECTOR FUNDING SINCE 1977 450+ clients, not tied to French interests ACTIVE IN DEVELOPING COUNTRIES (PER OECD DEFINITION) 80+ countries of operation, 23 local currencies in the portfolio SUPPORTING SUSTAINABLE DEVELOPMENT GOALS Devoting 30% of activity to projects with climate change co-benefits In 2018 €1.6bn 103 €5.5bn 300+ in financing new executed of outstanding loans staff members transactions and equity stakes A UNIQUE MODE OF GOVERNANCE PUBLIC AND PRIVATE SHAREHOLDER BASE FROM FRANCE AND ELSEWHERE 65% Agence Française de Développement 22% • BNP Paribas French • BPCE IOM Financial • CDC Entreprises ELAN PME (Bpifrance) Organizations • Crédit Agricole SA • Société générale • Aga Khan Fund for Economic Development (AKFED) 11% • Banque marocaine du commerce extérieur (BMCE) International • Bank of Africa Group (BoA Group SA) Financial • Banque ouest-africaine de développement (BOAD) Organizations • Corporación Andina de Fomento (CAF) • Development Bank of Southern Africa (DBSA) 2% • Bolloré Africa Logistics Corporates • ENGIE • Groupe Bouygues • Saur International -

Annual Integrated R E P O

2019 2019 ANNUAL ANNUAL INTEGRATED INTEGRATED REPORT REPORT INTRODUCING THE GROUP.....................................................................................................................................................8 BANK OF AFRICA, more than 60 years of continuous development ................................................................................9 BANK OF AFRICA Today......................................................................................................................................................................................... 11 Shareholders ........................................................................................................................................................................................................................ 13 BANK OF AFRICA Group’s business lines............................................................................................................................................... 16 Geographical presence................................................................................................................................................................................................ 17 A pan-African vocation................................................................................................................................................................................................ 18 Intra-Group synergies for Africa’s development .................................................................................................................................. -

Business in Africa

Deal Makers Vol 8: No 4 AFRICA TRANSACTION TABLE BY COUNTRY INCLUDING ADVISORS | BUSINESS IN AFRICA from the Most institutional and private equity investors (and of course the development finance institutions) are required to ensure that the target has the ability to comply with international anti-ceorruptdion, soiciatl anod environm’ens tal laws. dIn maney casess targk ets in Africa will not have the relevant systems and controls in place to monitor effectively compliance with these legal requirements, in particular anti-corruption laws. The cost of s global M&A hit record highs in 2015, dealmaking activity in sub-Saharan Africa implementing the procedures and the ability to A remained relatively muted despite an uptick in activity towards the end of the year. monitor systems and controls should be carefully In recent years, African markets have been one of the preferred destinations for funds considered. shunning lower interest rates in the US. But all that changed with the hike in interest rates by the US Federal Reserve. In addition, geopolitical uncertainties, market and currency volatility and a slump in commodity prices have seen focus shift away from emerging markets to Advertising rates are available on request from Infrastructure and developed countries. property Vanessa Aitken +27 (0)83 775 2995 Private equity firms too have become more creative as valuations remain high. Firms have development pursued other avenues to deploy capital. Some have opted for private investment in public The magazine may be purchased on transactions form equities in lieu of large leverage buyouts. subscription. These rates are available on the backbone of Years of rapid economic growth across sub-Saharan Africa have been fuelled by hopes of the request from: [email protected] developing development of a continent less dependent on the fickle global demand for its raw resources. -

Recent Trends in Banking in Sub-Saharan Africa from Financing to Investment

Recent Trends in Banking in sub-Saharan Africa From Financing to Investment Recent Trends in Banking in sub-Saharan Africa from Financing to Investment July 2015 Lead authors Tim Bending, Economist, European Investment Bank Angus Downie, Head of Economic Research, Ecobank Thierry Giordano, Economist, CIRAD Arthur Minsat, Africa Economist, OECD Bruno Losch, Research Director, CIRAD Daniela Marchettini, Economist, International Monetary Fund, Africa Department Rodolfo Maino, Senior Economist, International Monetary Fund, Africa Department Mauro Mecagni, Assistant Director, International Monetary Fund, Africa Department Oskar Nelvin, Economist, European Investment Bank Habil Olaka, Chief Executive Officer, Bankers Association, Kenya Jared Osoro, Director, Kenya Bankers Association Centre for Research on Financial Markets and Policy Henri-Bernard Solignac-Lecomte, Head of Unit, OECD Development Centre Jean-Philippe Stijns, Senior Economist, European Investment Bank Stuart Theobald, Chairman, Intellidex Economics editor Jean-Philippe Stijns, Senior Economist, European Investment Bank Debora Revoltella, Director, Economics Department, European Investment Bank Editorial, linguistic and statistical support Paul Skinner, Senior Translator-Reviser, Deputy Head of Unit, European Investment Bank Dr. Polyxeni Kanelliadou, Assistant, European Investment Bank Magali Vetter, Administrative Assistant, European Investment Bank Jurate Cepulyte-Dubois, Project Manager, European Investment Bank Rafal Banaszek, Statistical and Reporting Analyst, European Investment Bank The articles in this document were discussed at a roundtable event hosted by the EIB’s Economics Department in Luxembourg in the context of the Africa Day hosted on 9 July 2015 by the European Investment Bank in cooperation with Luxembourg’s Presidency of the European Union. About the Economics Department of the EIB The mission of the EIB Economics Department is to provide economic analyses and studies to support the Bank in its operations and in its positioning, strategy and policy. -

Annual Report 2013 Table of Contents

GHANA Annual report 2013 Table of contents 1 Message from the CEO of BOA GROUP 2-3 Over 30 years of growth and expansion 4 Over 30 years of experience serving customers 5 The commitments of the Group 6 Banking Products & Services of BOA-GHANA 7 ActivitY REport 8-9 Comments from the Managing Director 10 Highlights 2013 11 Key figures on 31/12/2013 12-13 Corporate Social Responsibility Initiatives 14 Board of Directors & Capital 15 Report and Financial Statements 2013 16-18 Corporate Information 19-20 Report of the Directors 21-22 Independent Auditors’ Report 23 Financial Statements 2013 24 Statement of Comprehensive Income 25 Statement of Financial Position 26 Statement of Changes in Equity 27 Statement of Cash Flows 28-81 Notes to the Financial Statements © All rights reserved. Message from the CEO of BOA GROUP The BANK OF AFRICA Group’s 2013 financial year was highlighted mainly by the following five objectives: • continue its external growth, • improve its operating structure, • launch a vast plan to strengthen its risk control, • expand its sales & marketing set up, • continue to enhance its financial results. The BANK OF AFRICA Group’s development was reflected in 2013 by the opening of a subsidiary in Togo. Meanwhile, the Group’s institutionalisation continued with an expansion in its Central Departments at head office. With the same determination of more precision-based management, a major project for redefining risk management was launched in synergy with the BMCE Bank Group, our majority shareholder. In the same light, a system of environmental and social management was set up in this same area. -

Bmce Bank of Africa Group

BMCE BANK OF AFRICA GROUP JUNE 2019 Content BMCE BANK OF AFRICA GROUP OVERVIEW 3 A LARGE PRESENCE IN AFRICA 11 A COMMITTED GROUP TO SUSTAINABLE 18 DEVELOPMENT AND POSITIVE IMPACT FINANCE FOCUS ON DIGITAL TRANSFORMATION 27 GROUP GROWTH DRIVERS 32 INVESTMENT RATIONALE 34 BMCE BANK OF AFRICA GROUP OVERVIEW A Multi Brand Universal Banking Group Bank Of Africa LCB Bank Banque de Développement du Mali BMCE International Holding – Retail Banking Madrid : Trade Finance ; London & Paris : Investment Corporate Wholesale Banking Banking & Corporate Finance BMCE Euroservices – Banking for Moroccans Living Abroad BMCE Shanghai BMCE Bank Parent Overseas Company Specialised operations Financial Services Salafin – Consumer credit Maghrebail - Leasing RM Experts – Debt Collection Maroc Factoring - Factoring Investment BMCE Capital Plc Euler Hermes Acmar – Credit Insurance banking BMCE Capital Bourse BTI Bank – Participatory Bank BMCE Capital Gestion Advisory & Financial Engineering, Asset Management, Private Banking, Securities Brokerage, Capital Markets, Financial Research, Post-Trade Solutions, Securitisation 4 BMCE Bank of Africa Worldwide Germany Italy China-Shanghai Belgium Netherlands Canada Spain Portugal United Arab Emirates France United Kingdom ASIA EUROPE NORTH AMERICA +15,200 Employees AFRICA 31 Countries 1,700 Branches Morocco Cote d’Ivoire Mali Rwanda Benin Djibouti Madagascar Senegal Burkina Faso Ethiopia Niger Tanzania 6.6 million Burundi Ghana Uganda Togo Customers Congo Brazzaville Kenya D.R.C Tunisia 5 5 BMCE Bank of Africa key figures -

En 2012, La BANK of AFRICA – MALI (BOA-MALI) a Principalement Orienté Ses Actions Citoyennes Dans Les Domaines Économique Et Social

Place de l'independance, Bamako-Mali. 6 avril 2025. 11-45-05 Au coeur du développement Annual report Annual Au coeur de l’Afrique 2012 Rapport annuel BANK OF AFRICA – MALI Le Groupe BOA fête ses 30 ans BOA Group celebrates its 30th Anniversary Sommaire BANK OF AFRICA Group Table of contents celebrates its 30th Anniversary 1 Le mot du PDG This year we are celebrating our Group’s 30th Anniversary. Comments from the CEO BANK OF AFRICA was established at a time when the West African banking sector experienced serious difficulties. 2-3 30 ans de croissance et d’expansion The founder’s goal of the first BANK OF AFRICA, BOA-MALI, 30 years of growth and expansion created in 1983 and then headed by Paul DERREUMAUX, 4 30 ans d’expérience au service des clients was to fill a gap by creating a private African bank, with 30 years of experience serving customers African capital, and dedicated to serving the African economy. 5 Les engagements du Groupe depuis 30 ans The original shareholders felt keenly the immense potential of a The commitments of the Group for 30 years project that would help bring Africa together for a better future. Investors – both private and public, both national and 6 Produits et Services disponibles international – had also placed their trust in this project French only and helped it to develop into what it is today – a group with a presence in 15 African countries through 16 commercial Rapport d’Activité banks as well as numerous financial companies. Activity Report The majority shareholder, BMCE Bank, has put at the disposal of BOA Group its multiple skills, as well as its international 8-9 Le mot du Directeur Général and continental experience. -

Bank of Africa – Rdc Rapport Annuel / Annual Report 2011

BANK OF AFRICA – RDC RAPPORT ANNUEL / ANNUAL REPORT 2011 Pour l’essor de notre continent. Developing our continent. Sommaire Table of contents Banques et Filiales du Groupe 1 Group Banks and Subsidiaries BANK OF AFRICA – NIGER 8 Agences à Niamey. Les points forts du Groupe 2-3 8 Agences régionales. Group strong points 8 Branches in Niamey. 8 Regional Branches. Produits et Services disponibles 4 BANK OF AFRICA – MALI French only 15 Agences à Bamako. 8 Agences régionales et 5 Bureaux de proximité. 15 Branches in Bamako. Rapport d’Activité Exercice 2011 8 Regional Branches and 5 Local Branches. Activity Report Fiscal year 2011 BANK OF AFRICA – SÉNÉGAL 18 Agences à Dakar. 7 Agences régionales. Le mot du Directeur Général 6-7 18 Branches in Dakar. Comments from the Managing Director 7 Regional Branches. Faits marquants 2011 8 BANK OF AFRICA – BURKINA FASO Highlights 14 Agences à Ouagadougou. 11 Agences régionales. Chiffres-clés 2011 9 14 Branches in Ouagadougou. 11 Regional Branches. Key figures Engagements citoyens de la Banque 10-11 BANK OF AFRICA – CÔTE D’IVOIRE 12 Agences à Abidjan. French only 8 Agences régionales et 1 Bureau de proximité. 12 Branches in Abidjan. Conseil d’Administration, Capital 12 8 Regional Branches and 1 Local Branch. Board of Directors, Capital BANK OF AFRICA – GHANA Rapport du Commissaire aux Comptes 14-15 14 Agences à Accra. 5 Agences régionales. Independent Accountant’s Report 14 Branches in Accra. 5 Regional Branches. États financiers 16-21 Financial Statements BANK OF AFRICA – BÉNIN 23 Agences à Cotonou. Notes aux États financiers 22-34 19 Agences régionales. -

Banking in Africa: Delivering on Financial Inclusion, Supporting Stability

Banking in Africa: Delivering on Financial Inclusion, Supporting Stability EUROPEAN INVESTMENT BANK Banking in Africa: Delivering on Financial Inclusion, Supporting Financial Stability years Banking in Africa: Delivering on Financial Inclusion, Supporting Financial Stability October 2018 Banking in Africa: Delivering on Financial Inclusion, Supporting Financial Stability About the Report At its fourth edition, this report provides an analysis of recent development in the African banking sectors and specific structural topics of relevance. It combines in house research with contribution from leading market experts from commercial banks operating in the region, IFIs and other institutions. About the Economics Department of the EIB The mission of the EIB Economics Department is to provide economic analyses and studies to support the Bank in its operations and in the definition of its positioning, strategy and policy. The Department, a team of 30 economists, is headed by Debora Revoltella, Director of Economics. Main Contributors to This Year’s Report Economic Editor: Jean-Philippe Stijns, under the lead of Barbara Marchitto, Head of the Country & Financial Sector Analysis Division, and Debora Revoltella, Director of the Economics Department Introduction - Jean-Philippe Stijns Chapter 1 - Sub-Saharan African Banking Sectors: Results from a Survey of Banking Groups: Jean- Philippe Stijns and Adeline Pelletier. Chapter 2 - Banking Sector Trends in West Africa: Claudio Cali, Emmanouil Davradakis, Nina Fenton and Amine El Kourchi Chapter 3 - The -

Bank of Africa Presentation

BANK OF AFRICA PRESENTATION May 2021 Contents BANK OF AFRICA OVERVIEW 3 BANK OF AFRICA’S STRATEGY 12 MAIN TAKEAWAYS 2020 14 LARGE PRESENCE IN AFRICA 20 EUROPEAN ACTIVITIES 28 A SOCIALLY RESPONSIBLE BANK 30 BANK OF AFRICA OVERVIEW BANK OF AFRICA, a universal banking group BANK OF AFRICA is one of Africa’s main pan-African financial groups. With an extensive portfolio of brands and subsidiaries, BANK OF AFRICA has adopted a universal banking business model comprising a variety of business lines, including commercial banking, investment banking as well as specialised financial services such as leasing, factoring, consumer credit and participatory banking. 4 A multi Brand Universal Banking Group BOA Holding LCB Bank Retail Banking Banque de Développement du Mali BMCE Corporate Wholesale Banking International Holding – Madrid : Trade Finance ; London & Paris : Investment Banking & Corporate Finance BMCE Euroservices –Diaspora activities BANK OF AFRICA Shanghai BANK OF AFRICA -Parent Company- Specialized Overseas Financial operations Services Salafin – Consumer credit Maghrebail - Leasing RM Experts – Debt Collection Investment BMCE Capital Plc Maroc Factoring - Factoring BMCE Capital Bourse banking Euler Hermes Acmar – Credit Insurance BTI Bank – BMCE Capital Gestion Participatory Bank Advisory & Financial Engineering, Asset Management, Private Banking, Stock Brokerage, Capital Markets, Financial Research, Post-Trade Solutions, Securitisation 5 BANK OF AFRICA across the world Germany Italy China Belgium Netherlands Canada Spain Portugal United -

Registration Document and Annual Report 2010 3 Summary

Registration document and annual report 2010 3 Summary Message from the Chairman and Chief Executive Officer 2 4 » Consolidated financial statements 245 General framework 246 Consolidated financial statements 253 Notes to the consolidated financial statements 259 Statutory Auditors’ report on the consolidated financial statements 367 1 » Presentation of Crédit Agricole S.A. 5 2010 key figures and stock market data 6 Significant events in 2010 12 Company history 14 Organisation of Crédit Agricole Group and Crédit Agricole S.A. 16 5 » Separate financial statements 369 The business lines of Crédit Agricole S.A. 17 Separate financial statements at 31 December 2010 370 Economic, social and environmental information 31 Notes to the separate financial statements 373 Statutory Auditors’ Report 418 2 » Corporate Governance 73 Report of the Chairman » General information 421 of the Board of Directors 74 6 Statutory Auditors’ report 99 Memorandum and Articles of Association 422 Compensation paid to Executive Information on the Company 439 and non-Executive Corporate Officers 100 Information concerning the share capital 447 Offices held by Corporate Officers 111 Statutory Auditors’ special report Governing bodies 138 on related party agreements and commitments 450 Fees paid to Statutory Auditors 453 General Meeting of Shareholders of 18 May 2011 454 Persons responsible for the registration document 471 Cross-reference table 473 3 » 2010 Management report 141 Operating and financial review 142 Information on the financial statements of Crédit Agricole S.A. (parent company) 167 Risk factors 176 Basel II Pillar 3 disclosures 216 Registration Document 2010 Annual report 3 Profile Crédit Agricole Group is the leading full-service retail bank in France and one of the major banking groups in Europe. -

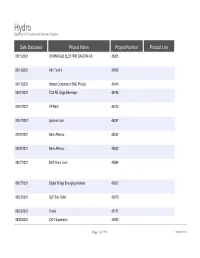

Date Disclosed Project Name Project Number Product Line 09/15/2021 OSMANGAZI ELEKTRIK DAGITIM AS 45265

Hydro Based on IFC Investment Services Projects Date Disclosed Project Name Project Number Product Line 09/15/2021 OSMANGAZI ELEKTRIK DAGITIM AS 45265 09/13/2021 A91 Fund II 45858 09/13/2021 Khaadi Corporation SMC Pvt Ltd 45445 09/07/2021 FCS RE Kings Beverage 44796 09/07/2021 AP Bank 45736 09/07/2021 Ipoteka Loan 45287 09/02/2021 Bank Alliance 45832 09/02/2021 Bank Alliance 45832 08/27/2021 BOP Omni Loan 43584 08/27/2021 Digital Bridge Emerging Markets 45362 08/23/2021 GyT Sub. Debt 43670 08/23/2021 Toters 45171 08/20/2021 CIDT Expansion 45030 Page 1 of 1790 09/24/2021 Hydro Based on IFC Investment Services Projects Company Name Country Sector OSMANGAZI ELEKTRIK Turkey Infrastructure DAGITIM AS A91 EMERGING FUND II India Funds LLP KHAADI SMC PVT. LTD. Pakistan Tourism, Retail, and Property KINGS BEVERAGES PVT Sierra Leone Agribusiness and Forestry LIMITED AGROPROSPERIS BANK, Ukraine Financial Institutions PAT IPOTEKA BANK JSC Uzbekistan Financial Institutions MORTGAGE BANK BANK ALLIANCE PUBLIC Ukraine Financial Institutions JOINT STOCK COMPANY BANK ALLIANCE PUBLIC Ukraine Financial Institutions JOINT STOCK COMPANY Omni S.A Credito Brazil Financial Institutions Financiamento e Investimento DIGITAL COLONY Latin America Region Telecommunications, Media, and Technology ACQUISITIONS BANCO G AND T Guatemala Financial Institutions CONTINENTAL S.A. TAN HOLDING SAL Lebanon Tourism, Retail, and Property COMPAGNIE IVOIRIENNE Cote D'Ivoire Agribusiness and Forestry Page 2 of 1790 09/24/2021 Hydro Based on IFC Investment Services Projects Environmental