Pr Spectus Initial Public Offer Offer for Sale and Offer for Subscription

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report & Financial Statements

2014 ANNUAL REPORT & FINANCIAL STATEMENTS EASTERN AND SOUTHERN AFRICAN TRADE AND DEVELOPMENT BANK TABLE OF CONTENTS LETTER OF TRANSMITTAL 3 CHAIRMAN’S STATEMENT 5 PRESIDENT’S STATEMENT 8 Strategic Overview 8 Operations 11 Project and Infrastructure Finance (PIF) 11 Trade Finance 11 Funds Management 11 Risk Management 11 Resource Mobilization 12 International Ratings 13 Financial Management 14 Human Resources and Administration 15 Conclusion 15 3 STATEMENT ON CORPORATE GOVERNANCE 16 SUSTAINABILITY REPORTING STATEMENT 20 ECONOMIC ENVIRONMENT 24 FINANCIAL MANAGEMENT & TREASURY 30 OPERATIONS 36 Project and Infrastructure Finance 38 Trade Finance 40 Funds Management 43 Portfolio Management 44 Compliance and Risk Management 45 Human Resources and Administration 47 2014 Annual Report & Financial Statements & Financial Annual Report 2014 Information Technology 48 ANNUAL REPORT & FINANCIAL STATEMENTS 2014 49-151 FINANCIAL HIGHLIGHTS 24% 30% LOAN ASSETS EQUITY CAPITAL US$ 2.51billion US$ 622 million 16% 31% NET PROFIT NON-PERFORMING US$ 77 million LOANS 3.04% LETTER OF TRANSMITTAL 5 The Chairman Board of Governors Eastern and Southern African Trade and Development Bank Dear Mr. Chairman, In accordance with Article 35(2) of the Bank’s Charter, I have the honour, on behalf of the Board of Directors, to submit herewith the Annual Report of the Bank for the period 1 January to 31 December 2014. The report covers the year’s activities and audited financial statements for the period. 2014 Annual Report & Financial Statements & Financial Annual Report 2014 Mr. Chairman, please accept the assurances of my highest consideration. MR. RUPERT HORACE SIMEON Chairman of the Board of Directors 6 2014 Annual Report & Financial Statements & Financial Annual Report 2014 CHAIRMAN’S STATEMENT Chairman’s Statement The African and International Economic Context subscribed up to 98% of the General Capital Increase launched in 2007. -

Malawi 2018-19 Draft Financial Statement

Budget Document No. 3 Government of Malawi DRAFT 2018/19 FINANCIAL STATEMENT Ministry of Finance, Economic Planning and Development P.O. Box 30049 Lilongwe ii 2018-19 Financial Statement DRAFT 2018/19 FINANCIAL STATEMENT iii 2018-19 Financial Statement iv 2018-19 Financial Statement Table of Contents Abbreviations and Acronyms .......................................................................................................................... viii 1. INTRODUCTION .......................................................................................................................................... 9 2. THE 2016/17 FISCAL YEAR PERFORMANCE.............................................................................................. 10 2.1 Revenue and Grants ......................................................................................................................... 12 2.1.1 Domestic Revenue ................................................................................................................... 12 2.1.2 Grants ....................................................................................................................................... 13 2.2 Expenditure and Net Lending .......................................................................................................... 14 2.2.1 Recurrent Expenditure ............................................................................................................. 15 2.2.2 Development Expenditures ..................................................................................................... -

Draft 2019/20 Financial Statement

Budget Document No. 3 Government of Malawi DRAFT 2019/20 FINANCIAL STATEMENT Ministry of Finance, Economic Planning and Development P.O. Box 30049 Lilongwe Table of Contents Abbreviations and Acronyms ............................................................................................................................ iv 1. INTRODUCTION .......................................................................................................................................... 5 2. THE 2017/18 FISCAL YEAR PERFOMANCE .................................................................................................. 6 2.1 Revenue ................................................................................................................................................ 9 2.1.1 Domestic Revenue ............................................................................................................................... 9 2.1.2 Grants .................................................................................................................................................. 10 2.2 Expenditure ......................................................................................................................................... 11 2.2.1 Expenses ............................................................................................................................................. 11 2.2.2 Acquisition of Non-Financial Assets .................................................................................................. 12 -

2015 BROOKINGS FINANCIAL and DIGITAL INCLUSION PROJECT REPORT Measuring Progress on Financial Access and Usage

WASHINGTON, DC | AUGUST 26, 2015 THE 2015 BROOKINGS FINANCIAL AND DIGITAL INCLUSION PROJECT REPORT Measuring Progress on Financial Access and Usage BY JOHN D. VILLASENOR, DARRELL M. WEST, AND ROBIN J. LEWIS About the Center for Technology Innovation at Brookings The Center for Technology Innovation (CTI) at Brookings focuses on delivering research that impacts public debate and policymaking in the arena of U.S. and global technology innovation. CTI’s goals include: Identifying and analyzing key developments to increase innovation; developing and publicizing best practices to relevant stakeholders; briefing policymakers about actions needed to improve innovation; and enhancing the public and media’s understanding of technology innovation. About the Brookings Institution The Brookings Institution is a nonprofit organization devoted to independent research and policy solutions. Its mission is to conduct high-quality, independent research and, based on that research, to provide innovative, practical recommendations for policymakers and the public. The conclusions and recommendations of any Brookings publication are solely those of its author(s), and do not reflect the views of the Institution, its management, or its other scholars. WASHINGTON, DC | AUGUST 26, 2015 THE 2015 BROOKINGS FINANCIAL AND DIGITAL INCLUSION PROJECT REPORT Measuring Progress on Financial Access and Usage BY JOHN D. VILLASENOR, DARRELL M. WEST, AND ROBIN J. LEWIS Comments and feedback regarding the Financial and Digital Inclusion Project can be submitted to [email protected]. THE 2015 BROOKINGS FINANCIAL AND DIGITAL INCLUSION PROJECT REPORT 1 TABLE OF CONTENTS EXECUTIVE SUMMARY ............................................................ 2 THE IMPORTANCE OF FINANCIAL INCLUSION ............................... 7 MEASURING FINANCIAL INCLUSION .......................................... 10 DIMENSIONS OF EVALUATION ................................................... 12 Overall ranking on financial inclusion .................................. -

Map District Site Balaka Balaka District Hospital Balaka Balaka Opd

Map District Site Balaka Balaka District Hospital Balaka Balaka Opd Health Centre Balaka Chiendausiku Health Centre Balaka Kalembo Health Centre Balaka Kankao Health Centre Balaka Kwitanda Health Centre Balaka Mbera Health Centre Balaka Namanolo Health Centre Balaka Namdumbo Health Centre Balaka Phalula Health Centre Balaka Phimbi Health Centre Balaka Utale 1 Health Centre Balaka Utale 2 Health Centre Blantyre Bangwe Health Centre Blantyre Blantyre Adventist Hospital Blantyre Blantyre City Assembly Clinic Blantyre Chavala Health Centre Blantyre Chichiri Prison Clinic Blantyre Chikowa Health Centre Blantyre Chileka Health Centre Blantyre Blantyre Chilomoni Health Centre Blantyre Chimembe Health Centre Blantyre Chirimba Health Centre Blantyre Dziwe Health Centre Blantyre Kadidi Health Centre Blantyre Limbe Health Centre Blantyre Lirangwe Health Centre Blantyre Lundu Health Centre Blantyre Macro Blantyre Blantyre Madziabango Health Centre Blantyre Makata Health Centre Lunzu Blantyre Makhetha Clinic Blantyre Masm Medi Clinic Limbe Blantyre Mdeka Health Centre Blantyre Mlambe Mission Hospital Blantyre Mpemba Health Centre Blantyre Ndirande Health Centre Blantyre Queen Elizabeth Central Hospital Blantyre South Lunzu Health Centre Blantyre Zingwangwa Health Centre Chikwawa Chapananga Health Centre Chikwawa Chikwawa District Hospital Chikwawa Chipwaila Health Centre Chikwawa Dolo Health Centre Chikwawa Kakoma Health Centre Map District Site Chikwawa Kalulu Health Centre, Chikwawa Chikwawa Makhwira Health Centre Chikwawa Mapelera Health Centre -

ACE) Office of Higher Education for Development (HED

U.S. Agency for International Development (USAID) and The American Council on Education (ACE) office of Higher Education for Development (HED) Michigan State University and University of Malawi Partnership “Agro-ecosystems Services: Linking Science to Action in Malawi and the Region (AgESS)” April 5, 2011 – May 30, 2014 FINAL ASSOCIATE AWARD REPORT August 2014 USAID/Malawi Associate Award Cooperative Agreement # AEG-A-00-05-00007-00 Associate Cooperative Agreement # 674-A-00-11-00030-00 Higher Education for Development was established in 1992 by the six major U.S. higher education associations to engage the higher education community in global development. — American Council on Education (ACE) | American Association of Community Colleges (AACC) | American Association of State Colleges and Universities (AASCU) | Association of American Universities (AAU) | National Association of Independent Colleges and Universities (NAICU) | Association of Public and Land-Grant Universities (APLU) PARTNERSHIP INFORMATION Lead Partner Institutions: Michigan State University; University of Malawi-Chancellor College; Lilongwe University of Agriculture and Natural Resources (LUANAR) Secondary Partner Institutions: The Lincoln University Region, Country: Malawi Performance Period: April 5, 2011 – May 30, 2014 Funding Level: Associate Award: $1,385,806 and Subaward: $1,140,000 Proposed Cost Share: $322,204 Table of Contents 1. Executive Summary .................................................................................................. 5 2. Partnership -

FDH Bank Financials 2019 FINAL

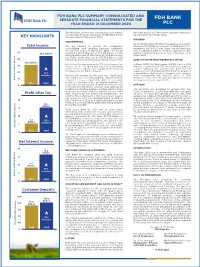

SUMMARY AUDITED FINANCIAL STATEMENTS FDH BANK FDH Bank FOR THE YEAR ENDED 31 DECEMBER 2019. LIMITED Main Highlights Net interest Income 7% Total Income Non Interest income 23% 10 40 K34.3 K7.8 Billion Corporate Social Responsibility 21% Billion K29 8 Billion a a 2019 K5.9 30 ach Billion 2019 ach Total Assets 24% Kw 6 Kw 2018 2018 20 4 Loan Book Growth 40% 10 Amount in Billion 2 32% Amount in Billion 18% Increase Increase Return on Equity 35% 0 0 NPL Ratio down to 0.80% K Customer Deposits Basic Earnings per Introduced WhatsApp Banking Share (Tambala) K137.1 Billion New Branch Goliati - Thyolo 150 2000 K112.5 1,696 Tambala a Billion 2019 1,289 Tambala ach 1500 Upgraded Branches Mulanje, Chiponde, Mzimba, Kw 100 2019 and Agencies Chitipa, Jenda & Neno 2018 ambala 2018 1000 50 Amount in T 500 Amount in Billion 22% 32% Increase Increase 0 0 FDH BANK LIMITED FINANCIAL RESULTS FOR Malawi GDP growth rate is projected to average between 5% and 6%, according to the Reserve Bank of Malawi. YEAR ENDED 31 DECEMBER 2019. Private sector credit annual growth in 2019 was 21.3% up from 11.5% in 2018. The The Directors present the audited summarised financial statements of FDH Bank stronger growth in private sector credit in 2019 is a reflection of reduced interest rates. Limited for the year ended 31 December 2019. We anticipate the low interest rates regime to continue and spur private sector credit growth in 2020. PERFORMANCE The Bank continues to consolidate and improve on the convenient delivery channels The Directors report a profit after tax of K7.846 billion for the year ended 31 through its digital products and providing innovative first class financial solutions. -

FEWS NET Malawi Enhanced Market Analysis September 2018

FEWS NET Malawi Enhanced Market Analysis 2018 MALAWI ENHANCED MARKET ANALYSIS SEPTEMBER 2018 This publication was produced for review by the United States Agency for International Development. It was prepared by Chemonics International Inc. for the Famine Early Warning Systems Network (FEWS NET), contract number AID-OAA-I-12-00006. The authors’Famine views Early expressed Warning inSystem this publications Network do not necessarily reflect the views of the 1 United States Agency for International Development or the United States government. FEWS NET Malawi Enhanced Market Analysis 2018 About FEWS NET Created in response to the 1984 famines in East and West Africa, the Famine Early Warning Systems Network (FEWS NET) provides early warning and integrated, forward-looking analysis of the many factors that contribute to food insecurity. FEWS NET aims to inform decision makers and contribute to their emergency response planning; support partners in conducting early warning analysis and forecasting; and provide technical assistance to partner-led initiatives. To learn more about the FEWS NET project, please visit www.fews.net. Disclaimer This publication was prepared under the United States Agency for International Development Famine Early Warning Systems Network (FEWS NET) Indefinite Quantity Contract, AID-OAA-I-12-00006. The authors’ views expressed in this publication do not necessarily reflect the views of the United States Agency for International Development or the United States government. Acknowledgements FEWS NET gratefully acknowledges the network of partners in Malawi who contributed their time, analysis, and data to make this report possible. Recommended Citation FEWS NET. 2018. Malawi Enhanced Market Analysis. Washington, DC: FEWS NET. -

Financial Market Update I Week Ending 21 May 2021 Financial Market Highlights for the Week Ending 21 May 2021

Financial Market Update I Week ending 21 May 2021 Financial market highlights for the week ending 21 May 2021 The following highlights compare the week ending 21 May 2021 to the week ending 13 May 2021: Government securities market (Source: RBM) Equity market (Source: MSE) • A total of K12.73 billion was allotted during this week’s • The stock market was bullish this week as the MASI Treasury Bills (TBs) and 2-Year Treasury Note (TN) marginally increased to 33,606.87 points from 33,398.30 auctions. points in the previous week. This was due to share price • There were nil rejections during the TB auctions. gains for Airtel (to K32.50 from K31.02) and Standard bank • The 2-Year TN had a rejection rate of 13.37%. (to K1,200.15 from K1,200.14), which offset share price • The 364-days TB had the highest subscription rate of losses for MPICO (to K17.00 from K19.00), ICON (to K12.14 59.95%. from K12.16), TNM (to K16.34 from K16.35), and FDH bank (to K16.42 from K16.46), during the period under review. Currency market (Source: RBM) • The year-to-date return of the MASI was 3.75% at the close • Based on middle rates, the Malawi Kwacha marginally of this week. It was negative 5.78% in the previous year, depreciated against the USD by 0.14% to K802.22/USD from during the same period. K801.11/USD in the previous week. Financial market developments (Source: RBM & • Based on middle rates, the Kwacha also depreciated against the GBP (to K1,192.11/GBP from K1,175.77/GBP) , the EUR Company Financials) (to K1,040.81/EUR from K1,025.90/EUR) and the ZAR (to • The average overnight interbank rate maintained its position K61.19/ZAR from K60.45/ZAR), during the period under at 11.92% during the period under review. -

Fdh Bank Plc Summary Consolidated and Separate Financial Statements for the Fdh Bank Year Ended 31 December 2020 Plc

FDH BANK PLC SUMMARY CONSOLIDATED AND SEPARATE FINANCIAL STATEMENTS FOR THE FDH BANK YEAR ENDED 31 DECEMBER 2020 PLC The Directors present the summarized consolidated per share and as at 31 December 2020 the share price and separate financial statements of FDH Bank Plc for had moved to K14.45 per share. KEY HIGHLIGHTS the year ended 31 December 2020. DIVIDEND PERFORMANCE On 8 February 2021, the Directors approved an interim Total Income We are pleased to present the summarized dividend of K3.0 billion in respect of 2020 profits, this consolidated and separate financial statements represents 43t (K0.43) per share. The dividend was for the year ended 31 December 2020. The Group paid on 26 March 2021 to members appearing in the 50 43.6 Billion reported a profit after tax of K14.368 billion and the register of the Company as at close of business on 12 Bank reported a profit after tax of K14.956 billion from March 2021. the Bank’s profit after tax of K5.193 billion in 2019 40 (Restated) amid a challenging operating environment. ACQUISITION OF MSB PROPERTIES LIMITED 30.6 Billion Net Interest Income went up by 77% on the back of an In March 2020, the Bank acquired 100% stake in MSB 30 increase in the loan book and other interest bearing Properties Limited from FDH Money Bureau Limited, assets. Interest expense went up by 15.8% reflecting a sister company. The consideration given for the the growth of the Bank’s deposits. acquisition was K5.599 billion. The Bank has prepared 20 42% a consolidated statement of comprehensive income Increase Non-interest Income in the year was significantly which incorporates the financial results of MSB 10 affected by the Covid-19 pandemic. -

Fdh Bank Plc Ipo Pre-Listing Statement

FDH BANK PLC IPO FDH Bank PRE-LISTING STATEMENT FDH Bank Offer for Sale of 979,175,000 Ordinary Shares and Offer for Subscription of 401,031,250 Ordinary Shares each at an Offer Price of MWK10.00 per Share and admission to trade on the Malawi Stock Exchange A copy of the Pre-Listing Statement has been delivered to and registered by the Registrar of Financial Institutions (‘Registrar’). The Registrar has not checked and will not check the accuracy of any statements and they accept no responsibility therefor or for the financial soundness of FDH Bank Plc or the value of the securities offered. The Registrar registered this Pre-Listing Statement on 26th June 2020 CORPORATE ADVISORS PRE-LISTING STATEMENT Lead Corporate Advisor Legal Advisor This Pre-Listing Statement is in respect of an Offer for Sale of up Ernst & Young Tembenu, Masumbu & Company to 979,175,000 ordinary shares and Offer for Subscription of up to Chartered Accountants Malawi Gelu House 401,031,250 ordinary shares (‘Offer Shares’) each at an Offer Price of Apex House, Kidney Crescent Kamuzu Procession Rd MWK10.00 per Share and admission to trade on the Malawi Stock P.O. Box 530 P.O. Box 2777 rd Blantyre, Malawi Lilongwe, Malawi Exchange with effect from the commencement of trading on Monday, 3 Tel +265 (0) 1 876 476 Tel +265 (0) 1 756 286 August 2020 (‘the Listing Date’). [email protected] [email protected] Reporting Accountant Transfer Secretary This Pre-Listing Statement is not an invitation to the public to subscribe for shares but is issued in compliance with the rules and requirements of the Deloitte NICO Asset Managers Limited Malawi Stock Exchange for the purpose of giving information to the public Chartered Accountants Malawi Chibisa House P.O. -

August 2020 August 2020 November 2020

AUGUST 2020 AUGUST 2020 NOVEMBER 2020 1 MONTHLY ECONOMIC REPORT NOVEMBER 2020 Contents LIST OF ACRONYMS ............................................................................................................................................. 3 EXECUTIVE SUMMARY ......................................................................................................................................... 4 ECONOMIC OVERVIEW ........................................................................................................................................ 6 Inflation (Source: NSO) ..................................................................................................................................................... 6 Government Securities (Source: RBM) ............................................................................................................................. 6 Foreign Currency Market (Source: RBM) ......................................................................................................................... 6 Interbank Markets and Interest Rates (Source: RBM)...................................................................................................... 6 Stock Market (Source: MSE) ............................................................................................................................................. 7 OTHER MARKET DEVELOPMENTS ....................................................................................................................... 9 Tobacco Markets Update