Canada's Energy Future: Scenarios for Supply and Demand to 2025 Was Released in 2003

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

IPC 2018 Program 9 19.Indd

CONFERENCE September 24 – September 28 Calgary, Alberta, Canada Program BUILDING the FUTURE NOW http://www.internationalpipelineconference.com IPC is co-owned by ASME and CEPA MESSAGE FROM THE PREMIER OF ALBERTA On behalf of the Government of Alberta, it is my pleasure to welcome everyone to the International Pipeline Conference 2018. The opportunity to build Canadian energy infrastructure is here. This is an important moment in Canada’s history; allowing us to put disagreements behind us and to work together as partners and members of the great Canadian family to build a greener, stronger, more sustainable, more prosperous, more equal, and more resilient country. We know pipelines are the safest, most cost-effective way to move oil to market. And we know there is a global appetite for oil that is developed responsibly. We have already seen interest in our products from markets around the globe – what we need is the means to get it there. This conference connects experts from around the world to exchange ideas and learn about exciting, new initiatives in the pipeline industry. From discussions on effective pipeline project delivery and design to reclamation and mitigation, we can all benefit from your shared ideas. I commend all the delegates here today for your dedication to work together to develop safe, reliable, and responsible ways to transport energy resources. Our government is committed to working in partnership with the energy industry and our provincial and federal partners to build pipelines and expand our market access. I’m very optimistic there is a way forward but this path requires a careful balance. -

How Will We Power the Future? an Exciting Benefit for You As a University of Alberta Alumni Association Member

How will we power the future? An exciting benefit for you as a University of Alberta Alumni Association member. Get preferred rates and coverage that fits your needs. Take advantage of your You save with alumni privileges. You have access to the TD Insurance Meloche Monnex preferred program. This means you can get preferred insurance insurance rates. rates on a wide range of home, condo, renter’s and car coverage that can be customized for your needs. For over 65 years, TD Insurance has been helping Canadians find quality insurance solutions. Feel confident your coverage fits your needs. Get a quote now. Recommended by HOME | CAR Get a quote and see how much you could save ! Call 1-866-269-1371 or go to tdinsurance.com/ualbertaalumni The TD Insurance Meloche Monnex program is underwritten by SECURITY NATIONAL INSURANCE COMPANY. It is distributed by Meloche Monnex Insurance and Financial Services, Inc. in Québec, by Meloche Monnex Financial Services Inc. in Ontario, and by TD Insurance Direct Agency Inc. in the rest of Canada. Our address: 50 Place Crémazie, 12th Floor, Montréal, Québec H2P 1B6. Due to provincial legislation, our car and recreational insurance program is not offered in British Columbia, Manitoba or Saskatchewan. All trade-marks are the property of their respective owners. ® The TD logo and other TD trade-marks are the property of The Toronto-Dominion Bank. SPRING 2019 VOLUME 75 NUMBER 1 “We are somewhere between the hydrocarbon age and the age of electricity. And one is supporting the other.” larry kostiuk, ’85 msc 3 39 Your Letters Trails Where you’ve been and 5 where you’re going Notes What’s new and noteworthy 40 Books 10 Continuing Education 42 Column by Curtis Gillespie feature Class Notes 13 20 51 Thesis Energy: from now to next In Memoriam It’s beyond the stars and within From fire to coal, wind to steam, our cells. -

ARC Energy Investment Forum Speaker Biographies

ARC Energy Investment Forum Speaker Biographies The Battle for the Hearts and Wheels of the Market Monday April 3, 2017 Heritage Park, Gasoline Alley Museum, Calgary, Alberta Watch for more exciting speaker announcements coming soon! Check back at www.arcenergyinstitute.com for updates. Steve Przesmitzki Global Team Leader for Strategic Transport Analysis in Saudi Aramco Research and Development Steve is based out of the Aramco Research Center in Detroit, and leads the analysis teams located in Detroit, Paris, and Dhahran. The teams perform technical analysis focusing on current and future transportation technology, transportation regulatory policy, energy-use trends, and economic impacts. Steve has worked at Aramco since April 2014. Steve was previously a Technology Development Manager for fuels and lubricants within the United States Department of Energy’s Vehicle Technologies Program. Steve’s prior responsibility was to support the development of energy policy and management of research programs in transportation. Steve’s other work experience includes transportation fuels research for DOE’s National Renewable Energy Laboratory and vehicle powertrain design and development at Ford Motor Company. Steve holds a PhD from the Massachusetts Institute of Technology, a MS from the University of Michigan, and a BS from Kettering University; all in Mechanical Engineering. He is also registered as a Professional Engineer in Michigan. Doug Suttles President and Chief Executive Officer of Encana Corporation Doug Suttles joined Encana as President & CEO in June 2013. With over 30 years of experience in the oil and gas industry in various engineering and leadership roles, he is responsible for the overall success of Encana and for creating, planning, implementing and integrating the strategic direction of the organization. -

Positioning Canada's Electricity Sector in a Carbon Constrained Future

Positioning Canada’s Electricity Sector in a Carbon Constrained Future Report of the Standing Senate Committee on Energy, the Environment and Natural Resources The Honourable Richard Neufeld, Chair The Honourable Paul J. Massicotte, Deputy Chair SBK>QB SK>Q CANADA March 2017 For more information please contact us: by email: [email protected] by phone: 613-990-6080 toll-free: 1-800-267-7362 by mail: The Standing Senate Committee on Energy, the Environment and Natural Resources Senate, Ottawa, Ontario, Canada, K1A 0A4 This report can be downloaded at: sencanada.ca/en/committees/enev The Senate is on Twitter: @SenateCA, follow the committee using the hashtag #ENEV *********************** Ce rapport est également offert en français. Contents Members ....................................................................................................................................... iii Order of Reference ...................................................................................................................... iv Executive Summary ...................................................................................................................... v Addressing Climate Change......................................................................................................... 1 Canada’s Emission Commitment ................................................................................................ 1 Canada’s Electricity System ....................................................................................................... -

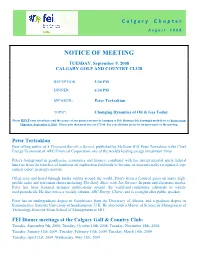

Peter Tertzakian

C a l g a r y C h a p t e r A u g u s t 2 0 0 8 NOTICE OF MEETING TUESDAY, September 9, 2008 CALGARY GOLF AND COUNTRY CLUB RECEPTION: 5:30 PM DINNER: 6:30 PM SPEAKER: Peter Tertzakian TOPIC: Changing Dynamics of Oil & Gas Today Please RSVP your attendance and the names of any guests you may be bringing to Deb Hastings [email protected] before noon Thursday, September 4, 2008. Please note that guest fees are $75.00. For cancellations please let us know prior to the meeting. Peter Tertzakian Best selling author of A Thousand Barrels a Second, published by McGraw-Hill, Peter Tertzakian is the Chief Energy Economist of ARC Financial Corporation, one of the world's leading energy investment firms. Peter's background in geophysics, economics and finance, combined with his entrepreneurial spirit, helped him rise from the trenches of hands-on oil exploration fieldwork to become an internationally recognized, top- ranked expert in energy matters. Often seen and heard through media outlets around the world, Peter's been a featured guest on many high- profile radio and television shows including The Daily Show with Jon Stewart. In print and electronic media, Peter has been featured in major publications around the world and contributes editorials to widely read periodicals. He also writes a weekly column, ARC Energy Charts, and is a sought after public speaker. Peter has an undergraduate degree in Geophysics from the University of Alberta, and a graduate degree in Econometrics from the University of Southampton, U.K. -

The Fiscal Pulse of Canada's Oil and Gas Industry

The Fiscal Pulse of Canada's Oil and Gas Industry A Review of Capital Flows and Activity energyresearch institute May 2016 Peter Tertzakian and Kara Jakeman May 2016 Table of Contents About ARC Financial Corp 4 Average Annual Operating Costs 24 Acknowledgements and Disclaimer 5 Other Costs 25 Executive Summary 6 Cash Flow, Capital Spending and Financings 26 The Fiscal Pulse of the Economy 8 Capital Spending Cuts 27 The 2016 Fiscal Pulse by the Numbers 9 Canadian Drilling Activity 28 Canadian Hydrocarbon Production 12 Market Access 29 Oil Sands Projects 14 The Fiscal Pulse With Varying Oil and Gas Prices 30 Global Commodity Reference Prices 15 Sensitivity of 2016 Metrics to Prices 31 Commodity Prices 16 Canadian Industry Metrics Compared to 2015 32 Canadian Upstream Industry Revenue 20 Industry Income Statement 34 Total Royalties and Land Bonuses 22 Industry Balance Sheet 35 © 2016 ARC Energy Research Institute. All Rights Reserved. May 2016 2 Fiscal Pulse of Canada’s Oil and Gas Industry © 2016 ARC Energy Research Institute. All Rights Reserved. May 2016 3 About ARC Financial Corp. and the Authors ARC Financial Corp. Peter Tertzakian, Chief Energy Economist and Managing Director, ARC Financial Corp. ARC Financial Corp. (“ARC”) is an energy-focused private equity firm based in Calgary, Alberta, Canada, with $5.3 billion of capital across eight Peter Tertzakian is the Chief Energy Economist and a Managing Direc- ARC Energy Funds. Leveraging off the experience, expertise, and indus- tor of ARC Financial Corp. Best selling author of A Thousand Barrels try relationships of more than 25 investment professionals, ARC invests A Second (McGraw-Hill, 2006) and The End of Energy Obesity ( John in upstream oil and gas, oilfield services and energy infrastructure. -

ALBERTA ENTERPRISE CORPORATION the Directory of Canadian Venture Capital & Private Equity Firms

The Directory of Canadian Venture Capital & Private Equity Firms Moscow 123317 Russia Korea Teachers Pension, 9th Floor Yeouido-dong Yeongdeungpo-Gu Seoul 150-742 South Korea Dubai Trade, 10th Floor Limitless Galleries Building 4 Downtown Jebel Ali Dubai United Arab Emirates Key Executives: Alex Kanayev, Managing Partner Education: San Diego State University; MBA, York University; CPA Background: Senior VP, Sprott Asset Management; Portfolio Manager, BMO Financial Group; Managing Partner, Goldman & Partners; Managing Director, RUS Communications Directorships: Capital Guardian Jeff Mesina, Vice President Education: University of Toronto Background: Toll Cross Securities; Front Street Capital; MacQuarie Private Wealth; Haywood Securities Kevin Temke, Associate Education: BSc, University of Victoria; University of Liverpool Medical School Background: National Institute of Clinical Excellence 6 ALBERTA ENTERPRISE CORPORATION Suite 1100 10830 Jasper Avenue Edmonton, AB T5J 2B3 Phone: 780-392-3901 Fax: 780-392-3908 [email protected] www.alberta-enterprise.ca Mission Statement: Our mission is to foster a thriving venture capital industry in Alberta that provides the capital and other resources needed to bring Alberta technologies to market, and create globally successful companies. We achieve this by investing as a Limited Partner in VC funds that meet the criteria outlined in our Investment Policy. These criteria include - but are not limited to - a successful track record, strong global networks, operational expertise, and a demonstrated -

Canada Rocks

22 Book Review: Canada Rocks – The Geological Journey 24 CSPG Finance Report 26 Reservoir Engineering for Geologists Part 5B 30 The Neoproterozoic Old Fort Point Formation, Southern Canadian Cordillera 35 Cadomin Tight Gas Reservoirs along the updip edge of the WCSB Deep Basin 40 2008 CSPG CSEG CWLS Convention MARCH 2008 VOLUME 35, ISSUE 3 Canadian Publication Mail Contract – 40070050 IHS AccuMap® “AccuMap encompasses speed, stability, efficiency and accuracy. As an intuitive and easy-to-use product, AccuMap serves a broad audience, from field users to the CEO.” Darrel Saik Senior Geological Technologist Paramount Energy Trust AccuMap is the most widely used and highly trusted oil and gas mapping software touching every segment of E&P, for every professional. www.ihs.com/energy Call toll free 1 877 495 4473 I_dY['/(-$$$ MARCH 2008 – VOLUME 35, ISSUE 3 ARTICLES Book Review: Canada Rocks - The Geological Journey ................................. 22 by Ashton Embry CSPG Finance Report ............................................................................................ 24 by Peter Harrington Reservoir Engineering for Geologists CSPG OFFICE #600, 640 - 8th Avenue SW Part 5B – Material Balance for Oil Reservoirs ............................................... 26 Calgary, Alberta, Canada T2P 1G7 by Ray Mireault P. Eng., Chris Kupchenko E.I.T., and Lisa Dean P. Geol. Tel: 403-264-5610 Fax: 403-264-5898 Web: www.cspg.org Office hours: Monday to Friday, 8:30am to 4:00pm The Neoproterozoic Old Fort Point Formation, Southern Canadian Cordillera ....................................................................... 30 Business Manager: Tim Howard Email: [email protected] by Mark D. Smith, R.W.C. (Bill) Arnott, and G.M. Ross Membership Services: Kristina Keith Email: [email protected] Cadomin Tight Gas Reservoirs along the updip edge Communications & Public Affairs: Heather Tyminski of the WCSB Deep Basin ............................................................................... -

Legislative Assembly of Alberta the 28Th Legislature First Session

Legislative Assembly of Alberta The 28th Legislature First Session Standing Committee on Alberta’s Economic Future Bitumen Royalty in Kind Program Stakeholder Presentations Tuesday, February 26, 2013 8:33 a.m. Transcript No. 28-1-7 Legislative Assembly of Alberta The 28th Legislature First Session Standing Committee on Alberta’s Economic Future Amery, Moe, Calgary-East (PC), Chair Bikman, Gary, Cardston-Taber-Warner (W), Deputy Chair Anglin, Joe, Rimbey-Rocky Mountain House-Sundre (W)* Barnes, Drew, Cypress-Medicine Hat (W)** Bhardwaj, Naresh, Edmonton-Ellerslie (PC) Blakeman, Laurie, Edmonton-Centre (AL) Donovan, Ian, Little Bow (W) Dorward, David C., Edmonton-Gold Bar (PC) Eggen, David, Edmonton-Calder (ND) Fenske, Jacquie, Fort Saskatchewan-Vegreville (PC) Goudreau, Hector G., Dunvegan-Central Peace-Notley (PC) Hehr, Kent, Calgary-Buffalo (AL) Jansen, Sandra, Calgary-North West (PC) Luan, Jason, Calgary-Hawkwood (PC) McDonald, Everett, Grande Prairie-Smoky (PC) Olesen, Cathy, Sherwood Park (PC) Quadri, Sohail, Edmonton-Mill Woods (PC) Quest, Dave, Strathcona-Sherwood Park (PC) Rogers, George, Leduc-Beaumont (PC) Sandhu, Peter, Edmonton-Manning (PC) Sherman, Dr. Raj, Edmonton-Meadowlark (AL) Smith, Danielle, Highwood (W) Starke, Dr. Richard, Vermilion-Lloydminster (PC) Strankman, Rick, Drumheller-Stettler (W) Towle, Kerry, Innisfail-Sylvan Lake (W) Young, Steve, Edmonton-Riverview (PC) Vacant * substitution for Danielle Smith ** substitution for Rick Strankman Support Staff W.J. David McNeil Clerk Robert H. Reynolds, QC Law Clerk/Director -

Vignettes of Canadian Petroleum Geology

June 5/11/06 7:21 PM Page 1 Canadian Publication Mail Contract - 40070050 $3.00 VOLUME 33, ISSUE 6 JUNE 2006 ■ Call for Photos ■ CSPG Awards – Honorary Membership, Graduate Thesis, and President’s Awards ■ Advances in Earth Sciences Research Conference ■ CSPG Outreach Student Conference ■ Triassic and Paleozoic Gas in the Foothills of British Columbia ■ Rock Creek Oil Discovery at Niton June 5/11/06 7:21 PM Page 2 June 5/11/06 7:21 PM Page 3 CSPG OFFICE #160, 540 - 5th Avenue SW Calgary,Alberta, Canada T2P 0M2 Tel:403-264-5610 Fax: 403-264-5898 Web: www.cspg.org Office hours: Monday to Friday, 8:30am to 4:00pm CONTENTS Business Manager:Tim Howard Email: [email protected] Office Manager: Deanna Watkins Email: [email protected] Communications Manager: Jaimè Croft Larsen Email: [email protected] ARTICLES Conventions Manager: Lori Humphrey-Clements Email: [email protected] CANADIAN INTERNATIONAL PETROLEUM CONFERENCE 2006 . .10 Corporate Relations Manager: Kim MacLean Email: [email protected] 2007 CALL FOR PHOTOS . 16 EDITORS/AUTHORS CSPG AWARDS – HONORARY MEMBERSHIP . 21, 23 Please submit RESERVOIR articles to the CSPG office. Submission deadline is the 23rd day of CSPG AWARDS – GRADUATE THESIS AWARDS . .26, 29 the month, two months prior to issue date. (e.g., January 23 for the March issue). CSPG AWARDS – PRESIDENT’S AWARD CITATION . 30 To publish an article, the CSPG requires digital CSPG OUTREACH – ADVANCES IN EARTH SCIENCES RESEARCH CONFERENCE . 38 copies of the document. Text should be in Microsoft Word format and illustrations should RENAME THE JOINT CONVENTION CONTEST . -

ARC Energy Investment Forum the Battle for the Hearts and Wheels of the Market

SPEAKER BIOGRAPHIES ARC Energy Investment Forum The Battle for the Hearts and Wheels of the Market Monday April 3, 2017 Heritage Park, Gasoline Alley Museum, Calgary, AB Explore the future of automotive technology and implications for investing KEYNOTE SPEAKERS Steve Koonin Larry Burns Peter Tertzakian New York, USA Detroit, USA Calgary, Canada Former US DOE Under Advisor to Google (now Waymo) Executive Director, Secretary and Current Director on Self Driving Cars and Former ARC Energy Research Institute of New York University’s Center Vice President of Research & for Urban Science and Progress Development for GM arcenergyinstitute.com/section/events #ARCForum ARC Energy Investment Forum The Battle for the Hearts and Wheels of the Market Monday April 3, 2017 Heritage Park, Gasoline Alley Museum, Calgary, AB Keynote Speakers: Steve Koonin (New York, USA) Former US DOE Under Secretary and Current Director of New York University’s (NYU) Center for Urban Science and Progress (CUSP) Steven E. Koonin was appointed as the founding Director of NYU’s CUSP in April 2012. That consortium of academic, corporate, and government partners will pursue research and education activities to develop and demonstrate informatics technologies for urban problems in the “living laboratory” of New York City. He previously served as the U.S. Department of Energy’s second Senate-confirmed Under Secretary for Science from May 19, 2009 through November 18, 2011. As Under Secretary for Science, Dr. Koonin functioned as the Department’s chief scientific officer, coordinating and overseeing research across the DOE. He led the preparation of the Department’s 2011 Strategic Plan and was the principal author of its Quadrennial Technology Review. -

CSEG 2008 ANNUAL REPORT 1 Executive Report

2008 CSEG ANNUAL REPORT 2008 Executive François Aubin, President Jon Downton, Vice President Petra Buziak, Director of Educational Services Jennifer Leslie-Panek, Assistant Director of Educational Services Marzena Feuchtwanger, Director of Member Services Torr Haglund, Assistant Director of Member Services Larry Herd, Director of Finance Brock Hassell, Assistant Director of Finance Michael Enachescu, Director of Communications Carol Laws, Assistant Director of Communications Doug Bogstie, Past President Jim Racette, Managing Director Canadian Society of Exploration Geophysicists 600, 640 - 8th Avenue SW, Calgary, Alberta T2P 1G7 Table of Contents Executive Reports President . 2 Vice-President . 3 Director of Educational Services . 4 Director of Member Services . 5 Director of Communications . 6 Director of Finance . 7 Managing Director . 7 Committee Reports Outreach . 8 The CSEG Foundation . 10 Scholarship . 10 CSEG / CSPG / CWLS National Joint Convention: C3GEO Back to Exploration . 12 RECORDER . 15 Website . 16 Doodlebug Golf Tournament . 17 DoodleSpiel . 18 Ski Spree . 19 Auditor’s Report . 20 Financial Statements . 21 Achievements . .27 Corporate Members . Back Cover CSEG 2008 ANNUAL REPORT 1 Executive Report President Year in review Association of Professional Engineers, between Outreach and the Foundation Geologists, and Geophysicists of Alberta are being reviewed to ensure maximum On March 30, 2009 the new CSEG (APEGGA) has regulated the practice of efficiency of all our activities and to Executive takes office. This will be the engineering, geology and geophysics in prevent duplication of efforts. end of my term as President of our Alberta since 1920. The Association’s society. To be President is a three-year authority is derived from provincial Elections minimum commitment: one year each as statute.” As part of this mandate, Vice President, President and Past APEGGA is actively involved in defining The voting for the CSEG executive President.