Annual Report to Shareholders

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Full Year Statutory Accounts

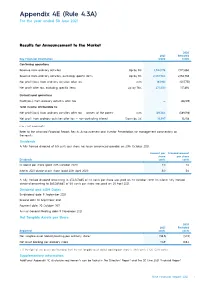

Appendix 4E (Rule 4.3A) For the year ended 30 June 2021 Results for Announcement to the Market 2020 2021 Restated Key Financial Information $’000 $’000 Continuing operations Revenue from ordinary activities Up by 8% 2,342,178 2,172,060 Revenue from ordinary activities, excluding specific items Up by 8% 2,332,984 2,156,785 Net profit/(loss) from ordinary activities after tax n/m 183,961 (507,751) Net profit after tax, excluding specific items Up by 76% 277,530 157,694 Discontinued operations Profit/(loss) from ordinary activities after tax — (66,189) Total income attributable to: Net profit/(loss) from ordinary activities after tax — owners of the parent n/m 169,364 (589,198) Net profit from ordinary activities after tax — non-controlling interest Down by 4% 14,597 15,258 n/m = not meaningful Refer to the attached Financial Report, Results Announcement and Investor Presentation for management commentary on the results. Dividends A fully franked dividend of 5.5 cents per share has been announced payable on 20th October 2021. Amount per Franked amount share per share Dividends cents cents Dividend per share (paid 20th October 2020) 2.0 2.0 Interim 2021 dividend per share (paid 20th April 2021) 5.0 5.0 A fully franked dividend amounting to $34,107,865 of 2.0 cents per share was paid on 20 October 2020. An interim fully franked dividend amounting to $85,269,663 of 5.0 cents per share was paid on 20 April 2021. Dividend and AGM Dates Ex-dividend date: 9 September 2021 Record date: 10 September 2021 Payment date: 20 October 2021 Annual General Meeting date: 11 November 2021 Net Tangible Assets per Share 2020 2021 Restated Reported cents cents Net tangible asset (deficit)/backing per ordinary share 1 (38.3) (40.9) Net asset backing per ordinary share 114.9 108.4 1. -

Presentation to Macquarie Conference

4 May 2021 ASX Markets Announcements Office ASX Limited 20 Bridge Street Sydney NSW 2000 PRESENTATION TO MACQUARIE CONFERENCE 4 May 2021: Attached is a copy of Nine’s presentation to the Macquarie Australia Conference 2021. Authorised for lodgment by Mike Sneesby, Chief Executive Officer. Further information: Nola Hodgson Victoria Buchan Head of Investor Relations Director of Communications +61 2 9965 2306 +61 2 9965 2296 [email protected] [email protected] nineforbrands.com.au Nine Sydney - 1 Denison Street, North Sydney, NSW, 2060 ABN 60 122 203 892 MIKE SNEESBY | CHIEF EXECUTIVE OFFICER Important Notice and Disclaimer as a result of reliance on this document. as a general guide only, and should not be relied on This document is a presentation of general as an indication or guarantee of future performance. background information about the activities of Nine Forward Looking Statements Forward looking statements involve known and unknown risks, uncertainty and other factors which Entertainment Co. Holdings Limited (“NEC”) current This document contains certain forward looking can cause NEC’s actual results to differ materially at the date of the presentation, (4 May 2021). The statements and comments about future events, from the plans, objectives, expectations, estimates information contained in this presentation is of including NEC’s expectations about the performance and intentions expressed in such forward looking general background and does not purport to be of its businesses. Forward looking statements can statements and many of these factors are outside complete. It is not intended to be relied upon as generally be identified by the use of forward looking the control of NEC. -

Sydney Program Guide

Page 1 of 42 Sydney Program Guide Sun Mar 14, 2021 06:00 EASY EATS Captioned HD WS G Nutritious & Delicious In this episode of Easy Eats, everything is gorgeous and guilt-free. Dishes like Lamb Stir Fry, Vegie Strudel, and Sweet Corn Soup are low in fat but high in flavour. There's even a low fat version of Hummingbird Cake which is perfect for those watching their waistline. 07:00 WEEKEND TODAY Captioned Live HD WS NA Join the Weekend Today team as they bring you the latest in news, current affairs, sports, politics, entertainment, fashion, health and lifestyle. 10:00 SPORTS SUNDAY Captioned Live HD WS PG Featuring Australia's leading sports personalities, Sports Sunday presents a frank and open debate about all the issues in the week of sport, with the promise of heated opinion and a few laughs along the way. 11:00 SUNDAY FOOTY SHOW Captioned Live HD WS PG Join hosts Peter Sterling, Erin Molan and Brad Fittler, with regular special guests to discuss all things NRL. 13:00 WOMEN'S FOOTY Captioned HD WS PG Join Bianca Chatfield for the 5th Season of Women's Footy for the latest news, opinion and analysis from in and around the AFLW - Each week, a raft of the AFLW's biggest names will join the show to discuss the weekend's action. 14:00 DAVID ATTENBOROUGH'S DYNASTIES Captioned Repeat HD WS PG The Making of Dynasties Follow five of the world's most celebrated, yet endangered animals: penguins, chimpanzees, lions, painted wolves and tigers, as they fight for their own survival and for the future of their dynasties. -

Deluxe Package

NSW DELUXE PACKAGE Unprecedented exposure for your premier property NSW DELUXE PACKAGE NSW DELUXE PACKAGE For the first time, Domain offers sellers this ultimate package – The cover of Domain in The Sydney Morning Herald and The Australian Financial Review, domain.com.au editorial exposure, a prime spot on the smh.com.au, domain.com.au, nine.com.au (NSW) 9news.com.au (NSW) homepages, plus extensive amplification through Domain’s leading social media platforms for your premier property. NSW DELUXE PACKAGE ELEMENTS Editorial • The cover of Domain in Saturday’s The SMH and Friday’s The AFR, plus cover story • Domain digital editorial article Magazine Advertising • Domain in The SMH and The AFR full page advertisement x 2 weeks • Domain Prestige in The AFR full page advertisement x 3 weeks Digital and Social Amplification • Domain Dream Homes on domain.com.au. smh.com.au, nine.com.au (NSW) and 9news.com.au (NSW) homepages • Listing showcased via Domain Facebook, Instagram and Twitter • Facebook Instant Experience INVESTMENT: $35,200 GST inclusive Cancellation of any portion of the NSW Deluxe Package that occurs after the first insertion / appearance date of any of the products outlined in the booking agreement will be billed at the total cost of the package. NSW Deluxe Packages are subject to availability. Editorial inclusion is subject to Editor approval. Online and magazine advertising terms and conditions: domain.com.au/group/agent-centre. Rates are for single resale properties only at the discretion of Domain and are not available for multiple dwelling buildings, projects or developments. Prices are subject to change without notice. -

Acmasphere Issue 62

acma investigations Broadcasting investigations, October to December 2010 � This summary is of ACMA broadcasting investigations completed in the three months from 1 October to 31 December 2010. There is also, with the cooperation of Free TV Australia and Commercial Radio Australia (CRA), a three-month report of the number and substance of complaints made directly to the commercial broadcasters. The broadcasting Complaints about possible breaches Most investigation reports (with the complaints process of program standards (children’s exception of community non-breach Primary responsibility for the resolution television, Australian content, captioning investigation reports) are published of broadcasting code-related and disclosure), provisions of the BSA on the ACMA website at complaints rests with the licensees. and licence conditions may be made www.acma.gov.au (go to About The Broadcasting Services Act 1992 directly to the ACMA. Complainants ACMA: Publications & research > (the BSA) lays down a general procedure are not obliged to contact a licensee Publications > Broadcasting publications for complaints-handling whereby a first in these instances. > Broadcasting investigations reports). complainant is required to approach a licensee first, who in turn is obliged The ACMA may find that a licensee to respond. has breached a broadcasting code of practice or a licensee may admit However, if a complainant does not to a breach of a code. Breaches of receive a response within 60 days, the codes are not breaches of the or considers the response received BSA, although the ACMA may make to be inadequate, the matter may then compliance with a code a condition be referred to the ACMA for investigation. -

Timber Lines

TIMBER LINES S VOL. VIII JUNE 19 THIRTY-YEAR CLUB R-6 FOREST SERVICE V TIMBER LINES NO. VIII - PUBLISHED NOW MD THEN 13Y R-6 THIRTY-YEAR CLUB - JUNEl9SL When things go wrong, as they sometimes will, When the road you're trudging seenis all up hill, Whe funds are low and the debts are high And you want to smile, but you have to sigh When care is pressing you doun a bit, Rest, if you must - but don't you quit. Success Is failure turned inside out, The silver tint on the clouds of doubt, And you never can tell how cl6se you are, It may be near when it seems afar; 'So stick to the fight when you're hardest hit - It'swhenthings seem worst that you niust'nt. quit.. Anonymous S .. :.:THE PURPOSE OF TIER LINES To provide a means of keeping the clib informed on matters of common interest, to provide a nidiuzn of communication between members, to assist in making real the objectives of our constitution arid to' provide a bridge to span the gap between membersinretirement arid those stillin active service. To these things we dedicate Timber Lines. Editor Ny greetings to the 30-Year Club with some notes of major happenings in F.Y. 1951i. The past year has been a busy one for Region Six. That's not new. There has never been a year since the Region was formed that has not been a busy one..This year our timber cut is up slightly. It is close to 2billionfeet, although prices are down and our receipts will be less than last year. -

Fairfax Media Ltd (Fxj) 16 August 2017

FAIRFAX MEDIA LTD (FXJ) 16 AUGUST 2017 RESULTS Full Year 2017 Full Year 2016 CHANGE Revenue ($m) 1,742.7 1830.5 -4.8% Bloomberg consensus ($m) 1,725.0 Domain EBITDA ($m) 113.1 120.0 -5.7% EBITDA ($m) 271.1 283.3 -4.3% Bloomberg consensus ($m) 263.8 Net profit (loss) after tax ($m) 83.9 (772.6) n/a Final Dividend ($) 0.02 0.02 no change Fairfax (FXJ) plans to spin-off Domain and trading to start in November Media group, Fairfax (FXJ) has returned to profitability, posting an improved $83.9m full year profit for the 12 months to June 30 and provided details on its planned Domain IPO. While underlying earnings (not including significant items) went backwards over the year, EBITDA came in ahead of market expectations. The result follows more than $900m in write-downs of its publishing assets which held back its FY16 result. While Domain has been its star performer for some time, its print business has been coming under pressure due to a slide in advertising dollars and a systemic change in the way Australians consume their news. FXJ confirmed it plans to spin-off its best performing asset, Domain and for trading in the real estate classifieds business to begin in mid to late November. The group intends to retain 60% of Domain with the remaining 40% to be distributed to FXJ shareholders. The split is still conditional on shareholder and regulatory approvals (including ASIC, ASX and ATO). Investors can expect the scheme booklet (which outlines all details of the separation) in late September 2017. -

Submission to the Inquiry Into Broadcasting, Online Content and Live Production to Rural and Regional Australia

SUBMISSION TO THE INQUIRY INTO BROADCASTING, ONLINE CONTENT AND LIVE PRODUCTION TO RURAL AND REGIONAL AUSTRALIA The Hon Bronwyn Bishop MP Chair Standing Committee on Communications and the Arts PO Box 6021 Parliament House CANBERRA ACT 2600 By email: [email protected] Introduction Thank you for the opportunity to make a submission to the House of Representatives Standing Committee on Communications and the Arts inquiry into broadcasting, online content and live production to rural and regional Australia. This letter is on behalf of the three major regional television providers, Prime Media Group (Prime Media), the WIN Network (WIN) and Southern Cross Austereo (SCA). Prime Media and SCA are members of Free TV Australia, the television peak body which has also made a submission to this inquiry on behalf of the industry. Prime Media broadcasts in northern New South Wales, southern New South Wales, the Australian Capital Territory, regional Victoria, Mildura, the Gold Coast area of south eastern Queensland and all of regional Western Australia. WIN broadcasts in southern New South Wales, the Australian Capital Territory, regional Queensland, regional Victoria, Tasmania, Griffith, regional WA, Mildura, Riverland and Mt Gambier in South Australia. SCA broadcasts in northern New South Wales, southern New South Wales, Queensland, the Australian Capital Territory, Griffith, regional Victoria, Tasmania, the Northern Territory and the Spencer Gulf region of South Australia. Through affiliation agreements, Prime Media, WIN and SCA purchase almost all of their programming from metropolitan networks1 and using more than 500 transmission towers located across the country, retransmit that programming into regional television licence areas. -

1 Transcript of 2019 Nine Entertainment AGM Sydney

1 Transcript of 2019 Nine Entertainment AGM Sydney, November 12, 2019 Chairman Peter Costello Good morning ladies and gentleman. As your Chairman, it's my pleasure to welcome you to the 2019 AGM of Nine Entertainment Company. My name is Peter Costello. Before opening the meeting, I refer you to the disclaimer here on the screen behind me and available through our ASX lodgement. It is now shortly after 10am and I am advised that this is a properly constituted meeting. There's a quorum of at least two shareholders present so I declare the 2019 Annual General Meeting open. Unless there are any objections, I propose to take the Notice of Meeting as read. Copies of the Notice of Meeting are available from the registration desk outside should you require them. Let me now introduce the people who are with us this morning. To my immediate left is Rachel Launders, our General Counsel and Company Secretary. Then Hugh Marks, our Chief Executive Officer, who will address the meeting a little later. Next to Hugh is Nick Falloon, the Independent, Non-Executive Director and Deputy Chair and Member of the People and Remuneration Committee. Then we have Patrick Alloway, Independent, Non-Executive Director and a member of the Audit and Risk Management Committee. Next to Patrick is Sam Lewis, Independent, Non-Executive Director, Chair of the Audit and Risk Committee and a Member of the People and Remuneration Committee. Then we have Mickie Rosen, Independent, Non-Executive Director. At the far end, we have Catherine West, Independent, Non-Executive Director, the Chair of the People and Remuneration Committee and a member of the Audit and Risk Committee. -

Master Thesis

University of Southern Queensland Faculty of COMMUNICATIONS FOR SMART GRID SUBSTATION MONITORING USING WIMAX PROTOCOL. A dissertation submitted by Sreekanth Anumula In fulfillment of the requirements of Courses ENG8411 and 8412 Research Project Master Thesis ABSTRACT The SMARTGRID is a general term for a series of infrastructural changes applied to the electric transmission and distribution systems. By using the latest communication and computing technology, additional options such as Condition Monitoring can now be implemented to further improve and optimise complex electricity supply grid operation. Lifecycle optimisation of high voltage assets and other system components in the utility provide a case in point. Today Utility experts agree that application of scheduled maintenance is not the effective use of resources. To reduce maintenance expenses and unnecessary outages and repairs of equipment due to scheduled maintenance, utilities are adopting condition based approaches. Real time online monitoring of substation parameters can be achieved by retrofitting the existing substation with SMARTGRID technology. The IEC 61850 is a common protocol meant for Substation Automation Systems, designed for the purpose of establishing interoperability, one that all manufacturers of all different assets must comply with. This thesis advocates the estimation of bandwidth required for monitoring a substation after retrofitting the existing substation with smart communication technologies. This includes establishing a latest wireless communication infrastructure from the substation to the control centre and evaluating the performance modelling and simulating the physical layer of communication technologies such as WIMAX (IEEE802.16) and MICROWAVE point to point using MATLAB SIMULINK and RADIO mobile online simulation software. Also, link budget of the satellite communication for the same application is calculated. -

Nine Network Australia Selects Intelsat to Distribute Domestic Television Programming

Nine Network Australia Selects Intelsat to Distribute Domestic Television Programming October 24, 2016 Intelsat will provide satellite connectivity and global fiber services via the IntelsatOne network to bring news content from around the world to Australia LUXEMBOURG--(BUSINESS WIRE)--Oct. 24, 2016-- Intelsat (NYSE: I), operator of the world’s first Globalized Network, powered by its leading satellite backbone, today announced a contract with Nine Network Australia to distribute programming to the company’s six domestic television stations as well as provide global satellite and fiber connectivity using the IntelsatOne terrestrial network to bring news content and special events from around the world to Australia for its network affiliates. Nine Network Australia (NNA) is one of the country’s top-rated commercial television networks, with local stations in Sydney, Melbourne, Brisbane, Adelaide, Perth and Darwin, along with a regional broadcaster, NBN. The network also has news bureaus in Canberra, London and Los Angeles. NNA is a subsidiary of Nine Entertainment Co., one of Australia’s leading media companies. Intelsat initially is providing services via the Australia/New Zealand Ku-Band beam on Intelsat 19 for the network’s broadcasting requirement. Under the agreement, Intelsat’s network support will extend well into the next decade. “Our Globalized Network allows us to meet NNA’s needs today and to increase our level of support if the network expands over time to meet the demands of multi-platform coverage,” said Terry Bleakley, Regional Vice President, Asia Pacific Sales, Intelsat. “NNA will also benefit from Intelsat’s global coverage for international contribution and distribution requirements.” NNA previously used Intelsat for its domestic and international occasional use requirements. -

Nine Response to Mr Anthony Klan

30 March 2021 Mr Nicholas Craft Standing Committee on Environment and Communications Department of the Senate PO Box 6100 Parliament House Canberra ACT 2600 Attention: Nicholas Craft By email: [email protected] Private & Confidential Dear Mr Craft Re: Inquiry into Media Diversity in Australia We refer to your email dated 16 March 2021 which attached Anthony Klan’s submission on Media Diversity in Australia. Nine denies the allegations contained in Mr Klan’s submissions, and in particular, Nine vehemently denies any allegation that Nine receives payment in return for favourable coverage or conversely payment for protecting individuals or companies from damaging media coverage. Nine maintains strong editorial independence across all of its platforms. Nine’s news, whether it be delivered by television, radio, print or online, is subject to the following standards which require editorial independence, disclosure of commercial arrangements, impartiality and accuracy: - Commercial Television Industry Code of Practice; - Commercial Radio Code of Practice; and - Australian Press Council Standards of Practice When Nine acquired the Fairfax publications (The Sydney Morning Herald, The Age, The Australian Financial Review, The Brisbane Times, WA Today), Nine agreed to commit to the Fairfax Media Charter of Editorial Independence at a Nine Board and Management level. This was confirmed in the materials publicly released by Fairfax as part of the scheme of arrangement under which Nine acquired Fairfax in 2018. There is no physical document which needs to be signed, to establish this commitment. This is something which I am instructed we have communicated to Mr Klan previously, and which he has failed to disclose in his submissions.