Annual Report 2016 Annual Report 2016 Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ethics Agreement in Order to Avoid Any Financial Conflict

Date: 7 .-e-•15 Iett..% 1--4 17 MEMORANDUM FOR THE RECORD SUBJECT: Ethics Agreement In order to avoid any financial conflict of interest in violation of 18 U.S.C. § 208(a) or the appearance of a financial conflict of interest as defined in the Standards of Ethical Conduct for Employees of the Executive Branch, 5 C.F.R. § 2635.502, and to adhere to the Ethics Pledge instituted by Executive Order 13770 issued on January 28, 2017, and entitled "Ethics Commitments by Executive Branch Appointees" (the Ethics Pledge), I am issuing the following statement. I understand that as an appointee I must sign the Ethics Pledge and that I will be bound by the requirements and restrictions therein even if not specifically mentioned in this or any other ethics agreement. Before beginning my covered Federal position, I resigned from my non-Federal positions with the Association of State and Territorial Health Officials (ASTHO) and the State of Georgia on July 6, 2017. Pursuant to the Ethics Pledge, I will not, for a period of two years from the date of my appointment to my covered Federal position, participate in an official capacity in any particular matter involving specific parties that is directly and substantially related to ASTHO, unless an exception applies or I am granted a waiver. I understand that this provision in the Ethics Pledge does not apply to state government entities, including the State of Georgia. Even when the two-year restriction of the Ethics Pledge does not apply, under 5 C.F.R. § 2635.502, I will not, for a period of one year from the date of my resignation from ASTHO and the State of Georgia, participate in any particular matter involving specific parties in which ASTHO or the State of Georgia is a party or represents a party, unless I am first authorized to participate, pursuant to 5 C.F.R. -

Corporate Governance

Strategic report Governance and remuneration Financial statements Investor information Corporate Governance In this section Chairman’s Governance statement 78 The Board 80 Corporate Executive Team 83 Board architecture 85 Board roles and responsibilities 86 Board activity and principal decisions 87 Our purpose, values and culture 90 The Board’s approach to engagement 91 Board performance 94 Board Committee information 96 Our Board Committee reports 97 Section 172 statement 108 Directors’ report 109 GSK Annual Report 2020 77 Chairman’s Governance statement In last year’s Governance statement, I explained that our primary Education and focus on Science objective for 2020 was to ensure there was clarity between the Given the critical importance of strengthening the pipeline, Board and management on GSK’s execution of strategy and its the Board has benefitted from devoting a higher proportion of operational priorities. We have aligned our long-term priorities its time in understanding the science behind our strategy and of Innovation, Performance and Trust powered by culture testing its application. It is important that the Board has a and agreed on the metrics to measure delivery against them. working understanding of the key strategic themes upon The Board’s annual cycle of meetings ensures that all major which our R&D strategy is based. These themes have been components of our strategy are reviewed over the course complemented by Board R&D science thematic deep dives. of the year. Our focus was on the fundamentals of our strategy: human The COVID-19 pandemic impacted and dominated all our genetics, the immune system and AI and ML, as well as to lives for the majority of 2020. -

TARGET PORTFOLIO TRUST Form N-PX Filed 2017-08-30

SECURITIES AND EXCHANGE COMMISSION FORM N-PX Annual report of proxy voting record of registered management investment companies filed on Form N-PX Filing Date: 2017-08-30 | Period of Report: 2017-06-30 SEC Accession No. 0000067590-17-000961 (HTML Version on secdatabase.com) FILER TARGET PORTFOLIO TRUST Mailing Address Business Address 655 BROAD STREET 655 BROAD STREET CIK:890339| IRS No.: 137000899 | State of Incorp.:DE | Fiscal Year End: 1031 17TH FLOOR 17TH FLOOR Type: N-PX | Act: 40 | File No.: 811-07064 | Film No.: 171060626 NEWARK NJ 07102 NEWARK NJ 07102 9738026469 Copyright © 2017 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document United States Securities and Exchange Commission Washington, DC 20549 FORM N-PX ANNUAL REPORT OF PROXY VOTING RECORD OF REGISTERED MANAGEMENT INVESTMENT COMPANY Investment Company Act file number: 811-07064 The Target Portfolio Trust (Exact name of registrant as specified in charter) 655 Broad Street 17th Floor Newark, NJ 07102 (Address of principal executive offices) (Zip code) Jonathan D. Shain, Esquire 655 Broad Street 17th Floor Newark, NJ 07102 (Name and address of agent for service) Registrant’s telephone number, including area code: 973-802-6469 Date of fiscal year end: July 31 Date of reporting period: 7/1/2016 through 6/30/2017 Copyright © 2017 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document Item 1. Proxy Voting Record. In determining votes against management, any ballot that management did not make a recommendation is considered to be "FOR" regardless of the vote cast. -

Annual Report and Accounts 2019

IMPERIAL BRANDS PLC BRANDS IMPERIAL ANNUAL REPORT AND ACCOUNTS 2019 ACCOUNTS AND REPORT ANNUAL ANNUAL REPORT AND ACCOUNTS 2019 OUR PURPOSE WE CAN I OWN Our purpose is to create something Everything See it, seize it, is possible, make it happen better for the world’s smokers with together we win our portfolio of high quality next generation and tobacco products. In doing so we are transforming WE SURPRISE I AM our business and strengthening New thinking, My contribution new actions, counts, think free, our sustainability and value creation. exceed what’s speak free, act possible with integrity OUR VALUES Our values express who we are and WE ENJOY I ENGAGE capture the behaviours we expect Thrive on Listen, challenge, share, make from everyone who works for us. make it fun connections The following table constitutes our Non-Financial Information Statement in compliance with Sections 414CA and 414CB of the Companies Act 2006. The information listed is incorporated by cross-reference. Additional Non-Financial Information is also available on our website www.imperialbrands.com. Policies and standards which Information necessary to understand our business Page Reporting requirement govern our approach1 and its impact, policy due diligence and outcomes reference Environmental matters • Occupational health, safety and Environmental targets 21 environmental policy and framework • Sustainable tobacco programme International management systems 21 Climate and energy 21 Reducing waste 19 Sustainable tobacco supply 20 Supporting wood sustainability -

Tobacco Deal Sealed Prior to Global Finance Market Going up in Smoke

marketwatch KEY DEALS Tobacco deal sealed prior to global finance market going up in smoke The global credit crunch which so rocked £5.4bn bridging loan with ABN Amro, Morgan deal. “It had become an auction involving one or Iinternational capital markets this summer Stanley, Citigroup and Lehman Brothers. more possible white knights,” he said. is likely to lead to a long tail of negotiated and In addition it is rescheduling £9.2bn of debt – Elliott said the deal would be part-funded by renegotiated deals and debt issues long into both its existing commitments and that sitting on a large-scale disposal of Rio Tinto assets worth the autumn. the balance sheet of Altadis – through a new as much as $10bn. Rio’s diamonds, gold and But the manifestation of a bad bout of the facility to be arranged by Citigroup, Royal Bank of industrial minerals businesses are now wobbles was preceded by some of the Scotland, Lehmans, Barclays and Banco Santander. reckoned to be favourites to be sold. megadeals that the equity market had been Finance Director Bob Dyrbus said: Financing the deal will be new underwritten expecting for much of the last two years. “Refinancing of the facilities is the start of a facilities provided by Royal Bank of Scotland, One such long awaited deal was the e16.2bn process that is not expected to complete until the Deutsche Bank, Credit Suisse and Société takeover of Altadis by Imperial Tobacco. first quarter of the next financial year. Générale, while Deutsche and CIBC are acting as Strategically the Imps acquisition of Altadis “Imperial Tobacco only does deals that can principal advisors on the deal with the help of has been seen as the must-do in a global generate great returns for our shareholders and Credit Suisse and Rothschild. -

To Arrive at the Total Scores, Each Company Is Marked out of 10 Across

BRITAIN’S MOST ADMIRED COMPANIES THE RESULTS 17th last year as it continues to do well in the growing LNG business, especially in Australia and Brazil. Veteran chief executive Frank Chapman is due to step down in the new year, and in October a row about overstated reserves hit the share price. Some pundits To arrive at the total scores, each company is reckon BG could become a take over target as a result. The biggest climber in the top 10 this year is marked out of 10 across nine criteria, such as quality Petrofac, up to fifth from 68th last year. The oilfield of management, value as a long-term investment, services group may not be as well known as some, but it is doing great business all the same. Its boss, Syrian- financial soundness and capacity to innovate. Here born Ayman Asfari, is one of the growing band of are the top 10 firms by these individual measures wealthy foreign entrepreneurs who choose to make London their operating base and home, to the benefit of both the Exchequer and the employment figures. In fourth place is Rolls-Royce, one of BMAC’s most Financial value as a long-term community and environmental soundness investment responsibility consistent high performers. Hardly a year goes past that it does not feature in the upper reaches of our table, 1= Rightmove 9.00 1 Diageo 8.61 1 Co-operative Bank 8.00 and it has topped its sector – aero and defence engi- 1= Rotork 9.00 2 Berkeley Group 8.40 2 BASF (UK & Ireland) 7.61 neering – for a decade. -

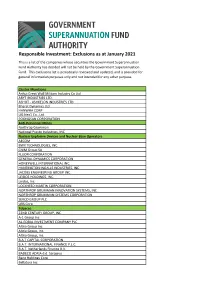

2021 01 GSF Website Version and Format.Xlsx

Responsible Investment: Exclusions as at January 2021 This is a list of the companies whose securities the Government Superannuation Fund Authority has decided will not be held by the Government Superannuation Fund. This exclusions list is periodically reviewed and updated, and is provided for general information purposes only and not intended for any other purpose. Cluster Munitions Anhui Great Wall Military Industry Co Ltd ARYT INDUSTRIES LTD. ASHOT ‐ ASHKELON INDUSTRIES LTD. Bharat Dynamics Ltd HANWHA CORP LIG Nex1 Co., Ltd. POONGSAN CORPORATION Anti‐Personnel Mines Northrop Grumman National Presto Industries, INC Nuclear Explosive Devices and Nuclear Base Operators AECOM BWX TECHNOLOGIES, INC. CNIM Group SA FLUOR CORPORATION GENERAL DYNAMICS CORPORATION HONEYWELL INTERNATIONAL INC. HUNTINGTON INGALLS INDUSTRIES, INC. JACOBS ENGINEERING GROUP INC. LEIDOS HOLDINGS, INC. Leidos, Inc. LOCKHEED MARTIN CORPORATION NORTHROP GRUMMAN INNOVATION SYSTEMS, INC. NORTHROP GRUMMAN SYSTEMS CORPORATION SERCO GROUP PLC URS Corp Tobacco 22ND CENTURY GROUP, INC. A‐1 Group Inc AL‐EQBAL INVESTMENT COMPANY PLC Altria Group Inc Altria Group, Inc. Altria Group, Inc. B.A.T CAPITAL CORPORATION B.A.T. INTERNATIONAL FINANCE P.L.C. B.A.T. Netherlands Finance B.V. BADECO ADRIA d.d. Sarajevo Bang Holdings Corp Bellatora Inc Tobacco continued Bots Inc BRITISH AMERICAN TOBACCO (MALAYSIA) BERHAD BRITISH AMERICAN TOBACCO BANGLADESH CO. LTD. British American Tobacco Holdings (The Netherlands) B.V. British American Tobacco Kenya plc BRITISH AMERICAN TOBACCO P.L.C. BRITISH AMERICAN TOBACCO P.L.C. British American Tobacco Uganda British American Tobacco Vranje a.d. Vranje British American Tobacco Zambia PLC British American Tobacco Zimbabwe (Holdings) Ltd Bulgartabac holding AD Carreras Ltd Cerealcom SA Alexandria CEYLON TOBACCO COMPANY PLC China Boton Group Company Limited Coka Duvanska Industrija ad Coka CONG TY CO PHAN NGAN SON CTO Public Company Ltd Duvanska industrija ad Bujanovac Eastern Company SAE ELECTRONIC CIGARETTES INTERNATIONAL GROUP, LTD. -

British American Tobacco's Submission to the WHO's

British American Tobacco’s submission to the WHO’s Framework Convention on Tobacco Control This is the submission of the British American Tobacco group of companies commenting on the WHO’s Framework Convention on Tobacco Control. We are the world’s most international tobacco group with an active presence in 180 countries. Our companies sell some of the world’s best known brands including Dunhill, Kent, State Express 555, Lucky Strike, Benson & Hedges, Rothmans and Pall Mall. Executive summary • The WHO’s proposed ‘Framework Convention on Tobacco Control’ is fundamentally flawed and will not achieve its objectives. • The tobacco industry, along with other industries involved in the manufacture and distribution of legal but risky products, is the subject of considerable public attention. It is important that the debate about tobacco remains open, objective, constructive and free from opportunistic criticism if we are effectively to address the real issues associated with tobacco. • British American Tobacco is responsible tobacco. We seek to operate in partnership with governments, who are significant stakeholders in our business, and other interested parties, based on our open acknowledgement that we make a risky product and therefore support sensible regulation. • British American Tobacco shares the World Health Organisation’s desire to reduce the health impact of tobacco use. This paper outlines British American Tobacco’s proposal for the sensible regulation of tobacco. • Our proposal will relieve the WHO of the cost and bureaucracy involved in its wish to become a single global tobacco regulator, leaving it free to do what it should be doing – policy orientation. Some facts about tobacco • Today over one billion adults, about one third of the world’s adult population, choose to smoke. -

FY 2020 Announcement.Pdf

17 February 2021 –PRELIMINARY RESULTS BRITISH AMERICAN TOBACCO p.l.c. YEAR ENDED 31 DECEMBER 2020 ‘ACCELERATING TRANSFORMATION’ GROWTH IN NEW CATEGORIES AND GROUP EARNINGS DESPITE COVID-19 PERFORMANCE HIGHLIGHTS REPORTED ADJUSTED Current Vs 2019 Current Vs 2019 rates Rates (constant) Cigarette and THP volume share +30 bps Cigarette and THP value share +20 bps Non-Combustibles consumers1 13.5m +3.0m Revenue (£m) £25,776m -0.4% £25,776m +3.3% Profit from operations (£m) £9,962m +10.5% £11,365m +4.8% Operating margin (%) +38.6% +380 bps +44.1% +100 bps2 Diluted EPS (pence) 278.9p +12.0% 331.7p +5.5% Net cash generated from operating activities (£m) £9,786m +8.8% Free cash flow after dividends (£m) £2,550m +32.7% Cash conversion (%)2 98.2% -160 bps 103.0% +650 bps Borrowings3 (£m) £43,968m -3.1% Adjusted Net Debt (£m) £39,451m -5.3% Dividend per share (pence) 215.6p +2.5% The use of non-GAAP measures, including adjusting items and constant currencies, are further discussed on pages 48 to 53, with reconciliations from the most comparable IFRS measure provided. Note – 1. Internal estimate. 2. Movement in adjusted operating margin and operating cash conversion are provided at current rates. 3. Borrowings includes lease liabilities. Delivering today Building A Better TomorrowTM • Revenue, profit from operations and earnings • 1 growth* absorbing estimated 2.5% COVID-19 revenue 13.5m consumers of our non-combustible products , headwind adding 3m in 2020. On track to 50m by 2030 • New Categories revenue up 15%*, accelerating • Combustible revenue -

Companies Subject to Exclusion

Opdateret 01-08-2021 Vellivs Ekslusionsliste Velliv ønsker ikke at investere i selskaber, som bryder med Vellivs ESG-kriterier fastlagt i politikken for ansvarlig investering og aktivt ejerskab og som ikke udviser forandringsvilje i forhold til deres håndtering af ESG-risici. Endelig ønsker Velliv ikke at investere i tobaksselselskaber, selskaber med aktivteter i kontroversielle våben eller selskaber, hvor mere end 5 pct. af omsætningen stammer fra udvinding af kul og oliesand. Selsakb Kommentar 22nd Century Group, Inc. Tobacco AECOM Contr.Weapons Aerojet Rocketdyne Holdings, Inc. Contr.Weapons Aerojet Rocketdyne, Inc. Contr.Weapons Aeroteh SA Contr.Weapons Airbus SE Contr.Weapons Al-Eqbal Co. for Investment Plc Tobacco ALLETE, Inc. Kul Alliance Holdings GP LP Coal Alliance Resource Operating Partners LP Coal Alliance Resource Partners LP Coal Alpha Metallurgical Resources, Inc Coal Alpha Natural Resources Inc Coal Altadis Emisiones Financieras SA Tobacco Altadis SA Tobacco AltaGas Ltd. Gas/ESG Altius Minerals Corporation Coal Altria Group, Inc. Tobacco Anglo American plc Kul Anglo Pacific Group plc Coal Arch Resources, Inc. Coal Arcis Resources Corp. Tobacco Aryt Industries Ltd. Contr.Weapons Asenovgrad Tabac AD Tobacco Ashtrom Group Ltd. Normviolation>human rights Athabasca Oil Corporation Oilsand Avco Corp. Contr.Weapons B.A.T. Capital Corp. Tobacco B.A.T. Finance BV Tobacco B.A.T. International Finance Plc Tobacco Babcock International Group plc Contr.Weapons BADECO ADRIA dd Tobacco BAE Systems (Finance) Ltd. Contr.Weapons BAE Systems plc Contr.Weapons Bat Brasil Tobacco Bathurst Resources Limited Coal Baytex Energy (LP) Ltd. Oilsand Baytex Energy Corp. Oilsand Bellatora, Inc. Tobacco BHP Group Limited Kul BHP Group Plc Kul BlackPearl Resources, Inc. -

Local Business Database Local Business Database: Alphabetical Listing

Local Business Database Local Business Database: Alphabetical Listing Business Name City State Category 111 Chop House Worcester MA Restaurants 122 Diner Holden MA Restaurants 1369 Coffee House Cambridge MA Coffee 180FitGym Springfield MA Sports and Recreation 202 Liquors Holyoke MA Beer, Wine and Spirits 21st Amendment Boston MA Restaurants 25 Central Northampton MA Retail 2nd Street Baking Co Turners Falls MA Food and Beverage 3A Cafe Plymouth MA Restaurants 4 Bros Bistro West Yarmouth MA Restaurants 4 Family Charlemont MA Travel & Transportation 5 and 10 Antique Gallery Deerfield MA Retail 5 Star Supermarket Springfield MA Supermarkets and Groceries 7 B's Bar and Grill Westfield MA Restaurants 7 Nana Japanese Steakhouse Worcester MA Restaurants 76 Discount Liquors Westfield MA Beer, Wine and Spirits 7a Foods West Tisbury MA Restaurants 7B's Bar and Grill Westfield MA Restaurants 7th Wave Restaurant Rockport MA Restaurants 9 Tastes Cambridge MA Restaurants 90 Main Eatery Charlemont MA Restaurants 90 Meat Outlet Springfield MA Food and Beverage 906 Homwin Chinese Restaurant Springfield MA Restaurants 99 Nail Salon Milford MA Beauty and Spa A Child's Garden Northampton MA Retail A Cut Above Florist Chicopee MA Florists A Heart for Art Shelburne Falls MA Retail A J Tomaiolo Italian Restaurant Northborough MA Restaurants A J's Apollos Market Mattapan MA Convenience Stores A New Face Skin Care & Body Work Montague MA Beauty and Spa A Notch Above Northampton MA Services and Supplies A Street Liquors Hull MA Beer, Wine and Spirits A Taste of Vietnam Leominster MA Pizza A Turning Point Turners Falls MA Beauty and Spa A Valley Antiques Northampton MA Retail A. -

Tobacco Securitization

Memorandum Office of Jenine Windeshausen Treasurer-Tax Collector To: The Board of Supervisors From: Jenine Windeshausen, Treasurer-Tax Collector Date: October 27, 2020 Subject: Tobacco Securitization Action Requested a) Adopt a resolution consenting to the issuance and sale by the California County Tobacco Securitization Agency not to exceed $67,000,000 initial principal amount of tobacco settlement bonds (Gold Country Settlement Funding Corporation) Series 2020 Bonds in one or more series and other related matters; authorizing the execution and delivery by the county of a certificate of the county; and authorizing the execution and delivery of and approval of other related documents and actions in connection therewith. b) Direct that eligible proceeds from the Series 2020 Bonds be expended on infrastructure improvements at the Placer County Government Center, construction of the Health and Human Services Building and other Board approved capital facilities projects. Background October 6, 2020 Board of Supervisors Meeting Summary. Your Board received an update regarding the County’s prior tobacco securitizations and information on the potential to refund the Series 2006 Bonds to receive additional proceeds for capital projects. Based on that update, the Board requested the Treasurer to return to the Board on October 27, 2020 with a resolution approving documents and other matters to proceed with refunding the Series 2006 Bonds. In summary from the October 6, 2020 meeting, the County receives annual payments in perpetuity from the 1998 Master Settlement Agreement (MSA). The MSA payments are derived from a percentage of cigarette sales. Placer County issued bonds in 2002 and 2006 to securitize a share of its MSA payments.