Portfolio Update

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

June 2011 Yearly Report

Alleron Investment Management Limited Yearly Report June 2011 Portfolio performance and attribution analysis Market commentary Portfolio commentary Since Inception (Annualised) Year to Date Global markets were lead, over Positives: financial year, by the strong per- CEU: The company’s revenue such Portfolio +10.297% +4.468% formance of the US market which that cash flow now funds their dis- Benchmark + 6.158% +11.503% responded strongly to Federal Re- tribution and reduces their risk pro- serve Bank policy of a second round file. Top 3 and bottom 3 performing stocks of quantitative easing. This along AXA: The stock price was sup- Top 3: ConnectEast Group (CEU), AXA Asia Pacific Holdings with continued government spend- (AXA), Oil Search (OSH). ported by the accepted takeover ing allowed the US economy and offer from AMP and AXA SA. company earnings to maintain Bottom 3: Seven West Media Limited (SWM), Resmed Inc. (RMD), growth into the beginning of 2011. OSH: The company has secured Computershare (CPU). While growth in the US continued, offtake agreements to their LNG European countries were besieged output which remains on schedule. Portfolio changes by the familiar problem of periph- Negatives: Stocks joined or increased significantly: eral nation debt and increased risks of sovereign debt default. Contrar- SWM: Company earnings were hurt Downer Limited (+2.25% New Stock): An Engineering and Contract- ily, strong activity in emerging by weak advertising activity from ing company. The company has developed a strong order book pro- economies has forced monetary uncertainly over the resource tax. viding significant growth potential and has cleared the way to success- authorities there to tighten policy to RMD: Earnings translation was hurt fully complete troubled contracts. -

Code Security Description ARI Arrium Ltd AWC Alumina Ltd AWE AWE

10-Sep-15 Australian Resources Index Trust NTA & Allotment Notice The manager of the Australian Resources Index Trust advises that as at close of business on 9 September 2015 a total of Nil units has been redeemed or allotted since 8 September 2015. The total number of units on issue on that day was 6,091,647. The asset backing for each ASR unit at close of business (Sydney) on 9 September 2015 was $3.25876 (NTA is net of applicable tax liability). The tracking difference was 1.03% Please note Basket applications and redemptions will be unavailable from Wednesday 09 September 2015 to Friday 25 September 2015. Basket applications and redemptions will resume on Monday 28 September 2015. The following companies are currently in the Fund: Code Security description ARI Arrium Ltd AWC Alumina Ltd AWE AWE Ltd BHP BHP Billiton Ltd BPT Beach Energy Limited BSL Bluescope Steel Ltd CTX Caltex Australia Ltd DLS Drillsearch Energy Ltd EVN Evolution Mining Ltd FMG Fortescue Metals Group IGO Independence Group NL ILU Iluka Resources Ltd KAR Karoon Gas Australia Limited LNG Liquefied Natural Gas Limited NCM Newcrest Mining Ltd NST Northern Star Resources Ltd ORG Origin Energy Ltd OSH Oil Search Ltd OZL OZ Minerals Limited PDN Paladin Energy Ltd. RIO Rio Tinto Ltd RRL Regis Resources Ltd S32 South32 Limited SFR Sandfire Resources NL SGM Sims Metal Management Ltd SIR Sirius Resources NL STO Santos Ltd SXY Senex Energy Limited SYR Syrah Resources Limited WHC Whitehaven Coal Ltd WOR WorleyParsons Ltd WPL Woodside Petroleum Ltd WSA Western Areas Ltd For further information please contact: Smartshares Limited 0800 80 87 80 [email protected]. -

Monthly NTA and Performance Update

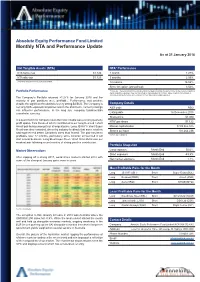

Absolute Equity Performance Fund Limited Monthly NTA and Performance Update As at 31 January 2018 Net Tangible Assets (NTA) NTA* Performance NTA before tax $1.122 1 month 1.27% NTA after tax $1.123 3 months 2.59% $ currency notation refers to Australian Dollars. 12 months 16.02% Since inception (annualised) 3.52% Portfolio Performance *Before tax. These calculations are unaudited and intended to illustrate the performance of the investment portfolio minus corporate expenses. They are calculated on a pre-dividend NTA basis. ‘Since inception (annualised)’ is annualised NTA performance since listing at $1.065 after listing related expenses The Company’s Portfolio returned +1.27% for January 2018 and the majority of pair positions were profitable. Performance was positive despite the significant headwind of a very strong $A/$US. The Company is Company Details net long $US-exposed companies and in the short term, currency swings ASX code AEG can influence performance. In the long run, company fundamentals overwhelm currency. Listing date 16 December 2015 Share price $1.080 In a quiet month for company news the most notable was a strong quarterly NTA* per share $1.122 profit update from Resmed which contributed to our long Resmed / short Ansell pair being amongst our strongest pairs. Long JB Hi-Fi / short Super Market capitalisation $109,365,375 Retail was also rewarded, driven by industry feedback that some retailers Shares on Issue 101,264,236 had experienced better Christmas sales than feared. The pair has been profitable over 12 months, particularly since Amazon announced it will *Before tax ex-dividend start a local business. -

June 2019 42

y 4 6 Equit 2019 June High Conviction High Quarterly NewsletterQuarterly No. Selector Fund In this quarterly edition, we review performance and attribution for the quarter. We highlight the importance of innovation and culture within organisations and profile ResMed and Cochlear, two leading healthcare businesses. We visit Fisher & Paykel Healthcare in New Zealand and look at one of the biggest growth industries in the world today, cyber security. Photo. Selector analyst trekking through the Atlas Mountains and local Berber kids. Selector Funds Management Limited ACN 102756347 AFSL 225316 Level 8, 10 Bridge Street Sydney NSW 2000 Australia Tel 612 8090 3612 www.selectorfund.com.au P Selector is a boutique fund manager. Our team, combined, have over 150 years of experience in financial markets. We believe in long-term wealth creation and building lasting relationships with our investors. We focus on stock selection, the funds are high conviction, concentrated and index unaware. As a result, the portfolios have low turnover and produce tax effective returns. Selector has a 15-year track record of outperformance and we continue to seek businesses with leadership qualities, run by competent management teams, underpinned by strong balance sheets and with a focus on capital management. Selector High Conviction Equity Fund Quarterly Newsletter #64 CONTENTS IN BRIEF – JUNE QUARTER 3 PORTFOLIO OVERVIEW 5 PORTFOLIO CONTRIBUTORS 7 MARKET INSIGHTS AND OBSERVATIONS 13 INNOVATION + CULTURE = SUCCESS 17 RESMED INC. 20 WAKE-UP CALL 31 FISHER & PAYKEL HEALTHCARE – JUNE 2019 42 RISK OUT…UPFRONT 45 COMPANY VISIT DIARY – JUNE 2019 QUARTER 57 2 Selector Funds Management IN BRIEF – JUNE QUARTER Dear Investor, Looking back on 2019, it would be fair to say that few identify the businesses we want to own on a case by case foresaw how the events of the financial year would basis, understand them to the best of our abilities and unfold. -

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

Asx Clear – Acceptable Collateral List 28

et6 ASX CLEAR – ACCEPTABLE COLLATERAL LIST Effective from 20 September 2021 APPROVED SECURITIES AND COVER Subject to approval and on such conditions as ASX Clear may determine from time to time, the following may be provided in respect of margin: Cover provided in Instrument Approved Cover Valuation Haircut respect of Initial Margin Cash Cover AUD Cash N/A Additional Initial Margin Specific Cover N/A Cash S&P/ASX 200 Securities Tiered Initial Margin Equities ETFs Tiered Notes to the table . All securities in the table are classified as Unrestricted (accepted as general Collateral and specific cover); . Specific cover only securities are not included in the table. Any securities is acceptable as specific cover, with the exception of ASX securities as well as Participant issued or Parent/associated entity issued securities lodged against a House Account; . Haircut refers to the percentage discount applied to the market value of securities during collateral valuation. ASX Code Security Name Haircut A2M The A2 Milk Company Limited 30% AAA Betashares Australian High Interest Cash ETF 15% ABC Adelaide Brighton Ltd 30% ABP Abacus Property Group 30% AGL AGL Energy Limited 20% AIA Auckland International Airport Limited 30% ALD Ampol Limited 30% ALL Aristocrat Leisure Ltd 30% ALQ ALS Limited 30% ALU Altium Limited 30% ALX Atlas Arteria Limited 30% AMC Amcor Ltd 15% AMP AMP Ltd 20% ANN Ansell Ltd 30% ANZ Australia & New Zealand Banking Group Ltd 20% © 2021 ASX Limited ABN 98 008 624 691 1/7 ASX Code Security Name Haircut APA APA Group 15% APE AP -

Balanced Style Investing — Winning by Not Losing September 2020

Insights Active Quantitative Equity (AQE) Balanced Style Investing — Winning by Not Losing September 2020 Bruce Apted Head of Portfolio Management Australia Active Quantitative Equity Human emotions and biases affect all investors. Left unchecked, these emotions can sabotage financial decisions and generate suboptimal investment outcomes. However, by understanding how human emotions and behaviour impacts our decision making we can unlock opportunities for investors. The key to unlocking these opportunities is: • understanding how financial markets interact with human behaviour; and • finding an investment style to exploit these biases. Emotions are the Financial markets have the ability to generate and destroy wealth. They are complex and Enemy for Investors volatile and evoke significant emotions. Figure 1 depicts an all too common emotional roller coaster for investors. The worst case scenario is letting your emotions drive your investment decisions — buying a security near the high or capitulating and selling near the low. How can investors avoid the mistakes of mass psychology and turn emotional short comings into opportunity? Be risk averse when the market is overly optimistic (Euphoria) and risk seeking when the market is overly pessimistic (Panic and Capitulation). 10 Figure 1 Euphoria Market Becomes Expensive — Greatest Financial Risk The Emotional Roller Coaster of Investing 8 Thrill Anxiety Denial Excitment 6 Fear Optimism Optimism 4 Panic Relief 2 Hope Market Becomes Cheap — Greatest Financial Opportunity Capitulation Depression 0 1 2 3 4 5 6 7 8 9 10 11 12 13 Source: State Street Global Advisors. The information contained above is for illustrative purposes only. Over the last 20 years, there are many examples of Euphoria followed by Fear and Capitulation (see Figure 2). -

(ASX100) Women on Boards Analysis

Australia/NZ | Australia Thematic Investing (Citi) Equities 18 August 2011 │ 32 pages ESG: ASX100 Women on Board Analysis Increasing Focus on Board Diversity Women on Boards of ASX100 Companies — The ASX Corporate Governance Council’s new principles and recommendations on diversity commenced on 1 January Elaine Prior 2011. This is likely to lead to increasing focus on companies’ approaches to diversity +61-2-8225-4891 issues, including female representation on company boards. This report looks at data [email protected] on women directors on ASX100 company boards. The number of women directors has Felipe Faria increased, particularly in recent months (Figure 5 to Figure 8). Board diversity may [email protected] enhance effectiveness, by providing a wider range of perspectives and knowledge. Women on Boards Data — We collected and analysed data on female board directors of S&P/ASX100 companies from FY08 to 8 August 2011 (Figure 5 to Figure 9). At 8 August 2011 there were 134 women on ASX100 boards, a 46% increase from FY08. ASX100 companies with no female board directors were AQP, CQO, EGP, FMG, IPL, JHX, LEI, LYC, OSH, PDN, PRY, RHC, RMD, SGM and SWM. Companies with three female directors (the highest number identified) are AMP, BEN, CBA, MQG, QAN, QBE and WBC. Seven female directors each currently hold three ASX100 directorships. Business Case for Gender Diversity — Reibey Institute research found that those ASX500 companies with women directors on 30 June 2010 had a 3-year return on equity (ROE) 10.7% higher than those without any women directors. The 5-year ROE was 11.1% higher. -

Stoxx® Pacific Total Market Index

STOXX® PACIFIC TOTAL MARKET INDEX Components1 Company Supersector Country Weight (%) CSL Ltd. Health Care AU 7.79 Commonwealth Bank of Australia Banks AU 7.24 BHP GROUP LTD. Basic Resources AU 6.14 Westpac Banking Corp. Banks AU 3.91 National Australia Bank Ltd. Banks AU 3.28 Australia & New Zealand Bankin Banks AU 3.17 Wesfarmers Ltd. Retail AU 2.91 WOOLWORTHS GROUP Retail AU 2.75 Macquarie Group Ltd. Financial Services AU 2.57 Transurban Group Industrial Goods & Services AU 2.47 Telstra Corp. Ltd. Telecommunications AU 2.26 Rio Tinto Ltd. Basic Resources AU 2.13 Goodman Group Real Estate AU 1.51 Fortescue Metals Group Ltd. Basic Resources AU 1.39 Newcrest Mining Ltd. Basic Resources AU 1.37 Woodside Petroleum Ltd. Oil & Gas AU 1.23 Coles Group Retail AU 1.19 Aristocrat Leisure Ltd. Travel & Leisure AU 1.02 Brambles Ltd. Industrial Goods & Services AU 1.01 ASX Ltd. Financial Services AU 0.99 FISHER & PAYKEL HLTHCR. Health Care NZ 0.92 AMCOR Industrial Goods & Services AU 0.91 A2 MILK Food & Beverage NZ 0.84 Insurance Australia Group Ltd. Insurance AU 0.82 Sonic Healthcare Ltd. Health Care AU 0.82 SYDNEY AIRPORT Industrial Goods & Services AU 0.81 AFTERPAY Financial Services AU 0.78 SUNCORP GROUP LTD. Insurance AU 0.71 QBE Insurance Group Ltd. Insurance AU 0.70 SCENTRE GROUP Real Estate AU 0.69 AUSTRALIAN PIPELINE Oil & Gas AU 0.68 Cochlear Ltd. Health Care AU 0.67 AGL Energy Ltd. Utilities AU 0.66 DEXUS Real Estate AU 0.66 Origin Energy Ltd. -

Dividend Reinvestment Plan

196 09) DIVIDEND REINVESTMENT PLAN CONTENTS PAGE SUMMARY OF RULES 1 COMMONLY ASKED QUESTIONS AND ANSWERS 4 DIVIDEND REINVESTMENT PLAN RULES 7 Sonic Healthcare Limited ABN 24 004 196 909 Version date: 15 February 2017 SUMMARY OF RULES The Sonic Healthcare Limited ("Sonic") Dividend Reinvestment Plan (the ”DRP”) allows you to automatically reinvest some or all of your cash dividend in exchange for additional ordinary shares. This booklet has been prepared to assist you in deciding whether you wish to receive a cash dividend or increase your shareholding in Sonic by reinvestment of your dividend. A copy of the DRP Rules is contained in this booklet, which you should read carefully before deciding whether to participate in the DRP, or vary or withdraw from your participation where you have previously elected to participate. That decision should be taken after considering your particular financial and taxation position. It is stressed that while this summary provides an outline of the Plan’s operation, nothing in this booklet is intended to constitute financial product advice (and Sonic is not licensed to provide such advice). This booklet provides general comments only and does not take into account your personal objectives, financial situation or needs and should not be relied on as the basis for any decision you make in relation to participating in the DRP. You should obtain independent financial, legal and taxation advice in relation to your personal circumstances and how the participation in the DRP will affect you before making any decision to participate. If you are not already a DRP participant, it is not necessary for you to take any action if you wish to continue to receive your dividends in the form of cash only. -

ESG Reporting by the ASX200

Australian Council of Superannuation Investors ESG Reporting by the ASX200 August 2019 ABOUT ACSI Established in 2001, the Australian Council of Superannuation Investors (ACSI) provides a strong, collective voice on environmental, social and governance (ESG) issues on behalf of our members. Our members include 38 Australian and international We undertake a year-round program of research, asset owners and institutional investors. Collectively, they engagement, advocacy and voting advice. These activities manage over $2.2 trillion in assets and own on average 10 provide a solid basis for our members to exercise their per cent of every ASX200 company. ownership rights. Our members believe that ESG risks and opportunities have We also offer additional consulting services a material impact on investment outcomes. As fiduciary including: ESG and related policy development; analysis investors, they have a responsibility to act to enhance the of service providers, fund managers and ESG data; and long-term value of the savings entrusted to them. disclosure advice. Through ACSI, our members collaborate to achieve genuine, measurable and permanent improvements in the ESG practices and performance of the companies they invest in. 6 INTERNATIONAL MEMBERS 32 AUSTRALIAN MEMBERS MANAGING $2.2 TRILLION IN ASSETS 2 ESG REPORTING BY THE ASX200: AUGUST 2019 FOREWORD We are currently operating in a low-trust environment Yet, safety data is material to our members. In 2018, 22 – for organisations generally but especially businesses. people from 13 ASX200 companies died in their workplaces. Transparency and accountability are crucial to rebuilding A majority of these involved contractors, suggesting that this trust deficit. workplace health and safety standards are not uniformly applied. -

Sonic Healthcare Limited ABN 24 004 196 909 Annual Report – 30 June 2018

Sonic Healthcare Limited ABN 24 004 196 909 Annual Report – 30 June 2018 Contents Corporate Directory 1 Chairman’s Letter 2 CEO Report 3 Financial History 4 Directors’ Report 5 Corporate Governance Statement 36 Financial Report 47 Directors’ Declaration 114 Independent Auditor’s Report to the Members 115 Shareholders’ Information 121 Corporate Responsibility Report 2018 - Please refer to the Sonic Healthcare website at: http://investors.sonichealthcare.com/corporate-responsibility/?page=corporate-responsibility Sonic Healthcare Limited and controlled entities Corporate Directory Directors Prof. M.R. Compton Chairman Dr C.S. Goldschmidt Managing Director Mr C.D. Wilks Finance Director Dr P.J. Dubois Mr N. Mitchell Mr L.J. Panaccio Ms K.D. Spargo Dr E.J. Wilson Company Secretary Mr P.J. Alexander Principal registered office in Australia 14 Giffnock Avenue, Macquarie Park, New South Wales, 2113, Australia. Ph: 61 2 9855 5444 Fax: 61 2 9878 5066 Website: www.sonichealthcare.com Share registry Computershare Investor Services Pty Limited Level 5, 115 Grenfell Street, Adelaide, South Australia, 5000, Australia. Ph: 1300 556 161 (Within Australia) Ph: 61 3 9415 4000 (Outside Australia) Fax: 1300 534 987 (Within Australia) Fax: 61 3 9473 2408 (Outside Australia) Website: www.computershare.com Email: www.investorcentre.com/contact Auditor PricewaterhouseCoopers Solicitors Allens Bankers Australia and New Zealand Banking Group BNP Paribas Citibank Commerzbank Commonwealth Bank of Australia Crédit Industriel et Commercial DNB Asia HSBC JPMorgan Chase Bank Mizuho Bank MUFG Bank National Australia Bank Westpac Banking Corporation Stock exchange listings Sonic Healthcare Limited (SHL.AX) shares are listed on the Australian Securities Exchange. Sonic Healthcare Limited also has a Level 1 sponsored American Depositary Receipt (ADR) facility managed by BNY Mellon (the ‘Depositary’).