Promises, Pathways & Performance

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

U Ethical Australian Equities Trust

Quarterly u ethical Australian Equities Performance Trust - Retail Review Quarterly highlights June 2021 • The Australian equity market performed Fund information strongly over the quarter buoyed by solid economic data and positive earnings revisions Inception date 7 July 2003 • The total return for the Trust over the quarter Fund size $91.35 million was 8.0 per cent, slightly below the benchmark Over the last 12 months the Trust has delivered Benchmark S&P/ASX 300 a strong total return of 25.9 per cent Accumulation Index • Sector allocation was a small drag, although Buy/sell spread1 0.25%/0.25%1 security selection was positive with top Management costs Estimated up to 1.315% p.a. performing stocks including ResMed, See Product Disclosure Statement Cleanaway Waste Management and REA Group • Recent lockdowns highlight the ongoing Portfolio manager Jon Fernie Covid-19 risks. Rising inflation and elevated Number of stocks 20-40 valuations relative to historic levels also remain concerns Growth of $1,000 invested† Investment objective The U Ethical Australian Equities Trust has been 3,000 U Ethical AET Benchmark developed for the long-term investor and aims to 2,500 outperform the benchmark after fees over rolling 5-year periods. It invests primarily in Australian 2,000 shares as well as up to 10 per cent in fixed interest and cash. 1,500 1,000 500 0 2006 2008 2010 2012 2014 2016 2018 2020 2022 Performance 3 months 6 months 1 year 3 years 5 years 10 years Since inception % % % p.a. % % p.a. % p.a. % p.a. -

Goodman Plus Trust Annual Report 2011 Cover: 82,015 Sqm Distribution Centre Under Development for Metcash at Bungarribee Industrial Estate

Goodman Plus Trust Annual Report 2011 Cover: 82,015 sqm distribution centre under development for Metcash at Bungarribee Industrial Estate. Goodman Annual 1 PLUS Trust Report 2011 Goodman PLUS Trust Annual Report 2011 Contents Corporate governance 2 Summary of terms of redemption and exchange of Goodman PLUS 12 Financial report 15 Independent auditor’s report 32 Securities information 33 Definitions 35 Corporate directory 39 2 Corporate governance Corporate governance is the framework of rules, systems and processes by which authority is exercised within Goodman and accountability placed. It influences how the objectives of Goodman PLUS Trust (Trust) are set and achieved, how risk is monitored and assessed and how performance is optimised. The Trust recognises that an effective corporate governance culture is critical to success. We have designed and implemented a substantial range of governance initiatives, described in detail below, and we believe that our corporate governance systems are robust and effective. We recognise corporate governance is not static and systems will need to evolve over time to meet the demands of a changing market and corporate circumstances. At all times, we strive to achieve governance outcomes which balance the needs or requirements of the Trust, its stakeholders, regulators and the market. The corporate governance statement below outlines the ways in which the Trust has met the Australian Securities Exchange (ASX) Corporate Governance Council’s Corporate Governance Principles and Recommendations (2nd Edition). Any departures to implementation of the ASX Corporate Governance Council’s Corporate Governance Principles and Recommendations are described in the corporate governance statement below. As a result of the Trust not having employees of its own, and as a result of the limited business activities of the Trust, some of the ASX Corporate Governance Council’s recommendations are undertaken by Goodman Group (Goodman) rather than the Trust, as set out below. -

The State of the Deal and Deloitte Queensland Index

The State of the Deal and Deloitte Queensland Index March 2021 – Queensland Index Exceeds $100 billion THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion Contents Executive Summary 1 Then & Now – Investment Landscape 3 Then & Now – Deloitte Queensland Index 4 Queensland Economic Update 7 The Deloitte Queensland Index Q1 2021 8 Contacts 11 Sources 12 ii THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion Executive Summary Following the significant rebound in the second half of 2020, companies in the Deloitte Queensland Index exceeded $100 billion at 31 March 2021, the highest month end market capitalisation on record for the State. Deloitte Queensland Index S&P/ASX All Ordinaries Companies in the Deloitte return in Q1 2021 return in Q1 2021 Queensland Index 3.5% 2.4% 169 at 31 March 2021 10.6% in Q4 2020 14.0% in Q4 2020 173 at 31 December 2020 90 companies increased Market capitalisation as at Mar-21 market capitalisation (53%) 66 companies decreased market $101.6b capitalisation (39%) 12 no movement (7%) $97.2b as at Dec-20 $18.5b as at Sep-02 5 delistings 1 listing (1%) Announced QLD M&A Disclosed value of announced transactions in Q1 2021 QLD M&A transactions in Q1 2021 64 $1.9b 92 in Q4 2020 $3.3b in Q4 2020 1 THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion The Deloitte Queensland Index increased by 3.5% in Q1 2021 Queensland M&A more broadly remains strong with with total market capitalisation increasing to $101.6b at 64 transactions announced in Q1 2021 including: Mar-21, the highest month end value on record for the State. -

Code Security Description ARI Arrium Ltd AWC Alumina Ltd AWE AWE

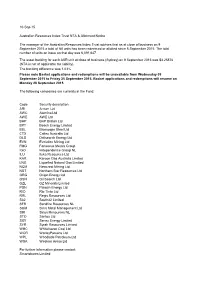

10-Sep-15 Australian Resources Index Trust NTA & Allotment Notice The manager of the Australian Resources Index Trust advises that as at close of business on 9 September 2015 a total of Nil units has been redeemed or allotted since 8 September 2015. The total number of units on issue on that day was 6,091,647. The asset backing for each ASR unit at close of business (Sydney) on 9 September 2015 was $3.25876 (NTA is net of applicable tax liability). The tracking difference was 1.03% Please note Basket applications and redemptions will be unavailable from Wednesday 09 September 2015 to Friday 25 September 2015. Basket applications and redemptions will resume on Monday 28 September 2015. The following companies are currently in the Fund: Code Security description ARI Arrium Ltd AWC Alumina Ltd AWE AWE Ltd BHP BHP Billiton Ltd BPT Beach Energy Limited BSL Bluescope Steel Ltd CTX Caltex Australia Ltd DLS Drillsearch Energy Ltd EVN Evolution Mining Ltd FMG Fortescue Metals Group IGO Independence Group NL ILU Iluka Resources Ltd KAR Karoon Gas Australia Limited LNG Liquefied Natural Gas Limited NCM Newcrest Mining Ltd NST Northern Star Resources Ltd ORG Origin Energy Ltd OSH Oil Search Ltd OZL OZ Minerals Limited PDN Paladin Energy Ltd. RIO Rio Tinto Ltd RRL Regis Resources Ltd S32 South32 Limited SFR Sandfire Resources NL SGM Sims Metal Management Ltd SIR Sirius Resources NL STO Santos Ltd SXY Senex Energy Limited SYR Syrah Resources Limited WHC Whitehaven Coal Ltd WOR WorleyParsons Ltd WPL Woodside Petroleum Ltd WSA Western Areas Ltd For further information please contact: Smartshares Limited 0800 80 87 80 [email protected]. -

Industry Associations & ASX Companies

Industry Associations, ASX Companies, Shareholder Interests and Lobbying CONTENTS About the Authors ........................................................................................................................ 3 ACCR ............................................................................................................................................ 3 About ISS-caer ............................................................................................................................. 3 About the Report .......................................................................................................................... 4 Foreword ...................................................................................................................................... 4 Introduction .................................................................................................................................. 5 Report Structure .......................................................................................................................... 6 PART 1 - Background ................................................................................................................... 8 What is an Industry Association? .............................................................................................. 8 Advantages and Disadvantages of Belonging to an Industry Association ........................... 10 Australian Legislation and Regulations Covering Industry Associations ............................. 11 -

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

Westpac Online Investment Loan Acceptable Securities List - Effective 3 September2021

Westpac Online Investment Loan Acceptable Securities List - Effective 3 September2021 ASX listed securities ASX Code Security Name LVR ASX Code Security Name LVR A2M The a2 Milk Company Limited 50% CIN Carlton Investments Limited 60% ABC Adelaide Brighton Limited 60% CIP Centuria Industrial REIT 50% ABP Abacus Property Group 60% CKF Collins Foods Limited 50% ADI APN Industria REIT 40% CL1 Class Limited 45% AEF Australian Ethical Investment Limited 40% CLW Charter Hall Long Wale Reit 60% AFG Australian Finance Group Limited 40% CMW Cromwell Group 60% AFI Australian Foundation Investment Co. Ltd 75% CNI Centuria Capital Group 50% AGG AngloGold Ashanti Limited 50% CNU Chorus Limited 60% AGL AGL Energy Limited 75% COF Centuria Office REIT 50% AIA Auckland International Airport Limited 60% COH Cochlear Limited 65% ALD Ampol Limited 70% COL Coles Group Limited 75% ALI Argo Global Listed Infrastructure Limited 60% CPU Computershare Limited 70% ALL Aristocrat Leisure Limited 60% CQE Charter Hall Education Trust 50% ALQ Als Limited 65% CQR Charter Hall Retail Reit 60% ALU Altium Limited 50% CSL CSL Limited 75% ALX Atlas Arteria 60% CSR CSR Limited 60% AMC Amcor Limited 75% CTD Corporate Travel Management Limited ** 40% AMH Amcil Limited 50% CUV Clinuvel Pharmaceuticals Limited 40% AMI Aurelia Metals Limited 35% CWN Crown Limited 60% AMP AMP Limited 60% CWNHB Crown Resorts Ltd Subordinated Notes II 60% AMPPA AMP Limited Cap Note Deferred Settlement 60% CWP Cedar Woods Properties Limited 45% AMPPB AMP Limited Capital Notes 2 60% CWY Cleanaway Waste -

Asx Clear – Acceptable Collateral List 28

et6 ASX CLEAR – ACCEPTABLE COLLATERAL LIST Effective from 20 September 2021 APPROVED SECURITIES AND COVER Subject to approval and on such conditions as ASX Clear may determine from time to time, the following may be provided in respect of margin: Cover provided in Instrument Approved Cover Valuation Haircut respect of Initial Margin Cash Cover AUD Cash N/A Additional Initial Margin Specific Cover N/A Cash S&P/ASX 200 Securities Tiered Initial Margin Equities ETFs Tiered Notes to the table . All securities in the table are classified as Unrestricted (accepted as general Collateral and specific cover); . Specific cover only securities are not included in the table. Any securities is acceptable as specific cover, with the exception of ASX securities as well as Participant issued or Parent/associated entity issued securities lodged against a House Account; . Haircut refers to the percentage discount applied to the market value of securities during collateral valuation. ASX Code Security Name Haircut A2M The A2 Milk Company Limited 30% AAA Betashares Australian High Interest Cash ETF 15% ABC Adelaide Brighton Ltd 30% ABP Abacus Property Group 30% AGL AGL Energy Limited 20% AIA Auckland International Airport Limited 30% ALD Ampol Limited 30% ALL Aristocrat Leisure Ltd 30% ALQ ALS Limited 30% ALU Altium Limited 30% ALX Atlas Arteria Limited 30% AMC Amcor Ltd 15% AMP AMP Ltd 20% ANN Ansell Ltd 30% ANZ Australia & New Zealand Banking Group Ltd 20% © 2021 ASX Limited ABN 98 008 624 691 1/7 ASX Code Security Name Haircut APA APA Group 15% APE AP -

Australian Equities Lending Margins Effective 21 April 2021

Australian Equities Lending Margins Effective 21 April 2021 Stock ASX Margin Stock ASX Margin Stock ASX Margin Code Rate Code Rate Code Rate A2B Australia A2B 40% AusNet Services AST 70% Costa Group Holdings CGC 60% The A2 Milk Company A2M 65% ASX ASX 75% Challenger Financial Australian Agricultural Company AAC 55% AUB Group AUB 50% Services Group CGF 70% Adelaide Brighton ABC 70% Australian United Challenger Capital Notes CGFPA 60% Abacus Property Group ABP 60% Investment Company AUI 70% Challenger Capital Notes 2 CGFPB 60% Audinate Group AD8 40% Aventus Retail Property Group AVN 50% Challenger Capital Notes 3 CGFPC 60% Adairs ADH 40% Alumina AWC 70% Charter Hall Group CHC 70% APN Industria REIT ADI 40% Accent Group AX1 40% Champion Iron CIA 50% Australian Ethical Amaysim Australia AYS 40% Cimic Group CIM 70% Investment Limited AEF 40% Aurizon Holdings AZJ 75% Carlton Investments CIN 50% Australian Foundation Bapcor BAP 60% Centuria Industrial REIT CIP 60% Investment Company AFI 75% Baby Bunting Group BBN 40% Collins Foods CKF 50% Ainsworth Game Technology AGI 40% Bendigo & Adelaide Bank BEN 70% Class CL1 40% AGL Energy AGL 75% Bendigo & Adelaide Bank BENHB 65% Clean Teq Holdings CLQ 40% AGL Energy USFDS AGLHA 75% Bendigo & Adelaide Bank CPS BENPE 65% Clover Corporation CLV 40% Automotive Holdings Group AHG 55% Bendigo & Adelaide Bank CPS BENPF 65% Charter Hall Long Wale REIT CLW 60% Asaleo Care AHY 50% Bendigo & Adelaide Bank CPS BENPG 65% Centuria Metropolitan REIT CMA 50% Auckland International Airport AIA 70% Bell Financial Group -

Bluescope Steel Limited Prospectus Abn 16 000 011 058

BLUESCOPE STEEL LIMITED PROSPECTUS ABN 16 000 011 058 PROSPECTUS FOR THE 1 FOR 1 NON-RENOUNCEABLE ENTITLEMENT OFFER OF UP TO APPROXIMATELY 911.7 MILLION NEW SHARES AT AN OFFER PRICE OF $1.55 PER NEW SHARE TO RAISE UP TO APPROXIMATELY $1,413 MILLION THIS PROSPECTUS IS AN IMPORTANT DOCUMENT AND REQUIRES YOUR IMMEDIATE ATTENTION. IF YOU ARE AN ELIGIBLE RETAIL SHAREHOLDER, YOU SHOULD READ THIS PROSPECTUS IN ITS ENTIRETY BEFORE DECIDING WHETHER TO ACCEPT THE OFFER OF NEW SHARES. YOUR ENTITLEMENT MAY HAVE VALUE AND YOU SHOULD THEREFORE CONSIDER WHETHER TO TAKE UP YOUR ENTITLEMENT RATHER THAN ALLOW IT TO LAPSE. IF YOU DO NOT UNDERSTAND ANY PART OF THIS PROSPECTUS, OR ARE IN DOUBT AS TO HOW TO DEAL WITH IT OR YOUR ENTITLEMENT, YOU SHOULD CONSULT YOUR STOCKBROKER, ACCOUNTANT, LAWYER OR OTHER PROFESSIONAL ADVISER. THIS DOCUMENT MAY NOT BE DISTRIBUTED INTO THE UNITED STATES OR TO ANY U.S. PERSON, AS DEFINED IN REGULATION S UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE “U.S. SECURITIES ACT”), EXCEPT ACCOMPANIED BY THE INSTITUTIONAL OFFERING MEMORANDUM AND TO A LIMITED NUMBER OF QUALIFIED INSTITUTIONAL BUYERS, AS DEFINED IN RULE 144A UNDER THE U.S. AS PART OF THE INSTITUTIONAL OFFER (AS DEFINED HEREIN). For personal use only SOLE LEAD MANAGER, UNDERWRITER & BOOKRUNNER This Prospectus may not be distributed to, or relied upon by, persons in the U.S. or who are IMPORTANT NOTICE U.S. Persons unless accompanied by the institutional offering memorandum as part of the Institutional Offer. By returning a completed Entitlement and Acceptance Form, or making a This Prospectus relates to the 1 for 1 Offer of new shares (“New Shares”) by BlueScope payment of the Application Monies for New Shares by BPAY®, you will be taken to make the Steel. -

2014 Annual Report Leighton Holdings Limited Abn 57 004 482 982

www.leighton.com.au @LeightonGroup 2014 ANNUAL REPORT LEIGHTON HOLDINGS LIMITED ABN 57 004 482 982 construction l mining l engineering l ppps Leighton Holdings Limited Annual Report 2014 2014 Annual Report CONTENTS Section Page Executive Chairman and CEO’s Review 2 Directors’ Report 4 Operating and Financial Review 12 Remuneration Report 27 Financial Report 44 Shareholdings 150 Shareholder information 152 Glossary 153 In this Annual Report a reference to ‘Group’, ‘we’, ‘us’ or ‘our’ is a reference to Leighton Holdings Limited ABN 57 004 482 982 and the entities that it controls unless otherwise stated. The Leighton Holdings corporate governance statement is available on our website, in the section titled Board and Governance (www.leighton.com.au/our-approach/board-and-governance/corporate-governance-approach). 1 Leighton Holdings Limited Annual Report 2014 Executive Chairman and CEO’s Review Dear Shareholders, As the Leighton Holdings Executive Chairman and CEO, I am proud to provide you with this review of the Leighton Group’s progress during 2014. STRATEGIC REVIEW 2014 marked the commencement of the transformation of the Leighton Group. We began a significant restructure, making progress on the objectives we set in June 2014 of strengthening the balance sheet, streamlining our operating model, and improving project delivery. Our achievements included establishing dedicated, streamlined and efficient businesses focused on contract mining, construction, public private partnerships, and engineering. We also produced a sustainable reduction in overheads, divested John Holland and established a 50:50 investment partnership for the Services operations of Leighton Contractors and Thiess. The John Holland divestment and Services partnership are subject to customary approvals including from the Foreign Investment Review Board. -

FTSE World Asia Pacific

2 FTSE Russell Publications 19 August 2021 FTSE World Asia Pacific Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) a2 Milk 0.04 NEW Asustek Computer Inc 0.1 TAIWAN Cheil Worldwide 0.02 KOREA ZEALAND ASX 0.12 AUSTRALIA Cheng Shin Rubber Industry 0.03 TAIWAN AAC Technologies Holdings 0.05 HONG KONG Atlas Arteria 0.05 AUSTRALIA Chiba Bank 0.04 JAPAN ABC-Mart 0.02 JAPAN AU Optronics 0.08 TAIWAN Chicony Electronics 0.02 TAIWAN Accton Technology 0.07 TAIWAN Auckland International Airport 0.06 NEW China Airlines 0.02 TAIWAN Acer 0.03 TAIWAN ZEALAND China Development Financial Holdings 0.07 TAIWAN Acom 0.02 JAPAN Aurizon Holdings 0.05 AUSTRALIA China Life Insurance 0.02 TAIWAN Activia Properties 0.03 JAPAN Ausnet Services 0.03 AUSTRALIA China Motor 0.01 TAIWAN ADBRI 0.01 AUSTRALIA Australia & New Zealand Banking Group 0.64 AUSTRALIA China Steel 0.19 TAIWAN Advance Residence Investment 0.05 JAPAN Axiata Group Bhd 0.04 MALAYSIA China Travel International Investment <0.005 HONG KONG ADVANCED INFO SERVICE 0.06 THAILAND Azbil Corp. 0.06 JAPAN Hong Kong Advantech 0.05 TAIWAN B.Grimm Power 0.01 THAILAND Chow Tai Fook Jewellery Group 0.04 HONG KONG Advantest Corp 0.19 JAPAN Bandai Namco Holdings 0.14 JAPAN Chubu Elec Power 0.09 JAPAN Aeon 0.2 JAPAN Bangkok Bank (F) 0.02 THAILAND Chugai Seiyaku 0.27 JAPAN AEON Financial Service 0.01 JAPAN Bangkok Bank PCL (NVDR) 0.01 THAILAND Chugoku Bank 0.01 JAPAN Aeon Mall 0.02 JAPAN Bangkok Dusit Medical Services PCL 0.07 THAILAND Chugoku Electric Power 0.03 JAPAN Afterpay Touch Group 0.21 AUSTRALIA Bangkok Expressway and Metro 0.02 THAILAND Chunghwa Telecom 0.17 TAIWAN AGC 0.08 JAPAN Bangkok Life Assurance PCL 0.01 THAILAND CIMB Group Holdings 0.08 MALAYSIA AGL Energy 0.04 AUSTRALIA Bank of East Asia 0.03 HONG KONG CIMIC Group 0.01 AUSTRALIA AIA Group Ltd.