Mercom Capital Group India Solar Market Update

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Government of India Ministry of New and Renewable Energy Lok Sabha Unstarred Question No-1538

GOVERNMENT OF INDIA MINISTRY OF NEW AND RENEWABLE ENERGY LOK SABHA UNSTARRED QUESTION NO-1538 TO BE ANSWERED ON-26.07.2018 SOLAR PARK SCHEME 1538. SHRI GEORGE BAKER SHRI PARBHUBHAI NAGARBHAI VASAVA SHRI ANIL SHIROLE Will the Minister of NEW AND RENEWABLE ENERGY be pleased to state:- (a) the salient features of the Solar Park Scheme; (b) the details of the funds sanctioned, allocated and utilised for the setting up of these parks during the last three years and the current year across the country, State/UT-wise including Gujarat, Maharashtra and West Bengal; (c) the details of the number of solar parks approved and set up/in progress during the above-mentioned period across the country, State/UT-wise including Gujarat, Maharashtra and West Bengal; (d) the details of the target set and achievements made under this scheme so far; (e) the percentage of clean energy generated by these parks so far across the country, State/UT-wise; and (f) whether the Government has faced any difficulty in some of the States with regard to setting up of these parks after approval and if so, the details thereof and the reasons therefor along with the action taken by the Government in this regard? ANSWER THE MINISTER OF STATE FOR NEW & RENEWABLE ENERGY AND POWER (I/C) (SHRI R.K. SINGH) (a) The salient features of the Solar Park Scheme are given at Annexure-I. (b) The State/UT-wise details of the funds sanctioned for setting up of Solar parks during last three years and the current year are given at Annexure-II. -

SOLAR PARKS Accelerating the Growth of Solar Power in India

Cover Story SOLAR PARKS Accelerating the Growth of Solar Power in India Anindya S Parira, discusses about the objectives, targets, the progress made so far, the solar power park developers (SPPDs), and the challenges that lie ahead of the Solar Parks flagship scheme under the National Solar Mission of the Government of India. Solar Parks: Accelerating the Growth of Solar Power in India he recent downward trends in zone of development of solar various permissions, etc., which solar tariff may be attributed power generation projects and delays the project. To overcome to the factors like economies provides developers an area that these challenges, the scheme for Tof scale, assured availability is well characterized, with proper “Development of Solar Parks and of land, and power evacuation infrastructure and access to amenities Ultra-Mega Solar Power Projects” was systems under the Solar Park and where the risk of the projects rolled out in December 2014 with an Scheme. The scheme aims to provide can be minimized. Solar Park also objective to facilitate the solar project a huge impetus to solar energy facilitates developers by reducing the developers to set up projects in a generation by acting as a flagship number of required approvals. The plug-and-play model. demonstration facility to encourage most important benefit from the solar project developers and investors, park for the private developer is the Target prompting additional projects of significant time saved. It was planned to set up at least 25 similar nature, triggering economies solar parks, each with a capacity of of scale for cost-reductions, technical Objective 500 MW and above; thereby targeting improvements and achieving large Solar power projects can be set up around 20,000 MW of solar power scale reductions in greenhouse anywhere in the country, however installed capacity. -

Solar Is Driving a Global Shift in Electricity Markets

SOLAR IS DRIVING A GLOBAL SHIFT IN ELECTRICITY MARKETS Rapid Cost Deflation and Broad Gains in Scale May 2018 Tim Buckley, Director of Energy Finance Studies, Australasia ([email protected]) and Kashish Shah, Research Associate ([email protected]) Table of Contents Executive Summary ......................................................................................................... 2 1. World’s Largest Operational Utility-Scale Solar Projects ........................................... 4 1.1 World’s Largest Utility-Scale Solar Projects Under Construction ............................ 8 1.2 India’s Largest Utility-Scale Solar Projects Under Development .......................... 13 2. World’s Largest Concentrated Solar Power Projects ............................................... 18 3. Floating Solar Projects ................................................................................................ 23 4. Rooftop Solar Projects ................................................................................................ 27 5. Solar PV With Storage ................................................................................................. 31 6. Corporate PPAs .......................................................................................................... 39 7. Top Renewable Energy Utilities ................................................................................. 44 8. Top Solar Module Manufacturers .............................................................................. 49 Conclusion ..................................................................................................................... -

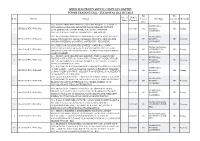

HUBLI ELECTRICITY SUPPLY COMPLANY LIMITED POWER TRADING CELL - TECHNICAL FILE DETAILS File File No

HUBLI ELECTRICITY SUPPLY COMPLANY LIMITED POWER TRADING CELL - TECHNICAL FILE DETAILS File File No. of Date of Sl No: File No. Subject Closed File Type vanished Remarks Pages Creation Date date M/s. SAI PET PREFORMS 3.5MW SOLAR POWE PROJECT, LOCATED AT WHEELING & UPPARAHALLI VILLAGE, HOSAPETE TALUK, BELLARY DISTRICT - 1 HESCOM/PTC/WBA-002/ 02-07-2019 NIL BANKING NIL Runing CONCURRENCE TO WHEEL ENERGY TO NON-CAPTIVE HT AGREEMENT INSTALLATION IN HESCOM JURISDICTION - REGARDING M/s. M. HANAMANTHARAO - 2.1MW WPP @ GUGGALMARI VILLAGE, WHEELING & 2 HESCOM/PTC/WBA-001/ ILKAL & HUNAGUND TALUK, BAGALKOT DISTRICT - REQUEST FOR 02-04-2019 NIL BANKING NIL Running SINGING WHEELING & BANKING AGREEMENT - REGARDING AGREEMENT M/s. THE UGAR SUGAR WORKS LIMITED - 44ME GROSS, 31MW POWER PURCHASE EXPORTABLE DURING SEASON, CO-GEN POWER PLANT AT UGAR 3 HESCOM/PTC/PPA-022/ 29-03-2019 NIL AGREEMENT-CO- NIL Runing KHURD VILLAGE, BELAGAVI DISTRICT - CLARIFICATION REGARDING GENERATION kVARH CHARGES M/s. RENEW SAUR URJA PRIVATE LIMITED - 50MW SOLAR POWER WHEELING & PROJECT @ ITTAGI VILLAGE< HOOVINA HADAGALI TALUK, BELLARY 4 HESCOM/PTC/WBA-016/ 15-03-2019 NIL BANKING NIL Running DIST - CONCURRENCE TO WHEEL ENERGY TO HT INSTALLATION IN AGREEMENT HESCOM JURISDICTION - REG M/s. RAI BAHADUR SETH SHREERAM NARASINGDAS PRIVATE LIMITED WHEELING & - 4.8MW (3.2MW +1.6MW) AT HARTHI, NAGAVI & BELADADI VILLAGES, 5 HESCOM/PTC/WBA-015/ 11-03-2019 NIL BANKING NIL Runing GADAG TALUK & DISTRICT. - REQUEST FOR RENEWAL OF AGREEMENT AGREEMENT AFTER EXPIRY OF TERM - REG M/s. GOLDEN HATCHERIES - 10MW SOLAR POWER PROJECT LOCATED WHEELING & AT LINGASHETTY HALLI VILLAGE, SIRA TALUK, TUMAKURU DISTRICT - 6 HESCOM/PTC/WBA-014/ 07-02-2019 NIL BANKING NIL Running REQUEST BY SLDC FOR PERMISSION TO WHEEL ENERGY TO HT AGREEMENT INSTALLATION IN HESCOM JURISDICTION M/s. -

Why the Rooftop Solar Market Is on Fire in India?

# 71 March-April 2018 Why the Rooftop Solar Market is on fire in India? Despite the ‘growth of sorts’ achieved in the past few years, India has miles to go before it achieves the solar rooftop target. According to the Bloomberg New Energy Finance report, the pace of new installations needs to double every year between now and 2022 if we were to achieve the 2022 target. INTERVIEW • Dr. Gundu Sabde, Chairman and Managing Director, RelyOn Solar Pvt. Ltd. ARTICLES • Why the Rooftop Solar Market is on fire in India - SOLAR POWER • FRP and the ‘No pains, All gains’ proposition for rooftop solar power - SOLAR POWER • Rooftop Solar Power Plant: Requirements & Challenges - SOLAR POWER EVENT • RENEWX 2018 E D ITO R I A L Dear Energetica India Readers, will account for 80% of the building's structures have two fundamental electricity consumption. drawbacks; they are heavy and prone to Energetica India welcomes you to the corrosion. The search for a material that is March-April 2018 issue. In addition to our Energetica India, in its March-April 2018 both light and maintenance-free ends online and print subscribers, the issue will also issue, meets up with industry leaders to learn with fiber-reinforced plastic (FRP). FRP is a be distributed at Renewx 2018 in Hyderabad. more about the industry's latest trends and lightweight alternative to steel and opinions: The Indian government is working to doesn't corrode even when exposed to create an ecosystem focused on sustainability — Dr. Gundu Sabde, Chairman and harsh environmental conditions. and especially in the power sector. -

List-Of-Approved-Solar-Parks

List of Solar Parks approved under the Solar Park Scheme of MNRE as on 30-06-2018 Sl. No. State Solar Park Approved Land identified at Capacity (MW) 1 Ananthapuramu-I Solar Park 1500 NP Kunta of Anantpuramu & Galiveedu of Kadapa Districts 2 Kurnool Solar Park 1000 Gani and Sakunala Village of Kurnool District Vaddirala, Thalamanchi, Pannampalli, Ramachandrayapalli, Konna 3 Andhra Pradesh Kadapa Solar Park 1000 Ananthapuram and Dhidium villages in Mylavaram Madal, Kadapa district Talaricheruvu & Aluru Villages, Tadipathri Mandal, Anathapuramu 4 Ananthapuramu-II Solar Park 500 District of Andhra Pradesh 5 Andhra Pradesh Hybrid Solar Wind Park 160 Kanaganapalli Mandal, Ananthapuramu District 6 Arunachal Pradesh Lohit Solar Park 30 Tezu township in Lohit district 7 Assam Solar Park in Assam 70 Amguri in Sibsagar district 8 Radhnesada Solar Park 700 Radhnesada, Vav, Distt. Banaskantha 9 Gujarat Harsad Solar Park 500 Villages-Harsad and Navapara, Taluka-Suigam, District-Banaskatha Dholera Special Investment Region (SIR), Taluka- Dholera, District- 10 Dholera Solar Park 5000 Ahmedabad in Gujarat Bugan in Hisar district, Baralu and Singhani in Bhiwani District and 11 Haryana Solar Park in Haryana 500 Daukhera in Mahindergarh district 12 Himachal Pradesh Solar Park in Himachal Pradesh 1000 Spiti Valley of Lahaul & Spiti District Villages Nangali & Bhoondh, Tehsil Basohli, District-Kathu district 13 Jammu & Kashmir Solar Park in J&K 200 in Jammu & Kashmir. Villages- Valluru, Rayacharlu, Balasamudra, Kyathaganacharlu, 14 Karnataka Pavagada Solar -

Renewable Energy Target

STANDING COMMITTEE ON ENERGY 17 (2020 -21) SEVENTEENTH LOK SABHA MINISTRY OF NEW AND RENEWABLE ENERGY ACTION PLAN FOR ACHIEVEMENT OF 175 GIGAWATT (GW) RENEWABLE ENERGY TARGET SEVENTEENTH REPORT LOK SABHA SECRETARIAT NEW DELHI March, 2021/Phalguna, 1942 (Saka) SEVENTEENTH REPORT STANDING COMMITTEE ON ENERGY (2020-21) (SEVENTEENTH LOK SABHA) MINISTRY OF NEW AND RENEWABLE ENERGY ACTION PLAN FOR ACHIEVEMENT OF 175 GIGAWATT (GW) RENEWABLE ENERGY TARGET Presented to Lok Sabha on 19th March, 2021 Laid in Rajya Sabha on 19th March, 2021 LOK SABHA SECRETARIAT NEW DELHI March, 2021/Phalguna, 1942 (Saka) 2 COE NO. 332 Price: Rs................... ©2021 by Lok Sabha Secretariat Published under Rule 382 of the Rules of Procedure and Conduct of Business in Lok Sabha (Sixteenth Edition) and Printed by__________. 3 CONTENTS Page No. Composition of the Committee (2020-21) 5 Composition of the Committee (2019-20) 6 Introduction 7 List of abbreviation 8 Part –I Narration Analysis I Introductory 10 II Solar Power 13 III Wind Power 44 IV Biomass and Small Hydro Power 52 V Domestic Manufacturing in Renewable Energy Sector 61 VI Green Energy Corridor 67 VII Financial Challenges in the Renewable Energy Sector 70 Part-II 79 Recommendations/Observations of the Committee Annexures I State and Union territory wise Potential of Renewable Energy 98 II State and Union territory wise Installed capacity of Grid Interactive 99 Renewable Power III State and Union territory wise list of sanctioned Solar Parks 100 IV State-wise expenditure details regarding Off-grid and -

Central Electricity Authority/ केे ��ीय िव�ुतु �ा�धकरण Renewable Energy Project Monitoring Division/ नवीकरणीय ऊजा� � प�रयोजना �बोधन �भाग

Central Electricity Authority/ केे ीय िवुतु ाधकरण Renewable Energy Project Monitoring Division/ नवीकरणीय ऊजा परयोजना बोधन भाग Daily Renewable Generation Report (ISGS)/ दिैै नक अय ऊजा उपादन रपोट (ISGS) 22 May 2021 Cumulative Generation during May Sector Installed Actual State/ Region Owner Type 2021 Station (Central/State/Private) Capacity Generation (MU) (MU) (MU) AURAIYA Uttar Pradesh Central NTPC Solar 8.0 0.06 1.97 DADRI SOLAR Uttar Pradesh Central NTPC Solar 5.0 0.02 0.4 SINGRAULI SOLAR Uttar Pradesh Central NTPC Solar 15.0 0.08 1.33 UNCHAHAR SOLAR Uttar Pradesh Central NTPC Solar 10.0 0.05 0.8 ADANI RENEWABLE ENERGY FOUR PVT Rajasthan Private IPP Solar 50.0 0.37 8.13 LTD MAHOBA SOLAR (UP) PRIVATE LTD Rajasthan Private IPP Solar 200.0 1.36 30.76 AZURE POWER FORTY THREE PRIVATE Rajasthan Private IPP Solar 250.0 2.29 43.82 LTD ACME CHITTORGARH ENERGY PVT LTD. Rajasthan Private IPP Solar 250.0 1.75 36.69 AZURE POWER INDIA PVT LTD Rajasthan Private IPP Solar 200.0 1.27 27.54 AZURE POWER THIRTY FOUR PRIVATE Rajasthan Private IPP Solar 130.0 0.92 20.43 LTD M/S ADANI SOLAR ENERGY JODHPUR TWO Rajasthan Private IPP Solar 50.0 0.37 8.25 LTD CLEAN SOLAR POWER (BHADLA) PVT LDT Rajasthan Private IPP Solar 300.0 2.19 48.6 RENEW SOLAR POWER PVT LTD Rajasthan Private IPP Solar 50.0 0.36 7.88 RENEW SOLAR POWER PVT LTD. BIKANER Rajasthan Private IPP Solar 250.0 1.85 35.49 SB ENERGY FOUR PVT LTD Rajasthan Private IPP Solar 200.0 1.34 29.88 TATA POWER RENEWABLE ENERGY LTD Rajasthan Private IPP Solar 150.0 1.2 22.31 उरी ेे / Northern Region 2118.0 15.48 -

The World's 50 Largest Operational Solar Power Plants

The world’s 50 largest operational solar power plants The world’s 50 largest operational solar power plants Capacity Country Plant name Year Developers Owners PPAs (MW) opened 2250 India Bhadla Solar Park 2020 Rajasthan Solar Park National Thermal Pow- Development Company, er Corporation (NTPC), (RSPDCL), Saurya Urja Company Solar Energy Corpora- of Rajasthan, Adani Renewable tion of India (SECI) Energy Park Rajasthan 2000 India Pavagada Solar Park - 2019 Karnataka Solar Power Karnataka Solar Power Shakti Sthala Development Corporation Limit- Development Corporation ed (KSPDCL) Limited (KSPDCL) 1963 UAE Mohammed bin 2019 ACWA Power, The Silk Road Dubai Electricity and Water Dubai Electricity Rashid Al Maktoum Fund, China’s Shanghai Authority (DEWA) and Water Authority Solar Park Electric, Masdar, (DEWA) Shuaa Energy 2, EDF Energies Nouvelles 1800 Egypt Benban Solar Park 2019 Alcazar Energy, IB Vogt, Scatec Egyptian Electricity Egyptian Electricity Solar, Shapoorji Transmission Company (EETC) Transmission Pallonji Company (EETC) 1547 China Tengger Desert Solar 2014 China National Grid China National Grid Zhongwei Park Zhongwei Power Supply Co. Power Supply Co. 1508 Mexico Enel Villanueva PV 2018 Enel Enel Centro Nacional de Plant Control de Energía (CENACE) 1177 UAE Sweihan Photovoltaic 2019 Sweihan Solar Holding Company Marubeni and JinkoSolar Abu Dhabi Water and Independent Power Electricity Company Project (ADWEC) 1000 China Yanchi Solar PV 2016 Minsheng New Energy Minsheng New Energy Station 1 The world’s 50 largest operational solar -

India's Utility-Scale Solar Parks a Global Success Story

1 Kashish Shah, Research Analyst May 2020 India’s Utility-Scale Solar Parks a Global Success Story India Is Home to the World’s Largest Utility-Scale Solar Installations Executive Summary Renewable energy in India has taken centre-stage when it comes to the significant development of energy infrastructure required to achieve India’s economic goals. In 2016, the Indian government set a giant target of 175 gigawatts (GW) of renewable energy by financial year (FY) 2021/22 and 275GW by FY2026/27 to transform the power sector from an expensive, unreliable, and polluting fossil-fuels based system into a low-cost, reliable and low-emission system based on renewable energy. In February 2019, the target was upgraded to 450GW by 2030 as per the Central Electricity Authority’s latest draft report on ‘optimal generation capacity mix for 2030’.1 India’s electricity sector transition had a promising start, driven by deflationary momentum in the cost of solar and wind energy generation equipment, cheaper financing and a favourable policy environment. As of March 2020, India’s on-grid renewable energy capacity stood at 87GW. Of the 30GW of renewable energy A promising start, capacity installed since the beginning of driven by deflationary FY2017/18 coupled with an additional 50GW awarded to date, more than 90% momentum in the cost has been contracted at tariffs ranging of solar and wind energy between Rs2.43-2.80/kilowatt hour generation equipment. (kWh) (~US$35-40/MWh) with zero indexation for 25 years. This is 60-70% 1 CEA. Draft report on optimal generation capacity mix for 2030. -

Solar Park Development and Business Structure

Solar Transmission Sector Project (RRP IND 49214) SOLAR PARK DEVELOPMENT AND BUSINESS STRUCTURE 1. Overview 1. India lies in the high solar insolation region, endowed with large solar energy potential with most of the country having about 300 days of sunshine per year with annual mean daily global solar radiation in the range of 4–6 kilowatt hour per square meter per day. Therefore, solar power projects can be set up anywhere in the country. However, the scattering of solar power projects leads to higher project cost per megawatt (MW) and higher transmission losses. Individual projects of smaller capacity incur significant expenses in site development, drawing separate transmission lines to nearest substation, procuring water and in creation of other necessary infrastructure. It also it takes a long time for project developers to acquire land, get change of land use and various permissions which tends to delay the project and is the perceived risk for project developers. 2. In order for the solar power generation project development to (i) mitigate upfront risks, (ii) reduce costs and time, and (iii) ensure coordination with various stakeholders, the Ministry of New and Renewable Energy (MNRE), the Government of India set out a scheme for solar park development in 2014.1 MNRE has planned to set up 34 solar parks in 21 states to develop about 20 gigawatt (GW) of solar power generation capacity within 5 years towards 2022. Concept of solar parks is outlined in Figure 1 with concentrated zones of solar power generation projects. Relating to the subprojects for transmission to help supply solar power under the sector loan project, specific features and indicative status of six solar parks in the states of Gujarat, Karnataka, and Rajasthan are in Annex 1 (the status may be changed over the development progress). -

Central Electricity Authority/ के ीय के ीय िव ुतुत ा धकरण

Central Electricity Authority/ केे ीय िवुतु ाधकरण Renewable Energy Project Monitoring Division/ नवीकरणीय ऊजा परयोजना बोधन भाग Daily Renewable Generation Report (ISGS)/ दिैै नक अय ऊजा उपादन रपोट (ISGS) 28 Aug 2021 Cumulative Generation during Sector Installed Actual State/ Region Owner Type Aug 2021 Station (Central/State/Private) Capacity Generation (MU) (MU) (MU) AURAIYA Uttar Pradesh Central NTPC Solar 8.0 0.1 2.37 DADRI SOLAR Uttar Pradesh Central NTPC Solar 5.0 0.01 0.52 SINGRAULI SOLAR Uttar Pradesh Central NTPC Solar 15.0 0.05 1.4 UNCHAHAR SOLAR Uttar Pradesh Central NTPC Solar 10.0 0.03 0.77 ACME CHITTORGARH ENERGY PVT LTD. Rajasthan Private IPP Solar 250.0 1.74 49.64 MAHOBA SOLAR (UP) PRIVATE LTD Rajasthan Private IPP Solar 200.0 1.47 41.59 AZURE POWER FORTY THREE PRIVATE LTD Rajasthan Private IPP Solar 250.0 2.94 72.14 AZURE POWER INDIA PVT LTD Rajasthan Private IPP Solar 200.0 1.34 36.11 AZURE POWER THIRTY FOUR PRIVATE LTD Rajasthan Private IPP Solar 130.0 0.96 28.62 CLEAN SOLAR POWER (BHADLA) PVT LDT Rajasthan Private IPP Solar 300.0 2.17 59.14 EDEN RENEWABLE CITE PRIVATE LIMITED Rajasthan Central IPP Solar 175.0 1.86 19.31 ADANI RENEWABLE ENERGY FOUR PVT LTD Rajasthan Private IPP Solar 50.0 0.39 10.89 M/S ADANI SOLAR ENERGY JODHPUR TWO LTD Rajasthan Private IPP Solar 50.0 0.39 11.01 MAHINDRA RENEWABLE PRIVATE LIMITED Rajasthan Private IPP Solar 250.0 1.79 42.48 RENEW SOLAR POWER PVT LTD Rajasthan Private IPP Solar 50.0 0.39 10.74 RENEW SOLAR POWER PVT LTD.