2731 CORAL WAY Miami, FL 33145

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

(Coral Way) Miami, Florida 33175 Tel (786) 315-2573

MIAMI-DADE COUNTY, FLORIDA Department of Permitting, Environment and Regulatory Affairs UNSAFE STRUCTURES BOARD 11805 S.W. 26 TH STREET (CORAL WAY) MIAMI, FLORIDA 33175 Chairperson TEL (786) 315 -2573 FAX (786) 315 -2570 James Cueva To: Building Officials, Construction Industry and Interested Parties Vice-Chairperson From: Secretary of the Board Gordon Loader th Date: January 11 , 2012 Board Members _________________________________________________________________________________ Emile P. Amedee A meeting of the Unsafe Structures Board has been scheduled and will be held as follows: Kevin Deeb Jose P. Escandell Benjamin S. Essien Date: January 18 th , 2012 - Wednesday Carlos A. Naumann Time: 1:00 P.M. Abel Ramirez Aymara D. Riley Place: Herbert Saffir Permitting & Inspection Center James Starkweather 11805 SW 26 th Street Robert E. Sweeney, Jr. 2nd Floor, Conference Room I & J Miami, Florida 33175 Staff TIME Michael Goolsby Kathy Charles Yvonne D. Bell New Business th Latisha Byrd 1. Minutes of December 14 , 2011 USSB Meeting 2. Consolidation of agreements, withdrawals, deferrals and uncontested cases Secretary of the Board 3. Heard Cases Charles Danger, P.E. Unincorporated Miami Dade County: 7001 NW 36 Avenue 8305 SW 72 Avenue, #1 2185 NW 57 Street, #1 7350 SW 8 Street, #1 4700 NW 72 Avenue, #1 2728 NW 32 Street, #1 14511 SW Moody Drive, #1 333 Mendoza Avenue, #1 City of North Miami Beach: 3755 NE 167 Street 1340 NE 177 Street Pursuant to F.S. 286.0105, any person who decides to appeal any decision made by the Unsafe Structures Board with respect to any matter considered at its meeting or hearing will need a record of the proceedings. -

Coral Way Plaza Anahi Quino Carlos Guzman 305-704-3104 305-704-3112 8755 SW 24Th Street, Miami, FL 33165 [email protected] [email protected]

For Leasing info: Coral Way Plaza Anahi Quino Carlos Guzman 305-704-3104 305-704-3112 8755 SW 24th Street, Miami, FL 33165 [email protected] [email protected] Unique Attributes Area Map Shopping Center anchored by Winn Dixie, Staples, and Babies”R”Us Excellent visibility, access and signage, located on SW 24th Street (Coral Way) and SW 87th Avenue (Galloway Rd.) Powerful intersection with Ross, Aldi, Party City, Publix, T.J. Maxx, and Walmart. Redevelopment planned for small shop space on the northeast corner of the center. Size of Center 162,175 SF Daily Traffic Count 63,500 Cars Parking (2.50/1,000 SF) 2014 Demographics 1 MILE 2 MILES 3 MILES 1,200 homes 2014 Estimated Total Population 24,266 101686 204,603 2,200 homes 1,076 homes Est. Population Growth 2014-19 2.33% 4.33% 4.24% Average Household Income $58,258 $55,880 $56,340 2014 Estimated Households 7,776 34,047 68,343 700 homes Average Age 45 44 43 777 Brickell Avenue, Suite 708 | Miami, FL 33131 • www.saglo.com • Tel 305-704-3192 • Fax 305-861-2703 Corsica Square - Square Corsica SITE PLAN| 777 Brickell Avenue, Suite 708 | Miami, FL 33131 • www.saglo.com •305-704-3192 708|Miami, Suite FL33131•www.saglo.com 777 BrickellAvenue, Disclaimer: 15772 SW 152nd Street, Miami,15772 SW152ndStreet, FL33196 Dancer-xise 1539sf 210' Insurance 1134sf The HappyTownAcademy Kimco Site#135 S.W. 24thSt./CoralWay Liquor 2236sf Play Area Outdoor 55,944sf 24,202sf 270' -cuts ortrafficcontrolsshallnotbedeemedtoarepresentationwarrantythatanytenantswillattheshoppingcente 3150sf |Miami-Dade County Safeguard -

US 1 from Kendall to I-95: Final Summary Report

STATE ROAD (SR) 5/US 1/DIXIE HIGHWAY FROM SR 94/SW 88 STREET/ KENDALL DRIVE TO SR 9/I-95 MIAMI-DADE COUNTY, FLORIDA FDOT FINANCIAL PROJECT ID: 434845-1-22-01 WWW.FDOTMIAMIDADE.COM/US1SOUTH March 2019 Final Summary Report ACKNOWLEDGMENTS Thank you to the many professionals and stakeholders who participated in and contributed to this study. From the communities along the corridor to the members of the Project Advisory Team, everyone played a crucial role in forming the results and conclusions contained in this study. 2 STATE ROAD (SR) 5/US 1/DIXIE HIGHWAY FROM SR 94/SW 88 STREET/KENDALL DRIVE TO SR 9/I-95 This report compiles the results of the State Road (SR) 5/US 1/ Dixie Highway from SR 94/SW 88 Street/Kendall Drive to SR 9/I-95 Corridor Study and includes: › Findings from the study › Recommendations for walking, bicycling, driving, and transit access needs along US 1 between Kendall Drive and I-95 › Next steps for implementing the recommendations This effort is the product of collaboration between the Florida Department of Transportation District Six and its regional and local partners. FDOT and its partners engaged the community at two critical stages of the study – during the identification of issues and during the development of recommendations. The community input helped inform the recommended strategies but the collaboration cannot stop here. Going from planning to implementation will take additional coordination and, in some instances, additional analysis. FDOT is able and ready to lead the effort but will continue seeking the support of community leaders, transportation and planning organizations, and the general public! To learn more, please read on and visit: www.fdotmiamidade.com/us1south WWW.FDOTMIAMIDADE.COM/US1SOUTH 3 CONTENTS 1. -

1200 Brickell Avenue, Miami, Florida 33131

Jonathan C. Lay, CCIM MSIRE MSF T 305 668 0620 www.FairchildPartners.com 1200 Brickell Avenue, Miami, Florida 33131 Senior Advisor | Commercial Real Estate Specialist [email protected] Licensed Real Estate Brokers AVAILABLE FOR SALE VIA TEN-X INCOME PRODUCING OFFICE CONDOMINIUM PORTFOLIO 1200 Brickell is located in the heart of Miami’s Financial District, and offers a unique opportunity to invest in prime commercial real estate in a gloabl city. Situated in the corner of Brickell Avenue and Coral Way, just blocks from Brickell City Centre, this $1.05 billion mixed-used development heightens the area’s level of urban living and sophistication. PROPERTY HIGHLIGHTS DESCRIPTION • Common areas undergoing LED lighting retrofits LOCATION HIGHLIGHTS • 20- story, ± 231,501 SF • Upgraded fire panel • Located in Miami’s Financial District • Typical floor measures 11,730 SF • Direct access to I-95 • Parking ratio 2/1000 in adjacent parking garage AMENITIES • Within close proximity to Port Miami, American • Porte-cochere off of Brickell Avenue • Full service bank with ATM Airlines Arena, Downtown and South Beach • High-end finishes throughout the building • Morton’s Steakhouse • Closed proximity to Metromover station. • Lobby cafeteria BUILDING UPGRADES • 24/7 manned security & surveillance cameras • Renovated lobby and common areas • Remote access • New directory • On-site manager & building engineer • Upgraded elevator • Drop off lane on Brickell Avenue • Two new HVAC chillers SUITES #400 / #450 FLOOR PLAN SUITE SIZE (SF) OCCUPANCY 400 6,388 Vacant 425 2,432 Leased Month to Month 450 2,925 Leased Total 11,745 Brickell, one of Miami’s fastest-growing submarkets, ranks amongst the largest financial districts in the United States. -

Fact Sheet a New Landscaping Project

FACT SHEET A NEW LANDSCAPING PROJECT. WILL BEGIN IN YOUR AREA FIN# 405610-4-52-01 Begins: November 2013 OVERVIEW "Z.-o On Monday, November"H,-the Florida Department ofTransportation (FDOT) is scheduled to begin a landscaping maintenance project that extends along SR 972/Coral Way/SW 22 Street from SW 37 Avenue to SW 13 Avenue. WORK TO BE PERFORMED AFFECTED MUNICIPALITIES • La ndsca ping City of Mia mi, City of Coral Gables • Trimming trees • Removing damaged and dise"<lsed trees ESTIMATED CONSTRUCTION COST $150,000 , PROJECT SCHEDULE LANE CLOSURE AND DETOUR INFORMATION November 2013 - January 2014 Lane clo,sures will occur only during non-peak hours on non-event days/ nights/weekends. Non-peak hours are: • 9_00 a.m. to 3:30 p.m. weekdays and weekends • 9:00 p .m. to 5:30 a.m. Su nday th rough Thursday nights • 11:00 p.m. to 7:00 a.m, Friday and Saturday nights Submitted Intei the public record in connectiQn Viitn HELPFUL TIPS 1t'3,1ll n{j.,- on 11/2.1 II21 .: • Allow extra time to reach your destination Prjscill~ A. Thomp~ol1 • Obey all posted signs and speed limits , ,_ City"'Clerk • Watch for signs with information about upcoming work and traffic conditions ALWAYS PUT SAFETY FIRST For your safety and the safety of others, please use caution when driving, walking or biking around any construction zone. Wearing a safety belt is the single most effective way to protect people and reduce fatalities in motor vehicle crashes. The department takes steps to reduce construction effects, but you might experience the following around the work site; • Side street, traffic lane and sidewalk closures • Increased dust and noise • Workers and equipment moving around the area. -

FOR LEASE Sears | Coral Gables / Miami 3655 SW 22Nd Street, Miami, FL 33145

FOR LEASE Existing Sears Dept Store and Auto Center Located in CORAL GABLES 3655 SW 22nd Street Miami, FL 33145 MIRACLE MILE 37TH AVE JUSTIN BERRYMAN SENIOR DIRECTOR 305.755.4448 [email protected] CAROLINE CHENG DIRECTOR 305.755.4533 [email protected] CORAL WAY / SW 22ND STREET FOR LEASE Sears | Coral Gables / Miami 3655 SW 22nd Street, Miami, FL 33145 HIGHLIGHTS Sears stand-alone department store building and auto center available for lease. 42ND AVE SUBJECT *Tenant is currently open and operating, please DO PROPERTY 27,500 AADT SALZEDO ST SALZEDO NOT DISTURB MIRACLE MARKETPLACE Located at the signalized intersection of Coral GALIANO ST GALIANO PONCE DE LEON PONCE Way/SW 22nd St (36,000 AADT) and MIRACLE MILE RETAILERS 37th Avenue (27,500 AADT) at the eastern 37TH AVE 37TH entrance of Coral Gable’s Miracle Mile Downtown Coral Gables offers a unique shopping and entertainment destination in a SW 32ND AVE SW lushly landscaped environment of tree-lined streets including Miracle Mile, Giralda Plaza, and CORAL WAY / SW 22ND ST 36,000 AADT MIRACLE MILE Shops at Merrick Park Coral Gables is home to the University of Miami, ranked as the 2nd best college in Florida (18K students), 150+ multi-national corporations (11M SF office), and numerous local and international retailers and restaurants (2M SF retail) attracting over 3 million tourists annually DOUGLAS RD DOUGLAS THE PLAZA CORAL GABLES • 2.1M SF of Retail, JUSTIN BERRYMAN Office, and Residences SENIOR DIRECTOR • Delivery August 2022 305.755.4448 LE JEUNE RD [email protected] -

Miami Office Market Report

FIRST QUARTER 2018 MIAMI OFFICE MARKET REPORT Licensed Real Estate Broker BLANCA COMMERCIAL REAL ESTATE | 1ST QUARTER 2018 MARKET REPORT | PAGE 1 EXECUTIVE SUMMARY DOWNTOWN | BRICKELL | CORAL GABLES | MIAMI AIRPORT As of first quarter 2018, favorable local and national economic Class A product remains robust. Highly populated suburban markets conditions, coupled with Miami’s continued global appeal, helped with abundant amenities and single-digit vacancies, such as Aventura sustain the success of Miami’s vibrant office market. The latest and Coconut Grove, have more than 350,000 square feet of office data demonstrate the continued decline of Miami-Dade County’s space delivering in the next 18 to 24 months The evolution of new unemployment rate (currently at 4.7%) with more than 30,000 jobs office submarkets like Wynwood, with its growing residential and added over the past year. The county also recorded 4.5% GDP vibrant amenity base, now able to offer Class A office product, poised growth, signaling a positive outlook for companies with an established to attract a new wave of companies looking to establish their offices in presence in Miami. Year-over-year, robust leasing activity and steady a creative and culturally driven office market. increase in rents evidence the demand for premium Class A office space, a trend we can expect to continue this year. With the first quarter showing local economic stability, a significant number of tenants (more than 900,000 square feet) in the market, and Year-over-year, the Miami Class A office market closed more than 1.8 limited new supply, we expect solid performance in the office sector million square feet of office lease transactions, and is outperforming this year. -

2052 Sw 1 St, Miami, Fl 33135

2052 SW 1 ST, MIAMI, FL 33135 LITTLE HAVANA SHOVEL-READY 43 UNIT DEVELOPMENT PROJECT. ASK $1,800,000 PROPERTY SIZE 12,500SF MAURICIO VILLASUSO C: 305 340 8901 E: [email protected] PROPERTY SUMMARY The site is ready to break ground under approved phased permitting. 12,000 SF T6 site benefits from efficient design, deferred impact fees, architecture and engineering costs paid, and 7 story height which precludes you from high-rise requirements, thus makes for a more efficient, cheaper to build building. Little Havana is a vibrant, and economically booming neighborhood, benefitting from its strategic location adjacent to cosmopolitan Brickell, and centric to all of Miami’s major employment centers such as Downtown, Coral Gables, the Health District and the airport. The area enjoys great public transportation, walkability, and a rich cultural environment. The area is also experiencing an economic renaissance, with many new projects being designed for the area, increasing population densities, and growing incomes. Join the wave of new investment targeting the cultural beating heart of Miami in Little Havana, and the abundant affluent consumers in nearby Brickell and Coral Gables. SITE PLAN SITE PLAN SITE PLAN PROPERTY LOCATION WYNWOOD ALLAPATTAH MIAMI INTL AIRPORT EDGEWATER HEALTH DISTRICT BECKHAM STADIUM MIDTOWN LITTLE HAVANA MARLINS PARK DOWNTOWN 2052 SW 1 ST BRICKELL CITY CENTER BRICKELL FINANCIAL DISTRICT 6.1 miles to Miami International Airport CORAL WAY CORAL GABLES 2.7 miles to Downtown UNIVERSITY OF MIAMI 1.6 miles to Calle 8 COCONUT GROVE Little Havana Is a booming neighborhood located in the heart of Miami. It is home to delicious restaurants such as LITTLE Versailles, trendy bars like Casa Florida, and outstanding dessert venues like HAVANA Azucar. -

COMMUNITY RESOURCE GUIDE Miami-Dade County Homeless Trust Community Resource Guide Table of Contents

MIAMI-DADE COUNTY HOMELESS TRUST COMMUNITY RESOURCE GUIDE Miami-Dade County Homeless Trust Community Resource Guide Table of Contents Adults & Families Animal Care Services 3 Dental Services 3 Food Assistance 4 Clothing 11 Counseling 14 Domestic Violence & Sexual Violence Supportive Services 17 Employment/Training 18 HIV/AIDS Supportive Services 27 Immigration Services 27 Legal Services 28 Low-Cost Housing 29 Medical Care: Hospitals, Urgent Care Centers and Clinics 32 Mental Health/Behavioral Health Care 39 Shelter 42 Social Security Services 44 Substance Abuse Supportive Services 44 Elderly Services 45 Persons with Disabilities 50 2 Adults & Families Animal Care Animal Welfare Society of South Florida 2601 SW 27th Ave. Miami, FL 33133 305-858-3501 Born Free Shelter 786-205-6865 The Cat Network 305-255-3482 Humane Society of Greater Miami 1601 West Dixie Highway North Miami Beach, FL 33160 305-696-0800 Miami-Dade County Animal Services 3599 NW 79th Ave. Doral, FL 33122 311 Paws 4 You Rescue, Inc. 786-242-7377 Dental Services Caring for Miami Project Smile 8900 SW 168th St. Palmetto Bay, FL 33157 786-430-1051 Community Smiles Dade County 750 NW 20th St., Bldg. G110 Miami, FL 33127 305-363-2222 3 Food Assistance Camillus House, Inc. (English, Spanish & Creole) 1603 NW 7th Ave. Miami, FL 33136 305-374-1065 Meals served to community homeless Mon. – Fri. 6:00 AM Showers to community homeless Mon. – Fri. 6:00 AM Emergency assistance with shelter, food, clothing, job training and placement, residential substance abuse treatment and aftercare, behavioral health and maintenance, health care access and disease prevention, transitional and permanent housing (for those who qualify), crisis intervention and legal services. -

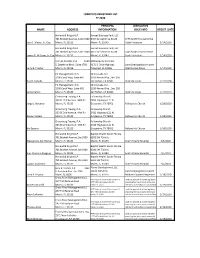

Lobbyists Registered List Fy 2020 Name Address Principal

LOBBYISTS REGISTERED LIST FY 2020 PRINCIPAL LEGISLATIVE NAME ADDRESS INFORMATION ISSUE INFO REGIST. DATE Holland & Knight LLP Sunset Business Park, LLC 701 Brickell Avenue, Suite 3300 6457 Sunset Drive South 6445 & 6457 Sunset Drive Juan J. Mayor, Jr., Esq. Miami, FL 33131 Miami, FL 33143 Code Violations 1/14/2020 Holland & Knight LLP Sunset Business Park, LLC 701 Brickell Avenue, Suite 3300 6457 Sunset Drive South 6445 & 6457 Sunset Drive James R. Williams, Jr. Esq. Miami, FL 33131 Miami, FL 33143 Code Violations 1/14/2020 Jerry B. Proctor, P.A. 9130 MMG Equity Partners S. Dadeland Blvd., Suite 1700 9171 S. Dixie Highway Land Use/Legislation work Jerry B. Proctor Miami, FL 33156 Pinecrest, FL 33156 5850 Sunset Drive 1/14/2020 P3 Management, N.A. Skinny Labs, Inc. 2100 Coral Way, Suite 405 2350 Kerner Blvd., Ste. 250 Eric R. Zichella Miami, FL 33145 San Rafael, CA 94901 mobility issues 1/21/2020 P3 Management, N.A. Skinny Labs, Inc. 2100 Coral Way, Suite 405 2350 Kerner Blvd., Ste. 250 Leslie Pantin Miami, FL 33145 San Rafael, CA 94901 mobility issues 1/21/2020 Greenberg Traurig, P.A. Fellowship Church 333 SE 2nd Avenue, 44th Flr 2450 Highway 121 N. Jorge L. Navarro Miami, FL 33133 Grapevine, TX 76051 Fellowship Church 1/28/2020 Greenberg Traurig, P.A. Fellowship Church 333 SE 2nd Avenue, 44th Flr 2450 Highway 121 N. Devon Vickers Miami, FL 33133 Grapevine, TX 76051 Fellowship Church 1/28/2020 Greenberg Traurig, P.A. Fellowship Church 333 SE 2nd Avenue, 44th Flr 2450 Highway 121 N. -

East Little Havana Development Site

EAST LITTLE HAVANA DEVELOPMENT SITE MULTIFAMILY PROJECT 67,500 SF BUILDING SIZE AVAILABLE WITH T4-R ZONING PERMITS MAURICIO VILLASUSO C: 305 340 8901 E: [email protected] PROPERTY SUMMARY 37,500 SF U r b a n C o r e D e v e l o p m e n t S i t e i n t h e H e a r t o f LOT SIZE M i a m i , 3 7 , 5 0 0 S F o f T 4 - R l a n d . S i t e h a s 3 s t r e e t f r o n t a g e s a n d f a c e s N W 1 0 t h A V , N W 4 t h S T a n d N W 3 r d S T , p r o v i n g f o r u n p a r a l l e l e d v i s i b i l i t y a n d e a s e o f i n t e r i o r c i r c u l a t i o n s / d e s i g n . M i a m i i s T4-R ZONING s u f f e r i n g a c r i s i s o f m i d d l e a n d w o r k i n g - c l a s s h o u s i n g , a n d L i t t l e H a v a n a i s u n i q u e l y p o i s e d t o p r o v i d e a n a n s w e r f o r t h a t n e e d . -

Coral Way Elementary School

Coral Way Elementary School 1 February 1998 www.ncela.gwu.edu No. 3 Cristina Pellerano and Sandra H. Fradd, University of Miami Lourdes Rovira, Miami-Dade County Public Schools Coral Way Elementary School came into being in 1936 as a combination of Spanish Heritage and Art Deco designs. The structure is filled with arches and courtyards that reflect its modern Mediterranean mystique. Today it is revered as an historic site and a shining example of Miami’s signature style. In many other ways, Coral Way Elementary reflects Miami’s Coral Way's academic program is first rate. Its test history as well as its present. As the nation’s oldest 20th century scores are among the highest in the city, and the public bilingual school, Coral Way also represents one of the most school's gifted bilingual program draws parents successful bilingual schools in the nation. As such, it is a from all over Dade County. significant example of educational achievement as well as architectural design. -- Claudio Sanchez, Commentator, Bilingual Education III, Morning Edition, National Public Radio Program In 1963, Coral Way responded to the educational needs of Cuban (www.npr.org), January 7, 1998 children who began arriving in the early 1960s. In becoming a bilingual school, Coral Way offered a welcoming gesture to the cultural and linguistic diversity that has become a trademark of South Florida and of Miami-Dade County Public Schools. In becoming bilingual, Coral Way embraced a curriculum that set it apart from other Florida schools of its time. Today, the school is recognized as a model for bilingual education nationally and internationally.