Supplemental Information Package

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2 0 2 0 a N N U a L R E P O

QUALITY INNOVATION INTEGRITY COMMUNITY 2020 ANNUAL R EPO R T From top to bottom: penthouse at 1676 International, McLean, VA; rendering of Block A at Broadmoor, Austin, TX; façade 4040 Wilson, Metro D.C.; Team members connecting on Cira Green at Cira Centre South, Philadelphia, PA; the Schuylkill Yards sign atop the Bulletin Building, Philadelphia, PA; construction crew and Brandywine worker on site at Drexel Square, Philadelphia, PA; rendering of promenade at Broadmoor, Austin, TX QUALITY INNOVATION INTEGRITY COMMUNITY n most crises, there is both danger and opportunity. I From a global pandemic, to an economic shutdown and reopening, and a social reckoning with race and justice, 2020 challenged the foundational elements of many organizations. At Brandywine, we leaned into our bedrock—the core values we’ve lived out for over 25 years by prioritizing people, relationships and communities. Our teams rose to the occasion, taking swift action to cover the danger side, and then shifting focus forward to the opportunities. Early on, as the pandemic unfolded, we quickly implemented business-continuity plans and activated a crisis response team to protect the health and safety of our employees, tenants, and stakeholders. Our operational model allowed us to keep 100% of our buildings open while we made further investments in on-site health and safety measures. We maintained strong levels of rent collection while working collaboratively with our tenants on rent relief solutions where necessary. We made great efforts to be true workplace partners, providing our tenants with custom Return to the Workplace plans and a comprehensive Tenant Resource Toolkit. We remained committed to our brand promise and leveraged this period of uncertainty to deepen our relationships. -

March 31, 2021

Units Cost Market Value US Equity Index Fund US Equities 95.82% Domestic Common Stocks 10X GENOMICS INC 126 10,868 24,673 1LIFE HEALTHCARE INC 145 6,151 4,794 2U INC 101 5,298 4,209 3D SYSTEMS CORP 230 5,461 9,193 3M CO 1,076 182,991 213,726 8X8 INC 156 2,204 4,331 A O SMITH CORP 401 17,703 28,896 A10 NETWORKS INC 58 350 653 AAON INC 82 3,107 5,132 AARON'S CO INC/THE 43 636 1,376 ABBOTT LABORATORIES 3,285 156,764 380,830 ABBVIE INC 3,463 250,453 390,072 ABERCROMBIE & FITCH CO 88 2,520 4,086 ABIOMED INC 81 6,829 25,281 ABM INDUSTRIES INC 90 2,579 3,992 ACACIA RESEARCH CORP 105 1,779 710 ACADIA HEALTHCARE CO INC 158 8,583 9,915 ACADIA PHARMACEUTICALS INC 194 6,132 4,732 ACADIA REALTY TRUST 47 1,418 1,032 ACCELERATE DIAGNOSTICS INC 80 1,788 645 ACCELERON PHARMA INC 70 2,571 8,784 ACCO BRANDS CORP 187 1,685 1,614 ACCURAY INC 64 483 289 ACI WORLDWIDE INC 166 3,338 6,165 ACTIVISION BLIZZARD INC 1,394 52,457 133,043 ACUITY BRANDS INC 77 13,124 14,401 ACUSHNET HOLDINGS CORP 130 2,487 6,422 ADAPTHEALTH CORP 394 14,628 10,800 ADAPTIVE BIOTECHNOLOGIES CORP 245 11,342 10,011 ADOBE INC 891 82,407 521,805 ADT INC 117 716 1,262 ADTALEM GLOBAL EDUCATION INC 99 4,475 3,528 ADTRAN INC 102 2,202 2,106 ADVANCE AUTO PARTS INC 36 6,442 7,385 ADVANCED DRAINAGE SYSTEMS INC 116 3,153 13,522 ADVANCED ENERGY INDUSTRIES INC 64 1,704 7,213 ADVANCED MICRO DEVICES INC 2,228 43,435 209,276 ADVERUM BIOTECHNOLOGIES INC 439 8,321 1,537 AECOM 283 12,113 17,920 AERIE PHARMACEUTICALS INC 78 2,709 1,249 AERSALE CORP 2,551 30,599 31,785 AES CORP/THE 1,294 17,534 33,735 AFFILIATED -

Pennsylvania ENERGY STAR Fact Sheet

PENNSYLVANIA April 2017 ® Families and businesses are saving with the help of ENERGY STAR Pennsylvania is home to more than 519 businesses and organizations participating in the U.S. Environmental Protection Agency’s ENERGY STAR program: 81 manufacturers of ENERGY STAR certified products 32 companies supporting independent certification of ENERGY STAR products and homes 83 companies building ENERGY STAR certified homes, three of which are committed to building 100% ENERGY STAR as well as many businesses, school districts, governments, and faith-based groups using ENERGY STAR resources to reduce energy waste in their facilities. Across the state of Pennsylvania 5,654,291 customers are served by ENERGY STAR utility partners U.S. Steel Tower, Pittsburgh, PA. 22,107 homes have earned the ENERGY STAR ENERGY STAR Certified in 2016. 19,501 buildings (nearly 1.8 billion square feet) have been benchmarked using EPA’s ENERGY STAR Portfolio Manager State Spotlights 1,033 buildings have earned the ENERGY STAR for superior efficiency, including 284 schools, 16 hotels, 7 hospitals, Air King America offers one of the most complete lines of 274 office buildings, and 4 industrial plants ENERGY STAR qualified ventilation products on the market including Bathroom Exhaust Fans, Continuous Operation Exhaust Fans, Inline Exhaust, Under Cabinet and Chimney Recent Partner of the Year Winners Range Hoods. Air King America Brandywine Realty Trust “It’s an honor to be recognized again by the EPA for our EnergyCAP Inc innovative energy efficiency solutions that are helping our Liberty Property Trust customers save energy and money every day.” – Craig North Penn School District Adams, President and CEO, PECO PECO PPL Electric SEPTA's Headquarters in Center City Philadelphia, built in Ricoh USA, Inc. -

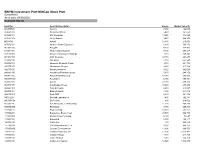

BNYM Investment Port:Midcap Stock Port (Unaudited) As of Date: 09/30/2020 Common Stocks

BNYM Investment Port:MidCap Stock Port (Unaudited) As of date: 09/30/2020 Common Stocks Identifier Security Description Shares Market Value ($) 002535300 Aaron's 7,450 422,043 00404A109 Acadia Healthcare 5,480 161,550 004498101 ACI Worldwide 13,250 346,223 00508Y102 Acuity Brands 9,470 969,255 BD845X2 Adient 12,480 216,278 00737L103 Adtalem Global Education 6,800 166,872 00766T100 AECOM 4,170 174,473 018581108 Alliance Data Systems 7,130 299,317 01973R101 Allison Transmission Holdings 7,110 249,845 00164V103 AMC Networks 10,710 264,644 023436108 Amedisys 2,760 652,547 025932104 American Financial Group 3,310 221,704 03073E105 AmerisourceBergen 2,220 215,162 042735100 Arrow Electronics 5,620 442,069 04280A100 Arrowhead Pharmaceuticals 5,670 244,150 045487105 Associated Banc-Corp 47,940 605,003 05329W102 Autonation 6,980 369,451 05368V106 Avient 23,030 609,374 053774105 Avis Budget Group 10,600 278,992 05464C101 Axon Enterprise 2,410 218,587 062540109 Bank of Hawaii 4,830 244,012 06417N103 Bank OZK 6,630 141,352 090572207 Bio-Rad Laboratories 1,480 762,881 09073M104 Bio-Techne 880 218,002 05550J101 BJs Wholesale Club Holdings 11,270 468,269 09227Q100 Blackbaud 3,750 209,363 103304101 Boyd Gaming 18,350 563,162 105368203 Brandywine Realty Trust 93,500 966,790 11120U105 Brixmor Property Group 6,300 73,647 117043109 Brunswick 8,150 480,117 12685J105 Cable One 300 565,629 127190304 CACI International, Cl. A 3,980 848,377 12769G100 Caesars Entertainment 11,890 666,553 133131102 Camden Property Trust 11,390 1,013,482 134429109 Campbell Soup 4,440 -

View Annual Report

BrandywineRealtyTrust | 2006 ANNUAL REPORT Brandywine Realty Trust (NYSE: BDN), with headquarters in Radnor, PA, is one of the largest full-service, completely integrated real estate companies in the nation. Organized as a real estate investment trust (REIT), Brandywine has a $6 billion market capitalization and develops, owns, leases, acquires, manages or has ownership interest in office and industrial properties aggregating 43 million square feet. Regional offices are located in Philadelphia, PA; Metropolitan Washington D.C.; Richmond, VA; Mt. Laurel and Lawrenceville, New Jersey; Oakland and San Diego CA; and Austin and Dallas, TX. To our shareholders: 2006 was an extraordinary year for BrandywineRealtyTrust. Our $2.7 billion merger with Prentiss Properties Trust in January effectively doubled the size of our company to $5.5 billion of total assets. As the year progressed, we executed a comprehensive integration process in which the best practices of each company were identified, refined and implemented across the combined company. Our integration process was collaborative, disciplined and incorporated every aspect of our business, and has resulted in a stronger and deeper platform for our future real estate activities. Throughout 2006, we sustained the momentum of our successful Prentiss merger with a series of value-oriented initiatives, including: Focused Developments: We made significant progress on six ground-up development projects and three major redevelopments aggregating 1.4 million square feet, and are actively marketing the associated office space to prospective tenants. During the year, we completed and leased $215.4 million of prior office developments at attractive yields, including the 99% lease-up of our award-winning, Cira Centre® office tower development. -

Usef-I Q2 2021

Units Cost Market Value U.S. EQUITY FUND-I U.S. Equities 88.35% Domestic Common Stocks 10X GENOMICS INC 5,585 868,056 1,093,655 1ST SOURCE CORP 249 9,322 11,569 2U INC 301 10,632 12,543 3D SYSTEMS CORP 128 1,079 5,116 3M CO 11,516 2,040,779 2,287,423 A O SMITH CORP 6,897 407,294 496,998 AARON'S CO INC/THE 472 8,022 15,099 ABBOTT LABORATORIES 24,799 2,007,619 2,874,948 ABBVIE INC 17,604 1,588,697 1,982,915 ABERCROMBIE & FITCH CO 1,021 19,690 47,405 ABIOMED INC 9,158 2,800,138 2,858,303 ABM INDUSTRIES INC 1,126 40,076 49,938 ACACIA RESEARCH CORP 1,223 7,498 8,267 ACADEMY SPORTS & OUTDOORS INC 1,036 35,982 42,725 ACADIA HEALTHCARE CO INC 2,181 67,154 136,858 ACADIA REALTY TRUST 1,390 24,572 30,524 ACCO BRANDS CORP 1,709 11,329 14,749 ACI WORLDWIDE INC 6,138 169,838 227,965 ACTIVISION BLIZZARD INC 13,175 839,968 1,257,422 ACUITY BRANDS INC 1,404 132,535 262,590 ACUSHNET HOLDINGS CORP 466 15,677 23,020 ADAPTHEALTH CORP 1,320 39,475 36,181 ADAPTIVE BIOTECHNOLOGIES CORP 18,687 644,897 763,551 ADDUS HOMECARE CORP 148 13,034 12,912 ADOBE INC 5,047 1,447,216 2,955,725 ADT INC 3,049 22,268 32,899 ADTALEM GLOBAL EDUCATION INC 846 31,161 30,151 ADTRAN INC 892 10,257 18,420 ADVANCE AUTO PARTS INC 216 34,544 44,310 ADVANCED DRAINAGE SYSTEMS INC 12,295 298,154 1,433,228 ADVANCED MICRO DEVICES INC 14,280 895,664 1,341,320 ADVANSIX INC 674 15,459 20,126 ADVANTAGE SOLUTIONS INC 1,279 14,497 13,800 ADVERUM BIOTECHNOLOGIES INC 1,840 7,030 6,440 AECOM 5,145 227,453 325,781 AEGLEA BIOTHERAPEUTICS INC 287 1,770 1,998 AEMETIS INC 498 6,023 5,563 AERSALE CORP -

Wilmington Funds Holdings Template DRAFT

Wilmington Large-Cap Strategy Fund as of 5/31/2021 (Portfolio composition is subject to change) ISSUER NAME % OF ASSETS APPLE INC 4.97% MICROSOFT CORP 4.69% AMAZON.COM INC 3.45% FACEBOOK INC 1.99% ALPHABET INC 1.80% ALPHABET INC 1.77% BERKSHIRE HATHAWAY INC 1.48% JPMORGAN CHASE & CO 1.35% TESLA INC 1.20% JOHNSON & JOHNSON 1.12% UNITEDHEALTH GROUP INC 0.98% VISA INC 0.96% NVIDIA CORP 0.96% BANK OF AMERICA CORP 0.89% HOME DEPOT INC/THE 0.87% WALT DISNEY CO/THE 0.82% MASTERCARD INC 0.80% PAYPAL HOLDINGS INC 0.77% EXXON MOBIL CORP 0.68% PROCTER & GAMBLE CO/THE 0.67% COMCAST CORP 0.66% ADOBE INC 0.62% INTEL CORP 0.59% VERIZON COMMUNICATIONS INC 0.59% CISCO SYSTEMS INC 0.57% CHEVRON CORP 0.55% PFIZER INC 0.54% NETFLIX INC 0.54% AT&T INC 0.53% SALESFORCE.COM INC 0.53% ABBOTT LABORATORIES 0.51% ABBVIE INC 0.50% MERCK & CO INC 0.48% WELLS FARGO & CO 0.48% BROADCOM INC 0.47% THERMO FISHER SCIENTIFIC INC 0.47% ACCENTURE PLC 0.46% CITIGROUP INC 0.45% MCDONALD'S CORP 0.44% TEXAS INSTRUMENTS INC 0.44% COCA-COLA CO/THE 0.44% HONEYWELL INTERNATIONAL INC 0.44% LINDE PLC 0.43% MEDTRONIC PLC 0.43% NIKE INC 0.43% ELI LILLY & CO 0.42% PEPSICO INC 0.42% UNITED PARCEL SERVICE INC 0.41% WALMART INC 0.40% DANAHER CORP 0.40% UNION PACIFIC CORP 0.40% QUALCOMM INC 0.38% BRISTOL-MYERS SQUIBB CO 0.37% ORACLE CORP 0.37% LOWE'S COS INC 0.36% BLACKROCK INC 0.35% CATERPILLAR INC 0.35% AMGEN INC 0.35% BOEING CO/THE 0.35% MORGAN STANLEY 0.35% COSTCO WHOLESALE CORP 0.35% RAYTHEON TECHNOLOGIES CORP 0.34% STARBUCKS CORP 0.34% GOLDMAN SACHS GROUP INC/THE 0.34% GENERAL ELECTRIC -

Annual Report 1960 1980 2000 2020

refLecting on the past, savoring the future ANNUAL REPORT 1960 1980 2000 2020 PROXY STATEMENT 1970 1990 2010 refLecting on the past, savoring the future refLecting on the past, savoring the future ANNUAL REPORT ANNUAL REPORT 1960 1980 2000 2020 PROXY STATEMENT 1960 1980 2000 2020 1970 1990 2010 PROXY STATEMENT 1970 1990 2010 refLecting on the parefLectingst, savoring on the the future past, savoring the future ANNUAL REPORT ANNUAL REPORT 1960 19601980 19802000 20002020 2020 PROXY STATEMENT PROXY STATEMENT 1970 19719900 19902010 2010 refLecting on the past, savoring the future ANNUAL REPORT 1960 1980 2000 2020 PROXY STATEMENT 1970 1990 2010 refLecting on the past, savoring the future ANNUAL REPORT 1960 1980 2000 2020 PROXY STATEMENT 1970 1990 2010 Retail is ever-evolving. Over the last several decades, we have seen many retail venues change with the times. We have seen the advent of the catalog and ecommerce platforms, big box the advent of the catalog and ecommerce platforms, big box stores and pop-ups, incorporation of a multitude of food and stores and pop-ups, incorporation of a multitude of food and beverage options and we have seen arcades come back, beverage options and we have seen arcades come back, big- bigger than ever. One thing remains, experience is a key driver ger than ever. One thing remains, experience is a key driver of of consumer spending. consumer spending. refLecting on the past, savoring the future PREIT (NYSE:PEI) is a publicly traded real estate investment trust that owns and manages quality properties in compelling markets. PREIT’s robust portfolio of carefully curated retail and lifestyle offerings mixed with destination dining and entertainment experiences ANNUALare located REPOR primarilyT in the eastern US with concentrations in the Mid-Atlantic’s top MSAs. -

Corporate Social Responsibility Report 2020

CORPORATE SOCIAL RESPONSIBILITY REPORT 2020 QUALITY | INNOVATION | COMMUNITY | INTEGRITY CORPORATE SOCIAL RESPONSIBILITY REPORT 2020 QUALITY | INNOVATION | COMMUNITY | INTEGRITY CONTENTS A MESSAGE FROM OUR CEO ..................01 THE BRANDYWINE DIFFERENCE..............02 ABOUT BRANDYWINE ...........................04 AN ONGOING COMMITMENT ..................06 – ESG Leadership and Recognition ............ 07 – Building Certifications .......................... 08 – U.N. Sustainable Development Goals ....... 10 – Managing Climate Risk ......................... 12 QUALITY .............................................14 – Environmental Goals ............................ 14 – Energy Efficiency ................................ 15 – Greenhouse Gas Emissions ................... 15 – Water Management ............................. 16 – Waste Reduction ................................ 16 – Prioritizing Health and Wellbeing ............. 18 INNOVATION ........................................21 – Development through Partnerships .......... 21 – Case Study: Innovative Planning ............. 23 – Case Study: Innovative Design ............... 24 – Case Study: Innovative Redevelopment .... 27 COMMUNITY .......................................28 – Placemaking for Vibrant Communities ...... 30 – Stakeholder Engagement ...................... 32 – Our COVID-19 Response ...................... 34 – Our Tenants ...................................... 36 – Our Employees .................................. 38 INTEGRITY ..........................................44 -

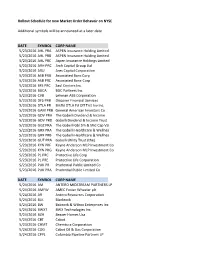

Rollout Schedule for New Market Order Behavoir on NYSE Additional

Rollout Schedule for new Market Order Behavoir on NYSE Additional symbols will be announced at a later date DATE SYMBOL CORP NAME 5/23/2016 AHL PRA ASPEN Insurance Holding Limited 5/23/2016 AHL PRB ASPEN Insurance Holding Limited 5/23/2016 AHL PRC Aspen Insurance Holdings Limited 5/23/2016 ARH PRC Arch Capital Group Ltd 5/23/2016 ARU Ares Capital Corporation 5/23/2016 ASB PRB Associated Banc Corp 5/23/2016 ASB PRC Associated Banc-Corp 5/23/2016 BFS PRC Saul Centers Inc. 5/23/2016 BGCA BGC Partners Inc. 5/23/2016 CVB Lehman ABS Corporation 5/23/2016 DFS PRB Discover Financial Services 5/23/2016 DTLA PR Brkfld DTLA Fd Off Trst Inv Inc. 5/23/2016 GAM PRB General American Investors Co 5/23/2016 GDV PRA The Gabelli Dividend & Income 5/23/2016 GDV PRD Gabelli Dividend & Income Trust 5/23/2016 GGZ PRA The Gabelli Gbl Sm & Mid Cap Val 5/23/2016 GRX PRA The Gabelli Healthcare & Wellnes 5/23/2016 GRX PRB The Gabelli Healthcare & Wellnes 5/23/2016 GUT PRA Gabelli Utility Trust (the) 5/23/2016 KYN PRF Kayne Anderson MLP Investment Co 5/23/2016 KYN PRG Kayne Anderson MLP Investment Co 5/23/2016 PL PRC Protective Life Corp 5/23/2016 PL PRE Protective Life Corporation 5/23/2016 PUK PR Prudential Public Limited Co 5/23/2016 PUK PRA Prudrntial Public Limited Co DATE SYMBOL CORP NAME 5/24/2016 AM ANTERO MIDSTREAM PARTNERS LP 5/24/2016 AMFW AMEC Foster Wheeler plc 5/24/2016 AR Antero Resources Corporation 5/24/2016 BLK Blackrock 5/24/2016 BW Babcock & Wilcox Enterprises Inc 5/24/2016 BWXT BWX Technologies Inc. -

Portfolio of Investments

PORTFOLIO OF INVESTMENTS Variable Portfolio – Partners Small Cap Value Fund, March 31, 2021 (Unaudited) (Percentages represent value of investments compared to net assets) Investments in securities Common Stocks 96.7% Common Stocks (continued) Issuer Shares Value ($) Issuer Shares Value ($) Communication Services 1.0% Automobiles 1.4% Diversified Telecommunication Services 0.3% Harley-Davidson, Inc. 162,974 6,535,257 (a) Vonage Holdings Corp. 234,766 2,774,934 Thor Industries, Inc. 37,439 5,044,531 Entertainment 0.0% Total 11,579,788 (a) Madison Square Garden Sports Corp., Class A 497 89,192 Diversified Consumer Services 0.0% Interactive Media & Services 0.1% Universal Technical Institute, Inc.(a) 17,528 102,363 (a) TrueCar, Inc. 52,852 252,897 Hotels, Restaurants & Leisure 3.4% (a) Yelp, Inc. 23,277 907,803 Del Taco Restaurants, Inc. 82,093 786,451 Total 1,160,700 Dine Brands Global, Inc.(a) 58,265 5,245,598 Media 0.5% Everi Holdings, Inc.(a) 33,130 467,464 comScore, Inc.(a) 34,027 124,539 International Game Technology PLC(a) 59,831 960,287 Cumulus Media, Inc., Class A(a) 4,137 37,688 Jack in the Box, Inc. 25,887 2,841,875 Entravision Communications Corp., Class A 7,595 30,684 Marriott Vacations Worldwide Corp.(a) 32,291 5,624,446 Gray Television, Inc. 33,631 618,810 Papa John’s International, Inc. 12,345 1,094,261 iHeartMedia, Inc., Class A(a) 35,169 638,317 PlayAGS, Inc.(a) 19,414 156,865 Marchex, Inc.(a) 6,280 17,647 Six Flags Entertainment Corp.(a) 241,229 11,209,912 TEGNA, Inc. -

Retail Brochure

schuylkillyards.com BY BRANDYWINE REALTY TRUST The Vision Schuylkill Yards transforms 14 acres adjacent to Philadelphia’s 30th Street Station, replacing parking lots with a vibrant 6.9 million SF neighborhood of parks, lifestyle experiences, and workspaces intentionally designed for productivity and wellbeing. Building upon our country’s historic values of invention, equity, entrepreneurship and courage, Schuylkill Yards introduces the next chapter for Philadelphia. Here, we are connecting people and communities, uniting bold brands with driven, entrepreneurial minded talent. Our vision is executed by the world’s best architects, engineers, planners and designers, and guided by an intentional, inclusive approach. Now, a new place is rising between Center City and University City—inspiring us to continue building the powerful legacy of Philadelphia. SF of4.8M Work Spaces SF of1.9M Living Spaces SF of Retail132K Experiences 6.5of Greenspace Acres The NEW HEART of America’s First Great City Your New Neighbors Our Neighborhood is Brilliant This is where talent flocks to and people set down roots after graduation. Anchored by several of the nation’s most acclaimed educational and medical institutions, University City continues to thrive as the center for innovation and opportunities. largest 4thpopulation of students in the U.S. with 440,000 students College54% Students Stay in Area after Talent Thrives Here Graduation It just got way easier to recruit the nation's top talent. Here, you are surrounded by Increase115% in College- the risk-takers, boundary-pushers, and educated 25-34 forward-thinkers. These people are driven by Year-olds, 2000-2017 passion and purpose, and they’re seeking like-minded companies and leaders who will push for advances in life sciences, technology and business.