Could 79 People Solarize the U.S. Electric Grid?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SOUTHEAST REGION CUMULATIVE GIVING Gifts As of January 13, 2021

SOUTHEAST REGION CUMULATIVE GIVING Gifts as of January 13, 2021 The Museum’s Southeast Regional Office serves Alabama, Arkansas, Florida, Georgia, Louisiana, Mississippi, South Carolina, Tennessee, Texas, Puerto Rico, and the US Virgin Islands. By inscribing the names of donors in perpetuity on the Museum’s walls, we recognize the generosity of individuals, families, corporations, and foundations in the southeast region that have made cumulative gifts above $50,000. Their donations were vital to the Museum’s creation and continue to sustain the Museum’s ability to acquire artifacts, develop new exhibitions, undertake scholarly research, and provide vital programming. GIFTS OF $30 MILLION OR MORE GIFTS OF $1 MILLION OR MORE Bernard Aptaker* Madlyn and Leonard Abramson Eric F. and Lore Ross* Anonymous Ted* and Lin Arison GIFTS OF $6 MILLION OR MORE David and Betty-Jean Bavar Deanie and Jay Stein Norman and Irma Braman Dorothy and Maurice* Bucksbaum GIFTS OF $5 MILLION OR MORE Rhoda and David* Chase Anne and Isidore Falk Charitable Foundation The Coca-Cola Company Sidney and Kyra Ferenc GIFTS OF $4 MILLION OR MORE Max M.* and Marjorie S. Fisher Planethood Foundation, Inc. Estate of Carl L. Glassberg Sylvia Greenberg GIFTS OF $3 MILLION OR MORE Murray H. and Joan M. Goodman Dennis Schuman Living Trust Nathan and Sophia Gumenick* Joseph Gurwin Family Foundation GIFTS OF $2 MILLION OR MORE Konover South Development Corporation Charles S. Ackerman* Murray Koppelman Anonymous Ann Wolk Krouse and Paul C. Krouse* Howard L. and Judie Ganek Mr. and Mrs. Robert Patron, and Marcia Patron* Estate of Andrew Harper Julie Peyton Jack and Barbara Kay* Pearl Resnick* Bernie and Doris Marcus Marcus and Ann Rosenberg Foundation Carl and Ruth Shapiro Family Foundation Irving and Helen* Schneider Fern and Manfred Steinfeld Family Richard Schwartz John and Janet Swanson Mickey and Karen Shapiro Elizabeth G. -

1 October 10, 2019 Scott Scheele, Esq. Chief, Telecommunications And

October 10, 2019 Scott Scheele, Esq. Chief, Telecommunications and Broadband Section Antitrust Division, U.S. Department of Justice 450 Fifth Street NW, Suite 7000 Washington, DC 20530 Re: United States v. Deutsche Telekom AG, et al., No. 1:19-cv-02232-TJK TUNNEY ACT COMMENTS OF THE COMMUNICATIONS WORKERS OF AMERICA Introduction. The proposed Final Judgment (“PFJ”) violates a number of clearly articulated Antitrust Division policies on merger remedies. These policies, incorporated in current policy guidance documents and in speeches by Division officials, are aimed at ensuring that antitrust remedies are appropriate, effective and principled. The remedy here satisfies none of these goals. The Division has not articulated any reasons, let alone principled reasons, why it has turned its back on its own merger remedy policies in this case, many of which are long-standing and represent sound antitrust enforcement. The Division has recently and successfully asserted a number of its merger remedy policies in litigated cases as a basis for rejecting proposed fixes to anticompetitive mergers, including one in which the proposed divestiture package did not include the network necessary for the buyer successfully to compete. That has particular relevance here. Judged from the standpoint of the competitive harm alleged in the Complaint, the divestiture assets do not restore the competition lost by the elimination of Sprint as an independent competitor under the theories of harm alleged in the complaint and in the product market alleged in the complaint. The divestitures create a Mobile Virtual Network Operator (“MVNO”), but the theories of harm and market definition treat competition from MVNOs as de minimis. -

Illinois Yearly Meeting of Friends

ILLINOIS YEARLY MEETING OF FRIENDS ANNUAL FOUR-DAY SESSIONS OPEN IN COMPATIBILITY, WHERE POSSIBLE, WITH THE SCHEDULING OF WESTERN AND IOWA CONSERVATIVE YEARLY MEETINGS AT THE DISCRETION OF THE CONTINUING COMMITTEE 2005 Sessions will be held from 7/27/05 to 7/31/05 on Quaker Lane near McNabb, Illinois at the Yearly Meetinghouse 130th Annual Session July 28 – August 1, 2004 YEARLY MEETING OFFICERS 2004–2005 Presiding Clerk: Recording Clerk: Reading Clerk: Assistant Clerk: Maurine Pyle Beth Schobernd Jeanette Baker Sue Davison Asst. Rec. Clerk: Treasurer Field Secretary: Admin. Coord.: Margie Haworth Roger Laughlin Roxy Jacobs Sharon Haworth Teen Friends Co-Clerks: Trevor Munroe, Meg Nelson, Alethea Tschetterwood, Teen Friends Recording Clerk: Ashlee Miller-Berry, Trustees: Richard Ashdown, Carol Bartles, Meetinghouse Phone: 815-882-2214 IYM Website: www.ilym.org 1 ILLINOIS YEARLY MEETING 2004 Blue River Quarterly B-N CC Co De P-G St.L SoI U-C Members & Attenders Statistics Average Attendance: 1 15 19 3 4 55 8 18 Adults 0 4 1 0 0 10 6 4 Under 18 years old Membership Statistics 13 26 15 2 5 61 6 26 Resident Adult Members 0 0 0 0 0 10 9 5 Resident Young Friends 4 34 31 10 2 64 4 21 Non-Resident Adult Members 1 0 0 1 0 8 0 6 Non-Resident Young Friends 18 60 46 13 7 143 19 58 TOTAL 17 60 46 12 7 125 10 47 Total Adult Members 1 0 0 1 0 18 9 11 Total Young Friends NEW MEMBERS 0 0 0 0 0 0 0 0 By Birth or Adoption 0 2 0 0 0 4 1 3 By Request 0 0 0 0 0 1 0 0 By Certificate of Transfer 0 2 0 0 0 5 1 3 TOTAL LOSSES 0 2 0 0 0 0 0 2 Deceased 0 2 1 0 0 -

Phony Philanthropy of the Walmart Heirs

Legal Disclaimer: UFCW and OUR Walmart have the purpose of helping Wal-Mart employees as individuals or groups in their dealings with Wal-Mart over labor rights and standards and their efforts to have Wal-Mart publically commit to adhering to labor rights and standards. UFCW and OUR Walmart have no intent to have Walmart recognize or bargain with UFCW or OUR Walmart as the representative of Walmart employees. Walmart1Percent.Org WALTON FAMILY “PHILANTHROPY”: A Distraction from the Walmart Economy Americans believe in the power of charitable giving. Eighty-eight percent of American households give to charity, contributing more than $2,000 per year on average.1 Despite their charitable inclinations, most American families, acting on their own, lack the financial resources to make a significant impact on the problems facing our society. The Walton family, majority owner of Walmart, is a notable exception. As members of the richest family in the United States, the Waltons have $140 billion at their disposal—enough wealth to make a positive mark on the world and still leave a fortune for their descendants. The Waltons certainly wish to be seen as a force for good. Their company claims to help people “live better” and the Walton Family Foundation mission statement speaks of “creating opportunity so that individuals and communities can live better in today’s world.”2 But that mission statement seems ironic, given that many of the most acute challenges facing American families in 2014 could rightfully be viewed as symptoms of our “Walmart economy,” characterized by rising inequality and economic insecurity. -

Graduation Invitation

Issue 2 Vol. 25 A Publication of Cornerstone Bible Institute Spring 2019 Graduation Invitation Owen Cornelius Registrar Bill Baxter Academic Dean Ruth Haynie Editor May 2019 Graduates: Micah Zulauf, Abi Johnson, Janelle Kull Cornerstone Bible Institute P.O. Box 1158 Hot Springs, SD 57747 On behalf of the CBI class of 2019, we invite you to attend and celebrate the twenty-fifth Office: (605) 745-6878 commencement program of Cornerstone Bible Institute. Graduation exercises will be Fax: (605) 745-4421 Email: [email protected] held at 1 PM on Saturday, May 4, 2019, at the Mueller Center in Hot Springs. The www.cornerstonebibleinstitute.com speaker this year will be Richard Kull, father of senior Janelle Kull. He is currently the Student Mail Address: Pastor of Outreach and Senior Ministries at College Heights Baptist Church in Casper, 1441 Martin Street Wyoming. Richard, along with his wife Starla, graduated from Prairie Bible Institute in Hot Springs, SD 57747-3085 1980. They were married in December of that same year. From 1980 to the present they have served the Lord in church planting ministry in Bolivia, Colombia, Panama, and Mexico with Avant Ministries and Faith Christian Missions. Richard is also the director of the Fellowship of Pastors and Missionaries of Mexico. The Kulls have seven children and twelve grandchildren. A reception in the CBI dining hall will follow the ceremony. Contents Founder’s Day Invitation Meet Our Graduates............ 2 You are welcome to attend our special Founder’s Day on Friday, May 3, the day before Word from the Board .......... 3 commencement. Sessions that day will start at 8 AM, 9:15 AM, and 11 AM. -

From Lawyer to CEO?

A Seat at the Head of the Table: From Lawyer to CEO? Interviews and Profiles Skills and Professional Development 1 / 13 2 / 13 3 / 13 CHEAT SHEET Risk aversion. Most law firm cultures are built around a strong bias to risk aversion. However, in transitioning to a more entrepreneurial role, lawyers must expand their perception from “no” to “yes,” even if the next question is “how?” Wearing two hats. For lawyers in business roles, it can sometimes be difficult to look beyond the legal issues when making decisions. As such, it’s essential to develop the ability to wear two hats at a time: one for the business, and one for the legal department. A fresh perspective. As in-house counsel, your seat is often at the center of the table. Given your understanding of the business from all angles, your input will be fresh and unique. Instilling interest. Unfortunately, not everyone is cut out to be an entrepreneur. Above being able to understand the business, lawyers must have a legitimate interest in business operations to succeed. April 2017 marked the 15-year anniversary of my law school graduation. I went through several stages before I realized my legal ambitions, ranging from public service to a coveted spot at a national firm. However, in 2008, I made the jump to general counsel for a technology company. Today, I’m still a GC with the same company, as well as a shareholder. Given my time with the company, familiarity with our “product,” and background, I am often called upon for business-related decisions. -

One False Move for Years, Investing Legend DAVID BONDERMAN Could Do No Wrong. and Then He Tried to Buy a Utility from Enron. By

One False Move For years, investing legend DAVID BONDERMAN could do no wrong. And then he tried to buy a utility from Enron. By NICHOLAS VARCHAVER April 4, 2005 (FORTUNE Magazine) – THEY'RE THE KINGS of American business these days. Private equity firms, hedge funds, and their cash-laden ilk have been pulling the levers of capitalism, with investors you've never heard of amassing billions and buying corporate icons like Sears. Among this extremely quiet species, David Bonderman is as dominant as they come. He has earned a reputation as a master dealmaker, a tornado of a man spinning equal parts brilliance, energy, and charm inside his ever-moving vortex. His private equity partnership, Texas Pacific Group, has massive throw-weight. The firm says it has $20 billion under management--a gaudy sum that includes a series of under-the-radar Texas Pacific affiliates in the U.S. and Asia. That war chest puts the firm in the top tier of buyout funds and dwarfs those of raiders like Carl Icahn or even hedge fund upstarts like Eddie Lampert. Just in the U.S., Texas Pacific controls companies with annual revenues of $35 billion. If it were a public company, it would rank at No. 51 on the FORTUNE 500, somewhere between Motorola and Lockheed Martin. Like any private equity firm, Texas Pacific, which is based in Fort Worth and San Francisco, gathers cash from pension funds and wealthy investors and uses it to buy control of companies. What sets it apart from its peers is its reputation for taking on risky, unfixable companies--and then devoting serious resources to fixing them. -

Honor Roll 2019

DONATION SPOTLIGHT HONOR ROLL OF DONORS ANONYMOUS CHILDREN’S HOSPITAL $25 MILLION LOS ANGELES DONATION SUPPORTS NEUROLOGICAL INSTITUTE Our history began in 1901, when a small group of caring individuals envisioned the benefits of a hospital for children. No one would have AND INTERVENTIONAL believed that the first children’s hospital in Southern California would RADIOLOGY evolve into one of the world’s leading pediatric health care facilities. More than a century later, the compassion of those founding members continues to thrive in our physicians, nurses, caregivers and researchers. The hospital’s international reputation is a testament to years of dedicated efforts from our team members and volunteers, as well as the philanthropic support from individuals, organizations, corporations and foundations. This generosity plays a pivotal role in our mission to create hope and build healthier futures. As a pediatric academic medical center, Children’s Hospital Los Angeles provides more than just the finest clinical care; we also remain at the forefront of novel research and professional education. Given the fundamental difference in the physiology of kids and adults, the best place In 2019, an anonymous donor made a $25 million to discover and develop the safest, most effective therapies and devices for gift to expand the Neurological Institute and children is at a hospital dedicated exclusively to their care. This work has increase the hospital’s capacity in interventional solidified Children’s L.A. as a global leader in the advancement of pediatric radiology (IR). This transformative gift will help treatment options, extending our commitment to caring—and the impact CHLA meet the rising demand for pediatric of donors’ philanthropic support—far beyond Los Angeles. -

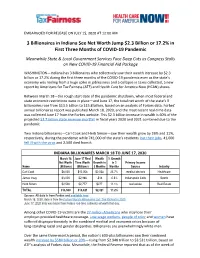

3 Billionaires in Indiana See Net Worth Jump $2.3 Billion Or 17.2% in First Three Months of COVID-19 Pandemic

EMBARGOED FOR RELEASE ON JULY 15, 2020 AT 12:00 AM 3 Billionaires in Indiana See Net Worth Jump $2.3 Billion or 17.2% in First Three Months of COVID-19 Pandemic Meanwhile State & Local Government Services Face Deep Cuts as Congress Stalls on New COVID-19 Financial Aid Package WASHINGTON—Indiana has 3 billionaires who collectively saw their wealth increase by $2.3 billion or 17.2% during the first three months of the COVID-19 pandemic even as the state’s economy was reeling from a huge spike in joblessness and a collapse in taxes collected, a new report by Americans for Tax Fairness (ATF) and Health Care for America Now (HCAN) shows. Between March 18—the rough start date of the pandemic shutdown, when most federal and state economic restrictions were in place—and June 17, the total net worth of the state’s 3 billionaires rose from $13.5 billion to $15.8 billion, based on an analysis of Forbes data. Forbes’ annual billionaires report was published March 18, 2020, and the most recent real-time data was collected June 17 from the Forbes website. This $2.3 billion increase in wealth is 60% of the projected $3.7 billion state revenue shortfall in fiscal years 2020 and 2021 combined due to the pandemic. Two Indiana billionaires—Carl Cook and Herb Simon—saw their wealth grow by 26% and 11%, respectively, during the pandemic while 741,000 of the state’s residents lost their jobs, 41,000 fell ill with the virus and 2,500 died from it. -

WAL-MART At50

WAL-MART at50 FROM ARKANSAS TO THE WORLD a supplement to . VOL. 29, NO. 27 • JULY 2, 2012 ARKANSASBUSINESS.COM/WALMART50 Fifty years old, and healthy as ever Congratulations, Walmart! And thanks for letting us care for your associates and communities. From one proud Arkansas company to another CONGRATULATIONS TO A GREAT AMERICAN SUCCESS STORY It has been a privilege to travel with Walmart on its remarkable journey, including managing the company’s 1970 initial public offering. From one proud Arkansas company to another, best wishes to all Walmart associates everywhere. INVESTMENT BANKING • WEALTH MANAGEMENT INSURANCE • RESEARCH • SALES & TRADING CAPITAL MANAGEMENT • PUBLIC FINANCE • PRIVATE EQUITY STEPHENS INC. • MEMBER NYSE, SIPC • 1-800-643-9691 STEPHENS.COM WAL-MART at 50 • 3 Wal-Mart: INSIDE: A Homegrown 6 The World of Wal-Mart Mapping the growth of a retail giant Phenomenon 8 Timeline: A not-so-short history of Wal-Mart Stores Inc. Thousands of Arkansans have a Wal-Mart experience to share from the past 50 years that goes far beyond the routine trip to a Supercenter last week. 10 IPO Set the Stage for Global Expansion Wal-Mart is an exciting, homegrown phenomenon engineered by the late Sam Walton, a brilliant businessman who surrounded himself with smart people and proceeded to revolutionize 14 Influx of Workers Transforms retailing, logistics and, indeed, our state and the world. He created a heightened awareness of stock Northwest Arkansas investments as investors from Arkansas to Wall Street watched the meteoric rise in share prices and wondered when the next stock split would occur. -

Press Release

CONTACT: McKenna Young FOR IMMEDIATE RELEASE 484-385-2913 (office) December 17, 2015 [email protected] PRESS RELEASE Horatio Alger Association Announces 12 Recipients of Annual Dennis R. Washington Achievement Graduate Scholarships The Dennis & Phyllis Washington Foundation provides graduate grants of up to $90,000 to Horatio Alger Scholars who wish to further their education WASHINGTON, D.C. (December 17, 2015) – Horatio Alger Association of Distinguished Americans, Inc., a nonprofit educational organization honoring the achievements of outstanding individuals and encouraging youth to pursue their dreams through higher education, today announced the 12 recipients of the 2015 Dennis R. Washington Achievement Graduate Scholarship. Endowed in 2008 and funded by the Dennis & Phyllis Washington Foundation, this scholarship provides financial assistance to Alumni recipients of Horatio Alger National and State Scholarships who aspire to obtain graduate degrees. The Dennis & Phyllis Washington Foundation was established in 1988 by Dennis Washington, chairman emeritus of Horatio Alger Association, and his wife, Phyllis. Since its inception, the Foundation has donated more than $199 million to charitable causes. The Foundation, which supports deserving individuals in an effort to better society as a whole, established its Achievement Graduate Scholarship program to provide financial assistance exclusively to Horatio Alger undergraduate scholarship recipients who are committed to pursuing a graduate degree. Applicants must have a minimum 3.0 -

Threat from the Right Intensifies

THREAT FROM THE RIGHT INTENSIFIES May 2018 Contents Introduction ..................................................................................................................1 Meeting the Privatization Players ..............................................................................3 Education Privatization Players .....................................................................................................7 Massachusetts Parents United ...................................................................................................11 Creeping Privatization through Takeover Zone Models .............................................................14 Funding the Privatization Movement ..........................................................................................17 Charter Backers Broaden Support to Embrace Personalized Learning ....................................21 National Donors as Longtime Players in Massachusetts ...........................................................25 The Pioneer Institute ....................................................................................................................29 Profits or Professionals? Tech Products Threaten the Future of Teaching ....... 35 Personalized Profits: The Market Potential of Educational Technology Tools ..........................39 State-Funded Personalized Push in Massachusetts: MAPLE and LearnLaunch ....................40 Who’s Behind the MAPLE/LearnLaunch Collaboration? ...........................................................42 Gates