Weyerhaeuser Company Seizing 2006 Annual Report and Form 10-K the Future Weyerhaeuser Company 2006 Annual Report and Form 10-K

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Proxy Statement

2020 WEYERHAEUSER NOTICE OF THE 2020 ANNUAL MEETING & PROXY STATEMENT DEAR SHAREHOLDER: We are pleased to invite you to attend your company’s annual meeting of shareholders at 8:00 a.m. Pacific Time on Friday, May 15, 2020. We are sensitive to the public health and travel concerns our various stakeholders may have and the recommendations that public health officials and federal, state and local governments have issued in light of the evolving coronavirus (COVID-19) situation. As a result, the annual meeting will be conducted virtually via audio webcast. You will be able to attend the meeting, vote your shares and submit questions by logging on to www.virtualshareholdermeeting.com/WY2020. The annual meeting will include a report on our operations and consideration of the matters set forth in the accompanying notice of annual meeting and proxy statement. All shareholders of record as of March 20, 2020 are entitled to vote. Your vote is important. Whether or not you plan to attend the virtual annual meeting, we urge you to please vote as soon as possible. You can vote in the manner described in the section titled Information about the Meeting—Voting Matters—Options for Casting Your Vote on page 65 of the accompanying proxy statement. On behalf of your board of directors, thank you for your continued ownership and support of Weyerhaeuser. Sincerely, Rick R. Holley Devin W. Stockfish Chairman of the Board President and Chief Executive Officer OUR CORE VALUES Safety Š Integrity Š Citizenship Š Sustainability Š Inclusion TABLE OF CONTENTS Notice -

Weyerhaeuser: a Good Reputation Instilled in Culture

Journal of Intercultural Management Vol. 7, No. 2, June 2015, pp. 21–29 DOI 10.1515/joim-2015-0008 Zbigniew Bochniarz5 University of Washington Jacek Lipiec6 Warsaw School of Economics Weyerhaeuser: A Good Reputation Instilled in Culture Abstract: The paper addresses the concept of Weyerhaeuser’s culture which was transformed as the result of mergers and implemented policies against recession. The culture, particularly their long-term vision and values played a crucial role in Weyerhaeuser’s company. Frederick Weyerhaeuser, founder of the firm, realized that a firm’s reputation was the most important asset. Significant increases in housing demand over 1997-2005 had led to an enormous pressure for faster deliveries and innovations in the construction industry. Weyerhaeuser decided to become global leader by transforming its culture and launching the iLevel concept7. Key words: corporate culture, family firm, Weyerhaeuser. This is not for us, nor for our children – but for our grandchildren Frederick Weyerhaeuser, 1900 Introduction The story of Weyerhaeuser begins with Frederick Weyerhaeuser who came to America from Germany in 1852. Although he was working as a simple laborer, he succeeded in each job he undertook. Asked whether he is a lucky in all these successes he simply replied (Robertson 2011): “The secret lay simply in my will to work. I never watched the clock and never stopped before I had finished what I was working on”. Frederick Weyerhaeuser teamed up with 15 partners with whom 5 [email protected] 6 [email protected] 7 The authors would like to express their gratitude to Weyerhaeuser Company for providing the data. -

MASS) Introduction and Objectives

Beese, W.J. (1995). Montane alternative silvicultural systems (MASS) introduction and objectives. In J.T. Arnott, W.J. Beese, A.K. Mitchell, & J. Peterson (Eds.), Montane alternative silvicultural systems (MASS). Proceedings of a workshop held June 7‐8, 1995 in Courtenay, British Columbia. (FRDA Report 238). (pp. 3‐8). Victoria, B.C.: Canadian Forest Service; Victoria, B.C.: Ministry of Forests. The complete publication is available on the Canadian Forest Service Publications website at http://cfs.nrcan.gc.ca/publications?id=4227. FRDA REPORT 238 Montane A ternative Silv·cultural Systems (MASS) Proceedings of a Workshop held June 7-8 1995 in Courtenay British Columbia PMEN1: FRD 11 Canada Montane Alternative Silvicultural Systems (MASS) Proceedings of a Workshop held June 7-8, 1995 in Courtenay, British Columbia Edited by: J.T. Arnott1, W.J. 8eese2, A.K. Mitchell1 and J. Peterson1 1 Pacific Forestry Centre, Canadian Forest Service, Victoria, B.C. 2 Sustainable Forestry Division, MacMillan Bloedel Ltd., Nanaimo, B.C. December 1995 FRDA Report No. 238 CAJ\ADA-BRlTISHCOLUMBIA PARTNERSHIP AGREEMEl\TT 01'1 FOREST RESOURCE DEVELOPMENT: FRDA IT Canada BC;;ti Funding for this publication was provided by the Canada-British Columbia Partnership Agreement on Forest Resource Development: FRDA 11- a four year (1991-95) $200 million program cost-shared equally by the federal and provincial governments. Canadian Cataloguing in Publication Data Main entry under title: Montane Alternative Sllvicultural Systems (MASS) Proceedings of a workshop held June 7-8, 1995 in Courtenay, British Columbia (FRDA report. ISSN 0835-0752 : 238) «Canada�British Co!umbla Partnership A_greement on Forest Resource Development FRDA !!.� Co-published by B.C. -

George Weyerhaeuser (Page 1)

George H.Weyerhaeuser 1926 - Although he spent 25 years leading a Fortune 100 company practices. He was proud that his company’s roots were connected to transportation projects. “He wanted to hear from the people doing the founded by his great-grandfather, George Weyerhaeuser doesn’t mind nature, and he championed the work of the forester. In an essay work. He always was open to hear what’s really going on. Best guy I being called a logger. As he once told the Seattle Times, “I have always encouraging young people to pursue forestry, he wrote: “To many, ever worked for.” thought of loggers and logging in terms of the outdoors—men with an forestry conveys inner peace through the physical and spiritual beauty F. Lowry Wyatt, who served as one of George’s vice presidents, independent frame of mind.” of the outdoors. It offers a stimulating combination of mental and called him “as good a leader as I’ll ever know.” In fact, George did some honest-to-goodness logging early in his physical challenges and the thrill of growing majestic trees for future When challenges arose in an ever-changing world, George faced career, learning the lumber business from the ground up. Having generations.” them squarely. During the 1980s, when a worldwide oversupply of completed his naval service during World War II, George took a At headquarters, George rose quickly from executive vice presi- wood products created difficult market conditions, he talked openly summer job in the woods of Washington state as a choker setter—the dent’s assistant (1957) to manager of the wood products group and vice with employees and made the necessary decisions to improve company logging crewman who wraps the cable around the log before it is president (1958); executive vice president for wood products, timber- competitiveness. -

Weyerhaeuser Company 2016 Annual Report

WEYERHAEUSER 2016 ANNUAL REPORT AND FORM 10K Working together to be the world’s premier timber, land, and forest products company DEAR SHAREHOLDER: This past year was transformative for our company. This work continues. We now expect to exceed our Over the past three years, we have been relentlessly focused $100 million cost synergy on making Weyerhaeuser a truly great company by driving value target by 25 percent, realize for our shareholders through a focused portfolio, industry-leading a total of $130–$140 million performance, and disciplined capital allocation. In 2016, we in operational synergies, FRPSOHWHGWZRVLJQLÀFDQWPRYHVWKDWUHSUHVHQWWKHFDSVWRQH and continue delivering on on our portfolio journey: our merger with Plum Creek Timber our operational excellence and the divestiture of our Cellulose Fibers business. targets. Capitalizing on these PORTFOLIO opportunities will enable us Following these transactions, we have emerged as a focused to further improve our relative forest products company with 13 million acres of world-class performance. timberlands and an industry-leading, low-cost wood products CAPITAL ALLOCATION manufacturing business. 2XUÀUVWSULRULW\IRUFDSLWDO 2XUWLPEHUKROGLQJVDUHQHDUO\ÀYHWLPHVWKHVFDOHRIRXU allocation is returning cash largest competitor, and we are one of the largest REITs in the to shareholders, and we continued to deliver on that commitment United States. Through the Plum Creek merger, we also gained in 2016 by repurchasing $2 billion of common shares. We remain unparalleled expertise in Real Estate, Energy and Natural strongly committed to disciplined capital allocation, including a Resources. This new business segment will further maximize sustainable and growing dividend. the value of our acres by identifying tracts with a premium POSITIONED FOR THE FUTURE value over timberland and fully capturing the value of surface In September, we moved our corporate headquarters from and subsurface assets. -

Project Capabilities

PROJECT CAPABILITIES PROJECTS IN CANADA Services in Canada Since our inception in 1976, JANSEN has completed numerous projects in all Canadian Provinces where pulp mills are located. The type of project and scope of work included: • Boiler Conversion to Biomass Burning (see Capabilities C-01) • Biomass Boiler Evaluations (see Capabilities C-02) • Biomass Boiler Combustion System Upgrades (see Capabilities C-03) • Recovery Boiler Performance and Engineering Evaluations (see Capabilities C-04) • Recovery Boiler Capacity Upgrades (see Capabilities C-05) • Computational Fluid Dynamics (CFD) Modeling (see Capabilities C-06) • Boiler Circulation Studies (see Capabilities C-07) • Ultrasonic Flow Monitoring (UFM) of Boiler Circulation (see Capabilities C-08) • Boiler Pressure Part Design (see Capabilities C-09) • Superheater Capacity & Performance Upgrades (see Capabilities C-10) • Boilers in Energy-from-Waste Industry (see Capabilities C-11) • Evaluation Disposal of DNCG and CNCG in Existing Boilers (see Capabilities C-12) • Superheater Corrosion Prevention (see Capabilities C-14) • NOx Emissions Reduction (see Capabilities C-15) • Sulfite (SSL) and Soda Liquor Recovery Boilers (see Capabilities C-17) • Fluidized Bed Boilers Bubbling/Circulating (BFB/CFB) (see Capabilities C-18) Selected References (see next page) C-20 2/17 Selected References Projects in Canada Alberta Pacific Forest Industries, Inc. - Boyle, AB Weyerhaeuser Canada Ltd. - Kamloops, BC Atlantic Power Company - Williams Lake, BC Weyerhaeuser Canada Ltd. - Price Albert, SK AV Cell - Atholville, NB AV Nackawic - Nackawic, NB AV Terrace Bay - Terrace Bay, ON Boise Cascade Canada - Fort Frances, ON Canfor Intercon - Prince George, BC Canfor Northwood - Prince George, BC Canfor PGP - Prince George, BC Cariboo Pulp & Paper - Quesnel, BC Catalyst Paper - Crofton, BC Catalyst Paper - Port Alberni, BC Catalyst Paper - Powell River, BC Corner Brook Pulp & Paper - Corner Brook, NF Daishowa Marubeni - Peace River, AB Domtar Papers - Cornwall, ON Domtar, Inc. -

The Evolution of Corporate Social Responsibility

CORPORATE PARTNERSHIPS WITH NON-GOVERNMENTAL ORGANIZATIONS: THE EVOLUTION OF CORPORATE SOCIAL RESPONSIBILITY A THESIS Presented to The Faculty of the Department of Economics and Business The Colorado College In Partial Fulfillment of the Requirements for the Degree Bachelor of Arts By Peder McDermott Johansen May/2009 CORPORATE PARTNERSHIPS WITH NON-GOVERNMENTAL ORGANIZA TIONS: THE EVOLUTION OF CORPORATE SOCIAL RESPONSIBILITY Peder McDermott Johansen May,2009 Economics Abstract The purpose of this thesis is to investigate the factors that motivate companies to partner with NGOs on the issue of climate change. In investigating these factors several appear to motivate companies to take action: cost savings, brand image, and altruistic motivations. Climate change has the ability to change the way we live and the global landscape. It is important to understand the factors that cause business to take action on climate change so that we can help to slow or reduce the intensity of climate change. I investigate six companies, three who are actively partnering with NGOs (Lafarge, Nike, and Starbucks) and three who are not (Boeing, Costco, and Weyerhaeuser) to determine what factors motivate these companies to either take action or not. KEYWORDS: (Climate Change, Corporate Social Responsibility, NGO) ON MY HONOR, I HAVE NEITHER GIVEN NOR RECEIVED UNAUTHORIZED AID ON THIS THESIS Signature TABLE OF CONTENTS Chapter Page I. INTRODUCTION ..................................................................... .. II. THEORy...... ........................................................................... -

Federal Reserve Notes

FEDERAL RESERVE BANK op« Federal Notes FEDERAL RESERVE BANK OF SAI^fftif^lSCO • NO. 3, 1980 Serving Alaska, Arizona, California, Hawaii, Idaho, Nevada, Oregon, Utah & Washington S.F. FED SETS UP DEREG COMMITTEE OUTREACH PROGRAM RULES ON NOW RATES The Federal Reserve Bank of San The Depository Institutions Dereg Francisco has developed a number ulation Committee (DIDC) ruled of programs to assist depository that banks and savings institutions institutions in complying with the will be able to pay as much as 5Va new procedures mandated under percent on check-type NOW ac the terms of the Monetary Control counts beginning in 1981, but it left Act. Under the Act, Congress at intact current interest-rate ceilings tempted to improve the effective on regular savings accounts. In ness of monetary policy by apply another key decision, the commit ing new Federal Reserve reserve tee agreed to permit the continued requirements to all depository in use of premiums or gifts that insti stitutions with transaction (check- tutions offer to people who open type) accounts and non-personal new accounts or add to existing time deposits. ones. G. H. Weyerhaeuser To implement this goal, the Act The DIDC ruled that the ceiling rate WEYERHAEUSER HEADS authorized the Federal Reserve to on "negotiable order of with SEATTLE BOARD collect reports from all depository drawal" accounts — NOW ac institutions. And among other key George H. Weyerhaeuser has been counts — will be raised to 51/4 per provisions, the MCA provided non- named Chairman of the Board of cent, effective December 31. The member institutions with access to Directors of the Seattle Branch of rate on "automatic transfer from Federal Reserve borrowing privi the Federal Reserve Bank of San savings" accounts — ATS ac leges and other Fed services, and Francisco. -

WEYERHAEUSER 2018 Annual Report and Form 10-K

WEYERHAEUSER 2018 Annual Report and Form 10-K Working together to be the world’s premier timber, land, and forest products company DEAR SHAREHOLDER This is an exciting time to be assuming leadership for Weyerhaeuser. :HDOVRFRQWLQXHGRXUGLVFLSOLQHGXVHRIFDSLWDOWRLQYHVWEDFN I’m thrilled and honored to be part of the journey that lies ahead for LQRXUEXVLQHVVWKURXJKORZULVNKLJKUHWXUQSURMHFWVWKDW this great company. UHGXFHRXUFRVWVWUXFWXUHLPSURYHSURGXFWLYLW\DQGLQFUHDVH reliability across our operations. )RUWKHODVWÀYH\HDUVZH·YHEHHQLQWHQVHO\IRFXVHGRQJHQHUDWLQJ VKDUHKROGHUYDOXHE\VWUHDPOLQLQJRXUSRUWIROLRLPSURYLQJSHUIRUPDQFH A LEADER IN CORPORATE RESPONSIBILITY DFURVVDOOEXVLQHVVOLQHVDOORFDWLQJFDSLWDOLQDGLVFLSOLQHGPDQQHU (DFK\HDUZHUHFHLYHQXPHURXVWKLUGSDUW\UHFRJQLWLRQVIRURXU GHYHORSLQJRXUSHRSOHDQGGULYLQJPHDQLQJIXOFXOWXUHFKDQJH sustainability and corporate citizenship performance. I encourage ,·PSURXGRIWKHZRUNZH·YHGRQH2XUEXVLQHVVVWUDWHJ\LVVLPSOH \RXWRUHYLHZDQHZVHFWLRQLQRXU3UR[\6WDWHPHQWWKDWIRFXVHV IRFXVHGDQGHIIHFWLYHDQGZHZLOOFRQWLQXHWRH[HFXWHDJDLQVWWKHVH RQRXUHQYLURQPHQWDOVWHZDUGVKLSVRFLDOUHVSRQVLELOLW\HWKLFV priorities in the years ahead. DQGWUDQVSDUHQF\7KHVHKDYHORQJEHHQFRUHYDOXHVIRURXU STRONG FINANCIAL PERFORMANCE IN 2018 FRPSDQ\7KH\DWWUDFWJUHDWSHRSOHWRFRPHZRUNIRUXVDQGKHOS XVPDLQWDLQVWURQJUHODWLRQVKLSVZLWKFXVWRPHUVDQGWKHFRPPXQLWLHV ,QZHGHOLYHUHGVWURQJSHUIRUPDQFHWKURXJKDEURDGUDQJHRI ZKHUHZHRSHUDWH,·PSURXGWREHSDUWRIDFRPSDQ\WKDWPDNHV PDUNHWFRQGLWLRQV2XUUHYHQXHZDVQHDUO\ELOOLRQIURPZKLFKZH FRUSRUDWHUHVSRQVLELOLW\DSULRULW\DQG,NQRZWKLVLVFULWLFDOO\ JHQHUDWHGQHWHDUQLQJVRIPLOOLRQXSIURPPLOOLRQLQ -

FOR LEASE__110 James

FOR 110 JAMES BUILDING LEASE 110 JAMES ST, EDMONDS, WA 98020 ASTRAEUS GYM'S GRAND RE-OPENING 1,450 SF & 3,345 SF Units Available GABRIEL GRAUMANN, CCIM THE PLATZ GROUP - KW COMMERCIAL | 206.257.7153 | [email protected] 110 JAMES BUILDING 110 JAMES ST, EDMONDS, WA 98020 AVAILABLE SPACES SPACE 1st Fl, Ste 101 24/7 access SIZE 1,450 SF Secured parking garage Walking distance to Edmonds ferry FULL terminal and Sounder commuter rail station SERVICE $30.00/SF RENT PAGE 2 110 JAMES BUILDING 110 JAMES ST, EDMONDS, WA 98020 1ST FL, STE 101 PAGE 3 110 JAMES BUILDING 110 JAMES ST, EDMONDS, WA 98020 SPACE 1st Fl, Ste 105 SIZE 3,345 SF FULL SERVICE $29.00/SF RENT PAGE 4 110 JAMES BUILDING 110 JAMES ST, EDMONDS, WA 98020 Puget Sound Market Overview & Demographics The Puget Sound region is a coastal area of the Pacific Northwest of Washington, including Puget Sound, the Puget Sound lowlands, and the surrounding region roughly west of the Cascade Range and east of the Olympic Mountains. INDUSTRY AND MAJOR EMPLOYERS Key businesses within the state include the design and manufacture of jet aircraft (Boeing), computer software development (Microsoft, Nintendo of America, Valve), online retailers (Amazon, Expedia, Inc.), electronics, biotechnology, aluminum production, lumber and wood products (Weyerhaeuser), mining, and tourism. Boeing Everett is the largest manufacturing building in the world, producing the 747, 767, 777, and the 787 airplanes. Over 30,000 aerospace employees in Everett support aircraft fabrication and production, product development, aviation safety and security and airplane certifications. Other production areas at 71,829 the site include the paint hangars, flight line and delivery center. -

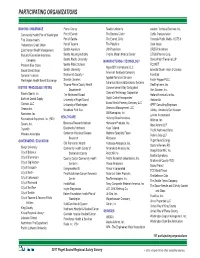

Participating Organizations

PARTICIPATING ORGANIZATIONS BANKING / INSURANCE Pierce County Seattle Children's Aviation Technical Services, Inc. Community Health Plan of Washington Port of Everett The Doctors Clinic+ Carlile Transportation First Choice Health Port of Seattle The Everett Clinic Cascade Public Media - KCTS 9 Harborstone Credit Union Port of Tacoma The Polyclinic Clark Nuber Laird Norton Wealth Management Seattle Aquarium UW Physicians CRISTA Ministries Mutual of Enumclaw Insurance Seattle Housing Authority Virginia Mason Medical Center CTI BioPharma Corp. Seattle Pacifi c University Davis Wright Tremaine LLP Company MANUFACTURING / TECHNOLOGY Premera Blue Cross Seattle Public Schools ECONET Algas-SDI International, LLC Sound Credit Union Seattle University Emerald Queen Hotel & Casinos American Seafoods Company Symetra Financial Snohomish County + FareStart Applied Technical Services Washington Health Benefi t Exchange Sno-Isle Libraries Foster Pepper PLLC Astronics Advanced Electronic Systems Tacoma-Pierce County Health GeoEngineers, Inc. DISTRIB / WHOLESALE / RETAIL Commencement Bay Corrugated Department+ Hart Crowser, Inc. Concrete Technology Corporation Brooks Sports, Inc. The Northwest School Holland America Line Inc. Digital Control Incorporated Burkhart Dental Supply University of Puget Sound Horizon Air Exotic Metals Forming Company LLC Coinstar, LLC University of Washington KPFF Consulting Engineers Geonerco Management, LLC Gensco Inc. Woodland Park Zoo LeMay - America's Car Museum GM Nameplate, Inc. Nordstrom, Inc. Lynden Incorporated HEALTHCARE Hartung Glass Industries Recreational Equipment, Inc. (REI) Milliman, Inc. Benaroya Research Institute Homecare Products, Inc. Savers, Inc. Moss Adams LLP Bloodworks Northwest Kaas Tailored Toysmith Pacifi c Northwest Ballet Center for Infectious Disease Madrona Specialty Foods Wireless Advocates Perkins Coie LLP Research Microscan GOVERNMENT / EDUCATION Puget Sound Energy CHI Franciscan Health Nabtesco Aerospace, Inc. -

Department of Justice Antitrust Division

Tuesday, June 10, 2008 Part III Department of Justice Antitrust Division United States v. Abitibi-Consolidated Inc. et al.; Response to Public Comment on the Proposed Final Judgment; Notice VerDate Aug<31>2005 17:35 Jun 09, 2008 Jkt 214001 PO 00000 Frm 00001 Fmt 4717 Sfmt 4717 E:\FR\FM\10JNN2.SGM 10JNN2 rwilkins on PROD1PC63 with NOTICES2 32834 Federal Register / Vol. 73, No. 112 / Tuesday, June 10, 2008 / Notices DEPARTMENT OF JUSTICE Judgment after the Comment and this the course of the Department’s Response have been published in the investigation into the proposed merger, Antitrust Division Federal Register, pursuant to 15 U.S.C. the NAA shared with the investigative 16(d). staff its concerns about the impact of the United States v. Abitibi-Consolidated The United States filed a civil proposed merger on competition; the Inc. et al.; Response to Public antitrust Complaint under Section 15 of investigative staff carefully analyzed its Comment on the Proposed Final the Clayton Act, 15 U.S.C. 25, on concerns and submissions, as well as Judgment October 23, 2007, alleging that the the data, market facts and opinions of Pursuant to the Antitrust Procedures merger of Abitibi-Consolidated other knowledgeable parties. and Penalties Act, 15 U.S.C. 16(b)–(h), Incorporated (‘‘Abitibi’’) and Bowater The Department concluded that the the United States hereby publishes the Incorporated (‘‘Bowater’’) would violate combination of Abitibi and Bowater public comment received on the Section 7 of the Clayton Act, 15 U.S.C. likely would lessen competition in the proposed Final Judgment in United 18.