Newquay Hotel & Holiday Accommodation Market & Planning

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

View in Website Mode

25 bus time schedule & line map 25 Fowey - St Austell - Newquay View In Website Mode The 25 bus line (Fowey - St Austell - Newquay) has 5 routes. For regular weekdays, their operation hours are: (1) Fowey: 6:40 AM - 4:58 PM (2) Newquay: 5:55 AM - 3:55 PM (3) St Austell: 5:58 PM (4) St Austell: 5:55 PM (5) St Stephen: 4:55 PM Use the Moovit App to ƒnd the closest 25 bus station near you and ƒnd out when is the next 25 bus arriving. Direction: Fowey 25 bus Time Schedule 94 stops Fowey Route Timetable: VIEW LINE SCHEDULE Sunday Not Operational Monday 6:40 AM - 4:58 PM Bus Station, Newquay 16 Bank Street, Newquay Tuesday 6:40 AM - 4:58 PM East St. Post O∆ce, Newquay Wednesday 6:40 AM - 4:58 PM 40 East Street, Newquay Thursday 6:40 AM - 4:58 PM Great Western Hotel, Newquay Friday 6:40 AM - 4:58 PM 36&36A Cliff Road, Newquay Saturday 6:40 AM - 4:58 PM Tolcarne Beach, Newquay 12A - 14 Narrowcliff, Newquay Barrowƒeld Hotel, Newquay 25 bus Info Hilgrove Road, Trenance Direction: Fowey Stops: 94 Newquay Zoo, Trenance Trip Duration: 112 min Line Summary: Bus Station, Newquay, East St. Post The Bishops School, Treninnick O∆ce, Newquay, Great Western Hotel, Newquay, Tolcarne Beach, Newquay, Barrowƒeld Hotel, Kew Close, Treloggan Newquay, Hilgrove Road, Trenance, Newquay Zoo, Kew Close, Newquay Trenance, The Bishops School, Treninnick, Kew Close, Treloggan, Dale Road, Treloggan, Polwhele Road, Dale Road, Treloggan Treloggan, Near Morrisons Store, Treloggan, Carn Brae House, Lane, Hendra Terrace, Hendra Holiday Polwhele Road, Treloggan Park, Holiday -

Copyrighted Material

176 Exchange (Penzance), Rail Ale Trail, 114 43, 49 Seven Stones pub (St Index Falmouth Art Gallery, Martin’s), 168 Index 101–102 Skinner’s Brewery A Foundry Gallery (Truro), 138 Abbey Gardens (Tresco), 167 (St Ives), 48 Barton Farm Museum Accommodations, 7, 167 Gallery Tresco (New (Lostwithiel), 149 in Bodmin, 95 Gimsby), 167 Beaches, 66–71, 159, 160, on Bryher, 168 Goldfish (Penzance), 49 164, 166, 167 in Bude, 98–99 Great Atlantic Gallery Beacon Farm, 81 in Falmouth, 102, 103 (St Just), 45 Beady Pool (St Agnes), 168 in Fowey, 106, 107 Hayle Gallery, 48 Bedruthan Steps, 15, 122 helpful websites, 25 Leach Pottery, 47, 49 Betjeman, Sir John, 77, 109, in Launceston, 110–111 Little Picture Gallery 118, 147 in Looe, 115 (Mousehole), 43 Bicycling, 74–75 in Lostwithiel, 119 Market House Gallery Camel Trail, 3, 15, 74, in Newquay, 122–123 (Marazion), 48 84–85, 93, 94, 126 in Padstow, 126 Newlyn Art Gallery, Cardinham Woods in Penzance, 130–131 43, 49 (Bodmin), 94 in St Ives, 135–136 Out of the Blue (Maraz- Clay Trails, 75 self-catering, 25 ion), 48 Coast-to-Coast Trail, in Truro, 139–140 Over the Moon Gallery 86–87, 138 Active-8 (Liskeard), 90 (St Just), 45 Cornish Way, 75 Airports, 165, 173 Pendeen Pottery & Gal- Mineral Tramways Amusement parks, 36–37 lery (Pendeen), 46 Coast-to-Coast, 74 Ancient Cornwall, 50–55 Penlee House Gallery & National Cycle Route, 75 Animal parks and Museum (Penzance), rentals, 75, 85, 87, sanctuaries 11, 43, 49, 129 165, 173 Cornwall Wildlife Trust, Round House & Capstan tours, 84–87 113 Gallery (Sennen Cove, Birding, -

Truro Livestock Market

TRURO LIVESTOCK MARKET MARKET REPORT & WEEKLY NEWSLETTER Wednesday 17th July 2019 “A quieter week with farmers making the most of the fine weather getting ready for harvest…. ….yet over 90 calves forward and a busy sheep section included over 150 cull ewes, and lambs selling to £94” MARKET ENTRIES Please pre-enter stock by Tuesday 3.30pm PHONE 01872 272722 TEXT (Your name & stock numbers) Cattle/Calves 07889 600160 Sheep 07977 662443 This week’s £10 draw winner: Chris Phillips of St. Mawes TRURO LIVESTOCK MARKET LODGE & THOMAS. Report an entry including Tuesday’s “Orange” Market of 17 UTM & OTM prime cattle, 32 cull cows & bulls, 72 store cattle, 93 rearing calves & stirks & 512 finished & store sheep UTM PRIME CATTLE HIGHEST PRICE BULLOCK Each Wednesday the highest price prime steer/heifer sold p/kg will be commission free Auctioneer – Andrew Body A small entry of generally good quality cattle sold well despite the current subdued deadweight prices. Top price of the day was 176p/kg and £1,276 for best of an entry of big South Devon x steers forward from Mr. B.J. Townsend of Mitchell purchased by Messrs. Rapson of Tavistock. Heifers selling to a premium of 170p/kg for a Limousin x from Messrs. W.S. Gay & Son of St. Allen bought by Trevarthens of Roskrow. 6 Steers & 4 Heifers – top 6 prices South Devon x steer to 176p (725kg) for Mr. B.J. Townsend of Mitchell, Newquay South Devon x steer to 174p (691kg) for Mr. B.J. Townsend of Mitchell, Newquay South Devon x steer to 172p (707kg) for Mr. -

CORNWALL. (KELLY's Red Lion Family, Tourist & Commercial Tabb Ell En (Mrs.), Saddler, Fore Street Gavrigan

1074 COLUMB MAJOR. CORNWALL. (KELLY'S Red Lion family, tourist & commercial Tabb Ell en (Mrs.), saddler, Fore street Gavrigan. hotel &posting house ( Chas. Brewer, Tamblyn Thomas, dairyman, Bridg~ The Indian Queens China Clay & Brick proprietor), Forest. See advert TaylorMary(Miss),dress maker,Bank st & Tile Works (A. E. Jonas, propr.), Richards William, surgeon-dentis~ (at- Teagle Thomas, farmer, Tregatillian Postal address, P. 0. Box 8 tends fortnighly), Bank street Tippett William Stacey, mason, Forest Gill John, farmer Rickard Enoder, farmer, Trenouth TonkynArthur,baker &confectr.Fore st Penrose John, blacksmith Rickard Jonathan, farmer, Hall Tonkyn John, butcher, North street Spear Thomas Hicks, farmer Rickard Pascoe, farmer, Pencrennys Tonkyn Murlin, butcher, Union hill . Tamblyn Henry, farmer Rickeard Israel, farmer, Enniswargy Tonkyn William, draper, Fore street Rodliff William, farmer, Rosedinnick TownHall(W.M.Cardell,sec.),Market st Gluvian. Rogers Jn. marine store dlr. Market pl Trebilcock Jas. Pearce, boot m a. Markt. pl Crapp John, jobbing gardener Rogers Mary Jane (Miss), King's Arms Trebilcock Richard, farmer, 'fregaswith Hawkey William, farmer P.H. Fore street Trebilcock Wm. farmr. Lwr.Bospolvans Jenkin Henry Row, mason Rogers Richard J n. tailor, St. Columb rd Tremaine John, auctioneer & valuer Stephens William, farmer Rowe Fredk. farmer, Trevlthick East & yeoman, Fair street Rowe James, farmer, Reterth Tremaine John, farmer & carrier, Lit- Indian Queens. Rowe William, carpenter, Armoury cot tle Retallick .arenton Jas. shopkeeper & shoe maker Rowse Henry Jenkm 1\LA. barrister, Trerise Edward, jun. farmer, Trugo Commons Thomas, farmer Carworgey Truscott Eva (Mrs.), farmer, Treliver Crow le John, farmer Rundle Reuben, farmer, Rosesurrants Truscott John, carpenter, Black Cross Dean Samuel, cowkeeper Rundle Richard, farmer, Tre~oose Truscott Williarn, farmer, Tresaddern Jane Thomas, carpenter St. -

Penarvon House Helford Village • South Cornwall

PENARVON HOUSE HELFORD VILLAGE • SOUTH CORNWALL PENARVON HOUSE HELFORD VILLAGE • SOUTH CORNWALL An extremely special waterfront family home occupying a fabulous elevated position high above the village of Helford and with panoramic waterfront views. With an easy walk down to the centre of the village to make the most of the waterfront lifestyle that the Helford Passage offers, the property enjoys a lovely mature garden and privacy. It is evident that the house has been extremely well built only 14 years ago and since then has been maintained to a very high standard. Entrance hall • Cloakroom • Kitchen/breakfast/dining room Open plan living room • Utility room Principal bedroom with en suite bathroom • 3 guest suites all with bathrooms and garden access • 5th bedroom dormitory/games room Double garage and boiler room Private landscaped garden and terraces Gross Internal floor Area (approx.): 4,435 ft² (412 m²) In all about 0.62 acres (0.25 Ha) Helford ¼ mile • Helston 10 miles • Truro 27 miles (All distances are approximate) These particulars are intended only as a guide and must not be relied upon as statements of fact. Your attention is drawn to the Important Notice on the last page of the text. Penarvon House – For sale freehold The property is ideally positioned off a quiet private lane and yet only a few minutes’ walk down to the village centre itself with its Helford Village Stores and the famous Shipwrights Arms Pub. The property is approached through electric gates into a large parking area with plenty of space for a number of cars or boat trailers. -

(Saints Trails – Perranporth to Newquay) Compulsory Purchase Order 2021

THE CORNWALL COUNCIL (SAINTS TRAILS – PERRANPORTH TO NEWQUAY) COMPULSORY PURCHASE ORDER 2021 The Town and Country Planning Act 1990 Local Government (Miscellaneous Provisions) Act 1976 and the Acquisition of Land Act 1981 The Cornwall Council (in this order called ‘the acquiring authority’) makes the following order — 1 Subject to the provisions of this order, the acquiring authority is under section 226(1)(a) of the Town and Country Planning Act 1990 and section 13 of the Local Government (Miscellaneous Provisions) Act 1976 hereby authorised to purchase compulsorily the land and the new rights over land described in paragraph 2 for the purpose of facilitating the development and improvement of the land for the provision of a new multi user trail between Perranporth and Newquay which will contribute to achieving the promotion or improvement of the economic social and environmental wellbeing of the area. 2 (1) The land authorised to be purchased compulsorily under this order is the land described in the Schedule and delineated and shown coloured pink on maps prepared in duplicate, sealed with the common seal of the acquiring authority and marked: (i) “Map 01 referred to in the Cornwall Council (Saints Trails – Perranporth to Newquay) Compulsory Purchase Order 2021”. (ii) “Map 02 referred to in the Cornwall Council (Saints Trails – Perranporth to Newquay) Compulsory Purchase Order 2021”. (iii) “Map 03 referred to in the Cornwall Council (Saints Trails – Perranporth to Newquay) Compulsory Purchase Order 2021”. (iv) “Map 04 referred to in the Cornwall Council (Saints Trails – Perranporth to Newquay) Compulsory Purchase Order 2021”. (v) “Map 05 referred to in the Cornwall Council (Saints Trails – Perranporth to Newquay) Compulsory Purchase Order 2021”. -

Page 1 Original Ratified and Signed by Chair 11.11.2013...370

S T E W E P A R I S H C O U N C I L Chair of the Parish Council Clerk to the Parish Council Councillor Janet Lockyer [email protected] Ms Rose Hardisty Mill Cottage The Headlands Polmassick School Hill St Ewe Mevagissey ST AUSTELL ST AUSTELL Cornwall PL26 6TH PL26 6HA 01726 842869 M I N U T E S Parish Council Meeting St Ewe Village Hall Monday 14 October 2013 7.00pm – 8.15pm Officers Present:- Parish Cllrs – Chair Cllr Janet Lockyer, Cllr Allan Brooks, Cllr Diane Clemes, Cllr John Dickinson , Cllr Trevor Johns, Cllr Will Richards, Cllr Sam Roberts and Cllr Lynne Tregunna Apologies Received:- Cllr Malcolm Harris – Cornwall Council Cllr Rueben Collins and Cllr Trevor Harman In Attendance:- Rose Hardisty, Clerk Public Participation:- 1 member of the public in attendance 069/13 Declarations of interests • Cllr Will Richards declared he is the applicant re PA12/09805. • Cllr Allan Brooks declared he is an immediate neighbour re PA13/02329. • Cllr Trevor Johns and Cllr Lynne Tregunna declared owning neighbouring land re PA13/07826. 070/13 Previous Minutes The minutes of the parish council meeting held on 9 September 2013, having been circulated with the agendas, were considered a true record and were adopted (proposed JD, seconded WR). Public Participation Ivan Tomlin, agent for the owners of Kilbol County House Hotel, was in attendance to provide councillors with any additional information they might require to make an informed decision on the application for change of use. He stressed that no alterations are proposed and this application is merely to formalise a change of use so that the property can be used/sold as a residential dwelling rather than a commercial hotel. -

Environmentol Protection Report WATER QUALITY MONITORING

5k Environmentol Protection Report WATER QUALITY MONITORING LOCATIONS 1992 April 1992 FW P/9 2/ 0 0 1 Author: B Steele Technicol Assistant, Freshwater NRA National Rivers Authority CVM Davies South West Region Environmental Protection Manager HATER QUALITY MONITORING LOCATIONS 1992 _ . - - TECHNICAL REPORT NO: FWP/92/001 The maps in this report indicate the monitoring locations for the 1992 Regional Water Quality Monitoring Programme which is described separately. The presentation of all monitoring features into these catchment maps will assist in developing an integrated approach to catchment management and operation. The water quality monitoring maps and index were originally incorporated into the Catchment Action Plans. They provide a visual presentation of monitored sites within a catchment and enable water quality data to be accessed easily by all departments and external organisations. The maps bring together information from different sections within Water Quality. The routine river monitoring and tidal water monitoring points, the licensed waste disposal sites and the monitored effluent discharges (pic, non-plc, fish farms, COPA Variation Order [non-plc and pic]) are plotted. The type of discharge is identified such as sewage effluent, dairy factory, etc. Additionally, river impact and control sites are indicated for significant effluent discharges. If the watercourse is not sampled then the location symbol is qualified by (*). Additional details give the type of monitoring undertaken at sites (ie chemical, biological and algological) and whether they are analysed for more specialised substances as required by: a. EC Dangerous Substances Directive b. EC Freshwater Fish Water Quality Directive c. DOE Harmonised Monitoring Scheme d. DOE Red List Reduction Programme c. -

The Boundary Committee for England Electoral Review

SHEET 11, MAP 11 Proposed Electoral Divisions in Newquay r e t MAWGAN-IN-PYDAR CP a W w o r L e t n a a Watergate Bay W e h Holiday Park M g i H n a e M Higher Tregurrian THE BOUNDARY COMMITTEE FOR ENGLAND Farm Tregurrian Tregurrian or Watergate Beach ELECTORAL REVIEW OF CORNWALL Final Recommendations for Electoral Division Boundaries in the Unitary Authority of Cornwall December 2009 Sheet 11 of 20 This map is based upon Ordnance Survey material with the permission of Ordnance Survey on behalf of the Controller of Her Majesty's Stationery Office © Crown copyright. Unauthorised reproduction infringes Crown copyright and may lead to prosecution or civil proceedings. The Electoral Commission GD03114G 2009. KEY UNITARY AUTHORITY BOUNDARY W A PROPOSED ELECTORAL DIVISION BOUNDARY T E R G PARISH BOUNDARY A T E PARISH BOUNDARY COINCIDENT WITH ELECTORAL DIVISION BOUNDARY R O A PARISH WARD BOUNDARY COINCIDENT WITH ELECTORAL DIVISION BOUNDARY D NEWQUAY CENTRAL ED PROPOSED ELECTORAL DIVISION NAME Watergate Bay NEWQUAY CP PARISH NAME NEWQUAY TRETHERRAS PARISH WARD PROPOSED PARISH WARD NAME B 3276 St Mawgan Airfield Scale : 1cm = 0.08500 km Grid interval 1km Tregurrian or Watergate Beach Fruitful Cove WHIPSIDERRY PARISH WARD D A O R E T A G R E T A W Sewage Whipsiderry Beach Works 6 7 2 3 B Trevegue Golf Course Caravan & Camping Park Caravan Park Hendra Paul Porth Island Whipsiderry Towan Head Ca ravan Park Porth Beach Newquay Bay Water Treatment Works Penrose D Porth R A R D N A X E L A Caravan Park & Camping Site D Lusty Glaze A O R E Playing Field -

Ref: LCAA1820

Ref: LCAA7115 Guide £425,000 Trekenning Cottage, Trekenning, St Columb, Nr. Newquay, Cornwall FREEHOLD An exciting opportunity to acquire a 3/4 bedroomed detached period cottage with glorious large south west facing gardens of approximately 0.59 of an acre and the rare asset of a detached 2 BEDROOMED ANNEXE providing ancillary accommodation. Occupying a wonderful quiet rural location convenient for north coast beaches, Newquay and access around the county. 2 Ref: LCAA7115 SUMMARY OF ACCOMMODATION TREKENNING COTTAGE Ground Floor: porch, kitchen opening through to breakfast room with Aga, lounge with two fireplaces (24’1” x 11’), study/bedroom 4, shower room/wc. First Floor: landing, 3 double bedrooms, family bathroom. WREN’S NEST Sitting/dining room/kitchen, inner hall, master bedroom with fitted wardrobe, bedroom 2, shower room/wc plus private garden. Outside: parking for numerous vehicles. Glorious south and west facing rear gardens with large areas of gently sloping lawned gardens interspersed with profusely stocked flowerbeds and borders, mature deciduous trees, fruit trees, composting area, polytunnel, productive fruit cage. In all approximately 0.59 of an acre. 3 Ref: LCAA7115 DESCRIPTION • Trekenning Cottage is a delightful, detached period cottage which occupies a quiet rural yet highly assessible location. • The property occupies a wonderful large garden plot of approximately 0.59 of an acre featuring large lawned gardens bounded by mature tree, shrub and hedge borders backing onto fields with storage sheds, polytunnel, ideal for green fingered plantsmen and families with children alike. • The property has neatly presented 3/4 bedroomed accommodation displaying much character and charm, is well presented yet still offering great scope for further improvement. -

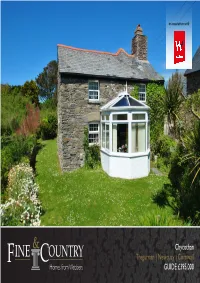

Chycothan Tregurrian | Newquay | Cornwall GUIDE £395 ,000

in association with Chycothan Tregurrian | Newquay | Cornwall GUIDE £395 ,000 CHYCOTHAN TREGURRIAN · NEWQUAY· CORNWALL · TR8 4AD A charming detached character cottage located in the hamlet of Tregurrian, less than half a mile from the beach at popular Watergate Bay and a similar distance from Mawgan Porth. 2 reception rooms, conservatory, kitchen and utility room. 4 first floor bedrooms of a good size, bathroom/wc & shower room/wc • Charming 4 bed detached character cottage • 21ft long master bedroom with vaulted ceiling • Less than half a mile from the beach at Watergate Bay • Oil fired central heating and double glazing • 2 reception rooms, kitchen and a conservatory • Just 4 miles from Newquay & 17 miles from Truro DESCRIPTION The UPVC double glazed conservatory overlooks the well kept Chycothan is a well presented cottage which stands just half a front garden. The garden extends around one side and to the mile from the coast at Watergate Bay between the popular rear where there is a pleasant decked sitting area that enjoys a resort of Newquay and the pretty fishing village of Padstow. distant view down to the sea. The cottage forms part of Tregurrian just 4 miles from Newquay Almost all of the windows are UPVC double glazed (triple glazed and 10 miles from Padstow. The interior is full of traditional in places) and the cottage has an oil fired central heating system, charm and character and there is more accommodation than one the boiler being housed in the downstairs utility room. might expect in the cottage which appears to be one of the oldest in the small hamlet. -

Year Dog Friendly Beaches

COUNCIL OFFICES If you have any queries or comments to make on the dog bans listed or any related matters please telephone the appropriate Council: CARADON DISTRICTCOUNCIL 01579 341000 CARRICK DISTRICT COUNCIL 01872 224400 KERRIER DISTRICT COUNCIL 01209 614000 Photo: Gyllyngvase Beach, Paul Watts NORTH CORNWALL DISTRICT COUNCIL 01208 893333 PENWITH DISTRICT COUNCIL 01736 362341 RESTORMEL BOROUGH COUNCIL 01726 223300 DOG OWNERS CORNWALL 6 BEACH GUIDE FOR 5 i BUDE Widemouth Bay 4 Boscastle i 2 3 BEACHES ON WHICH DOG BANS APPLY Tintagel i Dog bans apply on the following beaches from Easter Day to 1st October unless stated* 1 North i LAUNCESTON Port Isaac Cornwall Caradon Penwith i 1 Cawsand Beach 1 Perranuthnoe PADSTOW Polzeath CAMELFORD 2 Portwrinkle Beach 2 Marazion (Chapel Rock to Long Rock i 3 Millendreath Beach *all year ban Level Crossing) - 2 Rock 4 East Looe Beach *all year ban 3 Penzance Promenade (to Lariggan River) 4 Mousehole *all year ban in harbour Pentire i Carrick 5 Porthcurno - 2 Watergate WADEBRIDGE 1 Tattams Beach 6 Sennen Cove (including harbour) - 2 Bay Bedruthan 2 Porth Beach 7 Porthmeor - 2 Steps BODMIN i Photo: Gyllyngvase Beach, Paul Watts i LISKEARD 3 Summers Beach 8 Porthgwidden 10 9 11 4 Tavern Beach 9 St. Ives Harbour 5 Castle Beach 10 Porthminster - 2 i Caradon 6 Gyllyngvase Beach - 2 11 Carbis Bay - 2 NEWQUAY LOSTWITHIEL i SALTASH 7 Swanpool Beach 12 Hayle Towans (from Hayle River to Restormel 8 Maenporth Beach Black Cliffs) - 2 10 Holywell i i 9 Porthtowan Beach - 2 13 Gwithian (Ceres Rock to Red River) - 2 Perranporth ST.