Audit Report on the Accounts of Defence Services Audit Year 2013-14

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Section Iv District Profiles Awaran

SECTION IV DISTRICT PROFILES AWARAN Awaran district lies in the south of the Balochistan province. Awaran is known as oasis of AGRICULTURAL INFORMATION dates. The climate is that of a desert with hot summer and mild winter. Major crops include Total cultivated area (hectares) 23,600 wheat, barley, cotton, pulses, vegetable, fodder and fruit crops. There are three tehsils in the district: Awaran, Jhal Jhao and Mashkai. The district headquarter is located at Awaran. Total non-cultivated area (hectares) 187,700 Total area under irrigation (hectares) 22,725 Major rabi crop(s) Wheat, vegetable crops SOIL ATTRIBUTES Mostly barren rocks with shallow unstable soils Major kharif crop(s) Cotton, sorghum Soil type/parent material material followed by nearly level to sloppy, moderately deep, strongly calcareous, medium Total livestock population 612,006 textured soils overlying gravels Source: Crop Reporting Services, Balochistan; Agriculture Census 2010; Livestock Census 2006 Dominant soil series Gacheri, Khamara, Winder *pH Data not available *Electrical conductivity (dS m-1) Data not available Organic matter (%) Data not available Available phosphorus (ppm) Data not available Extractable potassium (ppm) Data not available Farmers availing soil testing facility (%) 2 (Based on crop production zone wise data) Farmers availing water testing facility (%) 0 (Based on crop production zone wise data) Source: District Soil Survey Reports, Soil Survey of Pakistan Farm Advisory Centers, Fauji Fertilizer Company Limited (FFC) Inputs Use Assessment, FAO (2018) Land Cover Atlas of Balochistan (FAO, SUPARCO and Government of Balochistan) Source: Information Management Unit, FAO Pakistan *Soil pH and electrical conductivity were measured in 1:2.5, soil:water extract. -

S# BRANCH CODE BRANCH NAME CITY ADDRESS 1 24 Abbottabad

BRANCH S# BRANCH NAME CITY ADDRESS CODE 1 24 Abbottabad Abbottabad Mansera Road Abbottabad 2 312 Sarwar Mall Abbottabad Sarwar Mall, Mansehra Road Abbottabad 3 345 Jinnahabad Abbottabad PMA Link Road, Jinnahabad Abbottabad 4 131 Kamra Attock Cantonment Board Mini Plaza G. T. Road Kamra. 5 197 Attock City Branch Attock Ahmad Plaza Opposite Railway Park Pleader Lane Attock City 6 25 Bahawalpur Bahawalpur 1 - Noor Mahal Road Bahawalpur 7 261 Bahawalpur Cantt Bahawalpur Al-Mohafiz Shopping Complex, Pelican Road, Opposite CMH, Bahawalpur Cantt 8 251 Bhakkar Bhakkar Al-Qaim Plaza, Chisti Chowk, Jhang Road, Bhakkar 9 161 D.G Khan Dera Ghazi Khan Jampur Road Dera Ghazi Khan 10 69 D.I.Khan Dera Ismail Khan Kaif Gulbahar Building A. Q. Khan. Chowk Circular Road D. I. Khan 11 9 Faisalabad Main Faisalabad Mezan Executive Tower 4 Liaqat Road Faisalabad 12 50 Peoples Colony Faisalabad Peoples Colony Faisalabad 13 142 Satyana Road Faisalabad 585-I Block B People's Colony #1 Satayana Road Faisalabad 14 244 Susan Road Faisalabad Plot # 291, East Susan Road, Faisalabad 15 241 Ghari Habibullah Ghari Habibullah Kashmir Road, Ghari Habibullah, Tehsil Balakot, District Mansehra 16 12 G.T. Road Gujranwala Opposite General Bus Stand G.T. Road Gujranwala 17 172 Gujranwala Cantt Gujranwala Kent Plaza Quide-e-Azam Avenue Gujranwala Cantt. 18 123 Kharian Gujrat Raza Building Main G.T. Road Kharian 19 125 Haripur Haripur G. T. Road Shahrah-e-Hazara Haripur 20 344 Hassan abdal Hassan Abdal Near Lari Adda, Hassanabdal, District Attock 21 216 Hattar Hattar -

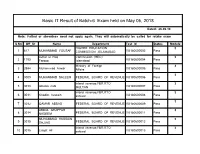

Basic IT Result of Batch-6 Exam Held on May 05, 2018

Basic IT Result of Batch-6 Exam held on May 05, 2018 Dated: 26-06-18 Note: Failled or absentees need not apply again. They will automatically be called for retake exam S.No Off_Sr Name Department Test Id Status Module HIGHER EDUCATION 3 1 617 MUHAMMAD YOUSAF COMMISSION ,ISLAMABAD VU180600002 Pass Azhar ul Haq Commission (HEC) 3 2 1795 Farooq Islamabad VU180600004 Pass Ministry of Foreign 3 3 2994 Muhammad Anwar Affairs VU180600005 Pass 3 4 3009 MUHAMMAD SALEEM FEDERAL BOARD OF REVENUE VU180600006 Pass inland revenue,FBR,RTO 3 5 3010 Ghulan nabi MULTAN VU180600007 Pass inland revenue,FBR,RTO 3 6 3011 Khadim hussain sahiwal VU180600008 Pass 3 7 3012 QAMAR ABBAS FEDERAL BOARD OF REVENUE VU180600009 Pass ABDUL GHAFFAR 3 8 3014 NADEEM FEDERAL BOARD OF REVENUE VU180600011 Pass MUHAMMAD HUSSAIN 3 9 3015 SAJJAD FEDERAL BOARD OF REVENUE VU180600012 Pass inland revenue,FBR,RTO 3 10 3016 Liaqat Ali sahiwal VU180600013 Pass inland revenue,FBR,RTO 3 11 3017 Tariq javed sahiwal VU180600014 Pass 3 12 3018 AFTAB AHMAD FEDERAL BOARD OF REVENUE VU180600015 Pass Basic IT Result of Batch-6 Exam held on May 05, 2018 Dated: 26-06-18 Muhammad inam-ul- inland revenue,FBR,RTO 3 13 3019 haq MULTAN VU180600016 Pass Ministry of Defense (Defense Division) 3 Rawalpindi. 14 4411 Asif Mehmood VU180600018 Pass 3 15 4631 Rooh ul Amin Pakistan Air Force VU180600022 Pass Finance/Income Tax 3 16 4634 Hammad Qureshi Department VU180600025 Pass Federal Board Of Revenue 3 17 4635 Arshad Ali Regional Tax-II VU180600026 Pass 3 18 4637 Muhammad Usman Federal Board Of Revenue VU180600027 -

Complete File Vol 18 Number 1.Cdr

ORIGINAL ARTICLE THE DEVELOPMENT OF CORONAVIRUS ANXIETY SCALE IN URDU (CASU) SADIQ HUSSAIN1, SABIH AHMAD2 1Karakoram International University Gilgit 2Combined Military Hospital, Kharian Cantt CORRESPONDENCE: DR. SABIH AHMAD E-mail: [email protected] Submitted: February 03, 2021 Accepted: March 13, 2021 ABSTRACT INTRODUCTION OBJECTIVE The COVID-19 pandemic that started in late 2019 and engulfed the world by We aimed at developing an instrument to screen anxiety the first three months of 2020, caused a lot of unprecedented panic and symptoms related to Covid-19, in Urdu language. anxiety1. Not just the exposure, fear of exposure, but also the overwhelming information on the social media, that changed rapidly, thus added to the STUDY DESIGN uncertainty2. And then the quarantines and lockdowns world over, added insult to injury. Uncertainty about jobs and financial problems further A descriptive study. aggravated the problem. PLACE AND DURATION OF THE STUDY The anxiety and fear thus caused did not leave any societal entity unaffected. 3 Combined Military Hospital, Kharian Cantonment, All ages, genders and professions were affected . Such psychiatric Pakistan, from September to December 2020. manifestations had remained under the attention of mental health workers. A need had emerged to quantify the presence of such signs and symptoms. SUBJECTS AND METHODS The symptoms mostly ranged from stress, worry, to fear, uncertainty, restlessness, dread, and other similar manifestations of anxiety syndrome4. A six step approach was taken up for development of the Being threatened by illness and death, and feeling vulnerable had been a scale. A pilot study was conducted on the final scale, hallmark of previous pandemics too5. -

Presentation of Early Onset Psoriasis in Comparison with Late Onset Psoriasis: a Clinical Study from Pakistan

Original PPresentationresentation ooff eearlyarly oonsetnset ppsoriasissoriasis inin ccomparisonomparison Article wwithith llateate oonsetnset ppsoriasis:soriasis: A cclinicallinical sstudytudy ffromrom PPakistanakistan AAmermer EEjaz,jaz, NNaeemaeem RRazaaza1, NNadiaadia IIftikharftikhar2, AArshirshi IIftikhar,ftikhar, MMohammadohammad FarooqFarooq3 Consultant Dermatologist, ABSTRACT Combined Military Hospital, Kharian Cantonment, Pakistan. Background: Early onset psoriasis and late onset psoriasis are known to have different clinical 1Consultant Dermatologist, PAF Hospital Faisal, Karachi, patterns in Caucasian population. However, there is paucity of data among Asian patients. Pakistan; 2Consultant Aims: To compare the clinical presentation of early onset psoriasis with late onset psoriasis Dermatologist, Military in Pakistani population. Methods: During the study period, participating dermatologists Þ lled a Hospital, Rawalpindi, Pakistan; pre-tested questionnaire for each patient with psoriasis on Þ rst encounter. The questionnaire 3 Consultant Dermatologist, Combined Military Hospital, incorporated information regarding clinical and demographic features of psoriasis including Attock Cantonment, Pakistan age of onset, clinical type of psoriasis, nail or joint involvement, and PASI score. Patients were then divided into early onset (age of onset <30 years, group I) and late onset (age of onset Address for ≥30 years, group II) psoriasis. Results: Five hundred and Þ fteen questionnaires were Þ lled correspondence: and returned for evaluation. There was no statistically signiÞ cant difference in both groups with Dr. Amer Ejaz, regards to gender, family history (P = 0.09), nail (P = 0.69) and joint (P = 0.74) involvement, Consultant Dermatologist, disease severity (P = 0.68), and clinical type of psoriasis (P = 0.06). No signiÞ cant difference Combined Military Hospital, Kharian Cantonment, Pakistan. between disease severities measured by PASI score was observed in the two groups E-mail: [email protected] (P = 0.68). -

PAKISTAN: REGIONAL RIVALRIES, LOCAL IMPACTS Edited by Mona Kanwal Sheikh, Farzana Shaikh and Gareth Price DIIS REPORT 2012:12 DIIS REPORT

DIIS REPORT 2012:12 DIIS REPORT PAKISTAN: REGIONAL RIVALRIES, LOCAL IMPACTS Edited by Mona Kanwal Sheikh, Farzana Shaikh and Gareth Price DIIS REPORT 2012:12 DIIS REPORT This report is published in collaboration with DIIS . DANISH INSTITUTE FOR INTERNATIONAL STUDIES 1 DIIS REPORT 2012:12 © Copenhagen 2012, the author and DIIS Danish Institute for International Studies, DIIS Strandgade 56, DK-1401 Copenhagen, Denmark Ph: +45 32 69 87 87 Fax: +45 32 69 87 00 E-mail: [email protected] Web: www.diis.dk Cover photo: Protesting Hazara Killings, Press Club, Islamabad, Pakistan, April 2012 © Mahvish Ahmad Layout and maps: Allan Lind Jørgensen, ALJ Design Printed in Denmark by Vesterkopi AS ISBN 978-87-7605-517-2 (pdf ) ISBN 978-87-7605-518-9 (print) Price: DKK 50.00 (VAT included) DIIS publications can be downloaded free of charge from www.diis.dk Hardcopies can be ordered at www.diis.dk Mona Kanwal Sheikh, ph.d., postdoc [email protected] 2 DIIS REPORT 2012:12 Contents Abstract 4 Acknowledgements 5 Pakistan – a stage for regional rivalry 7 The Baloch insurgency and geopolitics 25 Militant groups in FATA and regional rivalries 31 Domestic politics and regional tensions in Pakistan-administered Kashmir 39 Gilgit–Baltistan: sovereignty and territory 47 Punjab and Sindh: expanding frontiers of Jihadism 53 Urban Sindh: region, state and locality 61 3 DIIS REPORT 2012:12 Abstract What connects China to the challenges of separatism in Balochistan? Why is India important when it comes to water shortages in Pakistan? How does jihadism in Punjab and Sindh differ from religious militancy in the Federally Administered Tribal Areas (FATA)? Why do Iran and Saudi Arabia matter for the challenges faced by Pakistan in Gilgit–Baltistan? These are some of the questions that are raised and discussed in the analytical contributions of this report. -

Annexures for Annual Report 2020

List of Annexures Annex A Minutes of the Annual General Meeting held on March 08, 2019 Annex B Detailed Expenditures on Purchase and Establishment of PCATP Head Office Islamabad Annex C Policy guidelines for Online Teaching-Learning and Assessment Implementation Annex D Thesis guidelines for graduating batch during COVID-19 pandemic Annex E Inclusion of PCATP in NAPDHA Annex F Inclusion of role of Architects and Town Planners in the CIDB Bill 2020 Annex G Circulation List for Compliance of PCATP Ordinance IX of 1983 Annex H Status of Institutions Offering Architecture and Town Planning Undergraduate Degree Programs in Pakistan Annex I List of Registered Members and Firms who have contributed towards COVID- 19 fund in PCATP Account Annex J List of Registered Members and Firms who have contributed towards COVID- 19 fund in IAP Account Audited Accounts and Balance Sheet of PCATP General Fund and RHS Annex K Account for the Year 2018-2019 Page | 1 ANNEX A MINUTES OF THE ANNUAL GENERAL MEETING OF THE PAKISTAN COUNCIL OF ARCHITECTS AND TOWN PLANNERS ON FRIDAY, 8th MARCH, 2019, AT RAMADA CREEK HOTEL, KARACHI. In accordance with the notice, the Annual General Meeting of the Pakistan Council of Architects and Town Planners was held at 1700 hrs on Friday, 8th March, 2019 at Crystal Hall, Ramada Creek Hotel, Karachi, under the Chairmanship of Ar. Asad I. A. Khan. 1.0 AGENDA ITEM NO.1 RECITATION FROM THE HOLY QURAN 1.1 The meeting started with the recitation of Holy Quran, followed by playing of National Anthem. 1.2 Ar. FarhatUllahQureshi proposed that the house should offer Fateha for PCATP members who have left us for their heavenly abode. -

South Central Asia

Volume I Section IV-V - South Central Asia Afghanistan ALP - Fiscal Year 2013 Department of Defense Training Course Title Qty Training Location Student's Unit US Unit - US Qty Total Cost Start Date End Date ALC ALP Scholarship 1 DLIELC, LACKLAND AFB TX Ministry of Defense DLIELC, LACKLAND AFB TX $17,120 9/10/2012 1/18/2013 Oral PROF AV ALP Scholarship 1 DLIELC, LACKLAND AFB TX Ministry of Defense DLIELC, LACKLAND AFB TX $12,548 12/31/2012 6/21/2013 Fiscal Year 2013 Program Totals 2 $29,668 CTFP - Fiscal Year 2013 Department of Defense Training Course Title Qty Training Location Student's Unit US Unit - US Qty Total Cost Start Date End Date ALC Specialized English Training Only 1 DLIELC, LACKLAND AFB TX National Directorate of Security DLIELC, LACKLAND AFB TX $10,464 1/14/2013 3/8/2013 American Language Course General English Training Only 1 DLIELC, LACKLAND AFB TX National Directorate of Security DLIELC, LACKLAND AFB TX $10,980 12/17/2012 1/11/2013 American Language Course General English Training Only 1 DLIELC, LACKLAND AFB TX National Directorate of Security DLIELC, LACKLAND AFB TX $20,705 1/14/2013 4/5/2013 American Language Course General English Training Only 2 DLIELC, LACKLAND AFB TX Ministry of Defense DLIELC, LACKLAND AFB TX $28,702 7/22/2013 9/6/2013 American Language Course General English Training Only 1 DLIELC, LACKLAND AFB TX National Directorate of Security DLIELC, LACKLAND AFB TX $15,036 7/22/2013 9/6/2013 American Language Course GET and SET 2 DLIELC, LACKLAND AFB TX National Directorate of Security DLIELC, LACKLAND AFB -

Company Profile

Shaheen Medical Services, Opposite Benazir Bhutto Airport Chaklala, Rawalpindi Phone: +92-51-5405270,5780328, PAF: 3993 http://shaheenmedicalservices.com / Email: [email protected] Page 1 MISSION Gain trust of our valuable clients, with most efficient and ethical services, by providing quality pharmaceutical products with maximum shelf life procured from authentic sources. VISION SMS is continuously striving to be recognized as a leading distributor of pharmaceutical products by focusing on efficient and ethical delivery of services. GOAL To work in collaboration with our worthy partners, to provide high value and premium quality pharmaceutical products to our clients, in order to sustain long-term business relationship. Shaheen Medical Services, Opposite Benazir Bhutto Airport Chaklala, Rawalpindi Phone: +92-51-5405270,5780328, PAF: 3993 http://shaheenmedicalservices.com / Email: [email protected] Page 2 INTRODUCTION Shaheen Foundation, Pakistan Air Force (PAF), was established in 1977 under the Charitable Endowment Act, 1890, essentially to promote welfare for the benefit of serving and retired PAF personnel including its civilian’s employees and their dependents, and to this end generates funds through industrial and commercial enterprises. Since then, it has launched a number of profitable ventures to generate funds necessary for financing the Foundation’s welfare activities. Shaheen Medical Services (SMS) was established to fulfill the pharmaceutical and surgical requirement of Armed forces and public/private sector. Since it’s founding in Rawalpindi in 1996, Shaheen Medical Services, Shaheen Foundation, PAF has become the leading distributor of Pharmaceuticals & Surgical products in Pakistan Air Force Hospitals, with offices in 22 cities nationwide. SMS is a registered member of Rawalpindi Chamber of Commerce and Industries (RCC&I), Export Promotion Bureau (EPB) of Pakistan and Director General Defense Purchase (DGDP). -

Downloaded from the Website Including Documentaries

Year Book Ministry of ofInformationof Information Information Technology Technology Technology & Telecommunication & &Telecommunication Telecommunication 2015-2016 Government of Pakistan Ministry of Information Technology and Telecommunication (IT and Telecom Division) Year Book 2015-2016 Page 1 Year Book Ministry of ofInformationof Information Information Technology Technology Technology & Telecommunication & &Telecommunication Telecommunication 2015-2016 FOREWORD Ministry of Information Technology and Telecommunications (MoITT) is entrusted to formulate policies aimed at improving National Information and Communications Technology (ICT) infrastructure and services, to transform Pakistan into a knowledge-based economy by ensuring provision of reliable and affordable Information and Communications Technology enabled services. Rule 25 of the Rules of Business, 1973 requires every Division/Ministry of the Federal Government to prepare a Year Book on its activities and achievements during the year. The Year Book is prepared for information of the Cabinet as well as general public. The annual publication of this Year Book is also recognition of the public’s right to information. The Ministry of Information Technology and Telecommunications, therefore, in compliance with its responsibility has prepared its Year Book for the year 2015-16. The primary objective of this Book is to keep the public informed regarding the important activities undertaken by this ministry and organizations/companies/departments etc under its administrative control. It is sincerely hoped that this Year Book will serve as a useful reference for public, researchers, and scholars interested in activities carried out by MOITT in this year. --- (Rizwan Bashir Khan) Secretary IT Page 2 Year Book Ministry of ofInformationof Information Information Technology Technology Technology & Telecommunication & &Telecommunication Telecommunication 2015-2016 TABLE OF CONTENTS Contents Pages 1. -

Pakistan 2019 International Religious Freedom Report

PAKISTAN 2019 INTERNATIONAL RELIGIOUS FREEDOM REPORT Executive Summary The constitution establishes Islam as the state religion and requires all provisions of the law to be consistent with Islam. The constitution states, “Subject to law, public order, and morality, every citizen shall have the right to profess, practice, and propagate his religion.” It also states, “A person of the Qadiani group or the Lahori group (who call themselves Ahmadis), is a non-Muslim.” The courts continued to enforce blasphemy laws, punishment for which ranges from life in prison to execution for a range of charges, including “defiling the Prophet Muhammad.” According to civil society reports, there were at least 84 individuals imprisoned on blasphemy charges, at least 29 of whom had received death sentences, as compared with 77 and 28, respectively, in 2018. The government has never executed anyone specifically for blasphemy. According to data provided by nongovernmental organizations (NGOs), police registered new blasphemy cases against at least 10 individuals. Christian advocacy organizations and media outlets stated that four Christians were tortured or mistreated by police in August and September, resulting in the death of one of them. On January 29, the Supreme Court upheld its 2018 judgment overturning the conviction of Asia Bibi, a Christian woman sentenced to death for blasphemy in 2010. Bibi left the country on May 7, after death threats made it unsafe for her to remain. On September 25, the Supreme Court overturned the conviction of a man who had spent 18 years in prison for blasphemy. On December 21, a Multan court sentenced English literature lecturer Junaid Hafeez to death for insulting the Prophet Muhammad after he had spent nearly seven years awaiting trial and verdict. -

15 June 2020 [RASC COMPANY ESTABLISHMENT 1944

15 June 2020 [R.A.S.C. COMPANY ESTABLISHMENT 1944 - 1945] The Royal Army Service Corps The Royal Army Service Corps (R.A.S.C.) was the branch of the British Army responsible for the distribution of supplies to units in the field. Likewise, in the Indian Army, the Royal Indian Army Service Corps (R.I.A.S.C.) performed the same function. Both corps had the additional responsibility of transporting supplies as far as the front line, where individual units took over responsibility. The corps were also responsible for the administration and maintenance of barracks and quarters. The R.A.S.C. and R.I.A.S.C. did not issue or maintain weapons, military equipment, or ammunition as this was the responsibility of the Royal Army Ordnance Corps. However, the R.A.S.C. and R.I.A.S.C. did transport ammunition from Base Ordnance Depots to Forward Ammunition Points. It was also the task of the two corps to transport and distribute Petrol, Oil and Lubricants, often known simply as ‘POL’. Just as important, the R.A.S.C. and R.I.A.S.C. were responsible for supplying the food and water to keep the army personnel and animals fed and watered. The corps provided Field Butchery, Field Bakery and Cattle Conducting Sections. The two corps used vehicles, mules, and aircraft to keep the supplies moving. Railway and shipping transportation were the responsibility of the Royal Engineer Movements and Transportation Branch. In the 1700’s, when the British Army developed into a national army as we know it today, transport was provided by civilian contractors.