COVID-19 and Pakistan: the Economic Fallout

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

P14 3 Layout 1

THURSDAY, AUGUST 10, 2017 SPORTS Ranatunga urges ICC to probe Sri Lanka chief COLOMBO: Former skipper Arjuna office at SLC, as well as at the Asian Cricket Ranatunga has blamed Sri Lanka’s string of Council and ICC. “I deny any involvement humiliating defeats on the country’s cricket personally, directly or indirectly with gam- chief and demanded his investigation by ing business,” Sumathipala told AFP. the International Cricket Council. In what could be the opening shots of a new bid to ‘THEY MESSED UP EVERYTHING’ head Sri Lanka Cricket, Ranatunga, 53, told He also slammed Ranatunga, Sri Lanka’s AFP there was no “proper discipline” in the minister of petroleum, for accusing President national team which has had a horror run Maithripala Sirisena’s government of failing of results. to protect the game. “If he wants to criticise The team lost by an innings and 53 runs the government, he must first resign,” in the second Test against India on Sunday, Sumathipala, said adding that allegations are after being crushed in the first match by frequently made against the board when the 304 runs. They are now fighting to avoid a national team performs badly. whitewash in the three-Test series. Sri “Every time the game is affected at the Lanka also suffered an early exit from the middle, Sri Lanka cricketers are not per- Champions Trophy, and lost a one-day forming to the expectation, we hear this series at home to bottom ranked kind of noise coming from the same quar- Zimbabwe last month. Ranatunga accused ter,” Sumathipala said. -

Pakistan Media Legal Review 2019

Pakistan Media Legal Review 2019 Coercive Censorship, Muted Dissent: Pakistan Descends into Silence Annual Review of Legislative, Legal and Judicial Developments on Freedom of Expression, Right to Information and Digital Rights in Pakistan Pakistan Media Legal Review 2019 This report was voluntarily produced by the Institute for Research, Advocacy and Development (IRADA), an Islamabad-based independent research and advocacy organization focusing on social development and civil liberties, with the contribution of Faiza Hassan as research assistant and Muhammad Aftab Alam and Adnan Rehmat as lead researchers. Table of Contents Executive Summary ............................................................................................... 1 Attempts to Radicalize Media Regulatory Framework ....................................... 3 Pakistan Media Regulatory Authority (PMRA) .........................................................................3 Media Tribunals ...................................................................................................................................4 i Journalistic and Media Freedoms ........................................................................ 6 Pakistan Media Legal Review 2019 Media Legal Pakistan Murders of Journalists ......................................................................................................................6 Serious Incidents of Harassment and Attacks on Journalists and Media .......................7 Criminal Cases Against Journalists ...............................................................................................8 -

Governance Structure of the State Bank of Pakistan

Governance Structure of the State Bank of Pakistan The State Bank of Pakistan (SBP) is incorporated under the State Bank of Pakistan Act, 1956, which gives the Bank the authority to function as the central bank of the country. The Act mandates the Bank to regulate the monetary and credit system of Pakistan and to foster its growth in the best national interest with a view to securing monetary stability and fuller utilization of the country’s productive resources. Central Board of Directors The State Bank of Pakistan is governed by an independent Board of Directors, which is responsible for the general superintendence and direction of the affairs of the Bank. The Board is chaired by the Governor SBP and comprises of 8 non-executive Directors and Secretary Finance to the Federal Government. The Governor SBP is also the Chief Executive Officer of the Bank and manages the affairs of the Bank on behalf of the Central Board. The SBP Act, 1956 (as amended) stipulates that the Board members should be eminent professionals from the fields of economics, finance, banking and accountancy and shall have no conflict of interest with the business of the Bank. During FY13, all 7 vacant positions on the Board were filled through appointment of Directors by the Federal Government. Out of these 7 newly appointed Directors, 5 were appointed on February 26, 2013 followed by 2 appointments in March, 2013. Brief profile of the members of the Board is given on pages 9-10. The current composition of the Board brings a diverse range of professional expertise, adding value to the deliberations. -

Prospects of Youth Radicalization in Pakistan

THE BROOKINGS PROJECT ON U.S. RELATIONS W ITH THE ISLA M IC WORLD ANALYSIS PAPER Number 14, October 2008 PROS P ECTS OF Y OUTH RADICALIZATION IN PAKISTAN Implications for U.S. Policy at BROOKINGS Moeed Yusuf THE BROOKINGS INSTITUTION 1775 MASSACHUSETTS AVE ., NW WASHINGTON , D.C. 20036-2103 www.brookings.edu THE BROOKINGS PROJECT ON U.S. RELATIONS WITH THE ISLAMIC WORLD ANALYSIS PAPER Number 14, October 2008 PROS P ECTS OF Y OUTH RADICALIZATION IN PAKISTAN : Implications for U.S. Policy at BROOKINGS Moeed Yusuf ACKNOWLEDGMENTS would like to thank Stephen P. Cohen for help- I ing me conceptualize the idea and mentoring the project and Ejaz Hadier for providing continu- ous input on the manuscript. I am also grateful to Shanza Khan and Dhruva Jaishankar for their com- ments. THE SA B AN CENTER FOR MIDDLE EAST POLIC Y AT BROOKINGS III AB OUT THE AUTHOR Moeed Yusuf is currently a Fellow at the His research interests include: youth demographics Frederick S. Pardee Center for the Study of the in Pakistan, prospects for radicalization in Pakistan, Longer-Range Future at Boston University. He is Pakistan’s national security narrative, civil-military also a Doctoral student and Teaching Fellow at the relations, Pakistan’s nuclear program, the stability- University’s Political Science Department. Con- instability paradox, strategic balance between Paki- currently, Mr. Yusuf serves as a Research Fellow at stan and India, global non-proliferation regime, the Strategic and Economic Policy Research, Pakistan. He Kashmir dispute, and United States strategic inter- has previously been at the Brookings Institution as ests in South Asia. -

Pakistan 2013 International Religious Freedom Report

PAKISTAN 2013 INTERNATIONAL RELIGIOUS FREEDOM REPORT Executive Summary The government’s respect for and protection of the right to religious freedom remained poor. The government’s limited capacity and will to investigate or prosecute the perpetrators of attacks against religious minorities allowed a climate of impunity to persist. The constitution establishes Islam as the state religion, and it requires that laws be consistent with Islam. The constitution states, “subject to law, public order, and morality, every citizen shall have the right to profess, practice, and propagate his religion.” Some government practices and laws, however, limited freedom of religion, particularly for religious minorities. Authorities continued to enforce blasphemy laws and laws designed to marginalize the Ahmadiyya Muslim community. During the year, 34 new cases were registered under the blasphemy law, and 18 Ahmadis were arrested in matters related to their faith, although at least one death sentence for blasphemy was overturned, and the government has yet to carry out a death sentence for blasphemy. Nevertheless, at least 17 people are awaiting execution for blasphemy, and at least 20 others are serving life sentences. These laws continued to restrict religious freedom, and remained the most visible symbols of religious intolerance. Incidents including the September 22 suicide bombings of the All Saints Church in Peshawar, the March 9 mob attack on the Joseph Colony Christian community in Lahore, and twin bombings targeting the Hazara Shia community in Quetta on January 10 highlighted the government’s failure to provide adequate security, including to religious minority communities. There were continued reports of law enforcement personnel abusing members of religious minorities and persons accused of blasphemy while in custody. -

Pakistan Response Towards Terrorism: a Case Study of Musharraf Regime

PAKISTAN RESPONSE TOWARDS TERRORISM: A CASE STUDY OF MUSHARRAF REGIME By: SHABANA FAYYAZ A thesis Submitted to the University of Birmingham For the degree of DOCTOR OF PHILOSOPHY Department of Political Science and International Studies The University of Birmingham May 2010 University of Birmingham Research Archive e-theses repository This unpublished thesis/dissertation is copyright of the author and/or third parties. The intellectual property rights of the author or third parties in respect of this work are as defined by The Copyright Designs and Patents Act 1988 or as modified by any successor legislation. Any use made of information contained in this thesis/dissertation must be in accordance with that legislation and must be properly acknowledged. Further distribution or reproduction in any format is prohibited without the permission of the copyright holder. ABSTRACT The ranging course of terrorism banishing peace and security prospects of today’s Pakistan is seen as a domestic effluent of its own flawed policies, bad governance, and lack of social justice and rule of law in society and widening gulf of trust between the rulers and the ruled. The study focused on policies and performance of the Musharraf government since assuming the mantle of front ranking ally of the United States in its so called ‘war on terror’. The causes of reversal of pre nine-eleven position on Afghanistan and support of its Taliban’s rulers are examined in the light of the geo-strategic compulsions of that crucial time and the structural weakness of military rule that needed external props for legitimacy. The flaws of the response to the terrorist challenges are traced to its total dependence on the hard option to the total neglect of the human factor from which the thesis develops its argument for a holistic approach to security in which the people occupy a central position. -

Pakistan's Domestic Political Developments

Order Code RS21299 Updated January 5, 2003 CRS Report for Congress Received through the CRS Web Pakistan’s Domestic Political Developments: Issues for Congress K. Alan Kronstadt Analyst in Asian Affairs Foreign Affairs, Defense, and Trade Division Summary October 2002 elections in Pakistan nominally fulfilled President Gen. Pervez Musharraf’s promise to restore the National Assembly that was dissolved in the wake of his extra-constitutional seizure of power in October 1999. A pro-military alliance won a plurality of seats, while a coalition of Islamist parties made a surprisingly strong showing. Musharraf supporter M.Z. Jamali became Pakistan’s new Prime Minister. The civilian government was hamstrung for more than one year by fractious debate over the legitimacy of Musharraf’s August 2002 changes to the country’s constitution and his continued status as Army Chief and President. A surprise December 2003 agreement between Musharraf and the Islamist opposition ended the deadlock by bringing the constitutional changes before Parliament and by eliciting a promise from Musharraf to resign his military commission before 2005. Secular opposition parties strongly criticized the arrangement as undemocratic. The 1999 coup triggered restrictions on U.S. foreign assistance, restrictions waived in October 2001 (under P.L. 107-57) and again in March 2003 by President Bush. In November 2003 (P.L. 108-106), Congress extended the President’s waiver authority through FY2004. In response to continued perceived anti-democratic practices in Islamabad, there is legislation in the 108th Congress (H.R. 1403) aimed at restoring aid restrictions through removal of the U.S. President’s waiver authority. -

![Pagina 1 Van 2 Business Recorder [Pakistan's First Financial Daily] 27](https://docslib.b-cdn.net/cover/5586/pagina-1-van-2-business-recorder-pakistans-first-financial-daily-27-1405586.webp)

Pagina 1 Van 2 Business Recorder [Pakistan's First Financial Daily] 27

Business Recorder [Pakistan's First Financial Daily] pagina 1 van 2 Friday March 27, 2009 Back Issues [From 2004-01-01] 2009-03-27 Get LATEST : Bomb at Khyber Agency mosque, at least 45 de- Top Stories . Business & Economy - Stocks & Bonds Monsanto may be allowed to introduce hybrid, Bt Jobs in pakistan General News cottonseed varieties Middle East Job Editorials ASMA RAZAQ Opportunities. Upload ISLAMABAD (March 19 2009): The Economic Co-ordination Articles & Letters your Resume now: Free! Committee (ECC) of the Cabinet may approve plan to allow www.Bayt.com Cotton & Textiles Monsanto introduce both hybrid and Bt cottonseed varieties in Pakistan. Reliable sources told Business Recorder here on Agriculture & Allied Wednesday that the Ministry of Food and Agriculture (Minfa) had Fuel & Energy decided to move a summary to ECC meeting on Thursday (March Karachi Hotels Money & Banking 19) for giving permission to Monsanto to introduce hybrid and the Bt cotton seed varieties in Pakistan. One-stop source to Telecommunication compare hotel room rates IT & Computers According to the sources, after the ECCs approval, an agreement from across the web. would be signed between the government and Monsanto. The www.OneTime.com Taxation government had signed a LoI with Monsanto a year ago to Company News collaborate in biotechnology. Monsanto cotton traits are currently approved in 13 countries of the world. Stock & Funds Rates & Schedules Research Sports Sources said that Monsanto had demanded 16 dollars per acre as Get Insights with Weather royalty, which, according to Pakistan, was a huge amount. The Morningstar. 4000 government was not ready to pay even a single penny to Monsanto Reports with Free 14 Day that is why even after signing the LoI, Pakistan has not finalised the The Rupee agreement with Monsanto. -

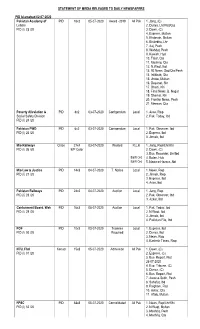

Statement of Media Released to Daily Newspapers Pid

STATEMENT OF MEDIA RELEASED TO DAILY NEWSPAPERS PID Islamabad 02-07-2020 Pakistan Academy of PID 18x2 05-07-2020 Award -2019 All Pak 1. Jang, (C) Letters 2. Dunya, Lhr/Fbd/Guj PID (I) 23 /20 3. Dawn, (C) 4. Express, Multan 5. Khabrain, Multan 6. Bhulekha, Lhr 7. Aaj, Pesh 8. Wahdat, Pesh 9. Kawish, Hyd 10. Talar, Qta 11. Mashriq, Qta 12. N.Waqt, Ibd 13. 92 News, Sgd/Qta/Pesh 14. Intikhab, Qta 15. Jhoke, Multan 16. Deyanat, Skr 17. Dharti, Khi 18. Final News, B. Nagar 19. Shamal, Khi 20. Frontier News, Pesh 21. Meezan, Qta Poverty Alleviation & PID 8x2 03-07-2020 Corrigendum Local 1. Asas, Rwp Social Safety Division 2. Pak. Today, Ibd PID (I) 24 /20 Pakistan PWD PID 6x2 03-07-2020 Corrigendum Local 1. Pak. Observer, Ibd PID (I) 25 /20 2. Express, Ibd 3. Jinnah, Ibd M/o Railways Circle 27x4 03-07-2020 Wanted R.L.K 1. Jang, Rwp/Lhr/Khi PID (I) 26 /20 B/P Color 2. Dawn, (C) 3. Bus. Recorder, Lhr/Ibd B&W Ord 4. Bolan, Hub B&W Ord 5. Nawa-e-Hazara, Abt M/o Law & Justice PID 14x3 04-07-2020 T. Notice Local 1. News, Rwp PID (I) 27 /20 2. Jinnah, Rwp 3. Express, Ibd 4. Asas, Ibd Pakistan Railways PID 24x2 04-07-2020 Auction Local 1. Jang, Rwp PID (I) 28 /20 2. Pak. Observer, Ibd 3. Azkar, Ibd Cantonment Board, Wah PID 16x3 08-07-2020 Auction Local 1. Pak. Today, Ibd PID (I) 29 /20 2. -

PAKISTAN NEWS DIGEST May 2021

May 2021 PAKISTAN NEWS DIGEST May 2021 A Select Summary of News, Views and Trends from the Pakistani Media Prepared by Dr. Zainab Akhter Dr. Nazir Ahmad Mir Dr. Mohammad Eisa Dr. Ashok Behuria MANOHAR PARRIKAR INSTITUTE FOR DEFENCE STUDIES AND ANALYSES 1-Development Enclave, Near USI Delhi Cantonment, New Delhi-110010 PAKISTAN NEWS DIGEST, May 2021 CONTENTS POLITICAL DEVELOPMENTS ........................................................................... 05 ECONOMIC ISSSUES............................................................................................ 06 SECURITY SITUATION ........................................................................................ 10 URDU & ELECTRONIC MEDIA Urdu ............................................................................................................................ 13 Electronic .................................................................................................................... 18 STATISTICS BOMBINGS, SHOOTINGS AND DISAPPEARANCES ...................................... 20 MP-IDSA, New Delhi 1 POLITICAL DEVELOPMENTS Perception management needed, Dr Zia Ul Haque Shamsi, Daily Times, 03 May1 Its has become fashionable to label Pakistan Armed Forces as ‘Assassins’ ‘Land Grabbers’ and ‘King-Makers’ etc. Be it a ‘Journalist’ or the ‘Judge’ or for that matter a ‘Politician’ the language of the charges is nearly the same. Forum may be a ‘Court Room’ ‘Social Media’ or a ‘Press Conference.’ I think it is time to put the things in perspective. Pakistan Armed Forces are -

Cultural Scenario of Pakistan in Democratic and Military Eras (1947-2013)

South Asian Studies A Research Journal of South Asian Studies Vol. 32, No. 1, January – June 2017, pp.67 – 80 Cultural Scenario of Pakistan in Democratic and Military Eras (1947-2013) Saira Siddiqui Government College University, Faisalabad, Pakistan. Syeda Khizra Aslam Government College University, Faisalabad, Pakistan. Muhammad Rashid Khan University of the Punjab, Lahore, Pakistan. ABSTRACT This study investigates a politico-cultural mapping of leisure and life in Pakistan, a country in South Asia, with a political developmental period in historical perspective from its independence in 1947. A classification of ruling eras is done, and accordingly the paper carries its discussion. A few tables are presented to give the percentage of leisure-time spent, and leisure-activities pursued by Pakistani men and women. The data is from nationally represented samples of 2690 respondents in 2009, and 1294 respondents interviewed in 2012 by Gilani Research Foundation, Pakistan. The findings also include statistics from a research by the authors own empirical study of 2013, from a sample of 222 women respondents in Faisalabad City, Punjab, Pakistan. Key Words: Democratic and military eras, Pakistan, leisure and life, recreational facilities Introduction South Asia is one of the most heavily populated places in the world. The countries within its area are Bangladesh, Bhutan, India, Maldives, Nepal, Pakistan, and Sri Lanka (Cultural Geography of South Asia, 2002). Pakistan and Bangladesh in South Asia have Muslim influence, politico-cultural histories of political conflicts, and different civilizations. Pakistan has seen military rule and instability from time to time. The cultural histories of Nepal, Bhutan, Maldives, and Sri Lanka are different. -

The Role of Media in Pakistan Dr

Journal of South Asian and Middle Eastern Studies, 35 :4, Summer 2012. The Role of Media in Pakistan Dr. Nazir Hussain The explosion of information revolution and the proliferation of electronic media have virtually converted the world into a globalized village. Now, information, news and events have no barriers and control to reach anywhere around the world. These happenings reach to every living room instantaneously even before the governments can react and control it. The enhanced role of media has impacted the social, economic and political life. What one thinks, believes and perceives are based on the images shown on the media. It has penetrated the routine life of all individuals; commoners, elites, decision-makers and statesmen. States have often been inclined to use the media as a propaganda tool for political and military purposes. The decades of 1980s and 1990s have for instance witnessed the use of US media for politico-military ends. The projection of Soviet Union as an ‘Evil Empire’, the Saddam saga and the ‘Weapons of Mass Destruction’ and the Osama Bin Laden from ‘Freedom Fighter to a Terrorist’ are some of the examples. However, now the media has come out of the domain of the state controls, it is the financiers, the media houses and the media anchors that make heroes and villains, leaders and terrorists. Therefore, the role of media is growing from an observer to an active player in political decision making. The political leaders and government officials have become dependent to convey and defend their policies through the use of media. The media where ‘more anti-government will earn more business’ is considered a basic key to success.