2016 Worldwide Rolling Stock Manufacturers

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LMOA Maintenance Officers Association O a 75 Th Annual Meeting 2013

L M LocomotiveLMOA Maintenance Officers Association O A 75 th Annual Meeting 2013 Proceedings of the 75th Annual Meeting SEPTEMBER 30 – OCTOBER 1, 2013 Indianapolis, IN at the Indiana Convention Center FINAL MAG_2012_PLAIN_AD 8/29/13 2:34 PM Page 1 WORLDWORLD WIDEWIDE LEADERLEADER ININ LOCOMOTIVELOCOMOTIVE FUELINGFUELING && SERVICINGSERVICING EQUIPMENTEQUIPMENT EQUIPMENT CO., INC. Locomotive Fueling & Servicing Equipment Established and reliable since 1936 Am 92 eri . 46 can No Flye uge, r, Pre-War, Standard Ga You’ll Find PMC Gears and Pinions Turning the World’s Finest Locomotives. PMC doesn’t toy around. We make the full size ones! SERVING THE RAILWAY INDUSTRY SINCE 1936 o one is better qualifi ed to supply locomotive gears and pinionsN than Penn Machine. With over 90 years of manufacturing FUELING & SERVICING EQUIPMENT experience,experience, PennPenn MachineMachine makes gears and HEATED HOSE REEL CABINETS (BOOM, COLUMN, PLATFORM) pinions of the highest FULL LINE OF METERS, AIR ELIMINATORS & CONTROL,VALVES qualityqua for use on NEW & REQUALIFIED FUEL CRANES locomotivesloc from NEW & REQUALIFIED PUMP SKIDS allal the leading ELECTRIC DERAIL SYSTEMS (wireless available) manufacturers.m We WAYSIDE FUEL FILTERS manufacturema over 120 WATER TREATMENT SYSTEMS bullbull anda engine gears FULL RANGE OF NOZZLES UP TO 300 GPM andand 80 pinions.pin The most popular ones are in stock. NEW AND REQUALIFIED DROP HOSES OurOur gears and pinions are made from triple alloy steel and carburized/hardened in CUSTOM FABRICATION our in-housei h heath treatingi equipment.i TheyTh provide up to 50% longer wear life than standard FACILITY MAINTENANCE & METER PROVING heat-treated gears. And they are AAR certifi ed and come with a 5-year limited wear warranty. -

Proceedings of the 2015 Joint Rail Conference JRC2015 March23-26, 2015, San Jose, CA, USA

Proceedings of the 2015 Joint Rail Conference JRC2015 March23-26, 2015, San Jose, CA, USA DRAFT JRC2015-5621 STUDY ON IMPROVING RAIL ENERGY EFFICIENCY (E2): BEST PRACTICES AND STRATEGIES Dr. Aviva Brecher Melissa Shurland USDOT USDOT Volpe National Transportation Center Federal Railroad Administration Energy Analysis and Sustainability Washington, DC, USA Cambridge, MA, USA ABSTRACT development test and evaluation (RDT&E)on advanced A recent Volpe Center report [1] for the Federal equipment (electric and hybrid, or dual fuel locomotives), or Railroad Administration’s (FRA) Rail Energy, Environment, alternative fuels (biodiesel, CNG/LNG, Fuel cells/Hydrogen); and Engine (E3) Technology research and development participation in international rail organizations (UIC) and trade program reviewed rail industry best practices (BPs) and associations (AAR, AREMA, APTA, AASHTO), and strategies for improving energy efficiency (E2) and partnering with regional and State environmental protection environmental sustainability. The review included examples of agencies for cross-enterprise E2 and sustainability and opportunities for adoption of international transferrable improvements. BPs, and US technologies for equipment, operations and logistics software tools that have measurably improved E2 INTRODUCTION performance for passenger and freight railroads. Drivers providing renewed impetus for rail industry E2 advances Although the primary FRA mission is to preserve, include environmental compliance requirements with US enforce, and enhance rail safety, -

Best Practices and Strategies for Improving Rail Energy Efficiency

U.S. Department of Transportation Best Practices and Strategies for Federal Railroad Improving Rail Energy Efficiency Administration Office of Research and Development Washington, DC 20590 DOT/FRA/ORD-14/02 Final Report January 2014 NOTICE This document is disseminated under the sponsorship of the Department of Transportation in the interest of information exchange. The United States Government assumes no liability for its contents or use thereof. Any opinions, findings and conclusions, or recommendations expressed in this material do not necessarily reflect the views or policies of the United States Government, nor does mention of trade names, commercial products, or organizations imply endorsement by the United States Government. The United States Government assumes no liability for the content or use of the material contained in this document. NOTICE The United States Government does not endorse products or manufacturers. Trade or manufacturers’ names appear herein solely because they are considered essential to the objective of this report. REPORT DOCUMENTATION PAGE Form Approved OMB No. 0704-0188 Public reporting burden for this collection of information is estimated to average 1 hour per response, including the time for reviewing instructions, searching existing data sources, gathering and maintaining the data needed, and completing and reviewing the collection of information. Send comments regarding this burden estimate or any other aspect of this collection of information, including suggestions for reducing this burden, to Washington Headquarters Services, Directorate for Information Operations and Reports, 1215 Jefferson Davis Highway, Suite 1204, Arlington, VA 22202-4302, and to the Office of Management and Budget, Paperwork Reduction Project (0704-0188), Washington, DC 20503. -

69Th Annual Meeting

- LMOA Locomotive Maintenance Officers Association Proceedings of the 69th Annual Meeting September 13-14, 2007 Chicago Hilton & Towers 720 S. Michigan Ave. Chicago, Illinois Solutions in Motion •MM Combining exceptional service, engineering expertise and world class manufacturing to serve the rail industry's locomotive needs. Commuter Locomotives Switcher Locomotives Locomotive Overhaulsand Modernizations Locomotive Modules Cm MotivePower Contract Fleet Maintenance ^^S AWabtec company Emissions Reduction Applications Solutions In Motion www.motivepower-wabtec.com 800.272.7702 Locomotive Maintenance Officers Association 2007 ADVERTISERS INDEX LOCOMOTIVE MAINTENANCE OFFICERS ASSOCIATION AMSTED RAIL GROUP 67 BACH-SIMPSON 159 CLARK FILTER CORP 47 DUROX EQUIPMENT 141 CE TRANSPORTATION 113 GRAHAM WHITE MANUFACTURING 35 INDUSTRY SPECIALTY CHEMICALS, INC 87 KIMHOTSTART 191 LPI LIFT SYSTEMS 11 MAGNUS, LLC 53 MIBA BEARINGS, U.S 207 MOSEBACH MANUFACTURING 29 MOTIVE POWER, INC INSIDE FRONT COVER NATIONAL ELECTRICAL CARBON PRODUCTS 195 NATIONAL RAILWAY EQUIPMENT CO 17 Locomotive Maintenance Officers Association PEAKER SERVICES, INC OUTSIDE BACK COVER PENN LOCOMOTIVE GEAR INSIDE BACK COVER PREDICT 41 RAILPOWER HYBRID TECH. CORP. 131 RAIL PRODUCTS INTL. INC 165 RAILROAD FRICTION PRODUCTS 151 RAILWAY EQUIPMENT ASSOCIATES 139 SAFETY KLEEN SYSTEMS, INC 99 SIMMONS MACHINE TOOL 71 SNYDER EQUIPMENT, INC 213 TAME, INC 203 TRANSPORTATION EQUIPMENT SUPPLY CO 79 TRIANGLE ENGINEERED PRODUCTS 137 ZTR CONTROL SYSTEMS 169, 171, 173, 175, AND 177 LOCOMOTIVE MAINTENANCE OFFICERS APPRECIATES THESE 2007 SUPPORTING ADVERTISERS AMSTED RAIL GROUP MIBA BEARINGS U.S. RAILROAD FRICTION PRODUCTS BACH-SIMPSON MOSEBACH MFG. RAILWAY EQUIPMENT ASSOC. CLARK FILTER CORP. MOTIVE POWER, INC. SAFETY KLEEN SYSTEMS INC DUROX EQUIPMENT NATIONAL ELECTRICAL CARBON PROD. SIMMONS MACHINE TOOL GE TRANSPORTATION NATIONAL RAILWAY EQUIPMENT CO. -

Rolling Stock: Locomotives and Rail Cars

Rolling Stock: Locomotives and Rail Cars Industry & Trade Summary Office of Industries Publication ITS-08 March 2011 Control No. 2011001 UNITED STATES INTERNATIONAL TRADE COMMISSION Karen Laney Acting Director of Operations Michael Anderson Acting Director, Office of Industries This report was principally prepared by: Peder Andersen, Office of Industries [email protected] With supporting assistance from: Monica Reed, Office of Industries Wanda Tolson, Office of Industries Under the direction of: Deborah McNay, Acting Chief Advanced Technology and Machinery Division Cover photo: Courtesy of BNSF Railway Co. Address all communication to Secretary to the Commission United States International Trade Commission Washington, DC 20436 www.usitc.gov Preface The United States International Trade Commission (USITC) has initiated its current Industry and Trade Summary series of reports to provide information on the rapidly evolving trade and competitive situation of the thousands of products imported into and exported from the United States. Over the past 20 years, U.S. international trade in goods and services has risen by almost 350 percent, compared to an increase of 180 percent in the U.S. gross domestic product (GDP), before falling sharply in late 2008 and 2009 due to the economic downturn. During the same two decades, international supply chains have become more global and competition has increased. Each Industry and Trade Summary addresses a different commodity or industry and contains information on trends in consumption, production, and trade, as well as an analysis of factors affecting industry trends and competitiveness in domestic and foreign markets. This report on the railway rolling stock industry primarily covers the period from 2004 to 2009, and includes data for 2010 where available. -

Two for the Long Haul

ProgressiveThe Information Leader for the Railroad Industry JANUARY 2013 TWO FOR THE LONG HAUL A NEW LINE FOR Crude oil and PORTLAND'S domestic intermodal TRIMET business pose the greatest long-term EASTERN growth potential SHALES for BNSF as long as STILL A enough capacity’s GROWTH DRIVER in place OUR 14TH ANNUAL GRADE CROSSING UPDATE WEB EXCLUSIVE: Michael DePallo, the new CEO at Metrolink, cites challenges and priorities www.progressiverailroading.com/cover www.ProgressiveRailroading.com C1_PR_0113 cover.indd C1 1/3/13 11:35 AM The Secret is Coming Down the Track... POWERRAIL IS CELEBRATING 10 YEARS OF EXCELLENCE! Celebrating 10 Years of Excellence! 10 Years of Delivering Results! We would like to sincerely THANK all of our loyal customers and friends for their support over the past 10 years. Without you, we would not be who we are today - An AAR M-1003 Quality Corporation offering a full line of Locomotive Parts and Components. We are Unique Manufacturer and full-service stocking company with multiple locations throughout North America offering a full range of New or Our Proven True Blue™ Remanufactured-Unit Exchange Components. We will continue to strive to exceed your expectations, while delivering products and services that meet exemplary standards of Quality, Service, Delivery and Value! www. powerrail.com™ | 570.883.7005 FREE INFO: Circle 101 C2_PR_0113_lr PowerRail.indd C2 12/27/12 11:21 AM PROGRESSIVE RAILROADING Volume 56, No. 1 January 2013 | CONTENTS | 1 COVER STORY • PAGE 16 TWO FOR THE LONG HAUL Crude oil and domestic intermodal business pose the greatest long-term growth potential for BNSF as long as enough capacity’s in place FEATURES 14 Deconstructing the North American rail industry Short-term caution and long-term bullishness ruled at RailTrends 2012 23 Connecting the dots TriMet’s Portland-Milwaukie light-rail line will be the latest in a series of corridors linking key employment, tourist destinations Photo courtesy of BNSF Railway Co. -

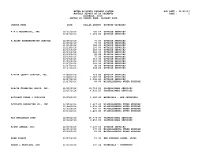

Metra Accounts Payable System Run Date : 03/16/17 Monthly Report of Ap Payments Page : 1 February, 2017 Sorted by Vendor Name, Payment Date

METRA ACCOUNTS PAYABLE SYSTEM RUN DATE : 03/16/17 MONTHLY REPORT OF AP PAYMENTS PAGE : 1 FEBRUARY, 2017 SORTED BY VENDOR NAME, PAYMENT DATE VENDOR NAME DATE DOLLAR AMOUNT EXPENSE CATEGORY A M C MECHANICAL, INC. 02/14/2017 1,902.15 MATERIALS - NON-INVENTORY 02/14/2017 968.50 OUTSIDE SERVICES 02/21/2017 111.90 MATERIALS - NON-INVENTORY 02/21/2017 9,378.24 OUTSIDE SERVICES 02/27/2017 532.00 OUTSIDE SERVICES A-ALERT EXTERMINATING SERVICE 02/14/2017 395.00 OUTSIDE SERVICES 02/15/2017 365.00 OUTSIDE SERVICES 02/16/2017 75.00 OUTSIDE SERVICES 02/16/2017 350.00 OUTSIDE SERVICES 02/28/2017 30.00 OUTSIDE SERVICES 02/28/2017 520.00 OUTSIDE SERVICES A-TIRE COUNTY SERVICE, INC. 02/13/2017 4,647.99 OUTSIDE SERVICES 02/14/2017 478.98 OUTSIDE SERVICES 02/15/2017 60.20 OUTSIDE SERVICES ABT 02/14/2017 1,079.00 MATERIALS - NON-INVENTORY 02/14/2017 115.00 MATERIALS - NON-INVENTORY 02/14/2017 193.99 MISCELLANEOUS OTHER EXPENSE ACA COMPLIANCE SERVICES, INC. 02/15/2017 11,999.00 MISCELLANEOUS OTHER EXPENSE ACE COFFEE BAR INC. 02/13/2017 276.75 MATERIALS - NON-INVENTORY ACORN GARAGE, INC. 02/13/2017 640.94 OUTSIDE SERVICES 02/13/2017 75.00 MISCELLANEOUS OTHER EXPENSE 02/14/2017 1,729.75 OUTSIDE SERVICES 02/14/2017 25.00 MISCELLANEOUS OTHER EXPENSE 02/15/2017 1,240.64 OUTSIDE SERVICES 02/15/2017 75.00 MISCELLANEOUS OTHER EXPENSE 02/16/2017 652.95 OUTSIDE SERVICES 02/16/2017 25.00 MISCELLANEOUS OTHER EXPENSE 02/21/2017 75.00 MISCELLANEOUS OTHER EXPENSE 02/27/2017 10,074.72 OUTSIDE SERVICES 02/27/2017 100.00 MISCELLANEOUS OTHER EXPENSE 02/28/2017 1,864.55 OUTSIDE SERVICES 02/28/2017 25.00 MISCELLANEOUS OTHER EXPENSE ACORN WIRE & IRON WORKS 02/13/2017 652.95 OUTSIDE SERVICES 02/13/2017 25.00 MISCELLANEOUS OTHER EXPENSE ACTON MOBILE 02/14/2017 341.00 OUTSIDE SERVICES - CAPITAL METRA ACCOUNTS PAYABLE SYSTEM RUN DATE : 03/16/17 MONTHLY REPORT OF AP PAYMENTS PAGE : 2 FEBRUARY, 2017 SORTED BY VENDOR NAME, PAYMENT DATE VENDOR NAME DATE DOLLAR AMOUNT EXPENSE CATEGORY 02/15/2017 341.00 OUTSIDE SERVICES - CAPITAL ADAM FARENCE 02/27/2017 406.82 EMP EXPENSE REIMB, LOCAL ADAMS & WESTLAKE, LTD. -

Taskload Report Outline

U.S. Department of Transportation Cost-Benefit Analysis of Alternative Fuels Federal Railroad Administration and Motive Designs Office of Research and Development Washington, DC 20590 DOT/FRA/ORD-13/21 Final Report April 2013 NOTICE This document is disseminated under the sponsorship of the Department of Transportation in the interest of information exchange. The United States Government assumes no liability for its contents or use thereof. Any opinions, findings and conclusions, or recommendations expressed in this material do not necessarily reflect the views or policies of the United States Government, nor does mention of trade names, commercial products, or organizations imply endorsement by the United States Government. The United States Government assumes no liability for the content or use of the material contained in this document. NOTICE The United States Government does not endorse products or manufacturers. Trade or manufacturers’ names appear herein solely because they are considered essential to the objective of this report. REPORT DOCUMENTATION PAGE Form Approved OMB No. 0704-0188 Public reporting burden for this collection of information is estimated to average 1 hour per response, including the time for reviewing instructions, searching existing data sources, gathering and maintaining the data needed, and completing and reviewing the collection of information. Send comments regarding this burden estimate or any other aspect of this collection of information, including suggestions for reducing this burden, to Washington Headquarters Services, Directorate for Information Operations and Reports, 1215 Jefferson Davis Highway, Suite 1204, Arlington, VA 22202-4302, and to the Office of Management and Budget, Paperwork Reduction Project (0704-0188), Washington, DC 20503. -

Potential New Locations to Use Dual-Mode Locomotives to Solve Operational Constraints

POTENTIAL NEW LOCATIONS TO USE DUAL-MODE LOCOMOTIVES TO SOLVE OPERATIONAL CONSTRAINTS A White Paper Prepared by the Locomotive Technology Task Force of the Next Generation Equipment Committee August 11, 2011 Introduction The Locomotive Technology Task Force (LTTF) was established by the PRIIA 305 Next Generation Equipment Committee’s Executive Board to investigate what advances in technology might be available to use in diesel-electric and dual mode locomotives purchased as part of the PRIIA effort. With regard to dual mode locomotives, the initial focus was on Amtrak, Metro-North Railroad and Long Island Rail Road routes serving New York City Terminals. At the present time, dual mode locomotives with a combination of diesel electric and 700vDC-third rail pickup are used. New Jersey Transit has recently taken delivery of the first of 29 diesel electric/12kV-25Hz/25kV-60Hz catenary dual mode locomotives. These are identical to the locomotives procured by Montreal’s AMT for use in Central Station and the Mount Royal tunnel. Several discussions were had among LTTF members about the expansion of dual-mode service to other locations to solve location-specific problems. This paper contains a summary of those locations, and the possible needs/benefits dual mode motive power might provide. Potential Locations This discussion focused on what “non-traditional” locations or services for which a dual mode locomotive could be used. Some of these had been mentioned during the May 18 call. 1. South Station, Boston. Amtrak’s Northeast Corridor NEC) service is all- electric; the Lake Shore Limited uses diesel locomotives. The MBTA’s extensive commuter rail service uses only diesel locomotives, and the authority is forced to halt its commuter trains several car lengths from the end of track to prevent diesel engines from idling underneath the bus station built 15 years ago over the station tracks. -

Progress Rail Services Corporation

Board Summary Progress Rail Services Corporation Date: November 16, 2017 1600 Progress Drive, Albertville, AL 85950 Main Location: Carson City Joshua Johnson, Director of Operational Excellence Manufacturing Business Type: New County: Clark County Development Authority Representative: Michael Walsh, LVGEA APPLICATION HIGHLIGHTS - Progress Rail Services Corporation has leased a 130,000 square foot manufacturing facility in Henderson, NV. The company expects the facility to be operational in the fall of 2017. - While some employees will relocate from the company's other facilities, it is anticipated the majority of the Henderson facility staff will be local hires. - The company is the world's largest builder of diesel-electric locomotives for all commercial railroad applications. PROFILE Progress Rail Services Corporation, a wholly owned subsidiary of Caterpillar since 2006, is a supplier of railroad and transit system products and services headquartered in Albertville, Alabama. The company offers advanced Electro-Motive Diesel (EMD) locomotives and engines, railcars, trackwork, fasteners, signaling, rail welding and Kershaw Maintenance-of-Way equipment, along with dedicated locomotive and freight car repair. The company also offers advanced rail technologies, including data acquisition and asset protection equipment. The company's Henderson facility will remanufacture traction motors for the rail industry. Progress Rail Services Corporation operates a network of nearly 200 locations across the United States, Canada, Mexico, Brazil, Germany, Italy, Australia, China, Germany, India, South Africa, the United Arab Emirates, and the United Kingdom. Source: Progress Rail Services Corporation SIGNIFICANCE OF ABATEMENTS IN THE COMPANY'S DECISION TO RELOCATE/EXPAND Progress Rail Services Corporation selected Henderson out of numerous potential cities. The company reviewed each city's economic climate, proximity to its main customers, utility rates, labor and property costs, highway accessibility, and incentives packages as points of comparison. -

10/21/16 Monthly Report of Ap Payments Page : 1 September, 2016 Sorted by Vendor Name, Payment Date

METRA ACCOUNTS PAYABLE SYSTEM RUN DATE : 10/21/16 MONTHLY REPORT OF AP PAYMENTS PAGE : 1 SEPTEMBER, 2016 SORTED BY VENDOR NAME, PAYMENT DATE VENDOR NAME DATE DOLLAR AMOUNT EXPENSE CATEGORY A M C MECHANICAL, INC. 09/12/2016 1,528.45 OUTSIDE SERVICES A-ALERT EXTERMINATING SERVICE 09/08/2016 45.00 OUTSIDE SERVICES 09/12/2016 225.00 OUTSIDE SERVICES 09/12/2016 180.00 OUTSIDE SERVICES 09/12/2016 115.00 OUTSIDE SERVICES 09/12/2016 685.00 OUTSIDE SERVICES 09/19/2016 75.00 OUTSIDE SERVICES 09/19/2016 190.00 OUTSIDE SERVICES 09/29/2016 775.00 OUTSIDE SERVICES A-TIRE COUNTY SERVICE, INC. 09/12/2016 330.00 OUTSIDE SERVICES 09/12/2016 4,179.70 OUTSIDE SERVICES A-1 EQUIPMENT SALES 09/12/2016 1,155.16 OUTSIDE SERVICES ABT 09/08/2016 367.98 MISCELLANEOUS OTHER EXPENSE ACCENTURE LLP 09/08/2016 136,972.50 OUTSIDE SERVICES 09/08/2016 1,500.00 OUTSIDE SERVICES 09/08/2016 1,900.85 OUTSIDE SERVICES 09/19/2016 87,371.00 OUTSIDE SERVICES ACCURATE FORMS & SUPPLIES 09/08/2016 4,820.20 MATERIALS - NON-INVENTORY 09/19/2016 1,348.60 MATERIALS - NON-INVENTORY ACCURATE REPORTING CO., INC. 09/06/2016 3,291.70 MISCELLANEOUS OTHER EXPENSE ACE BAKERY 09/12/2016 190.00 MISCELLANEOUS OTHER EXPENSE 09/12/2016 2,684.00 MISCELLANEOUS OTHER EXPENSE ACE COFFEE BAR INC. 09/29/2016 220.75 MATERIALS - NON-INVENTORY ACORN GARAGE, INC. 09/12/2016 11,221.67 OUTSIDE SERVICES 09/12/2016 724.00 MISCELLANEOUS OTHER EXPENSE 09/19/2016 25.00 MISCELLANEOUS OTHER EXPENSE ADAM FARENCE 09/21/2016 649.62 EMP EXPENSE REIMB, LOCAL METRA ACCOUNTS PAYABLE SYSTEM RUN DATE : 10/21/16 MONTHLY REPORT OF AP PAYMENTS PAGE : 2 SEPTEMBER, 2016 SORTED BY VENDOR NAME, PAYMENT DATE VENDOR NAME DATE DOLLAR AMOUNT EXPENSE CATEGORY ADAM GIBSON 09/01/2016 12.10 EMP EXPENSE REIMB, LOCAL ADAM SINGER 09/06/2016 35.15 EMP EXPENSE REIMB, LOCAL ADAMS & WESTLAKE, LTD. -

Metra Accounts Payable System Run Date : 01/25/17 Monthly Report of Ap Payments Page : 1 December, 2016 Sorted by Vendor Name, Payment Date

METRA ACCOUNTS PAYABLE SYSTEM RUN DATE : 01/25/17 MONTHLY REPORT OF AP PAYMENTS PAGE : 1 DECEMBER, 2016 SORTED BY VENDOR NAME, PAYMENT DATE VENDOR NAME DATE DOLLAR AMOUNT EXPENSE CATEGORY A M C MECHANICAL, INC. 12/15/2016 720.64 OUTSIDE SERVICES 12/27/2016 1,493.00 OUTSIDE SERVICES A-ALERT EXTERMINATING SERVICE 12/05/2016 75.00 OUTSIDE SERVICES 12/05/2016 75.00 OUTSIDE SERVICES 12/05/2016 780.00 OUTSIDE SERVICES 12/13/2016 150.00 OUTSIDE SERVICES 12/13/2016 105.00 OUTSIDE SERVICES 12/13/2016 680.00 OUTSIDE SERVICES 12/19/2016 45.00 OUTSIDE SERVICES 12/19/2016 75.00 OUTSIDE SERVICES 12/19/2016 115.00 OUTSIDE SERVICES 12/19/2016 225.00 OUTSIDE SERVICES 12/27/2016 150.00 OUTSIDE SERVICES 12/27/2016 30.00 OUTSIDE SERVICES 12/27/2016 408.00 OUTSIDE SERVICES A-TIRE COUNTY SERVICE, INC. 12/08/2016 210.00 OUTSIDE SERVICES 12/08/2016 1,262.94 OUTSIDE SERVICES 12/27/2016 1,502.20 OUTSIDE SERVICES 12/27/2016 46.00 MISCELLANEOUS OTHER EXPENSE ACACIA FINANCIAL GROUP, INC. 12/05/2016 19,756.25 PROFESSIONAL SERVICES 12/15/2016 6,931.25 PROFESSIONAL SERVICES ACCURATE FORMS & SUPPLIES 12/19/2016 1,646.00 MATERIALS - NON-INVENTORY ACCURATE REPORTING CO., INC. 12/05/2016 1,217.65 MISCELLANEOUS OTHER EXPENSE 12/08/2016 5,029.90 MISCELLANEOUS OTHER EXPENSE 12/12/2016 497.45 MISCELLANEOUS OTHER EXPENSE 12/13/2016 3,825.90 MISCELLANEOUS OTHER EXPENSE ACI WORLDWIDE CORP. 12/08/2016 24,774.00 PROFESSIONAL SERVICES 12/12/2016 9,855.00 PROFESSIONAL SERVICES ACORN GARAGE, INC.